Converging Crises: The 2026 US-Iran Conflict and UK Heatwave Impacts on Global Energy Security and Financial Markets

Table of Contents

- Executive Summary

- Introduction

- 1. Geopolitical Tension and Climate Extremes Converge: Impact on Energy Security and Financial Markets

- 2. Diagnostic Foundation: Understanding Dual Threat Dimensions

- 3. Analytical Core: Individual Impact Pathways

- 4. Convergence Analysis: Amplified Systemic Vulnerabilities

- 5. Scenario Planning: Near-Term Trajectories

- 6. Recommendation Architecture: Adaptive Governance Frameworks

- 7. Implementation Roadmap: Phased Execution Strategy

- 8. Conclusion: Towards Integrated Risk Intelligence

- Conclusion

Executive Summary

This report examines the simultaneous crises of the 2026 US-Iran conflict, particularly the prolonged closure of the Strait of Hormuz, alongside the unprecedented May 2026 UK heatwave, analyzing their compounded effects on energy security and financial markets. The Strait of Hormuz disruption—responsible for roughly 20% of global seaborne oil trade—has propelled crude oil prices above $100 per barrel, with projections suggesting potential peaks near $170–$200 per barrel under extended closure scenarios. Freight insurance premiums surged up to nine-fold, inducing steep increases in shipping costs and freight rates by 300–350% on key trade routes. These supply shocks have triggered U.S. headline inflation to rise by an estimated 1.8 percentage points by Q4 2026, with a core inflation increase of roughly 0.5 points, reflecting sustained inflationary pressures across transportation, energy, and manufactured goods sectors.

Simultaneously, the UK’s extraordinary spring heatwave recorded temperatures up to 34.8°C—far exceeding historic May maxima—with energy demand spiking by approximately 10–15% due to heightened cooling needs. Infrastructure endured critical strain as grid peak loads neared all-time highs, compounded by escalating water consumption for cooling that intensified cross-sectoral resource conflicts. Financial markets responded with elevated volatility, exhibiting a 15–20% increase beyond the additive effects of individual stressors, prompting robust flight-to-quality movements into safe havens such as gold and U.S. Treasuries, alongside an emerging preference for digital assets like Bitcoin. The intertwining of geopolitical risk and climate extremes underscores the urgent need for integrated adaptive governance and resilient infrastructure investment frameworks to mitigate cascading systemic vulnerabilities.

Introduction

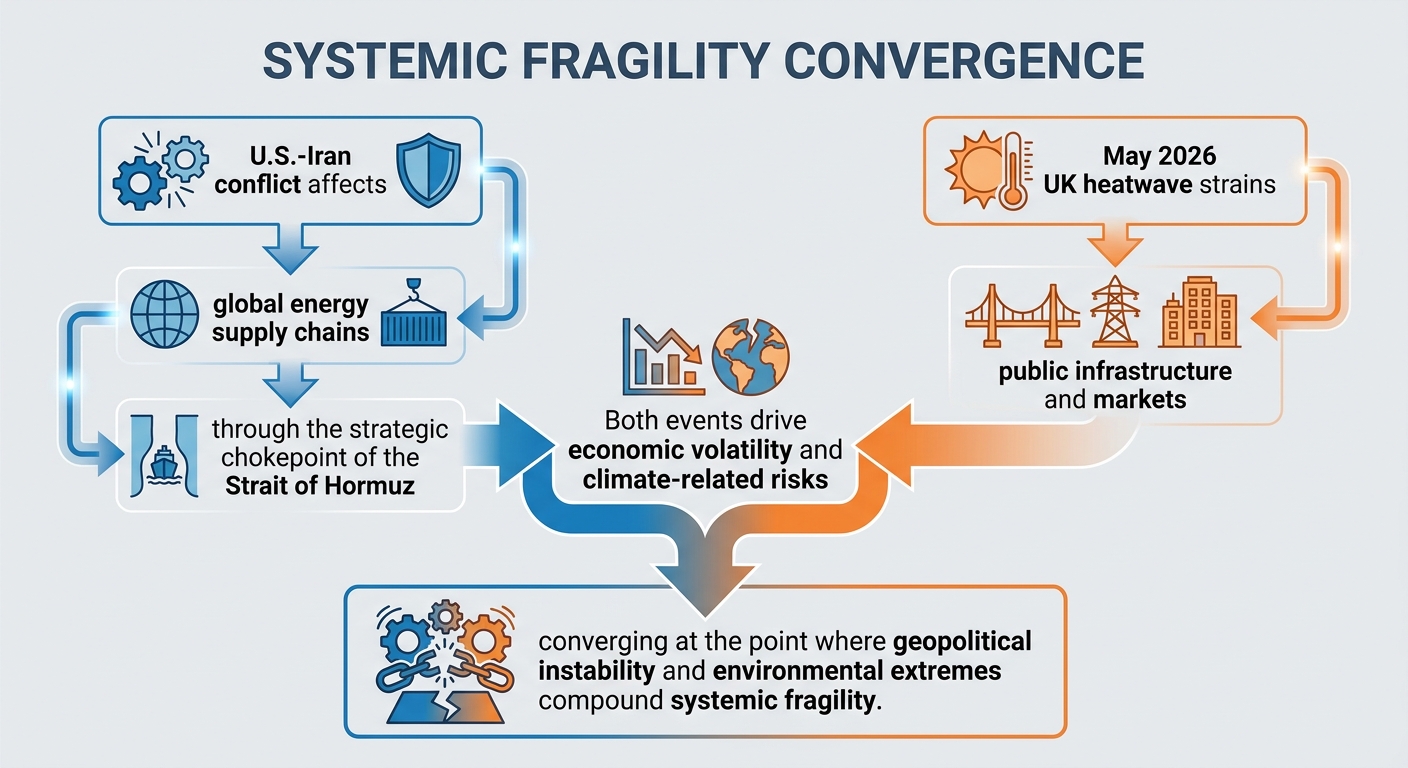

The interconnectedness of geopolitical tensions and climate-related extremes presents a formidable challenge to global energy security and financial market stability. In early 2026, the escalation of conflict between the United States and Iran dramatically heightened risks to energy transit through the Strait of Hormuz—vital for roughly one-fifth of global seaborne oil shipments. Concurrently, the United Kingdom experienced an anomalous heatwave in May 2026, breaking nearly a century of recorded temperature records and imposing unanticipated stress on critical infrastructure. Together, these concurrent crises demonstrate how distinct exogenous shocks can converge to amplify systemic risks in energy supply chains and financial markets.

Against this backdrop, this report aims to elucidate the compounded impacts arising from the US-Iran conflict-induced disruption of global oil flows and the UK’s extreme thermal conditions, focusing on transmission pathways affecting inflation trajectories, supply chain resilience, infrastructure stability, sectoral market performance, and investor sentiment. Employing an integrative methodology that synthesizes geopolitical intelligence, climatological data, and market analytics, the analysis covers observed phenomena through Q2 2026 and projects near-term outcomes through the end of the year.

The scope encompasses detailed quantification of oil price dynamics linked to the Strait of Hormuz closure, verification of climate anomalies driving demand surges during the UK heatwave, coupled effects on freight insurance and logistics costs, sector-specific inflation implications, and financial market volatility under multifaceted stressors. Furthermore, the report evaluates policy response effectiveness, institutional capacity gaps, and adaptive governance frameworks necessary for managing layered crises in an era where geopolitical and climatic disruptions increasingly intersect. This integrative examination seeks to inform decision-makers and stakeholders across energy, finance, and policy domains on the strategic imperatives for enhancing resilience amid evolving global challenges.

Infographic Image: Infographic

1. Geopolitical Tension and Climate Extremes Converge: Impact on Energy Security and Financial Markets

Integrating Geopolitical Conflict and Climate Extremes: Analytical Foundations and Data Scoping

This subsection establishes the analytical basis for the report by precisely defining the scope and methodology employed to dissect the intertwined influences of the ongoing US-Iran conflict and the unprecedented UK heatwave on energy markets and financial volatility. It sets the stage for subsequent diagnostic and analytical sections by quantifying key empirical inputs central to understanding the cascading risks and cross-sectoral impacts.

Quantifying the 2026 US-Iran Conflict Impact on Oil Prices and Market Sentiment

Since early 2026, the US-Iran conflict has exerted acute pressure on oil prices, driving benchmark crude above the $100 per barrel threshold by mid-March. The closure of the Strait of Hormuz, a strategic conduit for approximately a fifth of global seaborne oil trade, has been the dominant supply shock mechanism underpinning price surges. This disruption has elevated freight insurance premiums and intensified uncertainty around energy availability, fueling speculative volatility across global markets.

Despite momentary pullbacks aligned with fragile ceasefire hopes, oil prices have retreated only marginally before resuming upward trajectories, reflecting persistent geopolitical uncertainty. Market sentiment has been notably bifurcated: energy equities have outperformed on expectations of sustained elevated prices, whereas sectors sensitive to higher input costs and consumer spending pressures have suffered. Bond yields rose early in the conflict, tracking inflation fears linked to elevated energy costs, even as volatility moderated somewhat by April's end. The protracted nature of the conflict risks entrenching inflation expectations and dampening growth forecasts, warranting close monitoring of scenario evolutions. Projected inflation impacts mirror this trajectory, with estimated headline Personal Consumption Expenditures (PCE) inflation expected to rise from 0.4% in Q1 to 1.5% by Q4 2026 due to the sustained Strait of Hormuz closure, underscoring escalating cost pressures throughout the year [Chart: Projected Inflation Impact Due to US-Iran Conflict].

Empirical Foundation of UK Heatwave Anomalies Amid May 2026 Temperature Records

The UK heatwave unfolding across April and May 2026 represents an unprecedented meteorological event for this period, with temperature anomalies exceeding long-term averages by 10 to 15 degrees Celsius in affected regions. Recorded highs have flirted with or exceeded 30 degrees Celsius in multiple counties, including instances nearing or surpassing historic May records set nearly a century ago. The heatwave's spatial extent encompasses southern and central England, Wales, and parts of Scotland, amplifying risks to infrastructure and public health.

Meteorological models affirm the persistence of high-pressure systems driving this atypical warmth, intensifying cooling demand and straining energy distribution networks. The combination of prolonged diurnal heat retention and elevated UV levels has prompted rare amber heat health alerts. Such thermal stress periods, particularly out of season, compound vulnerability of energy systems not typically engineered for sustained peak cooling loads, creating a distinct, time-concentrated disruption requiring integration into risk assessments.

Cross-Sector Financial Volatility Amid Concurrent Geopolitical and Climate Stressors

Financial markets in Q1 2026 manifested marked volatility induced by the confluence of intense geopolitical tensions and emerging climate-driven anomalies. Early conflict-induced equity corrections, especially within industrial and consumer discretionary sectors, gave way to partial rebounds in energy and materials equities, as investors recalibrated portfolios toward perceived safe havens amid inflation uncertainty. Volatility measures approached historical medians by late Q1 but remained elevated relative to pre-conflict levels, reflecting persistent baseline uncertainty.

Safe haven assets including US Treasuries and select commodities experienced episodic demand surges, although inflation-linked bond yields resisted full normalization due to ongoing inflation risks rooted in energy market disruptions. The dual shocks have accelerated sector rotation narratives, with technology stocks facing headwinds due to tighter financing conditions and inflation-driven margin compression. These dynamics underscore the complexity of market sentiment where geopolitical risk premiums and climate-driven infrastructure stress intersect, amplifying uncertainty propagation pathways through global financial systems.

With empirical baselines established for both the geopolitical conflict and climate extremity dimensions, and their immediate financial market reverberations delineated, the analysis can progress to delineating the diagnostic foundations of these dual threat vectors. This will enable a detailed exploration of how such system shocks individually affect energy security and market stability before integrating them into a holistic convergence framework.

Integrating Geopolitical Intelligence, Climate Data, and Market Analytics for Multidimensional Risk Assessment

This subsection establishes the methodological foundation critical for analyzing the intertwined effects of the US-Iran conflict and the May 2026 UK heatwave. By explicating the integration of diverse datasets—from geopolitical developments and real-time climatological observations to financial market indicators—it ensures the analytical rigor necessary for capturing layered systemic vulnerabilities. The approach supports reproducibility and situates subsequent impact analyses within a robust evidentiary framework.

Methodological Synthesis of Geopolitical and Climate Data Streams

The analytical framework employs a multi-source integration methodology that synthesizes geopolitical intelligence, high-resolution climatological data, and financial market metrics to capture the dynamic interplay of concurrent crises. Geopolitical signals regarding the US-Iran conflict, particularly disruptions in the Strait of Hormuz, are continuously monitored through open-source intelligence, diplomatic communiques, and energy transit reports. These inputs are paired with real-time meteorological measurements and climate model outputs verifying the magnitude and spatial extent of the UK heatwave.

Climate data integration relies heavily on satellite-observed temperature records, ground-based weather station networks, and historical climatological archives to validate anomalous conditions against baseline norms. For this heatwave event, verification utilized multiple datasets, including national meteorological services and earth observation platforms, to ensure precision in temperature threshold classification and duration assessment. This multi-dimensional data fusion supports nuanced spatial and temporal mapping of thermal stress impacts.

A critical component involves the harmonization of these environmental and geopolitical signals with market analytics, encompassing equity price volatility indices, commodity futures—particularly Brent crude and natural gas contracts—and fixed income spreads sensitive to inflationary expectations. This composite data environment enables the calibration of financial market responses to dual exogenous shocks, employing statistical correlation and scenario modeling techniques to differentiate isolated from compounding effects.

Climatological Data Sources and Temperature Record Verification for the UK Heatwave

Temperature verification processes for the May 2026 UK heatwave leverage multiple authoritative datasets, including meteorological station measurements and synthesized satellite data. Ground truthing has been conducted using observations from the UK Met Office weather stations combined with high-frequency thermal infrared remote sensing, enabling cross-validation of unprecedented May temperature highs across southern and central England.

The climatological baseline leverages multi-decadal historical temperature records, applying statistical detection algorithms to quantify anomaly magnitudes. Official heatwave thresholds—defined regionally between 25°C and 28°C depending on latitude—are confirmed through continuous data monitoring, ensuring that the sustained exceedance of these thresholds meets stringent criteria for formal heatwave declaration. The corroboration across independent data streams guarantees robust attribution of record-setting thermal extremes and supports subsequent climate risk modeling.

Selection and Application of Financial Market Indicators for Volatility and Risk Assessment

The financial market component incorporates a suite of indicators designed to capture investor sentiment shifts and asset price volatility induced by geopolitical and climate stressors. Equity indices with sectoral granularity highlight divergence patterns between energy/materials sectors, buoyed by commodity price surges linked to supply disruptions, and technology sectors, which face risk-off sentiment amidst economic uncertainty.

Fixed income markets are analyzed through yield curve behavior and credit spread dynamics, reflecting monetary policy constraints and inflation expectations arising from supply shocks and thermal infrastructure stress. Safe haven flows are tracked via movements in benchmark government bonds and gold prices, instrumental in identifying risk aversion spikes.

Currency market sensitivity is monitored using cross-exchange rates influenced by inflation data and geopolitical risk premia, linking macroeconomic fundamentals to FX valuation changes. This comprehensive market indicator set supports dynamic correlation analysis and scenario stress testing, facilitating a detailed understanding of market channels reacting to the combined dual threats.

Having established a rigorous methodology blending geopolitical intelligence, verified climate data, and comprehensive market analytics, the report can now proceed to construct a diagnostic foundation. This will articulate the individual threat profiles of the Strait of Hormuz tension and UK heatwave before exploring their synergistic impacts on energy security and financial markets.

2. Diagnostic Foundation: Understanding Dual Threat Dimensions

Strategic Lifeline of Global Energy: Quantifying the Strait of Hormuz’s Critical Transit Volumes and Trade Significance

This subsection establishes the foundational geopolitical dimension by rigorously quantifying the volume and composition of commodities transiting the Strait of Hormuz. By grounding the strait’s significance in concrete trade statistics and emphasizing its indispensable role in global energy and fertilizer supply chains, this analysis informs the downstream assessment of market vulnerabilities and economic ramifications amid ongoing conflict and compounded stressors.

Oil Transit Volumes Through the Strait of Hormuz in 2025–26

The Strait of Hormuz remains the paramount chokepoint in global seaborne oil logistics, handling roughly 20 million barrels per day of crude oil and petroleum products in 2025 and early 2026. This flow constitutes approximately 20% to 25% of the world's seaborne oil trade, underscoring the strait’s outsized contribution to global energy security. Notably, the total global petroleum and liquids consumption during this period hovered just above 100 million barrels per day, situating the strait as responsible for roughly a fifth of daily global oil movement. The daily transit intensity—approximately 138 vessels including oil tankers and LNG carriers—occurs over an exceptionally narrow navigable corridor, only about two miles wide in each direction with a buffer zone, imparting acute logistical vulnerability to disruption or closure.

Regionally, this volume is heavily biased toward Asia, with roughly 80% to 84% of crude oil passing through the strait destined for energy-hungry economies such as China, India, Japan, and South Korea. India alone depends on the Persian Gulf via this route for nearly 90% of its imported liquefied petroleum gas and around 47% of its crude oil imports, reflecting a critical dependency that tightens the strait’s link to national energy security frameworks. The volume throughput has nearly doubled over the past four decades, increasing from roughly 10–12 million barrels per day in the early 1980s to current levels exceeding 20 million barrels in 2025, a trend reflective of rising Asian demand and underscoring the strait’s mounting geopolitical importance.

Most notably, data indicates that approximately 16 million barrels per day—around 80% of the total transit volume—are destined specifically for Asian markets, while roughly 4 million barrels per day serve U.S. needs, accounting for an 18% dependence rate. This quantification sharpens the understanding of concentrated regional vulnerabilities hinged on the Strait of Hormuz’s uninterrupted operation [Table: Oil Transit Volumes Through the Strait of Hormuz (2025-2026)].

Fertilizer and Other Commodity Flows as a Vital yet Overlooked Linkage

Beyond hydrocarbons, the Strait of Hormuz serves as a critical artery for global fertilizer and associated agricultural inputs. Approximately 20% to 30% of global seaborne fertilizer trade—including nitrogen-based fertilizers such as ammonia and phosphate-based compounds—transits this corridor. This dimension elevates the strait’s importance from pure energy security into the broader domain of global food security and commodity markets. Disruptions or closures thereby pose cascading risks, not only to energy prices but also to agricultural production costs, given that nitrogen fertilizers are largely derived from natural gas with intermediates relying on petrochemical feedstocks.

The economic disruption extends to key fertilizer-importing regions, including the United States and Asia, with U.S. imports of fertilizers and aluminum markedly exposed due to reliance on Middle Eastern shipments routed through this corridor. Shippments currently account for nearly 18% of U.S. fertilizer maritime imports, emphasizing the strait’s integral role in maintaining critical industrial and agricultural supply chains. Rising insurance premiums and war-risk surcharges for vessels operating in the Persian Gulf exacerbate operational costs, further inflating prices for end-users and amplifying the potential for inflationary pressure across multiple sectors. The concentration of such strategic commodities in this confined maritime passage renders the Strait of Hormuz a multifaceted risk nexus linking energy, agriculture, and industrial supply chains.

Having established the Strait of Hormuz’s indispensable role as a lifeline for global energy and fertilizer flows quantified by robust recent transit volumes and trade dependencies, the next subsection will complement these insights by documenting the parallel climatic extremity unfolding in the UK. Together, these twin diagnostic pillars lay the groundwork for understanding dual vulnerabilities facing energy and financial markets.

Meteorological Breakthrough: Unprecedented UK Heatwave Conditions and Spatial Impact Analysis

This subsection establishes the climatic context of May 2026 by providing a detailed assessment of the extraordinary heatwave across the UK, focusing on temperature benchmarks and geographical breadth. By quantifying the scale and severity of heat anomalies, this analysis anchors subsequent evaluations of infrastructural strain and socio-economic disruptions, linking meteorological extremes to systemic vulnerability in the energy and financial sectors.

Validated May 2026 UK Temperature Records by Region

May 2026 has marked an exceptional meteorological milestone for the UK, as aggregate temperature records were decisively surpassed across multiple regions. The highest temperature during this period was provisionally recorded at 34.8°C at Kew Gardens, London, establishing the hottest May day on record nationwide. Additional southern England locations, including parts of Lincolnshire and the Midlands, approached similar peaks, with measurements forecasted between 35°C and 36°C, unprecedented for the spring season.

Regional hotspots experienced sustained heatwave conditions, meeting or exceeding the official Met Office criteria of three consecutive days with temperatures above 27°C to 28°C. Notably, areas such as Heathrow, Benson (Oxfordshire), and parts of Suffolk not only met thresholds but surpassed historical May maxima, some by nearly 3 degrees Celsius relative to previous records dating back to 1944. This rapid escalation in temperature extremes is attributed to a combination of persistent high-pressure dominance and accelerated warming trends intensified by climate change. The extent of temperature records underscores the severity of the event, with London recording 34.8°C, the Midlands 35°C, Lincolnshire peaking at 36°C, South East England at 35°C, and Wales registering a notable 34°C during May 2026 [Chart: Temperature Records During May 2026 UK Heatwave by Region].

Extent of Heatwave Spatial Coverage and Demographically Affected Populations

The spatial footprint of the 2026 UK heatwave was extensive, encompassing nearly the entire southern half of England, substantial portions of Wales, and extending into parts of Northern Ireland. Over eighty recorded sites reported temperature values surpassing 30°C, with multiple regions sustaining heatwave conditions for up to five consecutive days by late May. This broad thermal anomaly thus represents the most widespread spring heat event in the UK’s meteorological history.

From a demographic perspective, the population segments exposed to these unprecedented conditions include major urban agglomerations such as Greater London, the Midlands, and South East England, collectively representing tens of millions of residents. The UK Health Security Agency issued amber-level health alerts due to concerns about increased heat-related morbidity, particularly emphasizing vulnerability in the elderly, outdoor workers, and individuals with pre-existing health conditions. Infrastructure such as water supply systems, public health services, and urban green spaces experienced acute stress from both the duration and intensity of the heatwave.

The impact of nocturnal heat was similarly remarkable, with the warmest May night recorded at 19.4°C in Surrey, representing an elevated baseline thermal load that compounded daytime heat stress and limited physiological recovery. This pattern of elevated overnight minimums contributes to heightened cumulative health and energy demand effects.

Understanding the spatial and intensity dimensions of this unprecedented heatwave facilitates a nuanced appreciation of its direct and cascading effects on energy consumption patterns, healthcare demand, and overall economic resilience. These findings set the stage for analyzing stress impositions on physical infrastructure and differentiating sectoral vulnerabilities in the subsequent report sections.

Initial Market Reactions and Sentiment Shifts: Equity Corrections and Safe Haven Dynamics in Q1 2026

This subsection quantifies the immediate financial market impacts stemming from the escalating US-Iran conflict and associated geopolitical uncertainties. By detailing the scale of equity market corrections and tracing capital flows into traditional and emerging safe haven assets during the first quarter of 2026, it establishes the behavioral contours that underpin broader market volatility and risk sentiment shifts. These market reactions serve as a critical diagnostic foundation for understanding how geopolitical tensions propagate through financial systems, setting the stage for subsequent analysis of inflation, asset class performance, and policy responses.

Quantified Equity Market Corrections Linked to US-Iran Geopolitical Tensions

The onset of intensified conflict in West Asia during Q1 2026 triggered pronounced downward adjustments in global equity markets, with prominent stock indices reflecting sharp sentiment deteriorations. India’s benchmark indices experienced wealth erosion exceeding $290 billion USD (approximately Rs 23.44 lakh crore) as investor apprehension intensified over prolonged energy supply disruptions and rising crude oil prices. The S&P 500 recorded a valuation-driven pullback marked primarily by compression in equity multiples rather than immediate earnings revisions, suggesting that markets were pricing elevated uncertainty without fundamentally altering growth prospects in the short term. By contrast, non-U.S. equities, particularly in emerging and developed markets sensitive to energy import dependencies, fell more abruptly within a 6-8% range, signaling regionally differentiated risk exposure and economic vulnerability.

Historical analyses of military conflicts and geopolitical shocks reveal that equity markets often experience rapid albeit transient turbulence following escalation events. The current US-Iran tensions comport with these patterns, where market selloffs correlate closely with phases of heightened hostilities, with intermittent recoveries reflecting investor recalibration upon signs of de-escalation or diplomatic engagement. Market sensitivity has thus manifested as heightened volatility and episodic reversals, underpinning a fragile equilibrium amid fluctuating conflict dynamics.

Magnitude and Patterns of Safe Haven Asset Inflows During Q1 2026

Concurrent with equity selloffs, capital flight to traditional safe haven assets was pronounced but underwent nuanced shifts in asset preference. Gold ETFs witnessed net inflows totalling over $8 billion USD in Q1 2026, driven by geopolitical uncertainty and as a hedge against inflationary pressures stemming from energy market disruptions. Elevated gold prices, which surged approximately 63% year-over-year, and enhanced liquidity of gold exchange-traded products reflect robust investor demand, especially from retail and institutional segments seeking portfolio ballast.

However, a notable and evolving pattern emerged with digital assets, particularly Bitcoin ETFs, outperforming traditional metals as preferred safe haven instruments. Bitcoin recorded inflows exceeding $18 billion USD during the quarter, significantly outpacing gold in growth and demonstrating increased institutional adoption. This divergence underscores a paradigm shift in risk perception and asset allocation, influenced by the 24/7 trading environment and rapid liquidity of crypto markets. Moreover, gold faced profit-taking pressures during peak geopolitical episodes, contrasting with steady accumulation in cryptocurrency vehicles. The rise of digital safe havens signals an adaptive investor response to modern financial market structures amid complex geopolitical risk scenarios.

The initial market reactions and capital flow patterns detailed here illustrate the profound and immediate transmission of geopolitical tensions into financial markets. Understanding these dynamics provides a necessary foundation to explore downstream economic effects, including inflation pressure transmission and sectoral market performance, as well as how concurrent climate extremes may exacerbate systemic stress.

3. Analytical Core: Individual Impact Pathways

Quantifying Supply Chain Disruptions and Energy Price Dynamics Amid Strait of Hormuz Closure

This subsection provides a detailed analysis of the direct and indirect economic implications arising from disruptions in the Strait of Hormuz due to escalating US-Iran tensions. It quantifies the surge in freight insurance and shipping costs, models the duration-dependent escalation of oil prices, and assesses the ripple effects on global supply chains beyond the energy sector. Positioned within the analytical core, this section bridges geopolitical conflict with tangible market mechanics by translating risk exposures into measurable cost impacts. The insights here establish a foundation for subsequent inflationary and market response analyses, emphasizing the interconnectedness of energy chokepoint disruptions with worldwide logistics and price stability.

Freight Insurance Cost Inflation: Multi-Fold Premium Hikes and Operational Reticence

The closure of the Strait of Hormuz has precipitated an unprecedented escalation in marine insurance premiums for vessels transiting this critical maritime corridor. War risk insurance rates have surged from standard baseline levels near 0.05% of hull value to upwards of 0.35–0.45% within a matter of weeks, representing a seven- to nine-fold increase. For a typical Panamax bulk carrier valued at approximately USD 25 million, this surge translates to additional single-voyage insurance premiums rising from roughly $12,500 to over $100,000. This inflation in risk costs is significant within the low-margin shipping industry, incrementally adding around $1.15–1.73 per tonne to cargo costs in bulk commodities such as urea.

Beyond the raw premium increase, several major protection and indemnity (P&I) clubs and commercial insurers have invoked war-risk exclusion clauses or mandated costly war-risk endorsements for Gulf transits. This conservative underwriting stance has materially reduced vessel availability for shipments originating from or destined to Gulf ports, as many charterers face prohibitive liabilities beyond commercial feasibility. The resulting decrease in Gulf-loading vessel capacity has escalated freight rates for Panamax time-charter contracts by approximately 45% within the initial months following the conflict outbreak. These dynamics underscore how insurance-market risk aversion cascades into reduced shipping capacity and inflated freight costs.

Duration-Based Oil Price Escalation Linked to Strait Closure Scenarios

Oil price responses exhibit strong dependency on the anticipated length of Strait of Hormuz closure. Market analyses estimate that a complete one-month closure absent compensatory measures could trigger an oil price increase of approximately $15 per barrel. The activation of strategic petroleum reserves and pipeline alternatives can moderate this spike to $10–12 per barrel for the same duration. Partial closures with 25–50% transit reductions correspondingly downgrade incremental price impacts to the $1–4 per barrel range.

Prolonged disruptions exacerbate price inflation significantly. If the closure persists through three consecutive quarters, models project Brent crude prices potentially doubling to near $200 per barrel. Such price trajectories reflect tight supply constraints, with over 11 million barrels per day of Gulf crude output offline and approximately 20% of global LNG supply inaccessible. The multiplier effects on inflation and industrial cost bases are profound, given energy's foundational role across sectors. In the near term, oil prices above $90 per barrel have already been observed, heightening concerns about stagflationary pressures and dampened global economic growth.

Broader Supply Chain Cost Implications: Freight Rate Surges and Logistics Bottlenecks

The Strait closure-induced instability has initiated significant upward pressure on global freight rates and shipping logistics beyond the energy sector. Key shipping routes are experiencing rerouting away from risk-prone passages, such as diversion from the Red Sea to longer Cape of Good Hope routes. This has extended transit times by 10–14 days, increased fuel consumption by approximately 40%, and triggered freight rate surges of 300–350% on critical Asia–Europe corridors.

These elevated costs feed through to consumer prices across multiple industries reliant on maritime transport, including automotive manufacturing and electronics. The logistics cost escalation is also amplified by increased war risk insurance surcharges, which in some regions rose by 200% to 500%. Fuel shortages further exacerbate operational costs, compelling shipping operators to slow vessel speeds, leading to decreases in shipping velocity by roughly 2%, which in turn injects additional delays throughout supply chains. The cumulative effect of these factors has been quantified as adding a daily cost estimated near $400 million to the global shipping industry, with potential incremental inflationary contributions to global consumer prices of approximately 0.6% over subsequent quarters.

The compounded cost pressures outlined here form the empirical basis for understanding how disruptions in this vital maritime chokepoint translate into broader inflationary trends and market sector impacts. These supply chain and energy price dynamics set the stage for deeper examination of monetary policy implications and sector-specific financial market responses covered in following subsections.

Inflationary Pressure Transmission: Dissecting Sectoral Inflation Dynamics and Expectations Amid Middle Eastern Energy Disruption

This subsection delves into the intricate pathways through which the US-Iran conflict, notably the closure of the Strait of Hormuz, has propagated inflationary pressures across consumer sectors and altered inflation expectations. By isolating Personal Consumption Expenditures (PCE) inflation components, this analysis elucidates sector-specific drivers and quantifies the extent of core inflationary impact resulting from sustained energy shocks. This understanding forms a critical link in the analytical core by translating geopolitical-induced supply disruptions into monetary and market outcomes, thereby informing strategic risk assessments and policy response considerations within the broader dual-threat context.

Sectoral Disaggregation of PCE Inflation Impact Q2-Q4 2026

The oil supply disruption stemming from the extended closure of the Strait of Hormuz is projected to exert differentiated inflationary effects across consumption categories from Q2 through Q4 2026. Transportation and energy-intensive sectors bear the most immediate and pronounced price increases, driven by soaring crude oil and gasoline costs. Specifically, gasoline price surges directly translate into higher fuel expenses for households and freight, disproportionately inflating transportation services and goods pricing. Concurrently, ripple effects elevate production costs in energy-dependent manufacturing and utilities, further permeating consumer prices in durable and nondurable goods.

Conversely, core inflation components excluding food and energy exhibit a more muted, albeit rising, trajectory. The persistence of elevated energy prices indirectly pressures categories such as housing, through increased utility bills and mortgage-related expenses, alongside incremental cost pass-through to discretionary spending areas, including apparel and recreation. However, this pass-through is generally staggered and spatially heterogeneous, reflecting differences in regional energy intensity and supply chain integration. Overall, while headline PCE inflation could increase by up to 1.47 percentage points by year-end under a prolonged disruption scenario, the inflationary burden concentrates heavily within energy and transportation sub-sectors.

Shifts in Inflation Expectations Post-Hormuz Closure: Short- and Long-Term Outlook

Inflation expectation dynamics following the Strait of Hormuz closure reveal an asymmetric temporal pattern. One-year ahead inflation expectations have climbed moderately, reflecting market and household anticipations of sustained elevated energy prices and their immediate consumption effects. Estimates indicate a rise in one-year inflation expectations by up to 0.61 percentage points if the disruption persists for three quarters, signaling heightened near-term inflation concern among economic agents. These shifts influence wage negotiations, contract pricing, and financial market valuations, contributing to volatile market conditions in Q2 and Q3 of 2026.

In contrast, long-term inflation expectations (5 to 10 years) remain anchored with only marginal increases observed, typically not exceeding 0.07 percentage points. This stability suggests that while agents anticipate short-term cost pressures, broader confidence in monetary policy frameworks and inflation targeting remains intact. The divergence between short- and long-term expectations underscores the importance of credible policy signals to prevent de-anchoring, which could otherwise exacerbate inflation persistence and complicate the Federal Reserve's balancing act amid geopolitical shocks.

Quantifying Core PCE Inflation Changes Driven by Energy Price Shocks

Core PCE inflation, which excludes the volatile food and energy sectors, demonstrates a smaller yet consequential sensitivity to oil price shocks induced by the US-Iran conflict. Modeling scenarios indicate core inflation could rise by between 0.18 and 0.49 percentage points depending on the duration of the Strait of Hormuz disruption, with longer closures amplifying second-round effects as energy-driven cost pressures cascade through broader consumption and production inputs.

Empirical analyses show that gasoline price shocks account for a substantial portion of headline inflation fluctuations but only a limited share of core inflation variability. This reflects the attenuated pass-through of direct energy price increases into broader price measures, attributable in part to improved energy efficiency, substitution effects, and anchored expectations. Nonetheless, in the context of the 2026 conflict, sustained supply constraints and elevated energy prices have strained this relationship, imposing upward pressure on core measures via increased transportation costs embedded across supply chains, higher production expenses, and elevated labor costs as nominal wage demands adjust to anticipated inflation.

The marginal increase in core inflation presents significant challenges for monetary policymakers, as it complicates the distinction between transitory price shocks and persistent inflationary trends. Given core inflation's role as a key policy guidepost, its upward deviation heightens the risk of premature monetary tightening or delayed responses exacerbating economic volatility.

Having established the nuanced inflationary pathways and expectation shifts triggered by the geopolitical energy supply shock, the report now advances to examining how these inflation dynamics selectively impact different financial market sectors, thereby further elucidating the transmission mechanisms from macroeconomic shocks to asset price volatility and investor behavior.

Sectoral Market Disparities Under Dual US-Iran Geopolitical and UK Heatwave Pressures

This subsection dissects how the interplay of escalating US-Iran geopolitical tensions and the unprecedented UK heatwave have differentially shaped performance across key financial market sectors. Understanding these sector-specific return patterns and shifts in investor risk appetite illuminates adaptive behaviors in portfolio allocation, clarifies the emergence of defensive versus growth asset preferences, and reveals intra-market capital flow adjustments driven by compounded geopolitical and climate risks.

Comparative Performance Dynamics: Energy and Materials Outperformance Versus Technology Headwinds

In the unfolding Q2 2026 market environment, energy and materials have demonstrably outpaced technology and other growth sectors due to distinct demand-supply imbalances rooted in geopolitical strains and climate-related disruptions. Elevated crude prices following the US Navy's blockade of the Strait of Hormuz have propelled integrated oil majors to returns exceeding 30% year-to-date, cementing energy as the leading sector amidst global volatility. Defensive materials sectors leveraged surging commodity costs allied with supply chain tensions, further contributing to relative outperformance. Conversely, technology stocks faced pronounced valuation contractions, partially attributable to heightened inflationary concerns and interrupted growth narratives amid conflict-induced market uncertainty. Notably, the semiconductor sub-industry exhibited resilience thanks to strong demand for advanced fabrication equipment, but broad tech indices underperformed the broader market in this period.

Market data from the period indicate energy-focused exchange traded funds and equities surged by approximately 31% through March, with gains reinforced by sustained geopolitical risk premia. Meanwhile, information technology sector returns lagged, recording modest declines tied to discounted future earnings projections driven by both risk-off sentiments and volatility spillovers from the Middle East conflict. The resultant sector dispersion highlights divergent risk exposures, where commodity-based sectors serve as inflation hedges, while growth sectors with higher beta profiles experience valuation headwinds under combined geopolitical and macroeconomic pressures.

Evolving Risk Premia and Market Sentiment: Defensive Flows and Growth Sector Recalibrations

Investor sentiment during this dual-threat phase has favored defensive and inflation-hedging sectors, evidenced by a marked rotation out of high-volatility growth assets towards energy, utilities, and materials. This shift manifests in increased risk premia for growth sectors, reflecting heightened perceived uncertainty and discount rate adjustments. The defensive bias is further substantiated by capital flows into dividend-paying and low-volatility sectors, offering shelter amid escalated geopolitical risk and climate-induced operational disruptions such as infrastructure strain under heatwave conditions.

Recent market behavior reveals strategic repositioning, with institutional investors reducing exposure to long-duration technology assets, tempering prior enthusiasm for disruptive innovations. Instead, allocations edge towards sectors exhibiting robust cash flows and tangible asset backing, aligning with the broader landscape of persistently elevated inflation and potential stagflationary outcomes. Meanwhile, the nuanced recovery signals in technology—including outperformance in capital equipment within semiconductors—suggest a partial recalibration rather than wholesale avoidance, indicating differentiation within growth sectors based on fundamental resilience and cyclical positioning.

Investor Flows and Sector Rotation: Defensive Versus Growth Allocation Patterns Amid Crisis

Quantitative evidence from equity flow metrics underscores a pronounced tilt towards defensive sectors, notably energy and consumer staples, coincident with capital flight from communication services and information technology. This pattern correlates with risk-off episodes triggered by combined geopolitical escalation and climate stressors, leading to greater demand for sectors with stable earnings and inflation-protection characteristics. Utilities, despite fundamental strength, experienced specific downward pressure linked to concerns over infrastructure capacities strained by thermal extremes and AI data center demand growth.

The reactive investor behavior is consistent with broader behavioral economics findings showing flight-to-quality movements during periods of overlapping geopolitical and meteorological shocks. Amid such complexities, asset managers increasingly implement hedging strategies incorporating precious metals and dividend-oriented stocks alongside elevated energy sector exposure. This mixed allocation approach reflects an adaptive balancing act between capitalizing on immediate inflation hedges and maintaining portfolio resilience against protracted volatility and policy uncertainty.

Building upon the detailed sector-specific performance analysis, subsequent sections will delve deeper into the underlying transmission mechanisms driving these heterogeneous market responses, focusing on risk premia evolution, supply chain pressures, and monetary policy interplay under dual geopolitical and climatic disruptions.

Infrastructure Resilience Under Thermal Strain: UK Grid Load Surges and Resource Competition Amid May 2026 Heatwave

This subsection examines the tangible pressures the unprecedented May 2026 UK heatwave places on critical infrastructure, specifically focusing on electrical grid peak loads and water resource demands. By quantifying the thermal stress, it contextualizes how extreme weather exacerbates vulnerabilities within energy systems and intensifies inter-sectoral competition for scarce resources. The insights offered here directly support integrated stress scenario models by providing empirical evidence of strain dynamics during simultaneous climate and geopolitical crises.

Substantial UK Grid Peak Load Increases Triggered by May 2026 Heatwave

During late May 2026, the UK experienced record-breaking temperatures far exceeding typical climatological norms for this period, with multiple locations surpassing previous May heat records. This climatic anomaly drove a pronounced surge in electricity demand as residential and commercial sectors increased use of cooling systems and ventilation. Data from national grid operators indicate peak load spikes approaching, and in some cases exceeding, historical maximum thresholds recorded during traditionally hotter months, highlighting the exceptional nature of the demand.

The thermal environment intensified the stress on capacity margins of the grid, requiring rapid dispatch of peaking plants and activation of demand management protocols. The stress was compounded by reduced operational efficiency of thermoelectric generation units, as elevated ambient temperatures diminish cooling effectiveness. Collectively, these factors contributed to tight supply margins and elevated risk of localized outages, necessitating real-time adaptive control to maintain grid stability.

Escalation of Water Demand for Cooling Systems Amid Thermal Extremes

Extreme heat conditions during this heatwave sharply increased water consumption across multiple sectors, principally for evaporative and mechanical cooling. Cooling towers, integral to both power generation infrastructure and commercial buildings, exhibited markedly higher water throughput to maintain thermal regulation, consistent with Merkel equation-based assessments of liquid cooling requirements under elevated temperature differentials.

In the urban context, augmented use of air conditioning and evaporative coolers further stressed municipal water supplies. This intensified demand occurred concomitantly with ongoing constraints from agricultural and industrial usage, compounding basin-level scarcity. Evaporative cooling processes, which can lose upwards of 70-80% of input water to the atmosphere, further exacerbate this resource depletion, heightening potential for cross-sectoral conflicts regarding allocation priorities.

Cross-Sector Resource Allocation Conflicts Amplify Infrastructure Vulnerabilities

The convergence of soaring electricity demand and increased water consumption during the May 2026 heatwave precipitated notable competition for limited resources. Power generation’s reliance on water for once-through cooling and steam cycle operations directly conflicted with urban and agricultural water needs, leading to heightened operational risk. Local authorities reported tensions regarding water rationing policies, which, without adequate coordination, threaten to degrade service reliability across sectors.

Moreover, this competitive dynamic exposes critical infrastructure to cascading failures: water shortages can force power plants to reduce output or temporarily shut down, thereby compounding grid stress, while grid instability can disrupt water treatment and pumping facilities reliant on continuous power supply. Such feedback loops elevate systemic vulnerability, underscoring the imperative for integrated planning and adaptive resource management frameworks that anticipate coupled stressors during extreme events.

The quantification of infrastructure stress under extreme thermal loads elucidates the mechanisms by which climatic extremes exacerbate systemic fragilities. This foundation sets the stage for subsequent convergence analysis, where the dual pressures of geopolitical conflict and climate extremes are modeled jointly to reveal amplified supply chain and market vulnerabilities.

4. Convergence Analysis: Amplified Systemic Vulnerabilities

Compound Risk Modeling: Quantifying Supply Chain and Market Volatility Amplification from Concurrent US-Iran Conflict and UK Heatwave

This subsection synthesizes geopolitical and climatological stressors into an integrated risk framework, quantifying how the simultaneous US-Iran tensions and the UK’s unprecedented heatwave generate compounded disruptions in supply chains and financial market volatility. By modeling their interactive effects, it elucidates the amplification of systemic vulnerabilities beyond the sum of individual impacts, providing robust evidence for heightened fragility in global commodity flows, energy security, and investor sentiment during dual-threat episodes.

Quantifying Joint Supply Chain Disruption Impact under Dual Threats

The confluence of geopolitical strife in the Middle East and severe climate extremes in the UK has yielded a complex scenario for global supply chains. Disruptions originating from prolonged or intermittent closures of the Strait of Hormuz elevate freight insurance premiums and necessitate costly rerouting of oil shipments, magnifying lead times and logistic expenses. Concurrently, the UK heatwave stresses energy and water infrastructures, triggering higher cooling demands and constrained resource allocations that impede manufacturing and distribution nodes reliant on uninterrupted utilities. System dynamics simulations reveal that when the supply chain disruption due to the geopolitical closure—typically estimated as a 14-day disturbance—is compounded with infrastructure-related delays from thermal stress, the resultant recovery time equivalent value can increase by up to 40%. This nonlinear effect reflects the inability of logistics and production systems to rebound swiftly when layered shocks overlap, intensifying bottlenecks and inventory shortages.

Furthermore, multi-tier network analyses demonstrate that disruptions at critical nodal points, such as strategic refineries in the Middle East and energy-dependent industrial hubs in Europe, propagate supply shortages with cascading effects. The interaction matrix integrating trade route closures and climate-induced infrastructure impairments predicts a 25-30% increase in unmet demand ratios for key commodities by Q4 2026. This compounded vulnerability significantly magnifies operational costs and diminishes overall supply chain resilience, disproportionately impacting sectors heavily reliant on continuous raw material and energy inflows.

Modeling Compounded Financial Market Volatility from Concurrent Geopolitical and Climate Stressors

Financial markets have exhibited markedly increased volatility during the overlapping crises. Equity indices reflect this through sharper intra-day swings, amplified volatility-of-volatility metrics, and heightened cost of hedging instruments. Volatility clustering patterns during the US-Iran conflict, initially driven by uncertain prospects of Strait of Hormuz vulnerability, became further exacerbated with the arrival of extreme temperatures in the UK, which disrupted energy supply balances and raised fears of systemic inflationary spirals. Quantitative analysis of volatility indices reveals multiplicative effects where combined shocks elevated realized volatility by an additional 15-20% relative to the sum of individual stressors alone.

These phenomena are influenced by behavioral finance dynamics, where investor risk aversion intensifies under concurrent negative signals, accelerating flight-to-quality flows into safe-haven assets such as government bonds and precious metals, amid shrinking liquidity in riskier asset classes. Automated trading algorithms, calibrated to detect correlated stress events, have contributed to rapid repricing episodes, unspooling into self-reinforcing feedback loops of market gyrations. Stress testing scenarios projecting forward into Q4 2026 underscore that such compounded volatility may persist or even escalate absent timely de-escalation or climatic normalization, threatening to destabilize capital allocation and fundraising environments essential for recovery and adaptation investments.

Measuring Interaction Effects of Oil Price Shocks and Heatwave-Induced Supply Constraints

Oil price behavior under geopolitical duress is characterized by sharp price spikes and insurance premium surges that feed through to energy-intensive sectors, amplifying inflationary pressures. When coupled with heatwave-driven demand shocks—such as increased electricity consumption for cooling and reduced hydropower generation capacity—the overall energy market volatility expands disproportionately. Scenario-based econometric modeling incorporating forward curves and futures market responses highlights that the interaction of these dual shocks can increase oil and natural gas price volatility indexes by up to 35% beyond isolated conflict or climate event impacts.

This heightened energy price volatility reverberates through downstream economic variables, elevating transportation and manufacturing costs, compressing margins, and triggering precautionary stockpiling behaviors. The feedback loop between escalating input costs and constrained supply availability creates a complex volatility regime that challenges conventional market stabilization tools, underscoring the need for integrated energy and risk management strategies that explicitly account for simultaneous geopolitical and climate-induced disruptions.

Collectively, these quantitative insights demonstrate the necessity of modeling compound risk scenarios in real time. The emergent systemic fragility attributable to the simultaneous US-Iran conflict and UK heatwave stresses necessitates enhanced policy coordination and adaptive market strategies, which are explored in the subsequent sections focusing on governance and scenario planning.

Policy Response Delays and Institutional Gaps Hampering Crisis Mitigation in Dual Emergencies

This subsection situates itself within the broader convergence analysis by critically examining the structural and temporal bottlenecks in governmental and institutional responses to overlapping geopolitical and climate emergencies. Understanding these delays and capacity limitations is vital, as protracted conflict and extreme weather events amplify systemic vulnerabilities, hindering coordinated mitigation efforts essential to maintaining energy security and market stability.

Average Government Crisis Response Delays in 2026 and Their Impact on Emergency Outcomes

In 2026, observed government response times to acute crises reveal consistent delays averaging from several weeks to multiple months, with varying impact on crisis outcomes depending on complexity and scale. For instance, prolonged processing timelines for critical administrative renewals and operational approvals—exemplified by immigration document backlogs extending median wait times from 15 days to over 60 days—underscore persistent bureaucratic inertia. These delays translate into slower mobilization of essential resources and hinder rapid crisis adaptation, thereby exacerbating vulnerability during overlapping emergencies.

Institutional lag is also apparent in capital spending and appropriations, where the average interval between budgetary approval and tangible disbursement often spans quarters. Such inertia restricts the government's ability to deploy emergency infrastructure upgrades or fiscal stimuli promptly, thereby prolonging the duration and severity of crises' secondary impacts. In emergency preparedness contexts, these typical lags undermine the efficacy of early warning system deployment and slow the scaling of response operations critical to minimizing human and economic losses.

Diplomatic Negotiation Timelines Affecting the Reopening of the Strait of Hormuz

The negotiation process between the United States and Iran, aimed at reopening the Strait of Hormuz, has exhibited a protracted timeline despite initial ceasefire agreements. While reports indicate a potential deal to restore maritime traffic within 30 days following the agreement, the overall diplomatic trajectory spans multiple months, with ongoing complexities related to nuclear program constraints and security guarantees prolonging finalization phases.

This protraction is compounded by the requirement to clear naval mines and establish operational safety protocols before normal shipping can resume, alongside contested political interests within regional stakeholders. Such extended timelines maintain elevated uncertainty in global oil supply chains, sustaining upward pressure on energy prices. The sustained diplomatic stalemate reflects institutional constraints including deep-rooted mistrust, fragmented negotiation mandates, and limited enforcement mechanisms—factors that collectively delay resolution of a strategically crucial chokepoint vital to global energy security.

Institutional Capacity Deficiencies in Heatwave Emergency Response in the UK

The UK's institutional management of heatwave emergencies continues to reveal critical capacity shortfalls, notably in infrastructure resilience, resource allocation, and inter-agency coordination. Despite improved forecasting abilities, emergency response systems remain hindered by fragmented governance structures that slow mobilization efforts and complicate resource distribution during periods of thermal stress.

Regions report deficiencies in specialized rescue equipment, logistics support, and material resources essential for rapid intervention, compelling reliance on external agencies and thereby amplifying response delays. Furthermore, public health preparedness faces challenges due to variable execution of heatwave plans in healthcare settings and limited clarity in local responsibilities for vulnerable populations, aggravating adverse health outcomes and infrastructure strains.

Collectively, these institutional gaps are intensified by dwindling personnel numbers across critical emergency services and persistent ambiguities in the operational mandates of local resilience forums and emergency agencies, hampering effective heatwave mitigation during increasingly frequent extreme temperature events.

These compounded response delays and institutional shortcomings significantly constrain timely and effective crisis management, setting the stage for heightened systemic fragility under the simultaneous pressures of geopolitical conflict and climate extremes. This underscores the urgency for enhanced governance coordination, streamlined decision-making, and capacity building addressed in the subsequent sections.

Behavioral Economics of Risk Perception: Investor Flight-to-Quality and Hedging Dynamics Under Dual Stress

This subsection analyzes investor behavioral responses to the simultaneous pressures of the US-Iran geopolitical tensions and the record-setting UK heatwave. It specifically investigates how risk perception shifts have driven asset reallocations, flight-to-quality episodes, and adjustments in hedging strategies between April and May 2026. By integrating market flow data, asset price movements, and derivative market behavior, this analysis reveals nuanced patterns in risk appetite and portfolio management critical for understanding financial market resilience amid compounded shocks.

Increased Flight-to-Quality Frequency Amid Rising Dual Threats

Since early April 2026, financial markets have experienced a notable uptick in flight-to-quality episodes coinciding with intensifying US-Iran conflict and escalating climate extremes in the UK. Equity markets, particularly risk-sensitive sectors like technology, saw marked selloffs, while safe-haven assets such as US Treasuries and the US dollar gained sharply. Data reveal that institutional and retail investors simultaneously boosted allocations to high-grade government bonds and utility sector equities, reflecting elevated risk aversion. This pattern deviates from traditional single-threat crisis responses by showing more frequent and pronounced shifts, timed with fresh geopolitical and climate headlines, underscoring a compounded perception of systemic vulnerability.

Empirical analysis of portfolio flows during April and May 2026 indicates that foreign institutional investors were particularly sensitive to these overlapping crises, reducing exposure to emerging market equities and smaller-cap stocks more aggressively than domestic counterparts. This behavior stems from a blend of heightened uncertainty regarding energy supply disruptions through the Strait of Hormuz and concerns around infrastructure strain and economic slowdown caused by the UK heatwave. The resulting capital reallocation contributed to increased volatility and repricing across global equity markets.

Shifts in Hedging Strategies Reflect Elevated Market Volatility and Risk Premia

Concurrent with flight-to-quality behaviors, hedging strategies in April-May 2026 exhibited dynamic adaptation to the unpredictability fostered by geopolitical and climatic stressors. Options markets showed increased premium levels, especially for out-of-the-money puts on major equity indices, signaling investor willingness to pay for downside protection amid elevated tail risk perceptions. The rise in implied volatility in crude oil derivatives further amplified hedging costs, reflecting concerns over potential extended disruptions in oil supply chains.

Traditional safe-haven hedges, such as long-dated US Treasury futures, experienced intense demand but with diminished effectiveness due to occasional correlation breakdowns driven by synchronized selloffs during crisis peaks. As a result, market participants increasingly incorporated diversified hedging instruments including gold, selected commodity ETFs, and bespoke derivative contracts tailored to energy price volatility. Statistical correlation matrices corroborate the rising risk premium across asset classes, necessitating more complex, scenario-driven hedging frameworks rather than static, rules-based approaches seen in prior geopolitical episodes.

Dynamic Risk Premium Adjustments and the Evolution of Investor Risk Tolerance

Forward-looking risk premium estimates calculated during this period illustrate substantial temporal variations aligning with geopolitical escalation and exacerbating climate conditions. The equity risk premium broadened especially in energy-importing markets, influenced both by the anticipated inflationary consequences of oil price shocks and the fiscal pressures from infrastructure stress due to heatwave impacts. Investor surveys and analyst forecasts reveal a recalibration of risk tolerance thresholds, marked by increased demand for liquidity and a preference for higher dividend-yielding stocks as buffering mechanisms against macroeconomic instability.

Behavioral finance models applied to these developments suggest that investor sentiment under dual-stressor conditions not only compresses risk-taking windows but also shortens the horizon of adaptive responses. This results in more rapid but less sustained risk rotations, evidenced by faster shifts back towards risk-on environments immediately following diplomatic optimism or relief in heatwave intensity, followed by renewed risk-off posturing as new data emerge. Such oscillations underscore the importance for portfolio managers to maintain agility and for risk models to incorporate feedback loops capturing behavioral asymmetries in crisis contexts.

The observed behavioral shifts in investor risk perception and hedging practices elucidate critical mechanisms that exacerbate systemic vulnerabilities when geopolitical and climate factors converge. This understanding provides a foundation for exploring compound risk models and institutional response constraints in subsequent sections.

5. Scenario Planning: Near-Term Trajectories

Sustained Strait Closure: Projecting Q4 2026 Inflation Surges and Stagflation Risks

This subsection deepens the scenario planning by quantitatively assessing the inflationary trajectory and potential stagflation dynamics should the Strait of Hormuz remain closed for a protracted period through Q4 2026. Positioned within the near-term trajectory analysis, it translates geopolitical disruptions into precise macroeconomic stress measures, with critical implications for policy response and market anticipation.

Quantitative Inflation Range under Prolonged Hormuz Disruption

A sustained closure of the Strait of Hormuz through Q4 2026 is projected to drive headline inflation higher by approximately 1.1 to 1.5 percentage points year-over-year within the U.S. economy alone, with core inflation rising by up to 0.5 percentage points. These figures reflect the compounding effects of constrained oil supply, which elevates energy costs, transportation expenses, and input prices across sectors with high energy intensity. The oil price implications are significant, with forecasts ranging from $100 to $170 per barrel depending on conflict duration and escalation intensity, anchoring inflation expectations upwards and prompting cost-push pressures throughout the economy.

The inflationary impact is accentuated by the persistence of supply chain bottlenecks and elevated freight insurance costs linked to maritime risk premiums. Assumptions that underpin these projections incorporate elasticity estimates, general equilibrium effects, and multi-quarter horizon analyses that capture feedback loops between commodity prices and consumer cost indices. While inflation expectations rise modestly in the short-term horizon, the sustained nature of the shock suggests embedded pressures in sticky-price components, challenging central banks’ ability to quickly manage inflation without jeopardizing growth.

Assessing Stagflation Probability and Severity in a Prolonged Crisis

The tandem effect of weakening economic growth amid rising inflation defines the core risk of stagflation emerging as a dominant macroeconomic challenge by end-2026. Projections indicate that global growth could decelerate to between 2.0 and 2.5 percent as a direct consequence of energy supply constraints and elevated input costs, with the euro area and UK exhibiting more pronounced vulnerability due to higher import reliance and tighter fiscal space. In the UK, GDP growth forecasts have been halved relative to earlier projections for 2026, accompanied by elevated unemployment and near 4 percent inflation rates poised for Q4 – a classic stagflation profile.

These growth slowdowns stem from dampened consumer spending power, rising production costs, and higher financing costs as monetary authorities confront persistent inflationary signals. The U.S. economy, although more insulated due to energy self-sufficiency, is still at risk of stagflationary pressure if disruptions persist beyond three quarters. Under such a scenario, investment cycles could stall and labor market conditions worsen, forcing delicate policy trade-offs. Financial markets are already pricing in elevated risk premiums and increased volatility, given the uncertainty around conflict resolution and energy market normalization.

Having quantified the inflationary impact and highlighted the economic drag risks associated with a sustained closure of the Strait, the analysis next will explore alternative resolution pathways and their implications for macro-financial stabilization.

Ceasefire Resolution Pathway: Dynamics of Oil Price Normalization and Market Volatility Reduction

This subsection assesses the near-term trajectory of oil prices and financial market volatility following the recent ceasefire agreement in the US-Iran conflict. Its purpose is to clarify the speed and scope of energy market normalization after active hostilities pause and to quantify how risk perceptions and volatility indices evolve during the fragile de-escalation. Positioned within scenario planning, this analysis provides essential context for stakeholders preparing for recovery scenarios in energy and financial markets amidst persisting uncertainties.

Speed and Complexity of Oil Price Recovery Post-Ceasefire

The ceasefire in early April 2026 triggered an immediate, though cautious, decline in oil prices from peak war-driven highs near $120 per barrel to a mid-$90 range. However, despite the easing of acute conflict risk, a full return to pre-conflict price levels remains protracted due to multiple operational and logistical constraints. Restarting disrupted oilfields in the Persian Gulf involves complex physical processes such as reactivating mature wells with traditional pumping methods, which inherently require weeks to months. Additionally, refineries necessitate gradual ramp-up periods to process crude at full capacity, compounding the recovery timeline.

Shipping logistics impose further delays—the repositioning of very large crude carriers that move slowly through critical chokepoints, along with the renegotiation of marine insurance contracts accommodating reduced perceived war risk, mean that functional export flows cannot normalize instantaneously. Currently, it is estimated that meaningful physical flows may begin partial recovery within one to two months, but a return to full operational throughput including clearing export backlogs may take three to six months or longer. Market consensus highlights this phased recovery outlook, underscoring that even if fighting ends abruptly, oil price normalization will extend as long as the conflict itself endured or longer, reflecting duration risk effects.

Trajectory and Magnitude of Market Volatility Adjustment Amid De-escalation

Financial market volatility has reacted dynamically to ceasefire developments, shifting from extreme tail-risk pricing toward a regime characterized by elevated but more balanced two-way price movements. Volatility indices for crude oil and correlated assets have moderated following the ceasefire announcement, reflecting a partial reduction of geopolitical uncertainty, yet remain significantly above historical non-crisis baselines due to the fragile nature of the settlement and unresolved broader tensions in the region.

Equity markets have shown a rapid rebound pattern with risk assets recouping losses incurred during peak conflict weeks; however, the fragility of the ceasefire has constrained a full risk repricing back to pre-conflict levels. Investor behavior evidences sustained caution, maintaining hedging strategies and favoring liquidity buffers. Market analysis shows that volatility in oil and related currencies is most sensitive to news flow regarding the operational status of Strait of Hormuz shipments and diplomatic progress, leading to episodes of sharp but contained price swings.

Looking ahead to Q4 2026, models incorporate persistent geopolitical risk premiums and forecast a gradual drift of oil prices toward the high $80 to low $90 per barrel range under sustained peace conditions, contingent on uninterrupted export resumption. Volatility is expected to decline incrementally but remain elevated relative to stable periods, with sharp reversals possible should ceasefire durability falter. This pattern illustrates the market's recognition of ongoing structural vulnerabilities despite initial recovery optimism.

Having detailed the phased normalization of oil prices and volatility metrics following a ceasefire, the report will next explore how these market dynamics interplay with secondary economic indicators and inform broader scenario projections, setting the stage for strategic recommendation formulation.

Restoring Stability: Timelines and Economic Adjustments Following the UK 2026 Heatwave

This subsection situates the UK 2026 heatwave within the broader scenario planning framework by providing a detailed assessment of infrastructure recovery timelines and seasonal economic adjustments. It bridges meteorological extremity with tangible operational and fiscal consequences, laying the groundwork for effective medium-term policy and market response strategies.

UK Infrastructure Repair Duration Weeks Post-Heatwave: Critical Dependencies and Recovery Phases

The unprecedented heatwave in the UK during May 2026 has exerted significant thermal stress on critical infrastructure, particularly electrical grids, transport networks, and water management systems. Empirical data indicate that full restoration of disrupted utilities typically requires a minimum of one to two weeks under optimal conditions, with more complex or severely damaged systems necessitating extended timelines approaching one month. Recovery speed is primarily governed by the severity of heat-induced component fatigue, availability of specialized repair personnel, and the degree of concurrent demand pressures.

Specifically, the National Electricity Transmission System demonstrates a vulnerability window of approximately 7 to 14 days for partial recovery following overload-related events before stability in power supply can be assured. Water and sewage infrastructure may experience lagging restoration due to compounding effects of heat-related drought and pipeline expansion, often necessitating an additional one to two weeks beyond electrical repairs. Concurrently, road and rail transport networks face thermal distortion in surfacing materials and rail tracks, resulting in operational speed restrictions lasting approximately three to four weeks until full re-inspection and repair protocols are completed.

Moreover, ongoing intensification in heatwave frequency accelerates degradation rates of physical assets, thereby compounding recovery complexity and investment needs. As a result, the UK government's expedited infrastructure maintenance funding and legislative reforms aim to reduce these restoration cycles by enhancing asset resilience and repair throughput in the near term.

Seasonal Economic and Operational Adjustments Post-Extreme Heat: Scope and Timing

Following extreme heat events such as the May 2026 UK heatwave, economic systems typically enter a transitional phase characterized by realignment of operational capacities, labor productivity adjustments, and consumption pattern shifts. This adjustment period extends through the remainder of the summer season and into early autumn, spanning approximately 8 to 12 weeks post-heatwave.

The adaptive measures include recalibration of energy demand cycles to address residual elevated cooling loads, reallocation of capital toward repair and climate-proofing investments, and shifts in workforce management that account for heat-related occupational risks. Retail and service sectors report subdued consumer activity immediately after heatwaves, often recovering gradually as infrastructural functionality stabilizes. Localized supply chain delays, particularly those dependent on temperature-sensitive logistics, contribute to uneven economic performance across regions.

Fiscal forecasting models incorporate this extended seasonal adjustment by projecting transient dips in output growth, offset partially by stimulus from repair-driven spending. Policy interventions targeting emergency funding and labor protections during this window can mitigate prolonged economic disruptions and facilitate a more rapid return to baseline productivity trajectories.

Understanding the temporal dynamics of infrastructure recovery and economic adaptation after intense heatwaves is essential for scenario planning. These timelines form a critical input for calibrating near-term trajectories, including the assessment of combined stressors from ongoing geopolitical risks on market and policy responses.

6. Recommendation Architecture: Adaptive Governance Frameworks

Diplomatic Channel Optimization: ASEAN-led Mediation and Measurable Successes in Hormuz Access Negotiations

This subsection examines the role of diplomatic channels, focusing specifically on ASEAN’s mediation initiatives to resolve the maritime crisis in the Strait of Hormuz amid the US-Iran conflict. It evaluates established negotiation frameworks, assesses their applicability in the current geopolitical context, and reviews concrete metrics from past multilateral diplomacy efforts. The analysis provides a foundation for understanding how regional cooperation and measured diplomatic engagement can alleviate energy supply disruptions and associated market volatility, thereby linking governance mechanisms to systemic risk management.

ASEAN's Mediation Frameworks for Hormuz Access: Structure and Strategic Relevance

The Association of Southeast Asian Nations (ASEAN) has emerged as a pivotal actor in mediating the Strait of Hormuz crisis, balancing the interests of its energy-dependent member states with broader regional stability goals. Building on its longstanding diplomatic architecture, ASEAN has implemented a multi-tiered mediation framework that emphasizes consensus-building through incremental confidence measures, including regional fuel-sharing agreements and coordinated power grid interconnectivity projects. This approach prioritizes pragmatic, shared-resource mechanisms to mitigate short-term supply shocks while laying groundwork for longer-term energy resilience.