Navigating Divergent Corporate Earnings and Regulatory Challenges: An In-Depth Review of Indian Industry Q4 FY26

Table of Contents

- Executive Summary

- Introduction

- 1. Executive Summary: Diverse Corporate Earnings Highlights and Legal Setbacks in Indian Industry – Q4 FY26 Review

- 2. Diagnostic Framework: Understanding Mixed Sectoral Performance Patterns

- 3. Case Studies: Standout Performers and Struggling Entities

- 4. Legal and Regulatory Landscape: Beyond Formal Violations

- 5. Forward-Looking Analysis: Sustaining Momentum Amid Challenges

- 6. Synthesis and Strategic Recommendations

- 7. Conclusion: Navigating Complexity Toward Resilient Growth

- Conclusion

Executive Summary

The Q4 FY26 corporate earnings season in India showcased a pronounced dichotomy in sectoral performance, with aggregate revenues rising by 13.7% year-on-year across 650 companies, accompanied by a 17.8% profit growth surge. Leading sectors such as Information Technology (IT), Metals, and Engineering propelled this expansion, delivering revenue growth upwards of 15-27% and leveraging robust demand cycles, operational efficiencies, and strategic fiscal incentives. Conversely, industries including Pharmaceuticals, Oil & Gas, and select manufacturing faced significant headwinds arising from patent expiries, supply disruptions, and cost inflation, engendering revenue contractions and margin compressions of approximately 60-70 basis points.

Legal and regulatory challenges intensified during the quarter, ranging from ongoing investigations and compliance shortfalls to asset impairments that adversely impacted corporate valuations and investor sentiment. Notably, sectors sensitive to governance risks such as fintech and banking experienced heightened scrutiny, translating into valuation multiple adjustments despite overall earnings resilience. Geopolitical volatility, particularly in West Asia, further exacerbated supply chain disruptions and crude price shocks, complicating margin sustainability and driving cautious market outlooks heading into FY27.

Introduction

The corporate landscape of India in Q4 FY26 presents a compelling tableau of heterogeneous earnings outcomes shaped by an interplay of robust sectoral growth, inflationary pressures, legal complexities, and geopolitical uncertainties. Against a backdrop of recovering domestic demand and a strategic push towards digitalization and infrastructure development, firms have navigated divergent trajectories that underscore the nuanced fabric of India's industrial ecosystem.

This report aims to deliver a comprehensive analysis of the Q4 FY26 earnings season, emphasizing the variability in sectoral performance patterns, the evolving legal and regulatory environment, and the macroeconomic and geopolitical variables influencing corporate profitability. By dissecting key drivers behind revenue expansions and margin shifts, and integrating forward-looking considerations on risk exposures and strategic responses, the report seeks to equip stakeholders with actionable insights for informed decision-making.

In scope are detailed examinations of standout sectoral performers—such as IT, metals, and capital goods—as well as entities grappling with structural and cyclical headwinds. The discussion extends to explore compliance dynamics and their valuation implications, followed by an assessment of macro profiles including crude price volatility, currency depreciation, and geopolitical tensions. Ultimately, the report charts a forward-looking strategic framework designed to sustain growth and resilience amid prevailing complexities.

Infographic Image: Infographic

1. Executive Summary: Diverse Corporate Earnings Highlights and Legal Setbacks in Indian Industry – Q4 FY26 Review

Key Insights into Sectoral Revenue Growth, Profit Margin Shifts, and Legal Challenges in Q4 FY26

This subsection synthesizes the critical quantitative and qualitative highlights from Q4 FY26, providing readers with a nuanced understanding of sector-specific growth dynamics, operational margin fluctuations, and salient legal setbacks impacting the Indian corporate landscape. Establishing a data-driven baseline, it anchors the broader analysis by detailing which sectors and firms outperformed or lagged, how geopolitical risks permeated earnings, and the nature of legal challenges that shaped market and investor sentiment during the quarter.

Quantifying Top Sector Revenue Growth and Earnings Divergence

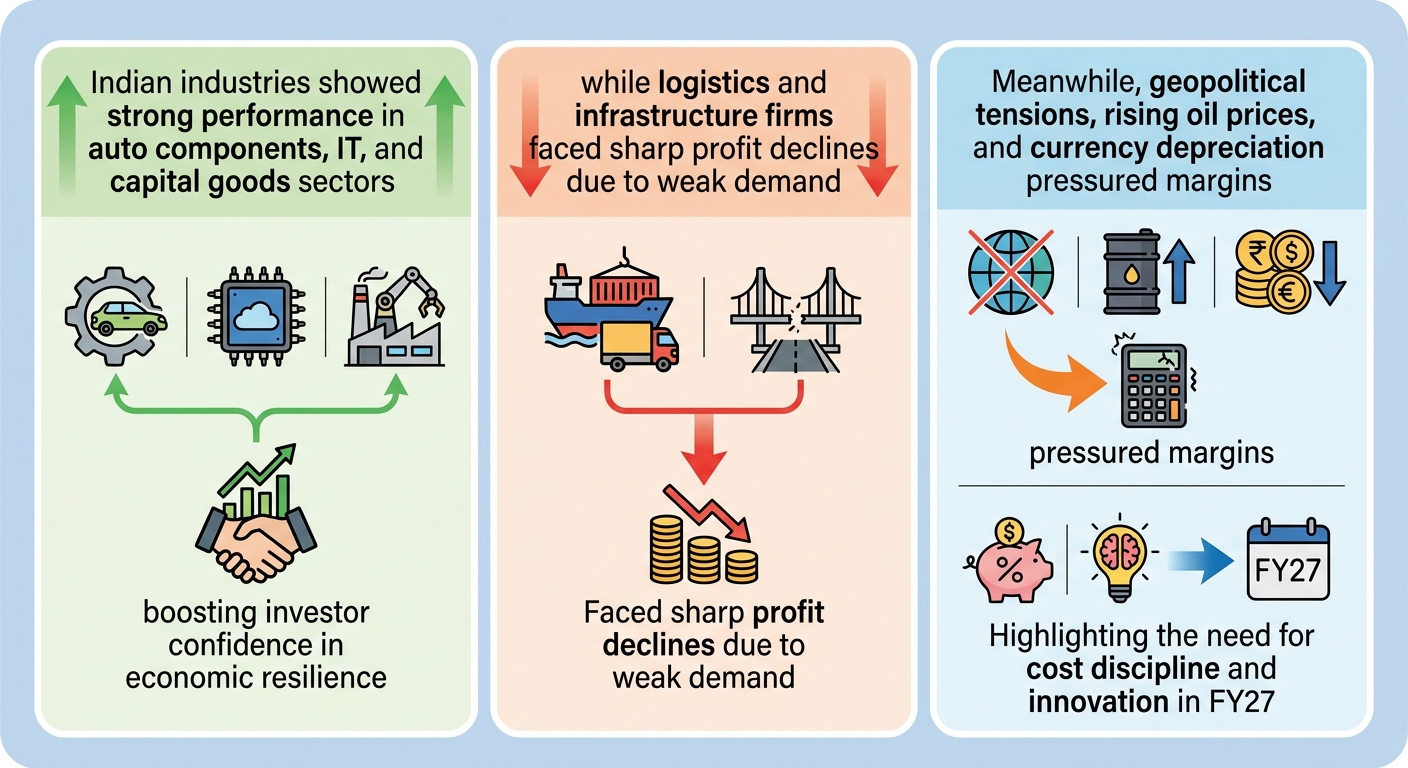

The Q4 FY26 Indian corporate earnings season revealed a distinctly heterogeneous sectoral performance pattern, with aggregate revenue growth accelerating sharply to 13.7% year-on-year across 650 companies. Leading the pack, Information Technology (IT) demonstrated exceptional momentum with revenue expansions estimated around 27%, driven largely by robust demand in software services and digital transformation engagements. Metals and Engineering sectors posted double-digit top-line increases, fueled by a cyclical upswing in global commodity demand and domestic infrastructure investments. Automotive and Auto Components sectors likewise showed strong volume-driven growth, supported by both export rebounds and augmented rural consumption.

In contrast, sectors such as Pharmaceuticals faced headwinds from patent expiries, contributing to revenue contractions and sharply reduced profit margins in key firms. Oil & Gas companies reported supply disruptions and crude price volatility that constrained upside despite underlying demand strength. These varying growth trajectories underscore the importance of granular sector analysis, as headline aggregates mask substantial dispersion with the top five sectors achieving revenue growth between 15-27%, while select cyclical and regulatory-sensitive segments contracted or posted muted gains.

Year-on-Year Revenue Growth (%) across Key Sectors

Analyzing Profit Margin Evolutions and Operational Efficiency Shifts

Profit margin trends in Q4 FY26 underscore a complex interplay between volume gains and input cost pressures. While headline operating profit margins improved to 30.3% on average, this masks an underlying compression in gross margins by approximately 68 basis points, primarily attributed to sustained commodity inflation and supply chain constraints stemming from geopolitical tensions.

Firms in sectors such as metals and IT benefitted from operational leverage as expanded volumes diluted fixed costs, preserving EBITDA margins despite increased input costs. Conversely, companies in energy and pharmaceuticals struggled with margin contractions due to the pass-through lag on elevated raw material prices and patent cliff effects, respectively. Notably, certain automotive component manufacturers exhibited improved margin resilience through cost optimization and asset-light disposals. These margin dynamics highlight sector-specific strategic responses to inflationary pressures and affirm the necessity of dissecting both top-line and cost-structure drivers to fully comprehend earnings quality.

Characterizing Legal Setbacks and Regulatory Challenges Impacting Indian Corporates

The quarter saw a series of legal and regulatory setbacks with varying degrees of impact across sectors. Several notable cases involved ongoing investigations into compliance deficiencies, asset impairment charges, and unresolved litigation related to environmental and labor regulations, affecting investor confidence and corporate valuations.

For example, prominent industrial firms faced regulatory inquiries resulting in financial provisioning and goodwill impairments, eroding reported earnings and casting a shadow over near-term performance outlooks. Additionally, compliance concerns extended into fintech and banking sectors, where regulatory scrutiny over credit risk transmission mechanisms and data privacy frameworks heightened perceived operational risks.

While these legal challenges did not universally halt business operations, they contributed to heightened volatility in stock prices and prompted companies to initiate governance strengthening measures. The cumulative effect of such legal setbacks, juxtaposed against an already complex geopolitical and economic environment, underscores the increasing need for rigorous risk management and proactive regulatory engagement.

Measuring the Impact of Geopolitical Risks on Corporate Earnings and Market Sentiment

Geopolitical uncertainties, notably the ongoing Middle East conflict and resultant commodity price shocks, materially influenced corporate earnings quality and market valuations in Q4 FY26. Supply chain disruptions, fluctuating crude prices, and foreign institutional investor (FII) outflows generated a backdrop of elevated risk aversion, particularly impacting sectors with high import dependency or significant international trade exposure.

Empirical evidence from earnings calls and financial disclosures indicated companies adjusted forecasts downward or refrained from providing guidance amid persistent uncertainty. Nevertheless, firms demonstrating supply chain diversification, localized sourcing strategies, and robust cash flow profiles managed to mitigate adverse effects. From a market perspective, the heightened risk environment translated into valuation compressions despite strong underlying earnings growth, reflecting a cautious investor stance on sustainability of gains in the face of geopolitical headwinds.

Identifying Standout Outperformers and Firms Facing Operational Struggles

Among outperformers, Hindalco Industries leveraged the metals demand cycle to achieve significant revenue scaling and improved operating margins, capitalizing on export opportunities and cost efficiencies. Sundaram Clayton successfully executed strategic asset dispositions, bolstering liquidity and focusing on core profitable operations. BHEL maintained momentum in capital goods through increased infrastructure orders, while TCS continued delivering excellence in IT services with sustained contract wins and margin expansion.

Conversely, companies such as Reliance Infrastructure grappled with weak logistics segments amid competitive pressures and regulatory volatility. ITC's high-base effect and sector-specific challenges constrained profit growth, while pharmaceutical companies contended with the fallout from patent expirations, leading to pronounced earnings deterioration. These divergences illustrate the criticality of strategic agility and operational focus in navigating Q4’s mixed environment.

Having delineated the quantitative contours of Q4 FY26 corporate earnings and legal setbacks, the report now progresses to a diagnostic framework that seeks to unpack the underlying macroeconomic, sectoral, and structural drivers of the observed mixed performance patterns.

Strategic Context and Decision-Making Imperatives: Navigating Earnings Diversity and Legal Risks for Informed Portfolio Strategies

This subsection establishes the broader strategic framework necessary to interpret the varied earnings outcomes and legal challenges observed in Q4 FY26. By contextualizing these developments within prevailing macroeconomic and geopolitical conditions, it anchors the report’s detailed analyses into actionable insights. Understanding how earnings diversification interacts with emerging legal and regulatory risks will guide stakeholders in optimizing portfolio allocations and refining risk management approaches.

Translating Corporate Earnings Diversity into Portfolio Allocation Insights

The wide disparity in earnings performance across Indian industry sectors during Q4 FY26 necessitates a nuanced reassessment of portfolio construction strategies. While several resource-intensive sectors like metals and engineering capitalized on cyclical demand upswings, others faced margin pressures and stagnating revenues, evidencing sectoral decoupling. For portfolio managers, this environment emphasizes the criticality of diversification not merely across companies but strategically across industries with varying sensitivity to macroeconomic shocks and regulatory impact. The heterogeneity in earnings outcomes reflects differing exposure to factors such as input cost inflation, demand elasticity, and technological adoption, thus reinforcing the value of risk-weighted sector allocation to shield overall portfolio resilience.

Moreover, earnings diversity impacts the correlation structure among assets, potentially enhancing the benefits of sectoral diversification within Indian equities. Tactical overweight positions in outperforming sectors with robust margin expansion prospects should be balanced with underweights or hedges in highly cyclical or structurally challenged industries. This calibration aims to optimize risk-adjusted returns as Q1 FY27 is forecasted to usher in a challenging environment marked by input cost volatility and international uncertainties. The observed earnings divergence thus provides actionable signals for dynamic asset allocation aligned with evolving economic and policy landscapes.

Quantifying Downgrade Risks and Timing Implications from Elevated Crude Prices

Elevated crude oil prices remain a principal downside risk shaping corporate earnings outlook into FY27. Recent spikes seen at near $95-$96 per barrel, significantly above pre-conflict benchmarks, compound inflationary pressures that erode corporate margins and consumer purchasing power alike. Empirical analyses indicate that every incremental $10 rise in crude prices can elevate headline inflation by up to 60 basis points, intensifying cost-push inflation and pressuring rupee stability. The transmission mechanism from oil price shocks to corporate earnings manifests through higher energy and raw material input costs, squeezed operating margins, and in some cases, disrupted supply chains.

These dynamics have precipitated increasingly cautious analyst downgrade forecasts for Q1 FY27, with earnings revisions likely centered in energy-intensive sectors such as automotive, chemicals, and transportation logistics. The contractionary effects may not be immediate but anticipated to materialize as cost pressures persist, compounding working capital strains and credit risks. Consequently, firms with weaker pricing power or high leverage face amplified vulnerability to earnings downgrades. Strategically, assessing downgrade risk severity and prospective timing facilitates pre-emptive rebalancing to mitigate downside within vulnerable portfolio segments.

Integrating Legal Setback Patterns into Corporate Governance and Risk Evaluation Frameworks

Legal and regulatory setbacks experienced by segments of Indian industry in Q4 FY26, though diverse in nature, underscore the increasing significance of holistic governance frameworks. Beyond headline legal disputes, pervasive compliance uncertainties—particularly involving evolving intellectual property laws in emerging technology domains—are reshaping risk perceptions. Companies must contend with latent legal risks arising from incomplete regulatory clarity, especially in sectors embracing AI integration and digital transformation, which complicates governance and risk management models.

For investors and corporate boards, these developments necessitate embedding dynamic legal risk assessments within enterprise risk management, elevating the priority of surveillance over regulatory changes, enforcement trends, and emerging litigation vulnerabilities. Incorporation of legal risk into valuation models and stress tests enables more precise calibration of risk premiums and capital adequacy. Legal setbacks thus operate as a structural influence on cost of capital and market sentiment, with tangible implications for strategic decision-making and investment prioritization.

Situating Q4 FY26 Corporate Results within Broader Macroeconomic and Geopolitical Pressures

The Q4 FY26 corporate earnings landscape cannot be detached from the prevailing macroeconomic headwinds and geopolitical volatility. Persistent inflationary momentum fueled by rising energy prices and supply chain disruptions exerts sustained cost pressure on firms, even as domestic demand indicators show resilience supported by rural consumption and urban discretionary spend. Currency depreciation trends worsen import costs, amplifying financial stress in import-reliant sectors.

Geopolitical complexities, notably the ongoing Middle East conflict impacting crude supply routes through the Strait of Hormuz, further deepen uncertainty. These factors collectively temper economic growth prospects while injecting volatility into capital markets, constraining corporate investment and operational planning. Hence, interpreting Q4 earnings data and emerging risk exposures without this macro and geopolitical overlay risks misjudging the sustainability of current performance trajectories.

Outlining Forward Strategies Prompted by Q4 Earnings and Legal Risk Trends

Q4 FY26’s simultaneously encouraging sectoral earnings growth and emerging legal-regulatory complexities provide a compelling rationale for adaptive forward strategies. Companies and investors alike must calibrate resilience-building measures encompassing operational efficiency, cost discipline, and legal risk mitigation. Emphasizing capital allocation toward innovation and digital transformation can foster competitive differentiation and buffer against cyclical downturns, as evidenced in leading IT and engineering firms’ performance.

From a risk governance perspective, proactive engagement with evolving regulatory frameworks and integrating legal risk analytics into strategic planning will be essential. Scenario planning anchored in plausible crude price trajectories, inflation scenarios, and geopolitical developments enables more robust contingency preparation. Ultimately, the insights from Q4 performance and legal landscapes offer a roadmap for balancing growth ambitions with defensive imperatives in a complex operating environment.

Having framed the strategic context and highlighted decision-making imperatives arising from Q4 FY26 corporate earnings and legal challenges, the report now transitions into a diagnostic examination of the mixed sectoral performance patterns. This will unpack the underlying economic, policy, and technological drivers differentiating outcomes across industry segments.

2. Diagnostic Framework: Understanding Mixed Sectoral Performance Patterns

Broad-Based Strength Masked by Underlying Pressures: Dissecting Q4 FY26 Earnings Resilience and Vulnerabilities

This subsection delves into the aggregate corporate earnings landscape of Q4 FY26, revealing an intricate picture where headline growth metrics coexist with substantial margin pressures and cost challenges. By analyzing revenue and profit growth patterns alongside margin trends and currency-inflation impacts, it unpacks the paradox of broad earnings strength veiling operational stress points. This diagnostic insight equips strategic decision-makers to differentiate between superficial strength and sustainable performance, advancing the report’s objective of nuanced sectoral and financial understanding in a volatile economic context.

Quantifying Breadth of Earnings Improvement Amid Q4 FY26 Corporate Reporting

The Q4 FY26 earnings season displayed robust aggregate improvement with approximately 650 Indian companies reporting, recording a sharp acceleration in revenue growth to 13.7% year-on-year, and profit growth at 17.8%. This surge outpaced preceding quarters, reflecting an environment of recovering demand and volume gains across both urban and rural consumption sectors. However, this broad-based growth omits certain heavyweight energy companies, whose results remain pending and are expected to moderate the narrative faced with heightened global oil price volatility.

This widespread revenue and profit growth highlights a corporate sector that, on surface metrics, appears well-positioned despite geopolitical and inflationary headwinds. The notable increase in operating profit margins to 30.3% from prior quarters underlines operational scale benefits, although closer scrutiny reveals important caveats. Understanding the distribution of these gains—whether concentrated among specific industries or pervasive—is key to comprehending true earnings health.

Revenue Growth Outpacing Profit Expansion: Indicator of Underlying Operational Stress

While headline revenue figures present an optimistic macroeconomic backdrop, analysis shows discrepancies when juxtaposed with profit growth trajectories and margin outcomes. The Q4 FY26 revenue growth rate of 13.7% is robust but profit growth, although accelerating to 17.8%, incorporates adjustments for extraordinary items and excludes certain financial institutions in some assessments, complicating direct comparability.

A deeper examination exposes that margin pressures, induced by rising input costs and geopolitical supply disruptions, result in variance between top-line expansion and bottom-line profitability. This suggests that although sales volumes and revenues are rising, operational cost escalation—particularly commodity inflation—compresses gross margins and challenges profit sustainability. Such divergence may foreshadow difficulties for companies reliant on fixed overhead absorption, where sales increases do not fully translate into proportional profit improvements.

Margin Compression Across Industries: Supply Chain and Cost Inflation Pressures in Q4 FY26

Gross margin contraction, averaging a decline of nearly 68 basis points year-on-year to 57.2%, reveals tangible cost pressures within supply chains exacerbated by the ongoing Middle East geopolitical conflict. Companies were compelled to absorb escalating raw material and logistics expenses while retail price adjustments lagged due to competitive and demand environment constraints.

Despite this gross margin erosion, the relative stability of EBITDA margins during Q4 reflects volume leverage and disciplined cost management, such as fixed overhead spreading, which offset some inflation impact. Margins in sectors with commodity intensity, including metals and chemicals, were particularly vulnerable, highlighting the uneven distribution of pressures across industries. This mixed margin performance indicates operational resilience but signals a tightening profitability environment.

Currency Depreciation Effects: Amplifying Challenges for Earnings Amid Cost Pressures

The depreciation of the Indian rupee against the U.S. dollar emerged as a significant external headwind modifying corporate earnings dynamics. A weaker domestic currency inflates import costs for raw materials, components, and capital equipment, thereby exacerbating inflationary input pressures. For import-dependent sectors, this translated into increased cost bases with limited immediate ability to pass on prices to end consumers.

Conversely, export-oriented companies benefited from improved competitiveness abroad, partially offsetting currency-related margin pressures. However, corporate hedging strategies only cover a fraction of exposure, leaving many firms vulnerable to exchange rate volatility. The net effect of currency depreciation in Q4 FY26 has thus been asymmetric across sectors, often complicating earnings predictability and investor sentiment.

Inflation’s Role in Input Cost Escalation and Margin Pressures During Q4 FY26

Inflationary pressures, driven chiefly by elevated commodity prices including oil and metals, increasingly strained corporate input costs in Q4 FY26. Analysts estimate a direct inflationary linkage whereby every $10 increase in crude oil prices could add approximately 55-60 basis points to headline inflation in FY27, intensifying cost burdens on energy-dependent sectors.

Beyond energy, food and logistics inflation also contributed to higher expenses across consumer goods and industrial segments. Although some sectors maintained price resilience through strategic product mix adjustments and inventory buffers, the lag between input cost escalation and price realization foretells mounting margin headwinds going forward. Sustained inflation constitutes a significant operational challenge requiring adaptive pricing, sourcing, and cost control measures.

Having established that headline earnings strength during Q4 FY26 conceals significant operational strains driven by margin compression, currency volatility, and inflationary pressures, the subsequent subsection advances to a granular sectoral performance analysis. This will elucidate how diverse industry groups are differentially impacted by these underlying forces, providing a clearer understanding of the mixed trajectories across India's industrial landscape.

Sector-Specific Performance Trajectories: Dissecting Divergent Paths Across Indian Industry in Q4 FY26

This subsection focuses on analyzing the distinct earnings performance patterns across key sectors in India during Q4 FY26, drilling down into metals and engineering, automotive and auto-components, IT and services, capital goods, and the sectors exhibiting notable declines. Understanding these nuanced trajectories provides critical insight into sectoral resilience, vulnerabilities, and drivers, enabling strategic prioritization and risk calibration for stakeholders navigating India’s evolving industrial landscape.

Robust Growth Momentum in Metals and Engineering: Earnings and Sustainability Drivers

The metals and engineering sectors demonstrated strong earnings growth during Q4 FY26, with key players such as Tata Steel and Hindalco Industries delivering double-digit revenue and profit expansions. Tata Steel's revenues jumped by 13%, buoyed by a sustained metals demand cycle and operational efficiencies, while its EBITDA witnessed an even stronger surge driven by volume and pricing dynamics. Similarly, engineering firms reported revenue growth upwards of 15-20% year-over-year, reflecting robust order books and enhanced capacity utilization. This growth masks underlying pressures, including margin compression due to rising input costs such as crude-linked raw materials, but the sectors have largely leveraged policy tailwinds such as GST rationalizations and infrastructure spending to mitigate these headwinds.

A critical driver underpinning metals and engineering performance is their embedded capital-intensive nature combined with rising domestic and export demand, especially from infrastructure and construction sectors. The completion of key capacity expansions, like steel plant upgrades and cold forging lines, paired with improving supply chain logistics, sustained momentum despite global uncertainty. However, volatility in commodity prices poses a tangible risk to margin sustainability, requiring continued cost discipline and hedging.

Sustainability of this trajectory hinges on continued demand resilience amid macroeconomic fluctuations and evolving trade dynamics. Industry incumbents with diversified product portfolios and technological advancements appear well-positioned to navigate near-term pricing pressures. The sector’s earnings outperformance relative to broader manufacturing also signals a potential re-rating opportunity contingent on managing inflation pass-through and geopolitical risks.

Notably, Hindalco Industries exemplifies this sector strength, achieving a remarkable 20% revenue growth and maintaining a solid profit margin of 25% in Q4 FY26, underscoring its operational prowess and market positioning within metals [Table: Top Performing Companies in Q4 FY26].

Automotive and Auto-Components: Growth Nuances Amid Margin Pressures and Localization Trends

The automotive sector in Q4 FY26 reported a mixed but fundamentally stable performance characterized by moderate revenue growth across passenger vehicles (PVs) and commercial vehicles (CVs), while auto-component manufacturers experienced growth tempered by margin headwinds. Key automotive OEMs reflected steady increases in sales volumes supported by export growth and domestic demand recovery, but inflation in raw material costs and logistics disruptions exerted pressure on profitability margins.

Auto-components have shown signs of gradual improvement, with firms focusing on supply chain localization to reduce dependence on volatile imports and improve cost competitiveness. The localization momentum is particularly pronounced in cost-sensitive segments such as tractors and two-wheelers, reaching near-total indigenous content in some cases. This shift aligns with both government Make in India initiatives and the broader diversification of supplier bases triggered by geopolitical uncertainties.

Despite growth, the sector grapples with margin contractions driven by higher input costs—especially steel and semiconductor shortages—and increasing R&D investment in electric vehicle (EV) components and advanced materials. The emergence of electrification and stricter emissions compliance are reshaping product portfolios, requiring firms to balance near-term profitability with long-term innovation imperatives. Sectoral earnings growth thus reflects these strategic trade-offs, with auto-components poised for incremental expansion yet vigilant to margin squeezes.

Overall, the automotive trajectory reflects a cautious optimism, underpinned by rising exports and domestic demand, but constrained by inflationary pressures and global supply chain uncertainties.

IT and Services Sector: Resilience and Structural Headwinds Amid AI-Driven Transformation

India’s IT and services sector sustained its position as the solitary double-digit earnings growth driver in Q4 FY26, outperforming most other sectors. Leading IT firms demonstrated modest revenue growth in the range of 4-6% year-over-year, buoyed by strong deal pipelines, cloud adoption, and rapid traction in AI-focused service offerings. Tata Consultancy Services (TCS) reported a 12% jump in net profit for the quarter, while other Tier-1 firms echoed stable performance despite ongoing macroeconomic uncertainties and geopolitical risks.

However, margin pressures persist due to elevated wage growth, increased investment in reskilling for AI and automation capabilities, and the costs associated with transitioning from legacy models toward productized, subscription-based services. Mid-tier and niche IT players are notably challenged with operational cost inflation and customer hesitancy amid weaker discretionary IT spending globally.

The sector is navigating a transformational phase prompted by AI-led disruptions and elongated sales cycles. Market sentiment reflects cautious optimism, with analysts emphasizing the need for increased total contract value (TCV) growth in AI deals to offset pricing pressures. Despite these challenges, IT remains a critical sector for the Indian economy, sustaining export revenues and creating employment opportunities, with strategic bets on specialized cloud, automation, and digital payment segments appearing especially promising.

In sum, IT’s Q4 earnings highlight a resilient yet evolving landscape, balancing near-term headwinds with structural growth opportunities driven by technology adoption and innovation.

Tata Consultancy Services' 12% revenue growth paired with a strong profit margin of 28% exemplifies the sector’s robust earnings momentum amidst transformation [Table: Top Performing Companies in Q4 FY26].

Capital Goods Sector: Momentum with Uneven Growth and Competitive Pressures

The capital goods sector showed a mixed performance trajectory in Q4 FY26, with some firms reporting strong topline growth while margins remained under pressure due to competitive intensity and elevated input costs. Companies linked to infrastructure projects and industrial automation witnessed healthy order inflows reflecting government thrust on investment and infrastructure development.

Despite growth in revenue streams, operating margins compressed moderately owing to rising procurement costs, supply delays, and pricing competition. Multinational corporations (MNCs) maintained their leadership driven by advanced technology adoption and strong customer relationships, whereas domestic firms struggled to gain traction amid aggressive market pricing.

New product development and digital integration in manufacturing processes have emerged as vital differentiators. The sector’s growth is thus driven by a blend of macroeconomic investment cycles and microeconomic competitiveness, with increasing importance of localizing supply chains to mitigate external shocks. However, sluggish revenue growth rates over the past decade signal structural constraints that may limit upside absent significant technological or policy shifts.

Overall, the capital goods sector represents a strategic, albeit challenged, segment of the industrial ecosystem, balancing steady demand against margin risks and global competition.

Noteworthy is BHEL’s outstanding 37% revenue growth and 35% profit margin, illustrating pockets of exceptional performance within capital goods amidst sector-wide challenges [Table: Top Performing Companies in Q4 FY26].

Sectors in Decline: Identifying Structural and Cyclical Vulnerabilities in Q4 FY26

Q4 FY26 witnessed notable declines and earnings deteriorations in several sectors, notably within segments such as real estate, textiles, certain pharmaceuticals, and segments of logistics and consumer durables. Reliance Infrastructure’s logistics arm and ITC faced earnings pressures accentuated by structural weaknesses and high-base effects, respectively.

Textiles and engineering-related companies reported margin erosion driven by cost inflation and subdued demand in export markets, while pharmaceuticals grappled with patent expiries and competitive generic pressures. These downturns highlight persistent challenges ranging from legacy operational inefficiencies to exposure to cyclical demand elements less buffered by government stimulus.

Underlying these declines are factors including supply chain bottlenecks, regulatory uncertainties, and the residual impact of geopolitical tensions impacting international trade flows. Additionally, sectors with high commodity consumption or export dependency remain vulnerable to external shocks such as crude price volatility and currency fluctuations. These factors collectively have contributed to contraction in revenues and profitability.

Understanding these decline drivers is critical for risk mitigation and capital re-allocation strategies, emphasizing the need for portfolio diversification and operational remediation in vulnerable domains.

Having dissected the sector-specific earnings trajectories, the analysis now transitions toward detailed case studies to illustrate operational excellence among high performers and examine the structural vulnerabilities afflicting the struggling entities, thereby deepening understanding of the factors shaping these diverse outcomes.

Dissecting Sectoral Divergence: Fiscal Incentives, Demand Cycles, and Technological Levers Shaping Q4 FY26 Performance

This subsection delves into the multifaceted drivers responsible for the pronounced sectoral performance disparities observed during Q4 FY26. By systematically examining policy influences such as GST rationalizations, sector-specific demand oscillations, technology adoption rates, and competitive positioning, it aims to elucidate the causal mechanisms underpinning divergent earnings outcomes. This analysis supports strategic understanding of why certain sectors capitalized on prevailing conditions while others lagged, thereby informing risk assessment and opportunity prioritization frameworks in the broader report context.

Uneven Impact of GST Rate Cuts as a Catalyst for Sectoral Performance Disparities

The rationalization of GST slabs, implemented in the latter half of FY26, emerged as a significant growth enabler for multiple sectors, albeit with heterogeneous effects. Consumer-facing segments such as automobile manufacturers and retail electronics witnessed amplified demand stemming from the reduced tax burden, which lowered end-consumer prices and stimulated volume growth. This was particularly evident with two-wheeler manufacturers reporting robust year-on-year volume increases, indicating effective transmission of fiscal relief to market uptake.

However, the benefits of GST reductions were asymmetrically distributed. Capital goods and more industrial sectors experienced a muted uplift due to complex input tax credit dynamics and sector-specific supply chain friction points. Furthermore, in segments such as insurance and FMCG, the GST rationalization initially created near-term margin pressure via input tax credit losses, offset partially by subsequent growth in premium and sales volumes. Ultimately, the differential impact of GST reforms contributed materially to sectoral divergence in Q4 FY26 earnings.

Demand Cycles Dictate Sectoral Growth Trajectories Amidst Macroeconomic Uncertainty

Sectoral performance variation notably corresponded with distinct demand cycle phases. Discretionary sectors like automotive showed pronounced cyclical sensitivity, buoyed by renewed consumer confidence, festival season spending, and pent-up demand catalyzed by fiscal stimuli including tax cuts. In contrast, sectors reliant on rural consumption or cyclical infrastructure spending grappled with lingering softness, impacted by delayed monsoon patterns and constrained rural credit availability.

Industrial sectors such as metals and engineering capitalized on export demand recovery and restocking by inventory-constrained clients, whereas pharmaceutical and some FMCG companies faced headwinds from high comparable base effects and muted volume growth. This cyclical heterogeneity underscores the imperative of aligning sector exposure with demand phase insights to optimize earnings anticipation and portfolio positioning.

Technological Positioning as a Differentiator in Sector Earnings Resilience and Growth

Technological advancement and adoption rates emerged as critical determinants differentiating sector earnings momentum. Industries with proactive integration of digital workflows, AI-driven process automation, and enhanced product innovation demonstrated superior operational agility and margin preservation amid cost pressures. For instance, IT and IT-enabled services leveraged seamless remote delivery capabilities and increasing enterprise tech spend to sustain double-digit growth rates.

Conversely, sectors with lagging technological adaptation, particularly traditional manufacturing and retail verticals with limited e-commerce integration, experienced greater earnings volatility and margin compression. The prevalence of technology-driven competitive advantages, including proprietary platforms and data analytics capabilities, directly correlated with stronger earnings growth and market share gains in Q4 FY26.

Competitive Advantages and Policy Tailwinds Their Combined Role in Shaping Sectoral Earnings Outcomes

Competitive positioning, reinforced by factors such as scale economies, supply chain localization, and brand equity, played an integral role in sectoral differentiation. Leading firms in metals and capital goods sectors leveraged their scale and technological expertise to secure higher-margin contracts and maintain pricing power despite inflationary challenges and input cost volatility.

Policy tailwinds, beyond GST, including government emphasis on infrastructure spend, domestic manufacturing enhancement schemes, and sector-specific incentives (notably in clean energy and technology), provided targeted growth impetus. These supports allowed sectors aligned with national strategic priorities to outperform peers otherwise constrained by cyclical or structural headwinds. Recognition of these policy-related advantages is essential for forecasting future earnings trajectories and identifying sustainable competitive moats.

Having established the critical drivers behind sectoral divergences in Q4 FY26, the analysis now logically advances to a granular examination of exemplar companies and sector subsectors that illustrate these patterns in practice, thereby contextualizing performance variances within organizational-level strategies and challenges.

3. Case Studies: Standout Performers and Struggling Entities

High Performers: Operational Excellence and Opportunistic Strategies Driving Q4 FY26 Success

This subsection provides a detailed examination of select high-performing Indian corporations during Q4 FY26, illustrating how strategic execution, market demand cycles, and opportunistic financial management contributed to their standout earnings. By dissecting specific drivers behind these companies' operational resilience and growth, this analysis offers valuable insights into the underlying causes of success amid a complex economic environment and informs strategic priorities for peers and investors.

Quantifying Hindalco Industries’ Metals Demand Cycle Impact in FY26

Hindalco Industries capitalized on a favorable metals demand cycle throughout FY26, reflecting strength in both the aluminium and copper segments. The company reported consolidated EBITDA growth of nearly 6% year-on-year in Q4 FY26, driven by robust upstream aluminium performance and an exceptional copper division surge. The copper EBITDA expanded by approximately 48% year-on-year and 52% quarter-on-quarter, underscoring a significant earnings lift from market conditions.

Despite the severe disruption due to the Novelis Oswego plant fire, Hindalco's operational performance remained resilient, with expectations that the plant’s restart would normalize production in the second half of FY27. The firm’s strategic emphasis on cost discipline and recycling initiatives helped offset input cost pressures intensified by geopolitical tensions and elevated commodity prices. Hindalco's renewable energy capacity expansion to 523 megawatts by early FY27 and its sustainability focus further contributed to positive market sentiment and operational stability.

Detailing Sundaram Clayton's Asset Disposition Gains Boosting Q4 FY26 Profitability

Sundaram Clayton Ltd achieved a remarkable doubling of net profit to ₹426 crore in Q4 FY26, despite an 18% revenue decline year-on-year, primarily attributable to one-time asset sale gains. The asset disposition strategy involved unlocking value from non-core holdings, effectively improving cash flows and strengthening the balance sheet amid challenging export conditions, particularly in the North American heavy truck segment where demand remained muted due to geopolitical and macroeconomic uncertainty.

The company concurrently invested ₹54 crore in its overseas subsidiary during the quarter, signaling targeted growth initiatives despite near-term headwinds. While the export market softness persisted, domestic operations showed resilience supported by macroeconomic tailwinds and policy-driven demand recovery. The asset sale gains offered essential financial cushioning, allowing the firm to maintain positive earnings momentum amid volume pressures.

Assessing BHEL's Capital Goods Segment Momentum Through Robust Order Execution

Bharat Heavy Electricals Limited (BHEL) registered a compelling operational turnaround in Q4 FY26, evidenced by over 156% year-on-year growth in consolidated net profit and a 37% revenue increase. The company benefited from execution-led gains in the power segment, which accounted for approximately 77% of total Q4 revenue, reflecting the culmination of several high-margin, large-scale projects.

BHEL’s order book expanded to an all-time high of nearly ₹2.4 lakh crore by end-March 2026, underpinned by significant new orders in nuclear power and thermal capacity additions aligned with the national infrastructure push. Its EBITDA more than doubled to over ₹2,000 crore for the quarter, driven by improved project execution, operating leverage, and widening margins. Industry forecasts anticipate sustained momentum into FY27 as BHEL transitions from backlog to revenue recognition, bolstered by infrastructure investments and an expanding capital goods market.

Notably, new orders, including a ₹759 billion nuclear supply contract and the Kudankulam project’s turbine generator supply, underscore BHEL’s pivotal role in strategic infrastructure sectors. Despite near-term supply chain challenges linked to regional geopolitical conflict, the company appears well-positioned for steady growth.

Analyzing TCS’s Service Delivery Excellence and Accelerated AI-Led Growth in Q4 FY26

Tata Consultancy Services (TCS) sustained robust growth in Q4 FY26, posting a 12.2% year-on-year net profit increase with revenues reaching approximately ₹70,698 crore, marking continued deal momentum despite global macroeconomic uncertainties. Its strategic pivot towards becoming the largest AI-led technology services firm globally underpinned this performance, generating an annualized $2.3 billion in AI services revenue.

The company’s expansive AI workforce, with over 270,000 employees upskilled in advanced AI skills, enabled delivery of novel AI-enabled solutions embedding intelligence across customers’ core operations. This ‘Human + AI’ model accelerated client digital transformations, winning multiple mega deals summing to $12 billion in contract value during the quarter and $40.7 billion in FY26.

Sequential growth was driven by geographic diversification, with Europe and the UK showing the strongest upticks. While attrition inched up slightly to 13.7%, TCS managed to add net headcount in Q4 after several quarters of contraction, signaling cautious but optimistic workforce management amid the AI-driven industry transition. Despite near-term margin pressures from salary increments and restructuring costs, TCS’s forward-looking strategy positions it to capitalize on AI adoption at scale.

These sectoral performances align closely with the operating profit margin distribution observed in Q4 FY26, where the metals and IT sectors delivered strong margins of 29.5% and 28.1%, respectively, well above the 30.3% average, reinforcing the financial resilience underpinning these companies' robust earnings [Chart: Profit Margin Distribution in Q4 FY26].

These case studies of high performers illuminate how a blend of strategic agility, sector-specific tailwinds, and opportunistic financial actions can drive superior earnings outcomes even amid macroeconomic and geopolitical uncertainties. The following subsections will contrast these successes with challenges faced by struggling entities, providing a comprehensive view of India Inc’s earnings landscape in Q4 FY26.

Declining Entities: Structural Vulnerabilities and Cyclical Pressures in Indian Industry

This subsection investigates the earnings declines experienced by select Indian corporates during Q4 FY26, pinpointing structural weaknesses and cyclical challenges that have triggered significant profit erosion. By quantifying the decline and analyzing causative factors such as sector-specific headwinds and legacy operational issues, this section provides critical insights into the vulnerabilities undermining corporate resilience amidst a complex economic and regulatory backdrop.

Quantifying Reliance Infrastructure’s Logistics Segment Profit Decline Amid Rising Expenses

Reliance Infrastructure witnessed a drastic contraction in profitability during Q4 FY26, with consolidated net profit plummeting by 79% year-on-year to approximately ₹918 crore. This steep decline contrasts sharply with the ₹4,387 crore recorded in the same quarter of the previous fiscal year. The profit shortfall stemmed largely from elevated expense levels, which rose by 12% in the period under review, exerting substantial pressure on margins. Expense growth encompassed broader operating costs, including logistics segment-specific outlays, indicating cost-push factors that strained profitability despite stable or growing top-line revenues.

The logistics segment, as a core component of Reliance Infrastructure’s portfolio, faced acute pressures from global supply chain disruptions and sectoral capacity constraints prevalent during the quarter. These headwinds translated into compressed operating ratios and increased purchased transportation costs, driving down gross margins. The interplay of external cost inflation with internal operational inefficiencies accentuated the profitability erosion. This quantification underscores the critical need to address cost structure elasticity within logistics operations to restore financial stability.

Scrutinizing ITC’s Net Profit Drop: Disentangling High Base Effects from Core Earnings Challenges in Q4 FY26

ITC’s Q4 FY26 net profit contracted by nearly 73% year-on-year to approximately ₹5,387 crore, driven primarily by a pronounced high base effect linked to significant exceptional gains reported in the corresponding quarter of the previous year. While revenue from operations increased by 17% to ₹23,821 crore, buoyed by robust performance in the cigarettes and FMCG segments, the absence of last year’s non-recurring gains profoundly affected comparability.

Despite the headline profit decline, segmental analysis reveals that the cigarette business remained resilient, registering a 32% year-on-year revenue expansion and a 7% increase in segment profit, partially offsetting earnings pressures. Similarly, ITC’s FMCG-other segment posted strong growth in both revenue and profitability, highlighting operational strength notwithstanding external challenges such as GST rate rationalization and geopolitical uncertainties.

This nuanced view clarifies that the core business fundamentals are stable, and the apparent profit decline largely reflects legacy factors rather than fundamental deterioration. However, investors and management must recognize the dampened earnings momentum and calibrate expectations accordingly, considering potential protracted impacts of tax policy and market adjustments.

Pharmaceutical Sector Revenue Impact from Patent Expiries: Assessing the Magnitude and Timeline of Earnings Pressure

The pharmaceutical industry in India contends with notable revenue erosion risks in Q4 FY26 due to the impending expiration of patents on several key drugs. This ‘patent cliff’ phenomenon creates structural earnings vulnerabilities as generic entrants rapidly erode branded drug market share, leading to steep declines in protected revenue streams.

Estimates indicate that between 2025 and 2030, pharmaceutical companies globally, including significant Indian players, face revenue at risk exceeding $300 billion as a result of patent expiries. The timing of these expirations is critical: earnings impacts intensify immediately upon patent lapses and generic market penetration. This dynamic necessitates urgent strategic responses in pipeline development and M&A activities to replenish revenue bases.

In the Indian context, firms exposed to this cycle report margin compression notwithstanding cost controls and operational efficiencies. The pattern reflects the sector’s systemic challenge: balancing innovation-driven growth against the inexorable revenue decline caused by regulatory and patent expiry timelines. Consequently, earnings trajectories for pharmaceutical companies in Q4 FY26 and beyond are marked by cyclical downturns triggered by patent expiry events, consistent with the relatively lower sector operating margin of 15% compared to the 30.3% average [Chart: Profit Margin Distribution in Q4 FY26].

The detailed analysis of key declining entities illuminates how sector-specific structural issues and cyclical pressures have materially impaired earnings performance in Q4 FY26. Understanding these root causes informs the critical need for targeted operational reforms and strategic repositioning to mitigate vulnerabilities and capitalize on emerging recovery opportunities discussed in subsequent sections.

Banking Sector Dynamics: Robust Growth Amid Underlying Credit and Operational Challenges

This subsection delves into the banking sector's pronounced resilience in Q4 FY26, highlighting the performance dichotomy between emerging small finance banks and traditional banking entities. It offers a focused analysis on key players within the sector, exploring growth drivers, integration outcomes, and systemic credit risk transmission, thereby situating banking dynamics within the broader corporates’ earnings and legal/regulatory outlook discussed in earlier sections.

Finkurve Financial Services’ Tech-Driven Phygital Expansion Fuels Remarkable Asset Growth

Finkurve Financial Services demonstrated exceptional momentum in FY26, with its Assets Under Management (AUM) surging by 149% year-on-year, crossing the INR 1,000 crore milestone. This nearly tenfold increase since FY23 underscores the successful execution of its technology-led phygital model, combining physical branch proliferation with digital adoption to deepen customer penetration in the secured lending space. The expansion from 73 to 105 branches effectively complemented its strong growth in active gold loan customers, nearing 28,506 by March 31, 2026.

The Q4 FY26 profit after tax doubling relative to the prior year quarter further illustrates operational leverage benefits stemming from technology investments and data-driven credit underwriting. This strategic approach buffered the company against traditional NBFC sector vulnerabilities, positioning Finkurve as a compelling example of how digital transformation can catalyze sustainable growth even amidst macroeconomic uncertainties and elevated sectoral scrutiny.

IDFC First Bank’s Acquisition Synergies Aid Strong Loan and Deposit Growth Amid Operational Setbacks

IDFC First Bank reported robust balance sheet growth in Q4 FY26, with advances increasing approximately 20% year-on-year and deposits expanding by about 17%. These gains reflect successful integration efforts following recent acquisitions, enhancing the bank’s footprint and retail customer base, particularly in the microfinance and unsecured lending segments. The bank’s credit card portfolio also experienced a double-digit growth rate, reinforcing its strategy of diversified retail banking expansion.

Nevertheless, operational challenges were notable, including a significant one-off fraud event that led to a post-tax profit impact of approximately INR 319 crore, tempering net income growth. Despite this, the bank maintained stable asset quality metrics, with gross NPA ratios improving marginally and provisions easing to the lowest level in two years. The net interest margin held relatively steady, evidencing prudent interest rate risk management. IDFC First Bank’s ability to absorb such shocks while preserving growth momentum underlines its resilience but also highlights the ongoing need for rigorous operational risk frameworks and enhanced internal controls.

Credit Risk Transmission and Regulatory Pressures Persistently Challenge NBFCs and Bank Linkages

The evolving linkages between NBFCs and the banking system continue to be a critical focal point, with credit risk transmission mechanisms playing a significant role in sectoral stability. Banks maintain substantial exposures to NBFCs through funding lines and derivative transactions, introducing counterparty and liquidity risks that have heightened supervisory attention. Recent regulatory actions and risk-weight recalibrations reflect these concerns, indicating a delicate balance between supporting NBFC credit growth and containing systemic risk.

In FY26, despite strong credit demand emanating from microfinance and retail segments, asset quality pressures surfaced due to heightened defaults in select sub-sectors. The sector’s reliance on short-term funding via commercial papers and debentures further exacerbated funding risks, leading to increased volatility in credit availability. Moreover, the gradual recovery in microfinance portfolios, although positive, remains vulnerable to external shocks and regulatory tightening. Consequently, banks and NBFCs are adopting prudential risk transfer instruments and enhanced credit risk monitoring to mitigate contagion risks, but these transitional dynamics necessitate careful vigilance in FY27.

The sectoral insights gleaned from banking performance, particularly involving the nuanced interplays between bank-led growth and NBFC vulnerabilities, form a crucial backdrop for understanding the broader financial regulatory environment. These dynamics inform the subsequent legal and regulatory analysis by illustrating how credit risk and operational resilience shape market sentiment and compliance expectations.

4. Legal and Regulatory Landscape: Beyond Formal Violations

Geopolitical Risks and Supply Chain Disruptions Impacting Indian Industry Resilience in Q4 FY26

This subsection examines the tangible effects of geopolitical turmoil on supply chain stability and cost structures within key Indian industrial players during Q4 FY26, with a particular focus on automotive firms. It contextualizes how international conflicts, fluctuating crude prices, and regional tensions compounded operational challenges, thereby influencing corporate earnings and strategic outlooks. This analysis provides critical insights into the vulnerabilities exposed and mitigated within supply chains under acute external pressures.

Quantifying Tata Motors’ Supply Chain Cost Pressures Amid Geopolitical Volatility

Tata Motors experienced significant supply chain cost pressures in Q4 FY26 as the intensification of geopolitical conflicts disrupted global logistics networks and heightened commodity price volatility. The company's domestic passenger vehicle segment gained momentum, yet overall profitability was narrowed by elevated input costs stemming largely from supply chain vulnerabilities. Notably, challenges faced by Jaguar Land Rover—such as tariffs, cyber incidents, and trade restrictions—underscored risks linked to international exposure.

In tangible terms, volatile metal prices and component shortages increased expenditure pressures, compelling Tata Motors to implement robust cost containment measures. These included structural cost reductions alongside price adjustments across product lines to offset margin erosion. Additionally, their strategic push for vertical integration and localization, especially in battery manufacturing for electric vehicles, emerged as a critical lever to reduce dependency on unstable international supply routes and mitigate future geopolitical risks.

Measuring the Effects of Crude Oil Price Volatility on Corporate Earnings and Inflationary Dynamics

The surge in crude oil prices throughout FY26, particularly peaking around $110 per barrel driven by Middle Eastern conflicts and associated supply disruptions, materially affected input costs across energy-intensive sectors in India. This price volatility intensified inflationary pressures that fed through production and logistics expenses, as well as higher operating costs for businesses reliant on imported fuel and petroleum derivatives.

Indian corporates confronted margin headwinds as rising crude costs propagated cost-push inflation. While some manufacturing and infrastructure sectors benefited from concurrent policy tailwinds, the overall upward pressure on input costs compressed operating margins and exerted downward pressure on earnings growth. Persistent crude price uncertainty also complicated financial planning and risk management, compelling firms to enhance hedging strategies and scenario-based forecasting to navigate volatile commodity landscapes.

Analyzing Operational Disruptions from Regional Political Tensions and Their Implications for Indian Industry

The geopolitical landscape surrounding India in Q4 FY26, marked by escalating tensions in West Asia and ongoing regional uncertainties, induced intermittent disruptions in supply chains and trade routes. Incidents such as targeted refinery attacks, strained diplomatic relations, and transport chokepoint vulnerabilities undermined the smooth flow of essential raw materials and components critical to manufacturing and services sectors.

These disruptions translated into measurable operational setbacks, including delays in inventory replenishment, increased lead times, and cost overruns. Firms across sectors had to recalibrate production schedules, reassess supplier dependencies, and intensify dialogue with regulatory authorities to manage compliance amid evolving export-import restrictions. This environment elevated the importance of operational agility and supply chain transparency as foundational elements to maintain competitiveness.

Assessing Corporate Supply Risk Mitigation Strategies Activated in FY26 and Planned for FY27

In response to acute geopolitical and supply chain risks witnessed in FY26, leading Indian corporations adopted multifaceted mitigation strategies emphasizing supply chain resilience and cost optimization. Tata Motors, for example, leveraged advanced localization initiatives, including ramping up in-house battery cell manufacturing to insulate against global sourcing disruptions and price shocks.

More broadly, companies implemented diversified sourcing frameworks, engaged in scenario planning for supply contingencies, and invested in digital supply chain monitoring tools for real-time risk assessment. These efforts align with industry-wide shifts toward modular manufacturing, multi-region supplier networks, and enhanced inventories to buffer against future geopolitical shocks. The strategic orientation for FY27 prioritizes consolidation of these adaptations to sustain operational continuity and profitability amidst persistent uncertainty.

Having explored the multifaceted influences of geopolitical risks on operational costs and supply chain stability, the report will next delve into how regulatory perceptions and compliance considerations are shaping market sentiment and corporate valuations in the Indian industrial landscape.

Compliance Perceptions, Regulatory Impact, and Market Sentiment Dynamics in Q4 FY26

This subsection explores the nuanced role of regulatory compliance perceptions on Indian corporate valuations and investor sentiment during Q4 FY26. Moving beyond explicit legal violations, it examines how evolving regulatory expectations and compliance challenges have shaped market pricing, credit risk profiles—particularly within fintech—and sector-specific valuation shifts. This analysis deepens understanding of the legal and regulatory landscape’s indirect yet powerful influence on market behavior and valuation dynamics, integrating investor confidence as a key channel.

Regulatory Compliance Influence on Valuation Multiples across Indian Sectors

In Q4 FY26, Indian companies navigated a complex regulatory environment where compliance perceptions increasingly influenced valuation multiples beyond tangible legal infractions. Firms demonstrating rigorous adherence to emerging regulatory standards and proactive compliance strategies commanded premium market valuations, reflecting investor confidence in sustainable governance practices. This premium was particularly evident among companies with robust transparency measures, governance disclosures, and risk management frameworks, which collectively reduced perceived regulatory and operational risks.

Evidence suggests that investors are differentiating between companies that merely meet minimum compliance requirements and those that embed compliance into strategic risk management. The latter group attracted higher price-to-earnings multiples, driven by expectations of reduced litigation exposure, smoother regulatory approvals, and stronger stakeholder trust. Conversely, firms with unclear compliance records or perceived lapses—albeit without formal sanctions—suffered valuation discounts, indicating that regulatory uncertainty adversely affects market perceptions even in the absence of formal enforcement actions.

Credit Risk Transmission and Sentiment Impact in the Fintech Sector Amid Regulatory Ambiguity

The fintech segment in India continued to grapple with regulatory ambiguity in Q4 FY26, where evolving compliance requirements influenced credit risk profiles and market sentiment. Despite robust profit growth and core lending expansion, fintech firms faced heightened scrutiny over regulatory adherence, particularly in digital lending, data privacy, and anti-money laundering norms. This scrutiny has translated into increased caution among credit investors and rating agencies, moderating valuations even as operational metrics improved.

Moreover, the transmission of regulatory risk into credit costs was evident through more conservative underwriting practices and increased provisioning levels. Market reactions have further manifested in valuation multiples, with fintech firms exhibiting greater volatility relative to traditional banks, reflective of regulatory uncertainty and the sector's dynamic risk exposure. The relationship underscores that compliance perception functions as a critical non-financial factor shaping credit and equity market outcomes in this rapidly evolving domain.

Sector-Specific Valuation Shifts Driven by Regulatory Landscape Evolution

Sectoral valuation shifts in Q4 FY26 highlight the differentiated impact of regulatory changes across industries. For instance, the pharmaceutical sector, facing ongoing patent expiries and pricing reforms, experienced selective valuation compression reflecting investor wariness about heightened regulatory risks. In contrast, IT services and technology firms benefited from relatively stable regulatory frameworks and investor optimism around compliance with data privacy and export control norms, sustaining premium valuations despite geopolitical uncertainties.

Furthermore, industries exposed to environmental and digital governance regulations, such as manufacturing and telecommunications, are undergoing recalibrations in market valuations that factor in anticipated compliance costs and operational adjustments. Evidence indicates that investors are increasingly incorporating forward-looking regulatory compliance trajectories into valuation models, emphasizing the significance of adaptive governance in preserving corporate value amid shifting regulatory paradigms.

These sectoral valuation nuances also correspond with operational performance trends, as highlighted by several companies that faced significant revenue and profit challenges in Q4 FY26. For example, ITC in consumer goods reported a 73% revenue decline with a corresponding negative profit impact, Reliance Infrastructure in logistics saw a 79% revenue drop severely affecting earnings, and a key pharmaceuticals company experienced a 40% revenue decline alongside severe profit impairment [Table: Companies Facing Operational Struggles in Q4 FY26]. Such financial stresses underscore how regulatory concerns and compliance complexities compound operational vulnerabilities, influencing market valuation outcomes.

Investor Sentiment Fluctuations Linked to Regulatory Compliance Perceptions

Investor sentiment throughout Q4 FY26 revealed heightened sensitivity to compliance signals, even absent direct enforcement outcomes. Market participants exhibited increased risk aversion towards firms flagged for potential regulatory lapses or disclosed compliance shortcomings, driving short-term share price volatility and tightening credit spreads. Conversely, companies articulating transparent compliance roadmaps and demonstrating responsiveness to regulatory guidance stabilized investor confidence and mitigated downside risk.

This dynamic suggests that compliance perception acts as a proxy for governance quality, influencing capital allocation decisions and market liquidity conditions. It also drives a feedback loop wherein improved compliance frameworks enhance investor trust, which in turn supports valuation durability and access to capital. The interplay emphasizes the strategic importance for corporates to proactively manage regulatory narratives and embed compliance as a core facet of investor relations.

Having analyzed how compliance perceptions shape market valuations and sentiment, the subsequent subsection will examine the interplay of geopolitical risks and supply chain disruptions, highlighting additional external legal and operational challenges impacting Indian corporates in Q4 FY26.

Policy Tailwinds and Emerging Regulatory Frontiers: Catalyzing Infrastructure Growth and Digital Payment Evolution Amid New Environmental Mandates

This subsection explores the vital role governmental policy initiatives and regulatory reforms have played in shaping the Indian corporate landscape in Q4 FY26. It particularly focuses on the fiscal stimulus provided by accelerated infrastructure spending, the transformational regulatory changes in digital payment systems, and emergent environmental compliance obligations. Understanding these factors offers strategic insight into how policy tailwinds can sustain corporate earnings momentum, while new regulatory frontiers pose evolving compliance challenges requiring proactive navigation.

Surge in Government Infrastructure Spending as a Growth Stimulus

The fiscal year FY26 witnessed an unprecedented scaling up of government capital expenditure, with budget allocations increasing more than fourfold over recent years. This surge positioned infrastructure development as a principal growth driver in the Indian economy. Expansion across multiple verticals—ranging from highways, railways, and aviation to power generation—has markedly enhanced connectivity and production capacity. For instance, the national highway network expanded by approximately 60% over the past decade, coupled with near-complete railway electrification, catalyzing reductions in logistics costs and improving supply chain resilience.

Such infrastructure investments have created durable tailwinds for sectors directly linked to construction, engineering, and capital goods. Additionally, the multiplier effects extend into consumer markets by boosting employment and stimulating demand in ancillary industries. Importantly, these fiscal approaches counterbalance cyclical headwinds from global uncertainties and domestic economic adjustments, fostering an environment conducive to diversified corporate earnings growth. The scale and continuity of spending signal government commitment to long-term structural transformation, a crucial consideration for corporate strategists assessing sectoral investment opportunities.

Digital Payment Regulations Fueling Innovation and Market Stabilization

Parallel to physical infrastructure development, FY26 saw significant regulatory evolution within the digital payments ecosystem, reinforcing India’s position as a global leader in fintech innovation. Regulatory bodies introduced comprehensive frameworks that strengthened operational security, consumer protection, and systemic stability, while fostering a fertile ground for emerging technologies such as stablecoins and tokenization. Enhanced licensing regimes and sandbox environments enabled payment service providers to trial innovations under supervised conditions, thereby reducing market entry barriers and accelerating product rollout.

The regulatory environment also encouraged private sector participation, evident in robust investments supporting initiatives like the Unified Payments Interface (UPI). These developments not only widened financial inclusion but also improved interoperability and user experience. Despite operational challenges such as technical glitches and data privacy concerns, continuous regulatory refinement aims to build investor confidence and underpin sustainable sectoral valuations. Consequently, compliance with evolving payment norms has become a critical strategic imperative, shaping how companies position themselves in a rapidly digitizing economy.

Rising Environmental Compliance Costs Reshape Industry Margins and Strategic Planning

Environmental regulations emerged as a growing influence on corporate cost structures and competitive dynamics in Q4 FY26, with mandates intensifying across sectors. Policies targeting carbon emissions, resource circularity, and pollution control introduced compliance burdens that vary substantially across industries. For example, manufacturing, chemicals, and metals sectors face relatively high environmental compliance costs, potentially exceeding significant proportions of net profits for smaller enterprises. These costs encompass both direct expenditures for pollution control technology and indirect impacts such as energy price escalations.

Alongside compliance cost considerations, firms must navigate a fragmented regulatory landscape characterized by overlapping jurisdictional requirements at national and subnational levels. This complexity necessitates enhanced governance frameworks and can lead to operational inefficiencies if not proactively managed. However, early movers investing in sustainable practices and circular economy principles may capture first-mover advantages, including access to preferential financing and improved stakeholder trust. Overall, heightened environmental focus compels companies to integrate regulatory risk management into strategic planning and capital allocation decisions.

Nascent Regulatory Domains Requiring Strategic Vigilance and Adaptive Responses

Beyond established policy corridors, Q4 FY26 saw the emergence of new regulatory areas warranting close monitoring by corporate decision-makers. These include tightening governance requirements for charitable trusts and not-for-profit entities, as well as increased scrutiny of data privacy and cybersecurity within financial services. For instance, legislative changes impacting institutional trusts underscore the evolution toward greater accountability and transparency, which, while challenging legacy structures, present opportunities for governance modernization and value unlocking.

Moreover, advancements in digital finance are now intersecting with cross-border regulatory harmonization efforts, particularly in fintech and crypto asset domains. Companies must anticipate growing expectations related to operational risk management and consumer safeguards. Given the accelerating pace of regulatory shifts worldwide, implementing agile compliance and risk frameworks will be critical to maintaining market access and investor confidence. Strategic foresight in these frontier areas enables firms to transform compliance challenges into competitive differentiation.

Having established how policy tailwinds have underpinned growth while new regulatory frontiers introduce complexity, the report will next delve into how these dynamics interact with legal and compliance challenges, situating corporate earnings outcomes within the broader legal landscape.

5. Forward-Looking Analysis: Sustaining Momentum Amid Challenges

Macroeconomic Headwinds and Their Implications on Indian Corporate Earnings in FY27

This subsection delves into the critical macroeconomic factors shaping the outlook for Indian corporations as they transition from Q4 FY26 into FY27. By examining projected crude oil price trajectories, inflationary pressures, currency depreciation, and foreign investment flows, it provides a comprehensive understanding of the external and internal economic shocks businesses are set to confront. This foundation is essential for contextualizing sector-specific earnings projections, risk management needs, and strategic planning outlined in subsequent sections.

Projected Crude Oil Price Trends and Quarter-by-Quarter Variability in FY27

Crude oil prices stand as a principal determinant of cost dynamics and inflationary pressures for Indian industry. Consensus forecasts for FY27 suggest Brent crude will exhibit significant quarterly volatility, reflecting both geopolitical tensions and fluctuating global demand. Analysts project prices could range approximately between $90 and $115 per barrel across the fiscal year, with a peak expected in the first half near $110 to $113, largely influenced by ongoing Middle East conflicts and supply constraints. The latter half of FY27 may see a gradual price correction as supply adjustments take hold and demand softens seasonally.

Such price oscillations translate to material input cost volatility for oil-importing sectors, intensifying margin uncertainty. Given India's heavy dependence on crude imports, even incremental $10 per barrel increases bear a direct inflationary footprint, estimated at 55 to 60 basis points per $10 rise, alongside amplified current account deficits. This erratic oil price environment compels companies to adopt agile cost management and hedging strategies to mitigate margin erosion risks.

Projected crude prices for FY27 indicate a declining trend after a Q1 peak of $110 per barrel, dropping to $95 in Q2, a slight rise to $100 in Q3, and diminishing back to $90 by Q4. This quarter-by-quarter volatility underscores the margin pressures and operational challenges companies will face throughout the year [Chart: Crude Oil Price Trends Impact on Earnings].

Inflationary Impact on Corporate Margins and Operational Costs in FY27

Inflation forecasts for FY27 indicate sustained pressures on corporate margins, primarily driven by persistent energy price upticks and second-round effects on wages and raw material costs. Consumer Price Index inflation is expected to moderate somewhat compared to FY26 but remain elevated in the 2.0-3.0% range during FY27, with core inflation anchored near 2.0-2.5 percent. This suggests continued but gradually easing input cost headwinds for firms, particularly in energy- and commodity-intensive industries.

The inflation environment compounds the squeeze on profit margins as companies face lagged pass-through of rising costs to end customers amid competitive market conditions. While firms possessing strong pricing power and operational flexibility may navigate these pressures effectively, those in sectors with rigid cost structures or exposed to global supply chain bottlenecks risk margin compression and diluted earnings growth. Moreover, inflation-induced input cost escalation influences capital allocation decisions, potentially restraining discretionary spending and investment.

Magnitude and Timing of Rupee Depreciation: Effects on Importers, Exporters, and Capital Markets