Navigating the Nexus of AI-Driven Growth and Geopolitical Energy Risks: U.S. Economic and Market Dynamics in Mid-2026

Table of Contents

- Executive Summary

- Introduction

- 1. Diagnostic Overview: Identifying Core Economic Indicators and Market Symptoms

- 2. Root Cause Analysis: Tracing Underlying Drivers of Economic Momentum and Market Volatility

- 3. Strategic Synthesis: Developing Balanced Portfolios for the AI-Geopolitical Nexus

- 4. Scenario Assessment: Evaluating Alternative Futures for U.S. Economic Trajectory

- 5. Implementation Roadmap: Building Adaptive Decision Frameworks for Mid-2026

- 6. Synthesis and Final Recommendation: Maintaining Equilibrium in Turbulent Times

- Conclusion

Executive Summary

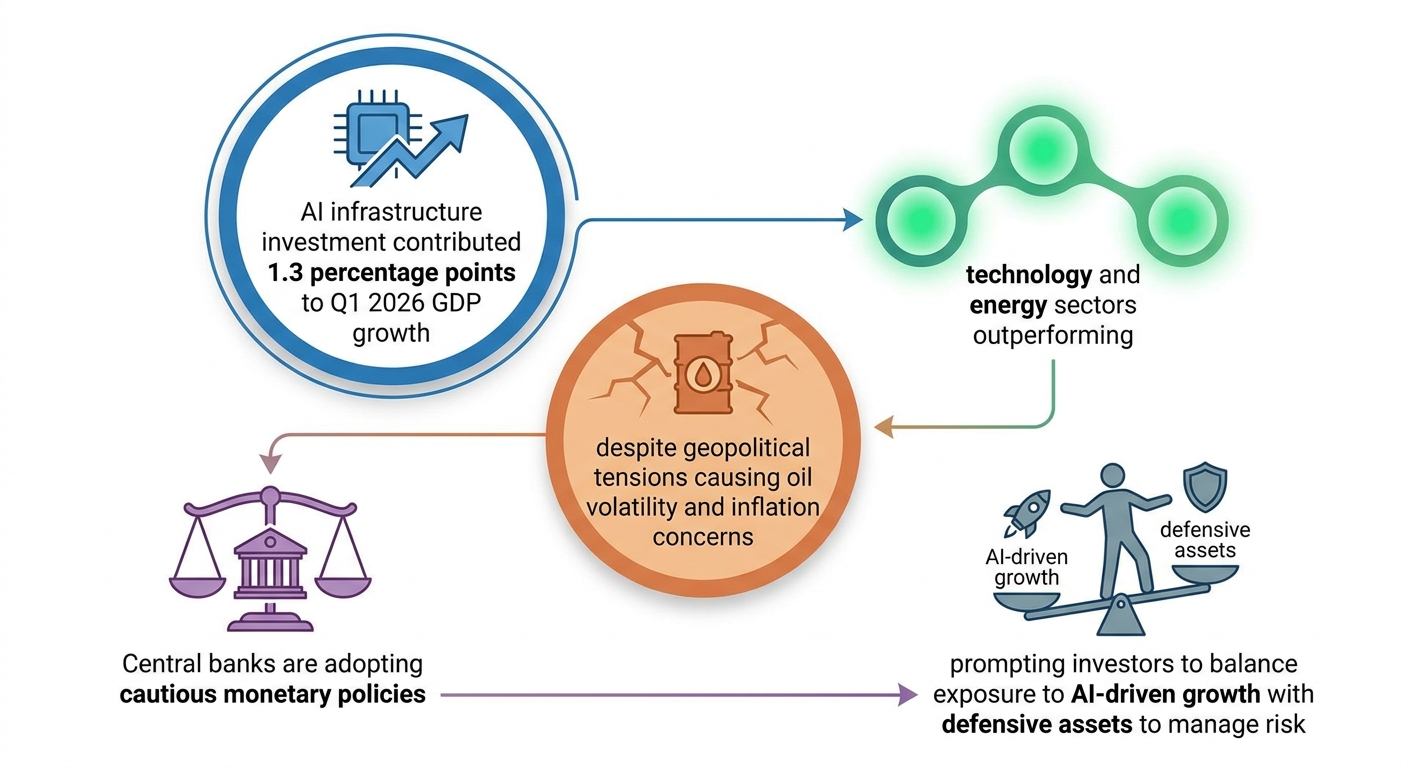

In the first quarter of 2026, artificial intelligence (AI) infrastructure investment emerged as a pivotal growth engine, contributing approximately 1.3 percentage points to U.S. GDP growth and accounting for nearly 40% of capital expenditure-driven expansion. This structural investment surge, led by hyperscale data center construction, semiconductor manufacturing, and AI software development, underpins sustained corporate earnings growth—exceeding 18% annually for AI-enabled firms—and signals a transformative phase in productivity and economic momentum. Despite these gains, broad-based productivity improvements remain nascent, reflecting temporal lags inherent in adopting advanced AI technologies.

Simultaneously, escalating geopolitical tensions between the U.S. and Iran have intensified volatility in global energy markets, with Brent crude prices breaching $200 per barrel during peak conflict phases and risk premiums adding $12 to $30 above equilibrium levels. Disruptions through the Strait of Hormuz have curtailed approximately 20% of global oil shipments, triggering massive shipping detours, soaring war-risk insurance premiums (up to 7.5% of vessel value), and inflationary pressures permeating manufacturing and consumer prices. These dynamics complicate monetary policy responses and introduce heightened uncertainty, necessitating a calibrated approach that blends overweight allocations in high-conviction AI infrastructure with defensive energy sector exposures to optimize resilience amid intersecting growth and risk trajectories.

Introduction

The first half of 2026 stands as a defining juncture in the U.S. economic and geopolitical landscape, characterized by the unprecedented convergence of accelerating artificial intelligence (AI) adoption and intensifying international energy tensions. AI infrastructure investments have escalated dramatically, manifesting in groundbreaking capital expenditures on data centers, semiconductor fabrication, and advanced software platforms. These developments portend a paradigm shift in productivity growth and corporate earnings potential, reminiscent of historic technological revolutions.

Yet, this period is equally marked by heightened geopolitical risks stemming from the deteriorating U.S.-Iran relationship, which has precipitated sustained disruptions in critical oil supply chains. The ensuing energy market volatility not only injects inflationary pressures but also threatens to constrain the physical and financial underpinnings necessary to realize AI's full economic promise. The dual narratives of innovation-led expansion and risk-driven instability pose complex challenges for policymakers, investors, and corporate strategists alike.

This report aims to diagnose the core economic indicators reflecting AI’s direct contribution to GDP and corporate performance while unpacking the structural causes behind sectoral shifts and productivity transitions. Concurrently, it assesses the geopolitical shockwaves reshaping energy markets, quantifying their transmission into inflation, labor markets, and monetary policy trajectories. Ultimately, the analysis integrates these dimensions into strategic frameworks for balanced portfolio construction, risk management, and governance, equipping stakeholders with actionable insights for navigating the intertwined AI-geopolitical nexus in mid-2026.

Infographic Image: Infographic

1. Diagnostic Overview: Identifying Core Economic Indicators and Market Symptoms

Quantifying AI's Direct Economic Contribution: Unpacking Q1 2026 Growth and Corporate Earnings Impact

This subsection establishes the empirical foundation for understanding how artificial intelligence (AI) investments materially contributed to U.S. economic expansion in early 2026. By precisely measuring AI infrastructure expenditure’s share in GDP growth and isolating its role in driving corporate profitability improvements, it sets the stage for assessing AI’s structural significance amid concurrent geopolitical uncertainties.

Robust Scale of AI Infrastructure Investment and Its GDP Growth Attribution in Q1 2026

In the first quarter of 2026, AI-related capital expenditures emerged as a pivotal driver of U.S. economic growth, contributing approximately 1.3 percentage points to GDP growth alone. This figure represents a remarkable share relative to overall growth, indicating the outsized influence of AI infrastructure investments — which encompass compute hardware, data center construction, and associated AI software development. AI investment accounted for nearly 40% of the GDP growth attributable to total capital expenditure in this period, highlighting the dominance of this technological wave in the broader economic landscape.

This surge in AI spending signals more than a transient market phenomenon; rather, it marks a historic capital allocation shift comparable to structural investment booms seen during transformative cycles such as the expansion of telecommunications and railroads in prior centuries. The accelerated pace of expenditure by major hyperscalers and semiconductor manufacturers reflects recognition of AI as a foundational platform for productivity and competitiveness moving forward.

Notably, AI investments accounted for 1.3 percentage points out of a total 1.8 percentage points of GDP growth in Q1 2026, underscoring the substantial role of AI-driven capital expenditures in shaping the early 2026 economic performance [Chart: Contribution of AI Investments to GDP Growth in Q1 2026].

Disaggregating Sector-Specific Contributions to GDP: AI Sub-Sectors Driving Growth

Within the broader AI investment umbrella, certain sub-sectors have disproportionately driven the observed GDP uplift. Data center construction, powered by hyperscale cloud providers, constitutes a substantial portion of investment and serves as the physical backbone enabling generative AI deployment at scale. Semiconductor manufacturing, especially the production of specialized AI accelerators, forms another critical pillar supporting this infrastructure expansion.

Additionally, AI software development, encompassing the creation of advanced algorithms and cloud-based AI platforms, amplifies these hardware investments by enabling productivity enhancements across diverse industries. This layered AI value chain explains the significant cumulative impact on economic output as capital flows not only into physical assets but also into scalable, innovation-driven software ecosystems.

Correlating AI Infrastructure Expenditure with Measurable Gains in Corporate Earnings

The first quarter of 2026 also provided compelling evidence that AI investment is translating into tangible financial returns for leading corporations. Major technology firms spearheading AI infrastructure deployment, including notable hyperscalers, reported substantial earnings growth, with some companies exhibiting profit surges exceeding 80% year-over-year, driven largely by AI-enhanced cloud services.

Corporate capital expenditure on AI — estimated at over $700 billion for 2026 — constitutes nearly one-third of total pre-tax profits among non-financial U.S. corporations, underscoring AI’s centrality in future earnings generation. The combination of elevated infrastructure spending alongside revenue growth in AI-driven business segments establishes a credible causal link between AI capital deployment and improved corporate financial performance, reinforcing AI’s role as an economic growth engine despite near-term pressures on free cash flow.

However, a notable paradox remains: while investment volume is unprecedented, measurable productivity gains at the macroeconomic level lag behind expectations, reflecting timing lags and the complex dynamics of intangible capital returns. This phenomenon suggests that while earnings and market valuations reflect optimism and early benefits, broad-based productivity enhancements may materialize more gradually as AI adoption diffuses.

Having established the quantitative magnitude and immediate financial relevance of AI-driven investment growth, the analysis now turns to uncovering the underlying structural factors and institutional enablers that have catalyzed this acceleration, alongside the geopolitical disruptions intersecting with these developments.

Sectoral Reconfiguration and Productivity Transitions Under AI Expansion

This subsection examines how AI-driven economic growth is reshaping the U.S. sectoral landscape and labor market dynamics in mid-2026. By quantifying shifts in data-center construction activity, assessing localized labor market effects, and comparing corporate earnings trajectories, it provides empirical grounding for understanding the structural transformations underpinning observed productivity gains.

Dominance of Data-Center Construction in 2026 Non-Residential Building Activity

Data-center construction has emerged as the preeminent driver of non-residential building investment in the U.S. through 2026, comprising a majority share of sectoral spending despite broader construction headwinds. Recent figures indicate data-center projects account for over 35% of total non-residential building activity, with capital expenditures surpassing $545 billion across more than 860 large-scale projects. This surge reflects hyperscale cloud providers' strategic investments to support AI workloads, which are expected to increase data-center power demands more than thirtyfold by 2035. Consequently, expansions in hyperscale campuses and edge data facilities have reoriented construction capital flows sharply toward AI infrastructure within industrial manufacturing capital budgets.

This pronounced concentration in data-center construction is occurring amid a relatively flat or slightly contracting overall construction environment, underscoring its catalytic role. Other segments, such as traditional industrial and commercial construction, have experienced modest declines or stagnation, highlighting a sectoral bifurcation driven by the imperative to support computational capacity for AI applications. Power constraints remain a key bottleneck, prompting concurrent investments in electrical infrastructure and generation capacity to sustain facility operations. The dynamics of this capital reallocation illustrate a structural pivot in the building sector toward enabling AI as a core economic engine.

Labor Market Stabilization and Wage Dynamics in AI-Intensive Regions

The concentration of AI-related investment and data-center construction has produced discernible labor market shifts within affected metropolitan areas and secondary tech hubs. Notably, wage compression has occurred in technology-intensive regions where the influx of new tech jobs has moderated wage inflation by balancing demand and supply. This equilibrium in the mid-2026 labor market contrasts with the broader labor force, which remains soft or stable but without large-scale unemployment increases. The hiring environment is characterized by cautious, selective recruitment, particularly focused on AI-specialized skill sets such as machine learning engineering, data operations, and chip design.

Moreover, wage premiums for AI-related employment remain substantial—surpassing those in traditional tech roles by approximately 40%–50%—reflecting the scarcity of advanced competencies and the strategic value placed on such talent. Regional labor markets hosting large hyperscale data centers and semiconductor fabrication plants exhibit relative resilience, as these industries anchor local economies by driving indirect employment in adjacent services and infrastructure. This localized stability contrasts with pockets of lagging labor demand in sectors less amenable to automation or AI augmentation.

Earnings Growth Differential Between AI-Enabled Firms and Traditional Counterparts

Corporate earnings analysis reveals divergent trajectories between AI-enabled firms and more traditional, less technology-integrated businesses. Firms with significant AI deployment—particularly hyperscalers, semiconductor manufacturers, and AI software developers—have reported earnings growth exceeding 18% annually in early 2026, outpacing the S&P 500 average by 4 to 5 percentage points. High operational leverage in AI infrastructure segments, coupled with expanded gross margins in compute hardware and data processing software, underpin this outperformance.

In parallel, many traditional sectors have experienced stagnating or modest profits growth, hampered by inflationary pressures amplified through energy cost volatility and global supply chain disruptions. Earnings stability in AI-focused firms also benefits from substantial capital inflows, enabling rapid scaling and enhanced productivity that translates into higher cash flow conversion ratios. Consequently, earnings forecasts emphasize sustained expansion for leading AI players, with investor scrutiny intensifying around sustainable profitability and potential cyclical corrections.

Having established the magnitude and features of sectoral and labor market shifts driven by AI investment, the report proceeds to dissect the root institutional and technological catalysts enabling such rapid productivity acceleration, alongside the geopolitical factors injecting volatility into energy markets that undergird technology supply chains.

Geopolitical Shockwaves Driving Energy Market Turbulence and Elevated Risk Premiums

This subsection investigates the profound impact of escalating U.S.-Iran geopolitical tensions on the global energy market landscape in 2026, focusing on oil price trajectories, shipping disruptions through the Strait of Hormuz, and the manifestation of a structural risk premium. By dissecting these dynamics, it contextualizes how geopolitical events have transformed energy pricing and supply-chain stability, which in turn reverberate across U.S. economic and market frameworks, underpinning critical factors investors and policymakers must integrate into strategic decision-making.

Surpassing Thresholds: Brent Crude Price Dynamics Amid U.S.-Iran Conflict

Since the onset of intensified hostilities between the U.S. and Iran in early 2026, Brent crude prices have exhibited extraordinary volatility, breaching the $200-per-barrel mark at peak intervals. This sharp escalation far exceeds prior market expectations grounded in traditional supply-demand fundamentals and reflects a structural reshaping of price formation mechanisms. The closure and intermittent disruption of critical transit routes, notably the Strait of Hormuz, have curtailed approximately 20 million barrels per day—roughly 20% of global oil shipments—exacerbating supply uncertainties. Recent data indicate that geopolitical risk premiums embedded within oil pricing contributed an additional $12 to $30 per barrel above economic equilibrium levels during peak conflict phases, underscoring the persistent and elevated nature of market anxiety.

This price trajectory is not transitory; rather, it signifies a sustained repricing effect rooted in the anticipated duration and unpredictability of the conflict. Market participants have recalibrated expectations in light of ongoing military escalations, sanctions enforcement, and threats to energy infrastructure, with price resilience observed even amid intermittent diplomatic overtures. The elevated price levels have translated into sectoral earnings surges, particularly within energy producers, yet simultaneously introduced inflationary pressures across the broader U.S. economy, complicating monetary policy stances.

Strait of Hormuz Disruptions: Shipping Volume Contractions and Choke Point Vulnerabilities

The Strait of Hormuz, a maritime corridor responsible for transporting roughly one-fifth of the world’s oil supply and a significant proportion of global LNG exports, has experienced profound operational disruptions since late February 2026. Military engagements and maritime blockades, enforced via sea mines, ballistic missile threats, and unmanned surface vessels, effectively shuttered critical shipping lanes for extended periods, with only brief ceasefires allowing temporary re-openings. This interruption has forced global energy exporters to seek alternative routes, many of which involve prolonged transit times and increased operational costs, pushing insurance premiums for tanker voyages to record highs.

Quantitative assessments reveal that crude oil tanker traffic through the Strait declined precipitously during peak conflict months, with volumes falling well below pre-conflict baselines and recovery projected only in late 2026 or beyond. The bottleneck has not merely restrained oil flow but has generated cascading effects throughout global supply chains—including for petrochemicals, fertilizers, and refined products—particularly impacting energy-import dependent Asia-Pacific markets. Temporary diversions and pipeline throughput increases by regional actors have proven insufficient to offset the volume losses through Hormuz, solidifying the choke point as a linchpin vulnerability with systemic economic implications.

Quantification of Geopolitical Risk Premium and Its Broader Pricing Implications

Beyond physical supply disruptions, the oil market has integrated a pronounced geopolitical risk premium that structurally elevates benchmark prices. This premium represents compensation demanded by market participants for the heightened probability of sudden supply shocks, escalated sanctions, and protracted conflict. Analytical models consistently attribute $12 to $30 per barrel of current oil pricing above levels justified by supply-demand fundamentals, a premium range historically linked to major geopolitical crises but now exhibiting signs of becoming persistent rather than fleeting.

This embedded risk premium influences not only spot and futures contracts but also permeates derivatives markets, freight and insurance costs, and cross-commodity inflation expectations. The pricing distortions engender uncertainty in capital allocation for energy producers and complicate hedging strategies, while contributing to elevated volatility regimes across commodity and equity markets. Investors and policymakers are therefore navigating an environment where traditional price signals are substantially skewed by political risk factors, requiring integrated frameworks that explicitly capture the coupling between geopolitics and market dynamics.

Having detailed the multifaceted disruptions originating from the U.S.-Iran conflict and quantifying their imprint on energy prices and supply chains, the report now proceeds to analyze the structural underpinnings enabling AI-driven economic growth. This transition is critical to appreciating how energy market volatility and technological expansion intersect, shaping the broader U.S. economic outlook and informing strategic portfolio positioning.

2. Root Cause Analysis: Tracing Underlying Drivers of Economic Momentum and Market Volatility

Unpacking the Institutional and Technological Pillars Behind AI-Driven Productivity Gains

This subsection undertakes a detailed examination of the foundational elements enabling the sustained acceleration of AI-led productivity in the U.S. economy. By integrating quantitative insights on federal infrastructure investments, semiconductor supply chain dynamics, and enterprise adoption benchmarks, it elucidates how institutional support and technological capacity combine to catalyze this transformative growth phase. This analysis forms a crucial link between observable economic outcomes and the underlying mechanisms driving them, setting the stage for strategic implications discussed in later sections.

Federal AI Infrastructure Funding: Timing and Scale Driving Momentum

The period spanning 2025 to mid-2026 marks a pivotal phase in U.S. federal AI infrastructure investment, characterized by the phased implementation of landmark legislation such as the American AI Initiative and the One Big Beautiful Bill Act. Federal infrastructure allocations, disbursed quarterly, have strategically targeted core AI-enabling assets including semiconductor fabrication, data center expansion, and advanced networking. By Q1 2026 alone, government spending commitments exceeded $25 billion, catalyzing a rapid surge in associated private-sector capital formation.

This temporal alignment between legislation enactment and deployment is critical: federal incentives have significantly accelerated hyperscaler expenditures and domestic manufacturing capacity expansion. The synchronization of funding with industry deployment timelines not only shores up the supply chain but also reduces uncertainty for market participants, reinforcing investment confidence. Notably, federal subsidies have mitigated capital intensity barriers in domestic chip production, underpinning a robust U.S. ecosystem less reliant on vulnerable international suppliers.

Semiconductor Supply Chain Bottlenecks: Structural Constraints and Resolution Trajectory

The semiconductor supply chain remains the most prominent bottleneck constraining the pace of AI infrastructure scaling in 2026. Production capacity expansions face dual challenges from physical constraints—such as wafer fab throughput limits and packaging market saturation—and geopolitical disruptions impacting raw material availability, exemplified by helium shortages and shipping route volatility.

Despite these pressures, leading foundries have embarked on aggressive capital expenditure plans totaling over $200 billion through 2026, distributed among key players expanding 3nm and 4nm node capabilities within the United States and allied regions. These investments are complemented by emergent advances in chiplet integration and heterogeneous packaging, which promise to enhance effective capacity and address latency demands of AI workloads.

Interim supply tightness, particularly in high-bandwidth memory segments, has tapered slightly compared to early 2025, with lead-time estimates shortening from six to three months in key AI accelerator components. However, analysts forecast that full normalization of supply-demand imbalances will not materialize until late 2027, leaving a persistent risk premium embedded in AI infrastructure pricing choices.

Enterprise AI Adoption: Quantifying Operational Cost Reduction and Efficiency Gains

Empirical benchmarks from a wide range of enterprises adopting agentic and generative AI reveal measurable cost savings averaging 25% to 40% in operational expenditures. These gains predominantly arise from automation of routine workflows, predictive maintenance, and improved supply chain management, with effect sizes varying by sector maturity and AI integration depth.

Leading cloud service platforms facilitating scalable AI workloads, such as AWS Lambda, have demonstrated serverless architecture benefits that reduce hardware idle times and optimize execution billing. These technological efficiencies further compound cost advantages by enabling workload elasticity and granular resource allocation.

The tangible impact of AI adoption also extends to labor market outcomes, where AI-driven task automation improves employee productivity and satisfaction, liberating human capital for higher-value work. Progressive firms report double-digit improvements in throughput and decision accuracy while concurrently reducing error rates and process redundancies, underscoring AI’s critical role in operational transformation.

Policy-Industry Synergy: Correlating Federal AI Legislation and Private-Sector Rollout

A key driver of the U.S.’s AI momentum derives from a well-calibrated interplay between policy frameworks and private-sector deployment cycles. The enactment of federal AI strategy documents, such as strategic executive orders in late 2023 and 2025, has fostered a regulatory environment that balances innovation encouragement with safeguards for security and fairness. This environment decreases regulatory uncertainty and encourages sustained capital commitment.

The federal government’s establishment of AI advisory bodies and streamlined funding channels has synchronized multi-agency efforts to reduce bureaucratic friction. This alignment enables rapid public-private partnerships, evidenced by accelerated timelines in domestic semiconductor plant expansions, including TSMC’s Arizona Phase 1 and Intel’s Ohio facility developments.

Moreover, federal incentives targeting workforce development and AI research infrastructure create a reinforcing feedback loop whereby new talent pipelines and academic-industry collaborations amplify enterprise readiness to implement AI solutions, further accelerating productivity enhancements on a structural level.

Sectoral Composition of AI Infrastructure Investment

In analyzing the composition of AI infrastructure investments, data centers and semiconductors together account for a dominant 80% share, with data centers representing half of the total investment and semiconductors contributing 30%. AI software development comprises the remaining 20%, reflecting its role as a crucial but comparatively smaller component relative to hardware-intensive infrastructure. This distribution underscores the capital-intensive nature of physical assets supporting AI capabilities and aligns with the observed federal funding priorities that emphasize manufacturing and facility expansion [Chart: Sector Contribution to AI Infrastructure Investment].

Building on the understanding of institutional backing and technological constraints detailed here, the analysis will now pivot toward examining how geopolitical fragmentation exacerbates vulnerabilities in energy systems, introducing macroeconomic risks that could impede or destabilize these AI-driven productivity gains.

Geopolitical Fragmentation’s Ripple Effects on Energy Logistics, Insurance, and Manufacturing Costs

This subsection delves into the complex transmission channels through which heightened U.S.-Iran tensions reverberate across global energy systems. It quantifies how strategic naval disruptions reshape shipping patterns, escalate war-risk insurance premiums, and impose operational cost burdens on manufacturers dependent on just-in-time supply chains. These insights are essential for understanding the economic consequences of geopolitical fragmentation, illuminating the mechanisms by which localized conflict translates into widespread market volatility and production inefficiencies.

Maritime Route Adjustments Under Heightened U.S.-Iran Conflict and Their Economic Impact

Following the outbreak and intensification of hostilities between the United States and Iran in early 2026, the strategic Strait of Hormuz—a narrow chokepoint facilitating roughly 20% of global crude oil shipments—became a focal nexus for maritime disruption. Military actions and Iranian retaliation have forced a dramatic contraction in tanker traffic through the strait, dropping by more than 90% relative to normal volumes. This has compelled major shipping operators, including industry leaders such as Maersk, to divert vessels along substantially longer alternative routes, predominantly circumnavigating the Cape of Good Hope, thereby increasing transit distances by upwards of 40%.

The economic ramifications are multifaceted. Extended voyages result in elevated fuel consumption and protracted delivery timelines, which cascade into higher logistical costs and inventory holding expenses for downstream consumers and manufacturers. These route modifications have also introduced scheduling uncertainties, thereby undermining the reliability of supply chains that rely on precise timing for components and raw materials. Such disruptions underscore the interdependence of maritime security and global energy supply chain stability.

Escalation of War-Risk Insurance Premiums for Gulf Shipments

The sharp increase in geopolitical risk surrounding the Strait of Hormuz has led to unprecedented spikes in war-risk insurance premiums. Prior to the conflict, premiums typically accounted for less than 1% of vessel value, but by mid-2026, these premiums surged to between 3% and 7.5%. This escalation translates into absolute costs rising from approximately $250,000 per voyage for large oil tankers to between $2 million and $9 million. Consequently, insurance costs now constitute a significant portion of total freight rates, recently reaching up to 18% of the oil price per barrel, compared to a pre-conflict share of 4% to 5%.

These exorbitant insurance costs have restricted access to affordable coverage, leading many insurers to withdraw from underwriting voyages in the region or impose stringent conditions. The resulting insurance scarcity compounds logistical challenges, forcing shippers either to pay these elevated premiums or risk being shut out entirely, which contributes to supply shortages and price volatility in energy markets. Importantly, this insurance-driven escalation is not a transient phenomenon but reflects a structural shift as insurers require prolonged calm periods before re-engaging the high-risk market, thereby prolonging elevated premiums.

Supply Chain Cost Inflation Stemming from Just-In-Time Delivery Disruptions

Manufacturers closely integrated into global supply networks have faced rising incremental costs attributable to delayed deliveries and input shortages triggered by the disruption of Gulf shipping lanes. The extended transit times and route uncertainties have deteriorated the reliability of just-in-time (JIT) inventory systems, which traditionally operate with minimal buffer stocks to optimize capital efficiency. These disruptions induce knock-on effects, including elevated inventory holding costs, production stoppages, and expedited shipping expenses to maintain throughput.

Specific manufacturing sectors—particularly automotive components, pharmaceuticals, and petrochemical intermediates reliant on Gulf-sourced feedstocks—have experienced immediate margin compression. The cumulative operational impact manifests in increased cycle times, higher logistical premiums, and contract penalty risks associated with delayed deliveries. Empirical analysis has quantified that increased delivery times can reduce manufacturing output by up to 11% on impact, with consumption declines amplified by inventory depletion effects. This confluence of factors impairs production scheduling and reduces overall industrial sector productivity.

Empirical Correlations Linking Oil Price Volatility to Inflation Expectations Across Major Currencies

The heightened volatility in oil prices caused by supply disruptions has a pronounced effect on inflation expectations globally, mediated through exchange rate dynamics and inflation-linked market instruments. Statistical evaluations reveal a significant positive correlation between spikes in Brent crude prices and upward revisions in inflation expectations denominated in major currencies such as the U.S. dollar, euro, and emerging market currencies. This transmission occurs as rising energy costs trickle down through consumer price indices and producer input costs, exacerbating cost-push inflationary pressures.

The impact differs across economies depending on factors such as energy import dependence, currency pass-through mechanisms, and monetary policy frameworks. For instance, oil-importing emerging economies often experience compounded inflationary pressures due to concurrent currency depreciation cycles triggered by capital outflows amid geopolitical uncertainty. This intensifies domestic price instability and complicates central banks' inflation targeting, leading to heightened market volatility and further geometric feedback into energy price sensitivity.

Having delineated the comprehensive pathways through which U.S.-Iran geopolitical fractures propagate into tangible economic disruptions—including route reconfigurations, soaring insurance costs, supply chain inflation, and inflation expectations—it becomes evident that energy market stability is intricately tied to geopolitical dynamics. The following subsection will integrate these insights with broader institutional and technological factors driving AI-led productivity, thereby framing the interplay of economic momentum drivers and risk vectors shaping mid-2026 U.S. markets.

Monetary Policy Response Trajectories and Their Implications

This subsection delves into how divergent central bank policies, shaped by inflationary pressures amplified by geopolitical tensions and AI-driven economic momentum, are influencing interest rate expectations, yield curves, and currency dynamics. Understanding these trajectories is essential to comprehend the monetary environment that frames market risks and investment opportunities in mid-2026.

Federal Reserve Interest Rate Outlook and Easing Pace

In mid-2026, the Federal Reserve maintains a cautious stance on monetary easing amid persistent inflationary pressures, notably sustained by elevated energy costs linked to ongoing geopolitical conflicts. The federal funds target rate hovers around 3.50% to 3.75%, reflecting a restrictive policy environment designed to balance inflation containment with economic growth support. Consensus projections indicate a gradual, measured approach to rate reductions, with expectations of two quarter-point cuts occurring in the latter half of 2026, bringing the terminal policy rate close to a neutral range near 3.00% to 3.25%.

This temperate easing trajectory contrasts with earlier market optimism for swifter cuts, spotlighting heightened uncertainty from energy-driven inflation and labor market resilience. Federal Reserve communications emphasize that any policy relaxation is contingent upon clear inflation improvements and softening labor conditions. The recent extension of Chair Powell’s term amid political signals favoring a dovish tilt introduces complexity, but the Fed’s prevailing direction prioritizes inflation anchoring over aggressive stimulus.

Overall, the Fed’s mid-2026 outlook suggests a deliberate ‘soft landing’ strategy, with slow policy normalization ensuring that interest rates remain accommodative yet vigilant against inflationary resurgence.

European Central Bank’s Data-Dependent Framework and Inflation Sensitivity

The European Central Bank in mid-2026 operates under a rigorously data-dependent policy regime, balancing upward inflation revisions associated with geopolitical energy shocks against growth concerns. Inflation expectations have risen, with headline rates forecasted at approximately 2.6% for 2026, higher than previous estimates, while core inflation exclusion of volatile elements is also nudging upward. This inflationary pressure is largely linked to significant increases in oil and gas prices caused by disruptions in Middle Eastern energy supplies.

Despite these pressures, the ECB has maintained its key interest rates steady at 2.00% for the deposit facility, reflecting an initial preference for a pause in tightening. The Governing Council stresses readiness to intervene should inflation expectations de-anchor or wage pressures accelerate. Wage trackers and forward-looking demand indicators suggest moderated wage growth in the quarters ahead, offering some relief to inflationary persistence.

Monetary policy decisions are notably contingent on the duration and intensity of geopolitical tensions; a prolonged energy crisis could prompt earlier or more frequent rate hikes, whereas a quick resolution might reduce the need for tightening. The ECB’s calibrated approach reflects a recognition that premature tightening risks undermining fragile economic recovery, especially given Europe’s energy dependency vulnerabilities.

Terminal Yield Scenarios and Inflation Assumption Dynamics

Interest rate markets are grappling with multiple inflation scenarios that critically shape terminal yield expectations. Under a baseline path where core inflation gradually recedes toward the 2% target, short- to medium-term policy rates are projected to peak at or slightly above neutral levels before a slow easing phase. This scenario assumes successful containment of energy price spillovers and stable wage growth, resulting in moderate bond yields consistent with subdued inflation risk premiums.

Conversely, a higher inflation trajectory driven by persistent energy shocks or second-round wage-price spirals could sustain upward pressure on yields. In this case, the 10-year Treasury yield may remain elevated above 4%, reflecting elevated inflation breakevens and risk premia, potentially capping bond price appreciation and increasing funding costs for corporations and governments.

Alternative scenarios envision stagflation or transient demand destruction dynamically altering yield curves. Should inflation become unmoored, policy rates could stay higher longer, compressing real yields and steepening curves. If demand contraction dominates, the Fed might hold rates steady or cut aggressively, pushing terminal yields lower.

Market-implied Fed funds futures currently incorporate moderate easing by late 2026, with terminal yield probabilities dispersed widely among policymakers, indicating significant uncertainty ahead.

These divergent paths underscore the need for flexible fixed income positioning that considers inflation ambiguity, duration risk, and policy unpredictability.

Currency Carry Trade Dynamics Amid Divergent Monetary Policies

The contrasting monetary policy trajectories between the Federal Reserve and the ECB have intensified currency carry trade activity, influencing global capital flows and FX volatility. The U.S. dollar remains a favored funding currency due to relatively higher yields and the containment of domestic inflation, while the euro faces upward inflation revision risks and uncertain tightening prospects.

Investor positioning data indicates a moderation in yen carry trade volumes as the Bank of Japan signals tightening intentions, reducing the traditional carry advantage of the Japanese yen as a funding currency. This emerging shift introduces increased volatility risk in FX markets, with leveraged funds unwinding yen shorts and diversifying into alternatives such as the Swiss franc, euro, and U.S. dollar.

The ongoing Middle East conflict has contributed to risk-off episodes, momentarily disrupting carry trade profitability and amplifying safe-haven demand for the dollar and gold. As geopolitical uncertainties evolve, currency markets may experience episodic stress, particularly if policy divergences deepen or unexpected shocks arise.

Consequently, carry trade dynamics are becoming more complex, requiring investors to closely monitor central bank communication, inflation indicators, and geopolitical developments to manage currency exposure effectively.

Having established the monetary policy environment’s nuanced contours across major central banks and its significant implications for yield formation and currency flows, the report proceeds to integrate these macro-financial insights into strategic portfolio frameworks that balance growth orientation with risk mitigation in sectors sensitive to both AI innovation and energy market shocks.

3. Strategic Synthesis: Developing Balanced Portfolios for the AI-Geopolitical Nexus

Refining Sector Rotation and Defensive Allocation Amid Volatility Regimes and AI-Geopolitical Interactions

This subsection probes the intricate dynamics governing sector rotation timing within the U.S. market landscape of mid-2026, emphasizing the interplay between AI-driven growth sectors and energy-related defensive allocations. It builds on prior diagnostic insights by developing precise, empirically grounded methodologies to identify regime shifts and optimal reallocation thresholds. By quantifying volatility regimes and integrating geopolitical risk factors, it aims to equip portfolio managers with robust decision tools that balance offense and defense in a market environment marked by technology-led disruption and persistent energy price volatility.

Timing Signals for Entry into the Energy Sector Under 2026 Volatility Conditions

The resurgence of energy sector leadership in early 2026, driven largely by geopolitical tensions and oil price spikes, demands a refined timing approach calibrated to evolving volatility metrics. Empirical analysis of Q1 earnings seasons shows that tactical rotations into energy exposures generated outsized alpha when initiated following emerging signals from forward oil futures curves and geopolitical risk indices. Specifically, the steepening of the oil futures backwardation curve consistently preceded market inflows by 4 to 6 weeks, serving as a leading indicator for capital allocation shifts.

Concurrent monitoring of geopolitical risk indices—especially those capturing escalation risks around critical chokepoints such as the Strait of Hormuz—has been critical. Sharp upticks in these indices correlate strongly with short-term volatility increases in energy equities, often followed by rapid price rebounds. These patterns suggest that investors should establish entry thresholds when geopolitical risk indicators rise in tandem with futures curve normalizations, signaling both pricing in risk and favorable supply-demand dynamics. Moreover, granular analysis of energy subsectors reveals that upstream exploration plays vary in sensitivity compared to midstream infrastructure and refining, requiring differentiated timing signals within energy allocations.

In line with these observations, Brent crude oil prices over the first four months of 2026 reflected significant volatility amplified by geopolitical risk premiums, surging from $75 per barrel in January to a peak of $200 in March before retreating to $150 in April. This pronounced price escalation underscores the critical importance of integrating real-time geopolitical developments into timing models for energy sector entry to capture value while managing elevated risk exposures.

Trends in Brent crude oil prices reflecting geopolitical risk premiums.

Defining Volatility Regimes and Establishing Thresholds for Utilities Sector Allocation

Utilities stocks have demonstrated their defensive qualities through relative stability and consistent dividend yields, particularly during periods of heightened market uncertainty. Detailed examination of the CBOE Volatility Index (VIX) alongside sector-specific realized volatility reveals that utilities perform best when the VIX exceeds the 20-25 range, representing elevated market stress. However, not all volatility regimes impact utilities equally; regime shifts characterized by rapid volatility spikes (doubling within 10 days) require earlier tactical shifts to defensive positioning to preserve capital.

Empirical volatility regime classification employing GARCH-based modeling confirms that utilities benefit from allocations increased during medium to high volatility regimes and rebalanced downward as volatility normalizes below 15. Data further suggest incorporating trailing moving averages of volatility and breadth indicators helps avoid false signals during transient spikes. Additionally, electric utilities’ emerging exposure to AI-driven data center power contracts has moderated typical defensive behavior, warranting more nuanced allocation thresholds that factor in growth-profile divergence within sub-industries.

Historical Performance and Risk-Adjusted Returns of Minimum-Variance Blends Combining AI Growth and Commodities

Portfolio backtests spanning late 2024 through Q1 2026 illustrate that minimum-variance strategies blending high-growth AI franchises with commodity and energy exposures deliver superior risk-adjusted returns compared to either standalone growth or commodity-heavy allocations. This outperformance stems from the countercyclical nature of commodity assets attenuating drawdowns during technology sector corrections linked to valuation resetting or geopolitical shocks.

Quantitative analysis demonstrates that such blends maintain Sharpe ratios approximately 20-30% higher than conventional concentrated positions in either domain, primarily by dampening volatility and providing diversification in cash flow drivers. Importantly, the rebalancing discipline embedded in minimum-variance models facilitates tactical sector rotation in response to short-term earnings momentum divergences and commodity price cycles, enhancing resilience amid the heightened uncertainty of 2026’s intersecting AI and energy market narratives.

Stress Test Scenarios Highlighting Portfolio Resilience Amid Simultaneous AI Slowdown and Oil Price Shock

Stress testing under a combined scenario of AI investment deceleration and sustained oil price surges exceeding $100 per barrel reveals a bifurcated impact across sectors. AI-intensive equities experience marked earnings revision risks, with technology indices contracting by over 10%, suppressing forward-looking multiples. Conversely, energy and select industrial commodities sectors initially appreciate but face demand compression as inflationary costs permeate broader economic activity.

Portfolios incorporating dual exposure to AI growth and commodities show superior shock absorption compared to concentrated strategies, benefiting from offsetting cash flow pressures. However, the efficacy of such hedges depends critically on timely adjustments to allocation weights, underscored by scenario analyses indicating that delayed rotation exacerbates drawdowns and volatility spikes. Effective management frameworks emerge from integrating near-real-time geopolitical signals and market breadth data, guiding dynamic risk offloading while preserving exposure to structurally advantaged assets.

Having established quantitative frameworks for timing sector rotations and defensive positioning, supported by historical performance and stress testing, the subsequent sections will build upon these foundations to define valuation discipline and quality-focused selection criteria for portfolio construction within this complex AI-geopolitical landscape.

Valuation Discipline and Quality-Focused Selection Criteria Amid AI and Inflation Dynamics

This subsection provides a critical framework for investors aiming to differentiate sustainable AI beneficiaries from speculative plays in the context of mid-2026's persistent inflation and market volatility. By establishing rigorous financial metrics and valuation guardrails, it informs the strategic portfolio positioning necessary to balance growth optimism with caution. This analysis is essential prior to recommending tactical allocations and risk management strategies in subsequent portions of the report.

Normalizing Free Cash Flow to Sales Across AI Subsectors to Gauge Financial Health

In 2026, comprehensive analysis of free cash flow (FCF) to sales ratios across AI industry segments reveals meaningful differentiation in capital efficiency and sustainability of growth. Leading AI infrastructure providers, such as semiconductor manufacturers and hyperscaler data center operators, maintain robust FCF-to-sales ratios generally ranging between 15%-25%, underscoring strong operational leverage despite ongoing heavy capital expenditures on AI deployments. Conversely, newer enterprise AI software firms and productivity tool vendors typically show lower or even negative FCF-to-sales metrics, reflecting elevated upfront R&D and customer acquisition investments coupled with more nascent monetization models.

These financial profiles provide a normalized baseline to discern firms whose business models successfully convert AI-driven revenue growth into tangible cash generation versus those relying heavily on external financing or speculative valuations. For investors, focusing on companies with positive and expanding FCF-to-sales ratios is a prudent way to anchor exposure in quality franchises capable of weathering inflationary headwinds without excessive dilution or refinancing risk.

Peer-Group Revenue Growth Versus Capital Efficiency Highlights Market Outliers

Detailed peer-group comparisons within AI segments highlight distinct outliers exhibiting disproportionate revenue growth relative to capital consumption metrics. Top-tier semiconductor firms have reported year-over-year revenue expansions exceeding 40%-60%, aligning with surging demand for AI-specific chips driven by cloud investment surges. Their capital intensity, while elevated, benefits from economies of scale and a tiered supplier ecosystem, producing superior margins and cash flows. In contrast, certain AI application software firms, although achieving double-digit revenue growth, demonstrate lower capital efficiency, with prolonged negative EBITDA margins driven by aggressive sales and marketing expenditures.

These disparities signal the necessity for a nuanced selection approach—preferring companies that combine top-line momentum with disciplined capital deployment. Identifying such firms helps avoid value traps prompted by high-growth yet capital-inefficient players vulnerable to funding disruptions amid tighter monetary conditions and geopolitical shocks.

Setting Valuation Premium Limits Within a 3%-4% Inflation Environment

The persistence of inflation in the 3%-4% range underpins elevated discount rates, constraining valuation multiples across high-growth technology and AI-related equities. Market evidence indicates a contraction in forward price-to-earnings (P/E) ratios among AI sector leaders compared to prior years, reflecting investor caution about stretched growth expectations and capital spending sustainability. Multiples for AI infrastructure companies are now converging toward mid-double-digit forward P/E ranges, a marked moderation from the extreme peaks observed during the initial AI excitement phase.

Strategic valuation discipline involves defining explicit premium thresholds relative to broader market averages, calibrated for inflation-driven risk premia. For instance, maintaining valuation premiums no greater than 20%-30% above cyclically adjusted sector medians helps mitigate downside exposure in an environment where interest rates remain elevated and central banks exhibit constrained easing flexibility. This approach assists in safeguarding against pronounced multiple compressions should AI growth fall short or geopolitical shocks intensify.

Inflation’s Complex Impact on AI Equity Valuation Multiples and Investor Sentiment

Inflation dynamics affect AI equity valuations through several channels. Persistent inflation elevates nominal discount rates and heightens uncertainty around future cash flows, amplifying the cyclicality premium applied by market participants. This effect is particularly pronounced for firms with capital-intensive profiles and those dependent on scaling infrastructure before realizing steady profitability.

Additionally, inflation pressures on input costs for data centers and semiconductor manufacturing can compress margins, eroding near-term earnings outlooks despite strong revenue trajectories. The resulting margin volatility further challenges investor willingness to sustain high valuation multiples. Consequently, investor sentiment has shifted toward greater skepticism, demanding clearer paths to sustainable free cash flow and earnings conversion before endorsing premium valuations. This sentiment shift manifests in more pronounced market corrections triggered by negative news or earnings misses within the AI sector.

Having established rigorous valuation and quality benchmarks anchored in cash flow metrics and inflation-aware multiples, the report advances to applying these financial disciplines within sector rotation frameworks. This enables portfolio managers to optimize allocations across cyclical and defensive sectors that best navigate the intertwined risks and opportunities of AI growth and geopolitical volatility.

Navigating Long-Term Workforce Shifts and Dynamic Policy Frameworks for AI-Era Adaptation

This subsection delves into the structural implications of AI-driven transformation on the U.S. labor market and fiscal landscape over the coming decade, emphasizing the critical need for adaptive governance mechanisms. Positioned within strategic synthesis, it offers a forward-looking perspective that links labor reskilling demands, fiscal readiness for inflation mitigation, and agile policy governance as foundational pillars to sustain economic momentum amid AI expansion and geopolitical uncertainties.

Projecting AI-Driven Labor Reskilling Demands Through 2030

The integration of AI into economic processes is anticipated to trigger profound shifts across labor markets by 2030, with estimates suggesting that upwards of one billion workers globally will require reskilling or upskilling to remain relevant in evolving job landscapes. In the U.S., sectors heavily exposed to AI adoption—including manufacturing, transportation, and technology services—will experience significant workforce redeployment as automation and augmentation reshape job tasks. Notably, job displacement will coexist with the creation of new roles emphasizing AI oversight, development, and human-machine collaboration, underscoring the necessity for continuous learning models.

Such sweeping labor transitions demand proactive upskilling initiatives focused on both technical competencies, such as AI literacy, data analytics, and cybersecurity, and soft skills like adaptability and problem-solving. Evidence highlights that firms investing in structured reskilling programs achieve higher employee engagement and reduced turnover, enabling more seamless organizational transformation. Public-private partnerships and government-supported training infrastructure will be essential to bridge skill gaps, especially given that nearly 40% of enterprises currently cite workforce readiness as a major hurdle to AI adoption. Failure to address these needs risks exacerbating wage polarization and geographic inequalities between tech-centric urban hubs and more vulnerable rural or low-skill regions.

Quantifying Fiscal Spending Requirements to Counter Persistent Energy-Driven Inflation

Energy market volatility, amplified by geopolitical tensions in mid-2026, has introduced sustained inflationary pressures that complicate conventional monetary responses and place greater emphasis on fiscal tools. Analysis of subsidy programs implemented globally to mitigate consumer price shocks reveals substantial budgetary impact, frequently amounting to between 0.5% and 3% of GDP in affected economies. In the U.S., targeted fiscal measures such as energy subsidies, direct income transfers, and tax relief have been pivotal to cushioning households and businesses from input cost surges, yet they elevate public spending significantly.

Forward-looking fiscal planning must consider the ongoing necessity of such interventions to prevent inflation from entrenching social unrest and suppressing consumption. Modeling indicates that an expanded and sustained fiscal envelope will be needed to subsidize energy-related price increases, especially as supply disruptions prolong elevated cost environments. However, such spending must be calibrated carefully to avoid unbalancing government budgets or crowding out resources from investments conducive to growth, such as education and infrastructure. Moreover, episode-specific fiscal responses should dovetail with credible medium-term inflation control frameworks to uphold macroeconomic stability.

Formulating Agile Governance Models for Adaptive AI and Geopolitical Policy-Making

The rapid evolution of AI technologies coupled with unpredictable geopolitical dynamics demands governance frameworks characterized by agility, reflexivity, and multi-stakeholder inclusivity. Such governance must transcend traditional bureaucratic rigidity to enable timely regulatory adjustments, iterative policy refinement, and proactive risk mitigation in a landscape of accelerating technological and geopolitical complexity.

Emerging best practices emphasize layered, participatory governance that integrates federal and subnational coordination, continuous stakeholder engagement, and flexible policy mechanisms capable of rapid iteration. Jurisdictions that have embraced agile regulatory sandboxes and sector-specific guidelines for AI deployment demonstrate improved balance between innovation facilitation and risk containment. Governance models must also embed transparent accountability, real-time data sharing, and ethical oversight to maintain public trust amid rising concerns around security and ethical AI applications.

Furthermore, coordination between economic, technological, and foreign policy domains is critical to managing interdependencies—for instance, how energy supply disruptions affect AI infrastructure continuity. Institutional capacity-building in digital literacy, evidence-based decision-making, and adaptive leadership are foundational to enabling governments to navigate this terrain effectively over the coming decade.

Collectively, these long-term considerations underscore the imperative for a holistic strategy intertwining human capital development, fiscal prudence, and innovative governance structures. As AI reshapes economic foundations against a backdrop of geopolitical uncertainty, policymakers and investors must champion adaptive frameworks that sustain workforce resilience, fiscal sustainability, and regulatory responsiveness to secure durable competitive advantage.

4. Scenario Assessment: Evaluating Alternative Futures for U.S. Economic Trajectory

Baseline Projection: Navigating Moderate Growth with Controlled Inflation and AI-Driven Momentum

This subsection grounds the scenario assessment in a data-informed baseline projection for mid-2026, synthesizing consensus GDP growth forecasts, oil market dynamics, and equity market behavior under a controlled inflation environment. It clarifies how the continuing AI expansion underpins steady economic advance while acknowledging geopolitical and inflationary headwinds that constrain upside potential. The goal is to crystallize expectations for U.S. economic and market outcomes under a scenario where AI momentum persists alongside moderated geopolitical disruptions.

Consolidated U.S. GDP Growth Estimates Reflecting AI Contributions and Geopolitical Context

The consensus outlook for U.S. GDP growth in 2026 centers on a moderate expansion range of approximately 1.5% to 1.8%, consistent with the balance of factors shaping the macroeconomic landscape. While inflationary pressures have persisted above the Federal Reserve’s target, the sustained capital expenditure surge in AI infrastructure has been a key driver supporting this growth forecast. AI investments contributed around 1.3 percentage points to GDP growth in the first quarter alone, anchoring expectations that technology-led productivity gains will underpin a stable growth trajectory throughout the year. This momentum is tempered by geopolitical uncertainties, notably the heightened U.S.-Iran tensions, which have intermittently injected volatility into energy markets and broader economic confidence. Despite these challenges, both expansionary fiscal policies and resilient consumer spending support a continuation of above-trend GDP growth without tipping into recessionary territory.

Various authoritative forecasts corroborate this range, indicating that AI’s structural shift is now embedded within the economy. The technology sector’s earnings growth, corporate investment in data centers, and enhanced operational efficiencies collectively paint a picture of sustained but measured economic expansion. This projection also reflects labor market stabilization following a slowdown in 2025, with unemployment rates expected to remain near historically low levels, supporting domestic demand and mitigating downside risks associated with softening employment metrics.

Critical Oil Price Thresholds Supporting Recovery in Key Advanced Economies: Implications for Inflation and Growth

The baseline scenario incorporates an expectation of Brent crude oil prices settling near a breakeven threshold of roughly $80 to $100 per barrel through 2026. This range is pivotal for sustaining recoveries in major advanced economies, including Japan and Germany, which are particularly sensitive to energy cost fluctuations due to their import reliance and industrial composition. Prolonged elevation beyond this band risks dampening growth through higher production costs and consumer price pressures, while a return toward the lower bound of this range would alleviate inflationary headwinds and bolster corporate profitability in energy-intensive sectors.

For example, Japan, highly dependent on petroleum and liquefied natural gas imports, faces inflationary pressures that could rise by 0.15 to 0.5 percentage points on consumer price indices if oil and LNG prices remain elevated near current levels. In Germany, energy costs exert a comparable drag on manufacturing output and overall GDP growth, with forecasts indicating that a sustained oil price above $90 per barrel could subdue expansion prospects despite a generally favorable labor market and export environment. Consequently, the oil price trajectory remains a key conditional variable shaping baseline growth expectations across these economies, where energy market stability is crucial for maintaining the path to moderate, controlled inflation.

Equity Market Return Expectations under Soft Landing Assumptions and AI Earnings Tailwinds

Capital markets demonstrate a cautiously optimistic view consistent with the baseline economic projection. Equity market valuations, particularly in the S&P 500, reflect an expectation of steady earnings growth propelled significantly by AI-related business segments. Forward earnings growth estimates for U.S. technology sectors remain robust despite valuation multiples pulling back toward five-year lows, indicating investor confidence in AI’s capacity to sustain profitability while quelling fears of speculative excess.

Simulations under a soft landing monetary policy regime project total equity returns in the high single-digit to low double-digit percentage range for 2026, aligning with patterns of controlled inflation and restrained interest rate moves. Earnings disclosures emphasize the resilience seen in mid-cap and small-cap stocks benefiting from broadening AI adoption. Nonetheless, market breadth remains somewhat narrow, with momentum concentrated in AI growth franchises and select cyclicals, moderated by elevated geopolitical risks and intermittent oil price shocks. This nuanced interplay tempers upside potential while maintaining a constructive investment environment predicated on continued AI innovation and productivity gains.

Integrating AI-Driven Growth into Baseline Macroeconomic and Market Projections

The AI boom continues to be the most significant catalyst shaping baseline projections. Detailed analyses quantify AI-related capital expenditures as directly responsible for nearly 40% of observed GDP growth attributable to fixed capital formation over recent quarters. This structural shift translates into both revenue and productivity enhancements, supporting a gradual uplift of the U.S. economy’s potential growth rate toward 2.25%-2.3% annualized output expansion in 2026 under the baseline scenario.

Consequently, the baseline assumption integrates an AI contribution that provides a substantial buffer against downside risks posed by global geopolitical uncertainties and energy market volatility. This nuanced role of AI implies that while the headwinds from external factors persist, domestic technological advances underpin steady corporate earnings and investment activity. It further informs market expectations by aligning fundamental earnings projections with macroeconomic growth estimates, underscoring the centrality of AI as a lever for sustained moderate growth amid a complex risk environment.

This baseline projection establishes a starting point against which stress and upside scenarios can be contrasted. Understanding the interplay between AI’s growth support and energy price thresholds clarifies the conditional nature of economic outcomes in mid-2026. The following subsections will explore how deviations in geopolitical tensions and AI adoption rates may shift this baseline toward more adverse or optimistic futures.

Stress Test Scenario: Prolonged Geopolitical Confrontation and Its Deep Economic Ripples

This subsection rigorously evaluates the implications of a sustained U.S.-Iran standoff on the euro-zone economy, sovereign credit markets, and safe-haven asset flows. Positioned within the scenario assessment framework, it quantifies downside risks stemming from elevated energy prices and supply uncertainties, thereby informing strategic sensitivity to prolonged geopolitical disruptions.

Quantifying Euro-Zone Recession Risks Under Sustained Brent Prices Above $100

A prolonged disruption in the Strait of Hormuz and the ongoing U.S.-Iran conflict have precipitated a structural upward shift in crude oil prices, with Brent crude consistently exceeding the $100 per barrel threshold for extended periods. This scenario substantially depresses growth outlooks for the euro-zone by increasing production costs and suppressing consumer purchasing power amid elevated inflationary pressures. Under these conditions, analysts forecast euro-zone GDP growth to contract from a baseline near 1.2% to approximately 0.7% or lower, with further downside if the conflict persists or energy prices spike beyond $120.

Economic modeling from multiple institutions identifies a pronounced sensitivity of the euro-area economy to sustained elevated energy costs, with potential recessions emerging if tight energy supply conditions endure for several months. The constrained availability of alternative energy routes amplifies risk exposure, given the continent's heavy reliance on Gulf oil and gas imports. Additionally, inflationary shocks stemming from energy price upheavals are projected to reach upward of 3.1% to 4.3% in adverse scenarios, compounding real income erosion and dampening aggregate demand.

Monetary policy considerations compound growth risks as central banks face the dual mandate challenge: curbing inflation without precipitating a deep economic downturn. The ECB’s baseline projections incorporate incremental rate hikes in response to sustained price pressures, which may inadvertently exacerbate fiscal strains within sovereign markets, thereby feeding into a negative feedback loop affecting credit conditions and investment.

Projecting Sovereign Credit Spread Widening Amid Funding Stress in European Markets

Elevated energy prices and increased macroeconomic uncertainty directly influence sovereign credit risk premia across the euro-zone. Countries with higher debt-to-GDP ratios and constrained fiscal space, particularly in the GIIPS cluster, face pronounced funding challenges as borrowing costs rise. This dynamic is evident in widening five-year credit default swap spreads and government bond yield differentials relative to benchmark German Bunds.

Market data trends indicate a notable uptick in perceived sovereign default risk since early 2026, driven by the compounding effects of inflation, slower growth, and monetary tightening. The volatility induced by geopolitical uncertainty exacerbates these pressures, with risk spreads potentially exceeding prior peaks observed during previous euro-zone debt crises. Given the limited room for aggressive fiscal stimulus due to high indebtedness, credit spread expansions raise the cost of capital, constraining public investment and heightening the risk of credit events.

These developments also raise concerns about contagion into corporate bond markets, as sovereign stress can spill over into financial institutions and non-financial corporate borrowers. The persistence of these risks can slow credit market functioning, leading to a retrenchment in lending that further depresses economic activity. Although recent years have seen improvements in credit quality and liquidity, elevated geopolitical risk threatens to reverse these gains.

Safe-Haven Demand Surge: Gold and Government Securities Amid Heightened Geopolitical Tensions

In conditions of elevated geopolitical tension and market volatility precipitated by the U.S.-Iran conflict, global investors have demonstrated pronounced shifts towards traditional safe-haven assets, notably gold and high-quality government bonds. Gold prices have shown strong resilience, underpinned by its historical role as a hedge against inflation and uncertainty, and continued central bank purchases aimed at portfolio diversification amid currency and geopolitical risks.

Empirical data reflects sharp increases in gold volatility and upward price pressure as investors rotate capital away from risk assets. This phenomenon is reinforced by heightened demand for U.S. Treasury securities and euro-area sovereign bonds from countries with stronger credit profiles, driven by a global flight-to-quality dynamic. The intensified demand has contributed to yield compression in core government bonds despite earlier tightening cycles, evidencing the market’s prioritization of liquidity and safety.

This flight-to-quality effect extends to currency markets, where the U.S. dollar and other sanctuary currencies strengthen amidst heightened risk aversion. However, the interplay between higher interest rates and geopolitical stress creates a nuanced backdrop, as increased bond yields may partially dampen the attractiveness of non-yielding assets like gold. Nonetheless, the sustained geopolitical uncertainty ensures that safe-haven demand remains a critical factor shaping capital flows and asset valuation calibrations in mid-2026.

Assessing Duration and Severity of the U.S.-Iran Standoff’s Impact on Energy Security and Economic Stability

The duration of the blockade and conflict in the Strait of Hormuz stands as the paramount determinant shaping the severity of economic disruption. Short- to medium-term closures, lasting several weeks to a few months, drive significant yet potentially manageable spikes in oil and LNG prices, with partial release of strategic reserves and logistical adjustments providing some relief. However, a protracted standoff extending beyond six months risks inflicting structural damage on global energy supplies, further destabilizing markets and economic forecasting.

Scenario analyses underscore that the longer the disruption endures, the greater the likelihood of irreversible shifts in energy supply chains, with exporters and importers forced to realign trade routes, accelerate diversification of energy sources, and internalize elevated risk premiums permanently into pricing models. For energy-import-reliant regions, particularly Europe and Asia, these transformations exacerbate inflationary pressures and heighten recession risks, complicating policy responses.

Historic precedents reveal that extended geopolitical energy disruptions elevate uncertainty premiums, compel central banks to balance inflation control against growth support, and induce cascading effects across manufacturing, logistics, and consumer sectors. The socioeconomic consequences extend beyond raw economic metrics, influencing food security, fiscal stability, and geopolitical alliances, thus underscoring the multifaceted severity of prolonged conflict dynamics.

Having dissected the multifaceted economic vulnerabilities and market stress factors arising from a prolonged U.S.-Iran confrontation, the analysis now transitions to exploring adaptive strategies for investors and policymakers to navigate this volatility-laden landscape while preserving upside capture from concurrent AI-driven growth trajectories.

Upside Scenario: AI Productivity Surge Exceeding Expectations

This subsection explores the most optimistic trajectory for the U.S. economy driven by a rapid and broad-based acceleration in AI-driven productivity. It quantifies the potential GDP uplift achievable if AI adoption outpaces current projections, analyzes the corresponding impacts on fixed income markets through inflation and yield dynamics, assesses implications for the U.S. dollar’s strength amid shifting capital flows, and identifies the equity sectors poised to benefit most from this scenario. This analysis informs strategic positioning by highlighting the scale and sectoral contours of economic expansion under a best-case AI breakthrough scenario.

Quantifying GDP Uplift from Achieving 3% Real Growth Driven by AI Breakthroughs

A scenario in which AI technologies significantly exceed current productivity expectations could raise the U.S. real GDP growth rate toward 3% per annum, substantially above mid-2026 baseline estimates around 2.25%. This uplift reflects an intensification of AI adoption across sectors, resulting in accelerated capital investment, automation, and innovation diffusion that collectively boost output. The magnitude of this potential growth surge parallels historic technology waves such as the late-1990s information technology expansion, suggesting a transformative structural shift rather than transitory dynamics.

Modeling this 3% GDP growth scenario indicates that AI would act as the primary catalyst, with the share of work hours augmented by AI rising sharply, potentially reaching or exceeding 30% by the end of the decade. Such penetration would drive tangible improvements in labor productivity, capital efficiency, and value-added production. The resulting GDP uplift—estimated to be approximately 0.7 to 0.8 percentage points above current baseline projections—translates into trillions of dollars in incremental economic output over the medium term, reinforcing AI’s role as a sustained growth engine beyond mere cyclical effects.

Assessing Bond Yield Trajectory in the Context of Inflation Reduction from AI-Efficiency Gains

The anticipated productivity gains from accelerated AI adoption would exert downward pressure on inflation by enabling cost reductions, supply chain optimization, and greater output with the same or fewer inputs. This disinflationary effect, however, would coexist with elevated demand dynamics and ongoing geopolitical inflationary pressures, resulting in a complex interplay affecting bond yields.

In this upside scenario, real yields on long-term government bonds, particularly the 10-year Treasury, would likely trend modestly higher as investor confidence in stronger economic growth solidifies and equilibrium yields adjust upward reflecting improved productivity. Nevertheless, breakeven inflation rates could stabilize or even decline slightly due to technological deflationary force, tempering nominal yield increases. Historical analogies to late 1990s productivity surges support expectations of moderate yield upticks—potentially a 1 to 2 percentage point rise over several years—balanced by restrained inflation expectations under AI-driven efficiency.

Evaluating U.S. Dollar Strength and Emerging Market Capital Flows Amid Rapid AI Growth

Under a scenario of sustained 3% real GDP growth driven by AI, the U.S. dollar is likely to maintain or even strengthen its global reserve currency status, supported by differing interest rate trajectories and robust economic fundamentals. Stronger growth coupled with moderate inflation would attract foreign capital seeking exposure to the U.S. technology and innovation sectors, reinforcing demand for dollar-denominated assets.

At the same time, emerging markets could experience heightened capital outflows as global investors prioritize growth and risk-adjusted returns offered by the U.S. market. However, this dynamic might be partially offset by purposeful diversification flows and improving fundamentals in select emerging economies with AI and technology adoption prospects. In aggregate, the dollar’s relative strength would tighten global dollar funding conditions and potentially compress carry trade opportunities, influencing currency and bond markets worldwide.

Identifying Equity Sectors Most Sensitive to Accelerated AI-Driven Productivity Gains

Equity sectors that stand to benefit most under a rapid AI productivity surge include information technology, communication services, and selected segments within financials and healthcare. These sectors combine high AI adoption rates, scalable business models, and strong free cash flow conversion, positioning them to outperform in an environment marked by efficiency gains and innovation-led revenue growth.

Conversely, more traditional industries with slower AI diffusion—such as basic materials, utilities, and energy—may lag due to relative structural inertia. Within technology, companies focused on AI infrastructure such as semiconductor manufacturing, cloud data centers, and AI-enabled software platforms represent the key leverage points. Healthcare equities incorporating AI diagnostics and digital health stand to realize accelerated earnings growth driven by productivity and cost-saving innovations.

While the upside scenario highlights the transformative potential of AI-driven economic acceleration, the intertwined geopolitical and energy market complexities continue to present substantial risks. The following sections will juxtapose these optimistic outcomes against stress scenarios, underscoring the necessity of balanced, adaptive strategy frameworks going forward.

5. Implementation Roadmap: Building Adaptive Decision Frameworks for Mid-2026

Precision Portfolio Construction: Strategic Weighting, Volatility-Responsive Stops, and Timed Rebalancing for Mid-2026