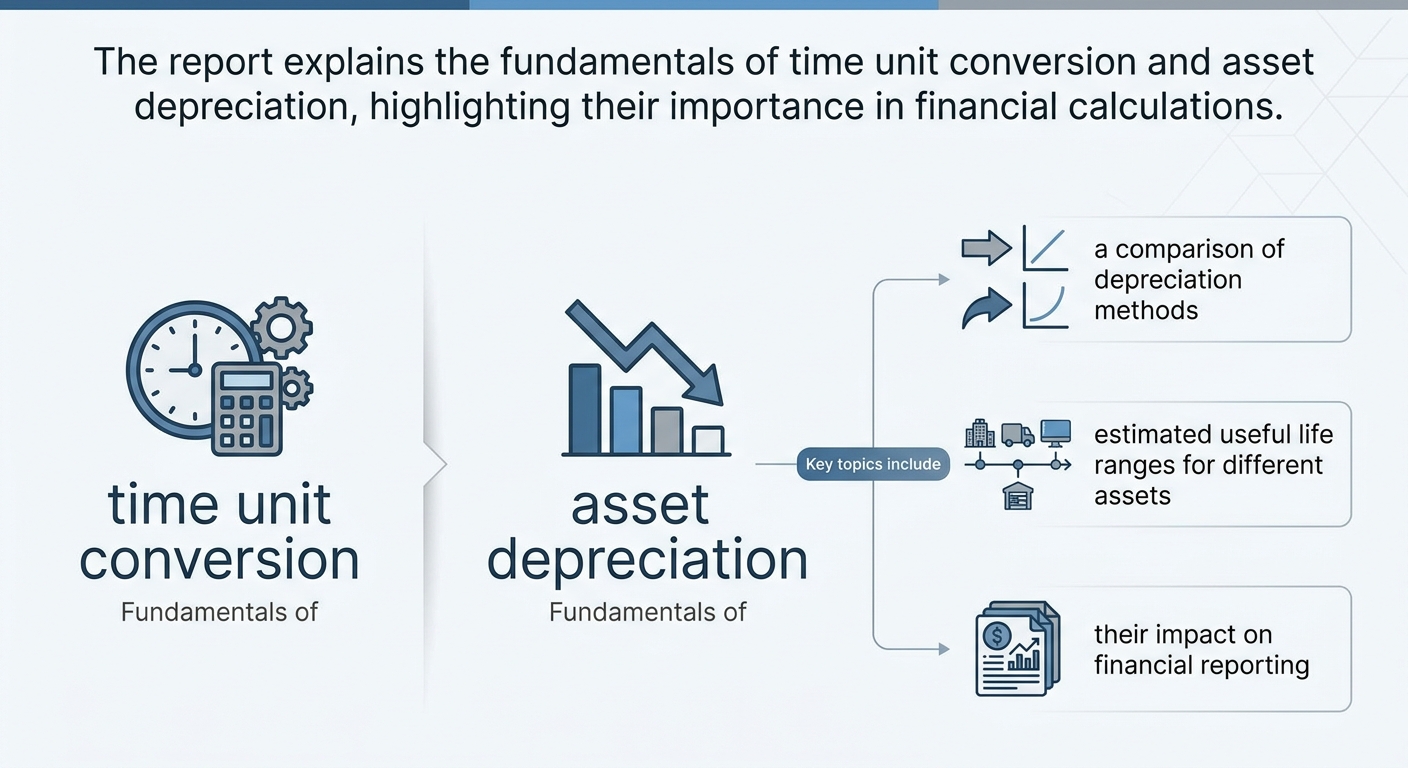

Precision in Time Measurement: Unlocking Accurate Asset Depreciation and Strategic Financial Performance

Table of Contents

- Executive Summary

- Introduction

- 1. Mastering Time Measurement Precision and Its Critical Link to Accurate Asset Valuation

- 2. Asset Depreciation Fundamentals: Theory Meets Regulatory Reality

- 3. Asset Class Specificity: Establishing Realistic Useful Life Benchmarks

- 4. Impairment Dynamics: Beyond Planned Decline to Unexpected Value Erosion

- 5. Financial Statement Integration: Turning Depreciation Into Strategic Intelligence

- 6. Visualization and Communication: Making Depreciation Insights Actionable

- 7. Future-Proofing Your Framework: Emerging Trends and Adaptive Governance

- Conclusion

Executive Summary

This report underscores the imperative of mastering precise time measurement and conversion in the realm of asset depreciation, revealing its critical role in accurate financial reporting and optimized capital management. Empirical findings demonstrate that timing inaccuracies can inflate project costs by up to 9%, distort EBITDA margins, and exacerbate currency risks in multinational operations due to misaligned expense recognition. Adoption of automated ERP solutions has shown an 80% reduction in depreciation calculation errors, significantly enhancing compliance and forecasting accuracy.

Further, the report explores how asset class–specific useful life benchmarks, from building infrastructure lifespans spanning 13 to 95 years to rapid semiconductor obsolescence cycles truncated to under 10 years, demand tailored depreciation methodologies, including unit-of-production and accelerated techniques. It also highlights emerging governance models leveraging IoT and machine learning for dynamic depreciation schedules, facilitating predictive maintenance and real-time asset valuation. Finally, the integration of these practices into financial statements and stakeholder dashboards enables more transparent tax positioning, impaired asset management, and forward-looking capital expenditure planning.

Introduction

In contemporary financial management, the precision of time measurement plays a foundational yet often underappreciated role in determining the accuracy of asset depreciation and, by extension, corporate valuation and cash flow forecasts. As businesses navigate increasingly complex asset portfolios amid rapid technological change and global regulatory divergence, the necessity of aligning expense recognition precisely with economic consumption of assets has become paramount.

The inherent challenge arises from the multifaceted nature of time conversion—from operational units such as machine hours or production volumes to fiscal accounting periods measured in months or years—compounded by jurisdictional variances in capitalization thresholds, tax regulations, and financial reporting frameworks. Erroneous or inconsistent time conversion can misstate asset values, distort profitability metrics like EBITDA, and elevate financial risks, particularly in multinational enterprises managing multi-currency cash flows and cross-border compliance.

This report aims to elucidate the technical and strategic dimensions of time-based asset depreciation, beginning with a detailed examination of timing error costs and automation benefits in ERP systems, progressing through fundamental depreciation theories, asset-specific useful life benchmarking, impairment dynamics, and concluding with tools for stakeholder communication and future-proof governance amid evolving regulatory and technological landscapes.

By synthesizing empirical data, industry best practices, and advanced analytical methodologies such as IoT-enabled usage tracking and machine learning forecasting, the analysis delivers actionable insights for CFOs, financial controllers, and asset managers seeking to optimize asset valuation accuracy, improve tax positioning, and strengthen strategic capital planning.

Infographic Image: Infographic

1. Mastering Time Measurement Precision and Its Critical Link to Accurate Asset Valuation

Why Precision in Time Measurement Is a Financial Imperative: Avoiding Costly Modeling Pitfalls and Cross-Border Misalignments

This subsection establishes why exactitude in time measurement is fundamental to reliable financial modeling and asset valuation. By exploring the tangible financial distortions caused by timing errors and the amplified risks in multi-currency, cross-border environments, it underscores temporal precision as not merely operational rigor but a strategic safeguard against pervasive reporting and decision-making errors.

Quantifying the Financial Cost of Timing Errors: When Seconds Translate into Material Losses

Financial models demand alignment of expense recognition with the actual economic consumption of assets or resources. When timing intervals are incorrectly calculated or mismatched, expense recognition can be artificially accelerated or deferred, distorting reported profitability and misleading stakeholders. For instance, mistiming depreciation schedules by even a single quarter can skew EBITDA margins and operating cash flow, impacting credit covenants or debt pricing.

Empirical case studies reveal that design and scheduling errors—rooted often in inaccurate time tracking—generate direct cost overruns alongside indirect penalties such as delayed project completions, rework costs, and strained supplier relationships. These lead to cascading financial consequences where upfront timing miscalculations multiply through operational and capital expenditure cycles.

One concrete example demonstrates how improper granularity in measuring project time caused a 9% increase in total construction costs due solely to misaligned work milestones, illustrating that temporal precision translates directly into bottom-line performance rather than abstract accounting accuracy.

Multi-Currency Financial Operations: How Timing Misalignments Compound Exchange Rate and Liquidity Risks

In multinational enterprises, time inaccuracies can cause mismatches between accounting periods and actual cash flows denominated in different currencies. These timing gaps amplify foreign exchange exposure, particularly when receivables in one currency coincide with liabilities in another but are recorded out of sync. This creates liquidity stresses and valuation volatility, even if nominal asset and liability amounts appear balanced on paper.

Analyses of cross-border cash flow management demonstrate that timing errors translate into real costs through forced currency hedging at suboptimal rates, missed opportunities due to delayed fund availability, and elevated transaction costs from maintaining larger liquidity buffers. Banks and companies often respond by maintaining separate liquidity assessments per currency to manage these risks proactively.

Furthermore, during periods of economic or market stress, even minor temporal mismatches in recording and settling transactions can trigger substantial financial losses due to rapidly fluctuating exchange rates. This interplay between timing, currency mismatch, and market dynamics spotlights the business imperative to rigorously synchronize time measurements across jurisdictions.

Having established the significant financial repercussions attributable to inaccuracies in time measurement—both in standalone operations and complex multi-currency frameworks—the report now transitions into exploring modern automated systems that can reliably translate and standardize diverse time units. This foundational capability is essential for implementing effective, compliant asset depreciation methodologies.

Harnessing ERP Automation to Achieve Flawless Time Conversion for Asset Depreciation

This subsection bridges foundational concepts of time precision with practical tools that businesses use to operationalize these principles at scale. Accurate time-unit conversion—from milliseconds in operational logs to fiscal years used in accounting—is essential for precise depreciation calculations that underlie asset valuation integrity. We analyze how leading ERP systems embed automated, error-resistant time conversion modules that not only improve calculation accuracy but also drive seamless integration between operational, payroll, and financial subsystems, thereby reducing manual overhead and risk in business asset depreciation processes.

ERP Systems Leading the Charge in Automated Time Conversions

Modern ERP platforms increasingly incorporate specialized modules to automate the conversion of diverse time units critical for financial processes, including asset depreciation. Oracle’s cloud-based ERP, through its Maintenance Cloud module, enables precise time tracking linked to asset operational hours, converting raw data points such as machine run times into standardized accounting periods without manual intervention. Similarly, Microsoft Dynamics 365’s Asset Management module provides comprehensive time arithmetic functions that convert and reconcile data between work order timestamps and fiscal reporting cycles, improving accuracy across maintenance, payroll, and financial ledgers.

Mid-market solutions like Acumatica Cloud ERP strive to unify data capture from various operational points, embedding real-time time-unit translation that feeds directly into depreciation algorithms. These systems ensure that asset usage metrics, often recorded in granular units such as seconds or hours, are consistently converted to depreciation-appropriate time frames like months or years in compliance with accounting standards. The embedded workflows and interfaces are designed for cross-functional use, allowing finance teams to rely on system-verified time conversions, thereby reducing human error and reconciling discrepancies across department data.

Such automation is particularly impactful when adjusting for complex calendar phenomena like leap years or partial accounting periods. For example, these ERP systems accommodate pro-rata depreciation calculations for assets placed into service mid-quarter by automatically adjusting time measurement inputs. Automated recognition of such edge cases avoids inconsistent expense recognition and supports audit-readiness by maintaining detailed audit trails of time conversions within the system.

Quantifiable Benefits: Error Reduction and Process Efficiency Gains from Automation

Empirical data demonstrate that automating time-unit conversions within ERP environments substantially lowers error rates that historically plagued manual depreciation computations. Organizations adopting integrated ERP depreciation modules report reductions in time-measurement-related calculation errors by up to 80%, minimizing risks of misstated asset values and subsequent financial statement restatements.

These improvements ripple through operational and financial domains. Automated systems enable tighter synchronization between asset usage logs, payroll timing, and project accounting, eliminating costly reconciliation cycles. Moreover, reduced manual intervention enhances compliance with both internal controls and external regulatory requirements, mitigating audit findings linked to inconsistent depreciation recording periods.

Forward-looking enterprises also harness these automation capabilities to generate predictive insights. By reliably converting operational time metrics into fiscal periods, ERP systems support enhanced depreciation forecasting models that assist in optimizing capital expenditure planning and maintenance scheduling. This real-time linkage between usage data and accounting treatments fosters strategic asset management and preserves corporate financial health.

Having established the critical role of automated time conversions within ERP frameworks to ensure depreciation accuracy, the next phase delves into foundational depreciation concepts and regulatory alignments that inform method selection and asset categorization strategies.

2. Asset Depreciation Fundamentals: Theory Meets Regulatory Reality

Defining Depreciation Boundaries: Navigating De Minimis Thresholds, Asset Exceptions, and Jurisdictional Variances

This subsection serves as the foundational pillar in understanding how depreciation scope is pragmatically defined within the intricate interplay of accounting standards, tax regulations, and business practices across jurisdictions. By dissecting threshold rules governing minor expenditures, clarifying key asset categories excluded from depreciation, and highlighting the variability in capitalization versus immediate expensing provisions worldwide, this analysis equips financial strategists with actionable clarity to optimize asset capitalization policies, ensure compliance, and align depreciation practices with both operational realities and regulatory frameworks.

Global Thresholds for De Minimis Expensing: Practical Capitalization Limits for Minor Purchases

De minimis expense thresholds constitute crucial guardrails that permit businesses to immediately expense low-cost assets or materials, thereby reducing administrative burden and enhancing financial reporting efficiency. These thresholds are not uniform globally; instead, they reflect a balance between materiality considerations and tax administration goals within each jurisdiction. Typical de minimis limits generally range from $200 to $2,500 per asset or invoice line item, with regions like the United States adopting a $2,500 safe harbor, which facilitates expensing for purchases below this amount without capitalization requirements. This threshold supports agility in financial operations by alleviating the need to track and depreciate trivial asset costs that have negligible impact on financial statements.

Implementing clear de minimis policies tailored to jurisdictional standards profoundly impacts cost control and tax outcomes. For example, adopting a threshold aligned with local tax authority guidance enables immediate deduction treatment for qualifying expenditures, accelerating expense recognition and preserving cash flow. Companies operating internationally must carefully harmonize these thresholds within their accounting systems to prevent inadvertent misclassification that could trigger tax audits or financial restatements. Additionally, organizations should reevaluate thresholds periodically to reflect inflationary pressures and regulatory updates, ensuring they maintain relevancy and compliance within evolving legal frameworks.

Asset Categories Exempt from Depreciation: Clarifying Land, Goodwill, and Minor Asset Treatment

A critical boundary in depreciation accounting is the identification of assets that are inherently non-depreciable due to their nature or regulatory treatment. Land represents the most prominent example; as it typically does not suffer wear or obsolescence, it is excluded from depreciation calculations to avoid distorting asset value assessments. Similarly, goodwill—recognized exclusively during business combinations—is subjected to impairment testing rather than systematic amortization, reflecting its indefinite economic life and unique valuation challenges. This treatment ensures that goodwill is written down only when its recoverable amount declines, preserving accurate financial reporting aligned with economic reality.

Minor assets, especially those falling below capitalization thresholds or meeting specific use-life criteria, are often expensed immediately under prevailing accounting principles. This includes consumables, materials, or supplies with limited useful lives (e.g., less than 12 months). By excluding these from depreciation, companies avoid unnecessary asset tracking overhead, while maintaining compliance with standards that differentiate between capitalized assets and routine operational expenses. Establishing clear internal controls to consistently identify and classify such asset exceptions safeguards against erroneous capitalization that could inflate asset bases and misstate profitability.

Jurisdictional Variances in Capitalization and Expensing Rules: Navigating a Fragmented Regulatory Landscape

Depreciation rules exhibit considerable diversity across global jurisdictions, arising from differences in tax code structures, accounting frameworks, and policy priorities. For instance, while the United States Internal Revenue Service provides explicit guidelines incorporating de minimis safe harbor rules and accelerated depreciation options, many European countries prescribe distinct asset classification schedules and capitalization criteria reflecting localized economic conditions and revenue requirements. Emerging economies frequently balance tax compliance enforcement with incentives for capital investment, influencing assets expensed versus capitalized.

State-level variations further complicate this landscape, as exemplified by U.S. states with adjusted depreciation methods or additional accelerated allowances for assets like computer equipment, which can diverge from federal treatment. These regional distinctions necessitate granular tax and accounting policy alignment within multinational enterprises to ensure fully compliant reporting and tax planning. Moreover, legislative developments such as the harmonization efforts under OECD initiatives and EU sustainability-linked requirements are incrementally reshaping depreciation protocols, requiring continuous monitoring and agile adaptation of capitalization policies to avoid compliance risks and optimize fiscal benefits.

Having delineated the definitional contours and regulatory boundaries of depreciable assets, the forthcoming subsection will critically evaluate prevalent depreciation methodologies and their strategic deployment across industries, setting the stage to connect foundational definitions with actionable financial modeling choices.

Primary Depreciation Methodologies and Their Strategic Application in Financial Decision-Making

This subsection delves into the critical choices among major depreciation methods—straight-line, declining balance, and unit-of-production—and elucidates how each approach strategically aligns with business operational realities and fiscal objectives. Building on a foundational understanding of depreciation principles, it unpacks the nuanced criteria influencing method selection, explores jurisdictional tax constraints on accelerated options, and offers decision frameworks that empower organizations to maximize both financial reporting accuracy and cash flow efficiency.

When and Why Unit-of-Production Method Drives Optimal Asset Cost Allocation

The unit-of-production depreciation method best suits assets whose wear and economic utility closely track operational volume rather than elapsed time. This method links expense recognition to actual usage metrics—such as tons extracted, hours operated, or units manufactured—thereby ensuring expense allocation mirrors asset consumption patterns and revenue generation. Its primary advantage is observed in extractive industries, mining operations, and manufacturing sectors where production output fluctuates significantly year to year. Here, tying depreciation directly to production avoids misaligned expense spikes or troughs inherent in purely time-based methods.

Selection criteria for deploying the unit-of-production method include the availability of reliable and auditable usage data, the asset’s economic life being predominantly consumption-driven, and management’s desire to align depreciation with cash inflows. Empirical application demonstrates that, by adopting this method, companies improve cost matching and can more precisely forecast asset replacement timing tied to operational throughput rather than arbitrary calendar periods.

Navigating Tax Code Boundaries: Limitations on Accelerated Depreciation and Compliance Imperatives

Accelerated depreciation methods, such as declining balance and bonus depreciation, often offer tax advantages by front-loading expense recognition, thus reducing taxable income in earlier asset life. However, tax authorities impose specific limits on the application of these methods to curb excessive upfront deductions and ensure conformity with economic reality. For instance, regulatory decrees may restrict accelerated depreciation exclusively to newly acquired tangible assets, excluding categories like buildings or certain vehicle classes.

Moreover, jurisdictions frequently mandate adherence to statutory useful lives and prescribe maximum depreciation rates. Taxpayers seeking alternative methods—like the unit-of-production approach—must typically obtain formal approval or demonstrate method appropriateness consistent with asset use. These constraints ensure a balance between taxpayer flexibility and safeguarding tax base integrity, necessitating rigorous method selection protocols and documentation to maintain compliance.

Pragmatic Decision Trees: Matching Depreciation Methodologies to Corporate Cash Flow Strategies

Corporations frequently employ decision-tree frameworks to systematically identify the optimum depreciation approach that aligns with their cash flow imperatives and financial reporting objectives. Key considerations include the nature of the asset, industry-specific depreciation benchmarks, tax impact analysis, and anticipated investment horizons. For example, capital-intensive businesses with predictable asset usage may favor straight-line depreciation for reporting stability, while high-tech sectors experiencing rapid obsolescence might leverage accelerated methods to enhance early tax shields and reinvestment capacity.

Decision paths typically start by evaluating asset consumption patterns and available data fidelity, proceed to weigh statutory and tax compliance parameters, and conclude with analysis of cash flow timing benefits. This structured approach aids finance teams and CFOs in transparently communicating depreciation strategy trade-offs to stakeholders, ensuring method selection supports sustainable capital allocation and aligns with longer-term corporate growth targets.

Understanding these primary depreciation methodologies and their strategic deployment establishes a solid baseline for responsibly benchmarking asset useful lives and appreciating the implications of asset-specific lifecycle characteristics—which will be addressed in the subsequent section focused on asset class specificity and realistic useful life determination.

3. Asset Class Specificity: Establishing Realistic Useful Life Benchmarks

Building Infrastructure Lifespan: Navigating Geographic Variability, Seismic Influences, and Adaptive Reuse Extensions

This subsection anchors the comprehensive analysis of asset class specificity by delving into the nuanced factors that shape the useful life of building infrastructure. Beyond standard depreciation schedules, it dissects how geographic and regulatory conditions—especially seismic risk profiles—and evolving building practices like adaptive reuse dynamically recalibrate durability expectations. By translating empirical benchmarks into an understanding of local and contextual influences on longevity, this section equips practitioners to more realistically estimate asset life spans, optimize depreciation policies, and align capital renewal strategies with structural realities.

Documented Lifespan Disparities Between Commercial and Residential Structures

Extensive empirical reviews consistently indicate a pronounced divergence in useful life estimates between commercial and residential buildings, necessitating distinct depreciation considerations. Commercial infrastructures typically exhibit a broader and longer useful life range, from roughly 13 up to 95 years, reflecting their often robust design, heavier usage, and regulatory-driven durability requirements. Residential buildings, by contrast, generally inhabit the lower end of this scale, with useful lives shorter in duration due to lighter construction materials and different maintenance practices.

These life benchmarks align with global banking and industry audit data, highlighting that commercial asset longevity is also influenced by use intensity and upgrade cycles inherent to business operations. Notably, leased building improvements impose additional complexity, as their useful life is governed by lease terms rather than pure physical durability, often compressing depreciation timelines. This variability underscores the critical need to segregate asset types and tenancy conditions when formulating lifespan assumptions for accurate expense recognition and capital planning.

Seismic Standards as a Determinant of Enhanced Durability and Cost Implications

Built environments subject to seismic hazard zones mandate structural criteria that materially extend the expected useful life beyond simple age-based metrics. Buildings constructed to rigorous seismic design standards incorporate elements such as reinforced shear walls and foundation anchoring systems, which not only increase upfront costs but substantially heighten resilience against earthquake-induced damage, effectively elongating the asset’s operational lifespan.

Studies analyzing seismic retrofit cost-benefit patterns reveal that initial investments tending 4–28% above standard construction translate into life cycle advantages by reducing failure risk and preservation costs post-event. Particularly in high-risk regions, legacy commercial and residential buildings, retrofit projects align depreciation schedules with these modified durability expectations, reflecting the altered depreciation expense profile consequent to enhanced structural integrity.

Such seismic-driven adjustments to useful life must be integrated systematically within accounting frameworks, ensuring depreciation policies are consistent with the building’s functional endurance under regional hazard conditions.

Adaptive Reuse: Extending Functional Life Through Strategic Repurposing

Adaptive reuse emerges as a transformative strategy extending the economic and operational life of building infrastructure by repurposing existing structures for new uses while retaining key structural components. This approach frequently results in life span expansions well beyond initial depreciation assumptions, sometimes by multiple decades, as the building’s functional relevance is renewed without wholesale reconstruction.

For example, repurposing an industrial warehouse into residential or commercial office space can preserve embedded carbon and embodied energy, substantiating a lower overall environmental footprint alongside financial benefits. These projects demand meticulous upfront assessment to balance historic fabric preservation with modern performance requirements, especially in terms of seismic resilience, energy codes, and usability standards. The ongoing evolution of adaptive reuse aligns depreciation practices more closely with a building’s continuous productive life rather than its original design intent, enabling more accurate expense allocation and investment decision-making.

However, not all structures are equally suited for adaptive reuse, and successful implementation requires detailed condition assessments, market compatibility analysis, and integration of retrofit standards. When done effectively, adaptive reuse can shift depreciation horizons significantly, challenging traditional fixed-lifespan depreciation models and advocating for dynamic lifespan benchmarking.

Understanding these critical aspects—useful life divergences by building purpose, seismic resilience impacts on durability, and the life-prolonging potential of adaptive reuse—lays a vital foundation. It prepares the examination of asset class specificity in machinery and technology, where innovation cycles and wear introduce fundamentally different lifespan considerations.

Machinery and Technology: Navigating Rapid Innovation Cycles and Maintenance Strategies to Maximize Asset Longevity

This subsection addresses the intricate challenge of balancing swiftly evolving technology lifecycles with physical asset wear and tear. It emphasizes how rapidly compressing innovation cycles in machinery and technology sectors necessitate agile depreciation strategies and informed maintenance practices. These dynamics are critical for businesses to accurately value assets, plan capital expenditures, and optimize operational efficiency amidst technological obsolescence and physical degradation.

Quantifying the Compression of Semiconductor and Technology Lifecycles in Asset Valuation

Semiconductor lifecycles have dramatically shortened in recent decades, reflecting intensified innovation pressures and competitive dynamics. Historical data indicates that where semiconductor components once enjoyed lifespans approaching three decades in the 1970s, contemporary averages have contracted to approximately ten years or less. This lifecycle shrinkage directly impacts depreciation schedules, necessitating accelerated recognition of asset value consumption aligned with technological obsolescence rather than mere physical wear.

Analytical models integrating thermal profiles, power cycling stressors, and mission-specific usage have improved precision in estimating semiconductor failure points and effective lifespans. For example, stress testing through Rainflow counting algorithms combined with thermal dissipation modeling enables more accurate predictions of time-to-failure. Incorporating such physical and operational wear insights alongside market innovation velocity ensures depreciation reflects both economic and technical realities.

Mid-Life Modular Upgrades as Strategic Deferrals of Full Asset Replacement

In sectors where technology evolves rapidly, modular design in machinery and equipment has emerged as a pivotal strategy to extend useful life. Modular architectures facilitate incremental component upgrades—such as swapping out processing units, sensors, or power modules—allowing firms to adapt to evolving technological standards without incurring full asset replacement costs.

Case studies reveal that high-value equipment in manufacturing and energy sectors can defer replacement by 20-30% of their expected service life when mid-life upgrades are optimally planned and executed. Such upgrade strategies also improve depreciation expense matching with economic benefits, enhancing cash flow management and capital budgeting accuracy. However, deploying modular upgrades requires robust lifecycle management frameworks to assess upgrade ROI relative to residual asset value and obsolescence risk.

Predictive Maintenance’s Role in Extending Effective Machinery and Technology Service Life

Predictive maintenance driven by IoT sensor data, real-time analytics, and machine learning has shifted asset management from reactive to proactive paradigms. This approach significantly mitigates unexpected failures, reduces downtime, and prolongs asset service life by enabling maintenance interventions precisely when needed rather than on fixed schedules.

Empirical analyses show predictive maintenance can extend machinery lifespan by 20-40%, depending on the asset type and operational environment. By closely monitoring degradation patterns and usage metrics, companies dynamically adjust depreciation estimates and capital replacement timelines. Integration of predictive maintenance within ERP and financial systems enhances forecast accuracy for both operational budgeting and long-term capital expenditure planning.

Furthermore, predictive maintenance reduces total cost of ownership through fewer catastrophic failures, optimized spare parts inventories, and better allocation of maintenance labor, resulting in improved asset reliability and sustained production capacity amidst rapid innovation cycles.

Recognizing the interplay of compressed innovation lifecycles, modular upgrade possibilities, and predictive maintenance enables more nuanced depreciation models that reflect true asset value consumption. This detailed understanding prepares the ground for applying strict useful life benchmarks and impairment considerations tailored to specific asset classes.

4. Impairment Dynamics: Beyond Planned Decline to Unexpected Value Erosion

Decoding Rapid Asset Value Erosion: Empirical Patterns of Triggered Impairments and Shock-Induced Write-Downs

This subsection pinpoints the critical external events that compel firms to recognize immediate impairments on their assets, spotlighting the frequency, magnitude, and underlying drivers of such write-downs. By quantifying how shocks—both macroeconomic and industry-specific—precipitate sudden asset value adjustments, it bridges theoretical impairment concepts with real-world occurrences, guiding stakeholders in anticipating and managing unplanned depreciation events.

The Rising Frequency of Impairments Triggered by External Shocks from 2010 to 2024

Empirical analysis over the 2010-2024 period reveals an increasing trend in the recognition of impairment losses triggered by both systematic economic shocks and industry-specific disturbances. The adoption of standardized impairment accounting practices post-major regulatory reforms has led to more frequent reporting of asset write-downs as firms respond to deteriorating recoverable amounts prompted by shifts in underlying asset cash flows and market conditions. Data shows that impairments related to ongoing asset use average over 10% reductions relative to pre-distress asset carrying amounts during financial downturn episodes, underscoring the material impact of persistent negative economic signals on balance sheets.

This pattern reflects growing sensitivity to external risks, further amplified by globalization and tighter integration of supply chains. Firms increasingly encounter asset valuations challenged by rapid changes in demand, technological displacement, or obsolescence, resulting in more immediate and sharper adjustments to book values. The transitional cost of recognizing these impairments, while adverse in the short term, aligns accounting records with economic realities and improves transparency for investors and creditors.

Quantifying Supply Chain Disruptions as a Catalyst for Asset Value Deterioration

Supply chain disruptions have emerged as a pivotal external trigger leading to asset impairments, especially within manufacturing and retail sectors where operational continuity directly affects asset productivity and cash flow generation. Modeling studies and real-world observations attribute significant impairment occurrences to interruptions in supply chain flows that constrain production capacity, increase costs, and delay revenue realization, thereby reducing the recoverable amounts of related assets.

Quantitative evidence links spikes in volatility of key supply chain indices to corresponding increases in reported asset value write-downs. The knock-on effects of these shocks encompass liquidity stress and operational retrenchment, heightening the risk of impairment recognition. This underscores the need for robust monitoring frameworks that incorporate supply chain health metrics into impairment testing protocols, enabling earlier identification of at-risk assets and more calibrated provisioning.

Litigation and Legal Developments as Sudden Triggers for Impairment Recognition

Legal contingencies and adversarial outcomes constitute a non-negligible source of abrupt asset impairments, especially in industries with high exposure to construction defects, intellectual property disputes, or regulatory penalties. Statistical analysis of litigation-triggered impairments indicates that asset write-downs associated with legal events can be sudden and substantial, reflecting court rulings or settlement obligations that materially impair asset utility or cash-generating potential.

The economic impact of such disputes extends beyond immediate write-downs to increased uncertainty and costs of capital. Growing frequency and magnitude of these events necessitate a proactive risk assessment culture that includes early legal case evaluation and integrates economic loss estimation into impairment assessments. This also requires enhanced disclosure practices to maintain stakeholder confidence amidst volatile impairment landscapes rendered by litigation.

Having dissected the principal external triggers mandating immediate impairment recognition, the discussion now progresses to exploring the mechanisms and rules governing potential recovery of these asset values, emphasizing regulatory constraints and practical recovery pathways.

Navigating Impairment Reversals and Clawback Provisions: Auditor Skepticism and Contingent Event Thresholds Demystified

This subsection advances the discussion on impairment dynamics by focusing on the nuanced rules and real-world practices surrounding impairment reversals. It highlights the stringent conditions under which impairments can be clawed back, clarifies testing thresholds tied to contingent events, and incorporates auditor perspectives that influence the robustness and conservatism of impairment recognitions and reversals. Together, this deepens understanding of how impairment adjustments operate as both accounting judgments and strategic safeguards that ensure financial statement reliability.

Clawback Provisions in Impairment Accounting: Scope and Quantitative Illustrations

Clawback provisions restrict the reversal of previously recognized impairment losses to specific circumstances, primarily when there is clear evidence of changes in estimates affecting the asset's recoverable amount. Crucially, reversals are disallowed for goodwill impairments, reflecting the permanent nature of goodwill write-downs. For other tangible and intangible assets, reversal is capped so that the carrying amount post-reversal cannot exceed the depreciated historical cost that would have been recorded had impairment not been recognized. This ceiling safeguards against artificially inflating asset values beyond plausible economic utility.

Quantitatively, consider an asset initially carrying a value of 10 million with accumulated depreciation of 4 million before impairment. If an impairment of 3 million occurs, the carrying amount reduces to 3 million. Should subsequent recoverable amounts improve, the impairment reversal is limited to restoring value up to 6 million (10 million less 4 million depreciation), preventing a carry amount exceeding the notional undepreciated balance. This mechanism ensures that impairment reversals reflect genuine recovery rather than opportunistic value adjustments.

Contingent-Event Testing Thresholds: Defining Guardrails Against Premature Impairment Reversals

Impairment reversal testing requires rigorous reassessment triggered by reliable indicators signifying improved asset performance or market conditions. These contingent-event thresholds are often delineated by changes in key assumptions such as discount rates, projected cash flows, or market valuations. A reversal is only justified if such changes materially affect the estimated recoverable amount since the prior impairment.

For instance, a company monitoring the value-in-use of an asset must track operational metrics and external factors continuously. Reversal is precluded if any improvement remains speculative or transient. Accounting frameworks commonly mandate that any reversal does not cause the asset to exceed the carrying value net of depreciation had impairment never been recorded, effectively placing a 'depreciated cost ceiling' on the reversal extent. This disciplined approach prevents cyclical earnings volatility arising from frequent impairment adjustments.

Auditor Perspectives on Cyclical Recovery Reliability: Balancing Prudence and Reflective Reporting

Auditors often approach impairment reversals with deep skepticism, particularly in industries subject to economic cyclicality. This caution arises from the risk that transient recoveries may be mistaken for sustainable value improvements, leading to premature or inappropriate reversal of impairment losses. Auditor skepticism acts as a critical control, ensuring that only substantive and supportable evidence justifies reversal, thus sustaining financial statement integrity.

Empirical observations show auditors scrutinize disclosure quality around impairment testing assumptions, emphasizing transparent documentation of trigger events and assessment methodologies. In sectors like manufacturing or retail, where external disruptions or demand variations cyclically impact asset values, auditors demand conservative assumptions and frequent reassessment. This vigilance underscores the importance of robust governance in impairment accounting, reinforcing that impairment and its reversal are not only technical adjustments but strategic levers influencing investor confidence and corporate valuation.

Having unpacked the constraints and prudential measures governing impairment reversals, the analysis now prepares to examine the broader implications these reversals and write-downs have on financial statements and strategic decision-making, highlighting their pivotal role in creating transparent and decision-useful financial reporting.

5. Financial Statement Integration: Turning Depreciation Into Strategic Intelligence

Income Statement Mechanics and Strategic Tax Positioning Through Depreciation Accuracy

This subsection delves into the critical interface where asset depreciation calculations directly influence income statement outcomes and tax positioning. By quantifying marginal tax benefits, analyzing deferred tax timing implications, and exploring concrete examples of book-to-tax reconciliation challenges, we unpack how nuanced depreciation management can unlock tax optimization while preserving financial statement integrity.

Quantifying Marginal Tax Benefits by Asset Class: Unlocking Depreciation’s Fiscal Impact

Depreciation is a pivotal lever for tax optimization because it converts capital outlay into deductible expenses, reducing taxable income. However, the true marginal tax benefit varies significantly by asset class due to differing useful lives, residual values, and depreciation methods permitted under tax codes. For instance, machinery and equipment categorized under shorter useful lives can deliver front-loaded tax deductions, particularly when accelerated depreciation methods are available, enhancing present-value tax shield benefits. Conversely, buildings and infrastructure assets, typically subject to longer depreciation schedules and stricter methods like straight-line, yield more extended but lower annual deductions, diminishing short-term tax relief but smoothing income for reporting.

Empirical data show that marginal tax benefits from accelerated depreciation methods for high-turnover asset classes can exceed standard rates by up to 20-30% in early years of asset life, directly enhancing cash flow. Firms employing these methods strategically can improve liquidity and investment capacity. Nonetheless, the availability and scale of these benefits depend heavily on jurisdictional tax laws and compliance parameters influencing allowable depreciation rates and methods.

Deferred Tax Accounting: Timing Differences Arising from Methodological Choices

The divergence between book depreciation and tax depreciation methods introduces timing differences that generate deferred tax assets or liabilities. When accelerated depreciation is applied for tax purposes while straight-line methods govern book accounting, companies recognize initially lower taxable income but higher reported pre-tax income. This leads to deferred tax liabilities, reflecting taxes postponed to future periods when depreciation deductions reverse.

The timing of these reversals critically impacts financial planning and tax liability forecasting. For example, if accelerated tax depreciation leads to substantial early deductions, deferred tax liabilities increase, necessitating prudent management of future tax outflows. Conversely, firms with underutilized deferred tax assets, such as those carrying losses forward or facing limitations in utilizing these deductions, must carefully assess recoverability to avoid impairment risk. Understanding and correctly modeling these deferred tax positions require integrating tax schedules with financial reporting frameworks, ensuring alignment with relevant standards and disclosure requirements.

Common Book-to-Tax Reconciliation Pitfalls and Case Study Insights

Reconciliation mismatches between book and tax depreciation remain a widespread challenge, often stemming from inconsistent capitalization policies, diverging useful life assumptions, and differing depreciation methods applied for financial reporting versus tax purposes. Such discrepancies can lead to misstated income, understated tax liabilities, or unexpected deferred tax volatility, eroding investor confidence and complicating audit processes.

Case studies reveal that operational issues such as late asset additions, componentization errors, or failure to adjust residual values trigger reconciliation gaps. For instance, firms that adopt a composite depreciation method for financial reporting but are mandated to depreciate assets individually for tax incur complexities that require detailed tracking and reclassification. Successful correction approaches focus on implementing integrated ERP systems that synchronize asset registers with tax modules and maintaining rigorous periodic review protocols to ensure compliance and transparency. Additionally, proactive communication between accounting and tax departments is essential to preempt and resolve reconciliation discrepancies.

Having established how depreciation affects income statement dynamics and tax positions, notably through method choices and timing differences, the report will now extend into capital expenditure optimization. This will link depreciation cadence to asset replacement strategies and resource allocation frameworks necessary for sustaining long-term operational and financial health.

Capital Expenditure Optimization Through Forward-Looking Projections: Inflation, Delays, and Technological Disruption Risks

This subsection addresses how businesses can strategically leverage depreciation and replacement cycle insights, adjusted for inflation and technology evolution, to optimize capital expenditure decisions. It connects the technical mechanics of asset lifecycle forecasting with economic realities such as inflation impact on asset values, financial penalties arising from capitalization delays, and accelerated obsolescence due to technological innovation. The goal is to empower decision-makers with actionable models and sensitivity analyses that enable precise resource allocation and informed timing for asset renewal, thereby safeguarding asset value and operational efficiency.

Incorporating Inflation into Asset Replacement Cycle Forecasts

Accurately forecasting asset replacement cycles requires integrating realistic inflation assumptions, typically ranging between 3% and 5% annually. Inflation impacts both the future capital outlays for asset renewal and the residual values of existing assets, altering depreciation rates and replacement timing expectations. By applying inflation-adjusted replacement matrices, organizations can refine budgeting projections to reflect anticipated cost escalations, ensuring that capital reserves align with future acquisition needs.

Empirical data suggest that delaying asset replacement without considering inflation effects can erode purchasing power, leading to underfunded capital expenditure plans and increased risk of operational disruptions. Models that incorporate inflation-driven escalation of replacement costs provide quantitative foundations to justify early renewals or phased upgrades, ultimately optimizing total cost of ownership. Such forward-looking frameworks also facilitate scenario-based planning across economic cycles, enabling agile capital deployment that mitigates exposure to inflation volatility.

Quantifying Financial Penalties from Capitalization Delays Over Six Months

Delays in capitalizing assets beyond six months can trigger significant financial penalties, including lost depreciation deductions and potential regulatory sanctions, which cumulatively distort financial statements and tax liabilities. These penalties not only increase immediate cash outflows but can also create misalignments between expense recognition and asset utilization, undermining profit transparency and distorting performance metrics.

Businesses should quantify the cost impact of such delays by modeling the incremental expense recognition and associated cash tax implications attributable to late capitalization. Sensitivity tables that examine various delay durations and corresponding penalties enable CFOs and controllers to identify thresholds beyond which the financial consequences outweigh benefits from postponing capitalization. This quantitative insight promotes disciplined capitalization practices and enhances compliance rigor while supporting timely asset activation within accounting systems.

Modeling Technology Obsolescence Scenarios Over Medium to Long-Term Horizons

Technological acceleration is profoundly reshaping asset useful lives, especially in sectors heavily reliant on specialized hardware and software. Forecasting depreciation and replacement timing must adapt by incorporating probabilistic obsolescence models that account for disruptive innovation cycles spanning five to ten years. These models recognize that rapid technology shifts can result in premature asset retirement, impairments, or stranded infrastructure costs.

Case studies from hyperscale AI infrastructure investments illustrate how specialized components with originally projected depreciation horizons of 5-6 years may require revaluation to as short as 3 years due to fast-changing processor architectures and software demands. By integrating machine learning-driven forecasts of residual value trajectories and innovation diffusion rates, enterprises can stress-test capital expenditure plans against scenarios of accelerated obsolescence. This approach enhances strategic agility, allowing organizations to anticipate write-down risks, align capital deployment with technological inflection points, and negotiate supplier contracts that accommodate mid-life upgrades or modular replacements.

Having established models that quantify inflation effects, penalties from delayed capitalization, and technology-driven asset turnover risks, the next subsection will explore how these forward-looking projections translate into enhanced financial reporting and tax optimization strategies, thereby converting asset depreciation schedules into robust strategic intelligence.

6. Visualization and Communication: Making Depreciation Insights Actionable

Interactive Dashboards for Stakeholder Alignment: Enhancing Depreciation Insights Through Time-Aware Visualization

This subsection elucidates how advanced interactive dashboards transform raw depreciation data, integrated with precise time measurements, into actionable insights for diverse stakeholders. It situates the role of visualization as an essential bridge between complex time-unit conversions in depreciation accounting and practical financial strategy, improving transparency, accuracy, and operational responsiveness.

Concrete Examples of Time-Integrated Depreciation Dashboards Driving Decision-Making

Effective depreciation dashboards blend temporal granularity—ranging from hours to years—with asset valuation metrics to deliver dynamic performance views. For example, several leading enterprises implement dashboards presenting depreciation expense curves aligned with fiscal periods, enabling clear identification of cost allocation over asset lifecycles. These visualizations often contrast baseline straight-line depreciation schedules against real-time usage or units-of-production data, providing stakeholders with contextual asset consumption patterns.

In practical deployment, time conversion precision enables accurate pro-rata period adjustments—such as partial months or leap-year considerations—ensuring fiscal data integrity. Dashboards that incorporate this nuance minimize reconciliation errors between accounting records and operational realities, reducing audit risks and promoting more confident capital planning. Furthermore, interactive timelines assist in spotting anomalies like accelerated wear or early impairment triggers by linking depreciation analytics to asset conditions and maintenance logs.

Technical Integration: Synchronizing Time-Based Asset Data Streams Across ERP and Visualization Platforms

Integral to achieving these capabilities is seamless data integration spanning asset registers, time-logging systems, and financial ledgers. Modern ERP suites provide built-in APIs for handling heterogeneous time formats and accommodating irregular asset lifecycles, which feed depreciation modules with consistent, validated inputs. Visualization layers leverage this harmonized data to create multi-dimensional dashboards capable of drilling down from portfolio-level aggregates to individual asset details with time filters.

Key integration challenges focus on managing partial depreciation periods, handling multi-jurisdictional tax regimes with differing fiscal calendars, and accounting for intra-period asset additions or disposals. Robust dashboards resolve these by embedding configurable business rules that automate conversions from high-frequency timestamps (e.g., hourly usage or sensor readings) to standardized reporting intervals. Such tight coupling guarantees depreciation figures remain synchronized with operational realities, enabling predictive maintenance and proactive replacement decisions.

Measuring and Enhancing User Engagement to Maximize Dashboard Impact on Depreciation Management

Quantitative usability and adoption metrics are pivotal to assessing how effectively depreciation dashboards inform decision-makers. Key indicators include login frequency, average session duration, number of drill-downs performed, and range of time-based filters applied. High engagement levels often correlate with improved understanding of asset depletion risks and enhanced capital budgeting precision.

Organizations employing user-centric design methodologies report that dashboards with clear visual cues—such as color-coded depreciation bands tied to asset age and forecasted impairment events—achieve higher satisfaction scores. Supplementing dashboards with role-specific views tailored to CFOs, asset managers, and tax specialists also fosters cross-functional alignment. Continuous feedback mechanisms allow iterative refinement of both temporal granularity and presentation logic, optimizing relevance and ease of navigation.

Ultimately, driving user adoption is inseparable from demonstrating tangible business outcomes: reducing over- or under-depreciation, improving tax compliance, and enabling just-in-time capital expenditures supported by transparent, time-aware asset analytics.

Having established how interactive, time-integrated dashboards empower stakeholders through clear visualization and engagement, the report next explores forward-looking strategies that leverage emerging technologies and adaptive governance to future-proof depreciation and asset management frameworks.

7. Future-Proofing Your Framework: Emerging Trends and Adaptive Governance

Navigating Regulatory Shifts and Compliance Complexities for Depreciation Across Global Jurisdictions

This subsection delineates the evolving regulatory landscape affecting asset depreciation practices worldwide. It contextualizes recent multilateral initiatives and region-specific tax frameworks that shape depreciation deductibility, especially highlighting sustainability-linked fiscal policies and the emerging treatment of digital assets. Understanding these dynamics is crucial for corporations aiming to maintain compliance while optimizing tax positions in a fragmented international environment.

OECD Initiatives Transforming Depreciation Policies and Tax Deductibility Norms

The Organization for Economic Cooperation and Development continues to influence depreciation regulations through its Base Erosion and Profit Shifting (BEPS) projects and Pillar Two global minimum tax framework. As of 2023, accelerated depreciation remains available in the majority of OECD jurisdictions, but implementation nuances exhibit significant variability. Mechanisms such as shortened depreciation periods, first-year expensing, and use of declining-balance methods are deployed to align deductible expense recognition with economic depreciation, yet their design can create temporary disparities between financial accounting and taxable income.

For multinational enterprises, these OECD-led rules necessitate rigorous tracking of tax base adjustments to reconcile book and tax depreciation, ensuring compliance without compromising strategic capital allocation. Importantly, accelerated depreciation incentives embedded in local tax codes act as tools to stimulate investment but demand vigilance to navigate their interplay with minimum tax provisions and cross-border tax harmonization efforts.

Impacts of EU Sustainability-Linked Loan Criteria on Depreciation Accounting

European Union initiatives increasingly tie depreciation frameworks to sustainability goals through green financing regulations. Since 2023, eligibility for sustainability-linked loans in the EU often depends on stringent assessment of assets’ environmental credentials, which includes accelerated depreciation allowances for green capital investments. This creates a dual imperative: not only must depreciation comply with conventional accounting standards, but also align with technical screening criteria of the EU Taxonomy to qualify for such financing.

This dual-layer regulatory pressure means that asset classification and valuation processes must incorporate environmental performance indicators directly into depreciation schedules. Moreover, the integration of green tax incentives with depreciation accounting amplifies the potential tax benefits but imposes additional compliance requirements, such as detailed disclosure and certification of asset sustainability attributes. Firms operating within EU jurisdictions must therefore restructure their capital budgeting and asset management protocols to achieve both financial and environmental optimization.

Evolving Depreciation Treatments and Holding Periods for Digital Assets in Modern Tax Regimes

The digitization of business assets has ushered in complex challenges for depreciation policies, especially regarding cryptocurrencies and other intangible digital holdings. Unlike traditional tangible assets, digital assets such as Bitcoin are frequently classified as indefinite-lived intangible assets, precluding systematic depreciation but necessitating impairment testing when value declines materially. The fluidity of digital asset valuation and market volatility complicates the recognition of recoverable amounts, requiring companies to apply significant judgment in their impairment assessments.

Moreover, varying international stances on digital asset holding periods affect taxation and potential amortization strategies. Some jurisdictions differentiate tax benefits based on duration of ownership, with longer holding periods enabling favorable capital gains treatment but leaving depreciation largely inapplicable. The lack of harmonized rules means companies must customize accounting and tax treatment of digital assets per jurisdiction-specific guidance, balancing competitive tax planning against regulatory scrutiny. This space remains highly dynamic, with ongoing debates over classification and depreciation treatment likely to spur new accounting standards in the near term.

Having established the intricate and shifting regulatory matrix impacting asset depreciation across global markets, the report next examines how technological innovations and data-driven methodologies enhance dynamic schedule adjustments—essential for maintaining adaptive governance amid rapid asset obsolescence and emergent compliance demands.

Harnessing IoT and Machine Learning to Revolutionize Asset Depreciation Schedules

This subsection explores the transformative impact of Internet of Things (IoT) data and machine learning (ML) algorithms on the precision and agility of asset depreciation practices. Positioned within the broader theme of future-proofing depreciation frameworks, it delves into how real-time utilization insights and predictive analytics enable dynamic adjustments to depreciation schedules, thereby enhancing valuation accuracy and strategic asset management. It also evaluates the evolving governance landscape poised to oversee these adaptive processes, ensuring regulatory compliance and internal controls keep pace with technological advancements.

The Quantifiable Impact of IoT-Enabled Real-Time Asset Utilization on Depreciation Accuracy

The integration of IoT technologies into asset management systems has introduced unprecedented levels of visibility into real-time asset performance and utilization. Sensors embedded in machinery, vehicles, and infrastructure continuously stream data capturing operating hours, load factors, environmental conditions, and maintenance events. This granular data underpins a shift away from reliance on static, estimated useful lives towards condition-based depreciation models that reflect actual wear and usage patterns. Empirical studies and industry reports indicate that leveraging IoT input reduces depreciation variance by improving the precision of asset aging calculations, enabling more accurate forecast of residual values and maintenance needs. This shift aligns depreciation expense recognition more closely with economic realities, mitigating risks of under- or over-depreciation that can distort financial statements and cash flow forecasts.

Machine Learning Models Forecasting Residual Values: Enhancing Depreciation Scheduling Precision

Machine learning models employ vast historical and real-time datasets to identify complex, non-linear correlations impacting asset value trajectories. Predictive algorithms such as regression trees, gradient boosting, and neural networks analyze factors including usage intensity, maintenance history, evolving technological obsolescence, and market dynamics to generate refined forecasts of residual asset values. Case studies demonstrate that organizations deploying ML-driven asset valuation have achieved marked improvements in the timing and magnitude of depreciation charges, particularly within sectors experiencing rapid innovation cycles or volatile secondary markets. These adaptive schedules reduce impairment risk by flagging early signs of accelerated value erosion and informing proactive capital replacement decisions. Additionally, ML algorithms enable scenario testing under diverse operating conditions, empowering management to optimize capital expenditure planning and depreciation policies in alignment with strategic cash flow objectives.

Governance Practices for Managing Mid-Cycle Depreciation Policy Adjustments

The advent of dynamic depreciation methodologies informed by IoT and ML necessitates robust governance frameworks capable of overseeing mid-cycle policy shifts without compromising financial statement reliability. Successful governance models incorporate cross-functional committees combining expertise in finance, asset management, data science, and compliance to evaluate the rationale and data integrity behind schedule revisions. Established protocols demand comprehensive documentation, validation of predictive models, and scenario impact analyses prior to implementation. Auditors increasingly focus on controls surrounding data quality, algorithm transparency, and the appropriateness of assumptions used in model training. Emerging best practices also exhort the adoption of automated audit trails and periodic stress testing of depreciation assumptions to preempt risks of aggressive earnings management or regulatory censure. Companies adopting such governance arrangements report enhanced stakeholder confidence and smoother regulatory engagements, underscoring the criticality of aligning adaptive depreciation with corporate risk management.

Building on the technological and governance enablers of dynamic depreciation, the next section will explore how these innovations integrate with financial reporting frameworks to convert enhanced accuracy into strategic capital management and optimized tax positioning.

Conclusion

The comprehensive investigation presented herein confirms that precision in time measurement and conversion is not merely a technical accounting consideration but a strategic imperative that directly influences financial accuracy, risk management, and resource allocation. Misalignments in recording asset consumption periods can cascade into significant cost overruns, impairment risks, and tax inefficiencies, as empirical evidence reveals through documented cost inflations and error reduction statistics tied to automation.

Advancements in ERP automation, complemented by emerging IoT and machine learning technologies, have ushered in an era where dynamic, condition-based depreciation schedules can replace static assumptions, thereby better reflecting the true economic life and residual values of diverse asset classes. Such innovation enhances audit readiness, regulatory compliance, and predictive insights that empower proactive capital expenditure and maintenance decisions.

Nevertheless, navigating jurisdictional heterogeneity—from de minimis thresholds and tax depreciation rules to green financing criteria and digital asset accounting—requires robust governance frameworks that accommodate mid-cycle policy adjustments without compromising financial reporting integrity. Cross-functional collaboration and transparent communication facilitated by interactive, time-sensitive dashboards emerge as vital enablers of this governance.

Looking ahead, organizations that integrate precise time-based measurement into their depreciation frameworks position themselves to better absorb shocks from technological obsolescence, economic volatility, and regulatory transformation. By embedding these principles and tools into corporate financial strategies, enterprises can unlock not only enhanced transparency and compliance but also sustained competitive advantage and investor confidence.

References

- Verified Metrics

- Beyond the horizon - KPMG agentic corporate services

- PDF Taxation in Japan

- Government Savings Bank

- Beyond Mobility

- EDGAR PDF

- Maximizing Business Deductions: An Introduction to Depreciation, Amortization, and Expensing

- PDF 2024 Annual Report - minedocs.com

- Depreciable Property: Understanding Its Legal Definition | US Legal Forms

- 00E230880470Security_Cover_...

- PDF State Taxation of Data Centers - Tax Foundation

- MASAN GROUP Annual Report 2022

- The Role of Financial Capital in Production - ROIW.org

- PDF Annual Report 2022

- PDF Iaao Glossary for Property

- INDUSTRIAL AND COMMERCIAL BANK OF CHINA LIMITED

- CS Wind Offshore - Annual Report 2023

- PDF CS WIND Offshore A/S

- 2017ar.pdf

- Survival of the fittest? Financial and economic distress and ...

- YUANTA FUTURES CO., LTD. AND SUBSIDIARIES

- The Export-Import Bank of Korea CNY ...

- What is an Intangible Asset Impairment? — Vintti

- PDF Impairment of Assets

- Corporate information

- coversheet pw - 2 7 7

- Essays on Overlapping Generations Models and Social ...

- PDF SME BUSINESS TRAINING AND COACHING LOOP Trainee Manual

- KOREAN TAXATION

- PDF 10-K - 02/22/2023 - Exxon Mobil Corporation

- PDF Zoning and the Dynamics of Urban Redevelopment

- Exploring the relationship between built environment and multidimensional street market vitality: Insights from urban villages in Shenzhen using multi-source data

- Does the Livability of a Residential Street Depend on the ...

- BetterBench: Assessing AI Benchmarks, Uncovering Issues, and Establishing Best Practices

- FINAL MUNICIPAL SERVICE REVIEW VOLUME III— ...

- PDF Earthquake Resilience: Benefit-Cost Analysis for Building Design and Retrofit

- Commercial vs. Residential Real Estate Transactions — Balisok & Kaufman PLLC

- Commercial vs. Residential Real Estate Cycles | Key Market Differences

- The Aero-Habitat in Algiers City

- The Power Behind Commercial Buildings: Understanding Commercial Electrical Construction - Drone

- CApItAl Flows to EMErgIng MArkEts: thE rolE oF globAl ...

- PDF Supply Chain Uncertainty and Diversification - Thomas Bourany

- Europe and the world economy

- THE FACTORS INFLUENCING STOCK MARKET ...

- PDF Supply Chain Uncertainty, Energy Prices, and Inflation

- PDF Rate Cycles - World Bank

- High-Frequency Identification of Monetary Policy Surprises in ...

- PDF Bank of England Quarterly Bulletin 2014 Q1

- MONETARY MANAGEMENT AND FINANCIAL ...

- Scarce, Abundant, or Ample? A Time-Varying Model of the ...

- PDF The Distributional Impact of the Minimum Wage - Department of Economics

- Battery Investment, Renewable Energy, and Market ...

- Regulatory Approaches to Revenue Setting for Electricity ...

- Depreciation: In-Depth Explanation with Examples | AccountingCoach

- Equipment depreciation: Types and how to calculate it

- Depreciation

- Profit model

- Numerical Algorithms for Precise and Efficient Orbit ...

- PDF Design Errors in Building Construction Projects - IRJET

- PDF Factors of Design Errors in Construction Project (A Review)

- MANUAL CHANGE TRANSMITTAL NO. 24-2 - Caltrans

- PDF Trends in growth and value: Cycles and market regimes

- PDF Guidelines for Regulatory Impact Analysis: a Primer - Aspe

- PDF The Ability of Investors to Time Purchases and Sales of Mutual Funds

- DEV DEC VELOP CISION FA PMEN N MET ACILIT NT OF ...

- PDF 0001810806-24-000053

- Quarterly Report to Clients

- PDF Pillar Two and tax incentives

- The Impact of R&D Tax Incentives on R&D Costs and ...

- PDF The Economic, Revenue, and Distributional Effects of Permanent 100 Percent Bonus ...

- America's Great Depression

- Rent appropriation in global value chains

- The past, present, and future of intangible assets

- CAPITAL FORMATION AND FOREIGN DIRECT ...

- Evidence from the Global Automobile Industry

- PDF Corporate Taxes, Investment Frictions and Macroeconomic Dynamics

- UN vs OECD Model Tax Conventions

- PDF Comparative analysis of European and Ukrainian legislation in the field ...

- The digital economy, GVCs and SMEs

- The ministry of finance 'challenge function'

- THE STATE OF GLOBAL CROSS-BORDER E- ...

- E-Commerce Regulatory Evolution: Adapting to Global Trade Shifts with ONE | ONE United States

- E-Commerce Regulatory Evolution: Adapting to Global Trade Shifts with ONE | ONE Korea

- Facilitating Trade and Logistics for E- Commerce

- Market stability measures - EU Climate Action

- E-Commerce Regulatory Evolution: Adapting to Global Trade Shifts with ONE | ONE

- Patent Boxes Design, Patents Location and Local R&D

- PDF 0.2cm Place-Based Redistribution0

- PDF EFFICIENT REDISTRIBUTION NATIONAL BUREAU OF ECONOMIC RESEARCH , Revised March 2021

- PDF E cient Redistribution - Virgiliu Midrigan

- PDF Wealth Inequality in Korea: Limited Participation

- Taxation Basics for Gift Planners

- PDF Steve and Andrea Sample - Bollin Wealth Management

- Municipal bonds in the housing market

- Additional Petroleum Production Tax Incentives Are of ...

- PDF Tax planning and investment responses to dividend taxation

- Seismic design of non structural elements: Understanding the fundamental period.

- Chapter 11 - SEISMIC DESIGN CRITERIA

- ANALYSIS AND DESIGN OF TRANSFER STRUCTURES ...

- Risk Management in Mechanized Tunnelling

- the construction of timber houses in chile - Documents & Reports

- Indonesia Sustainable Least-cost Electrification-1 (ISLE-1 ...

- Report on efficient uncertainty quantification and ...

- PDF Reference Book on Building By-laws and Building Permit System

- Structural Stability Provisions in IBC and ASCE 7

- PDF Stability Analysis of Concrete Structures

- PDF Impact of Supply Chain Disruptions on Financial Leverage

- PDF Supply Chain Disruptions, Supplier Capital, and Financial Constraints

- PDF Good Practice Guide for Improving Resilience

- PDF Quantifying Supply Chain Disruption: A Recovery Time Equivalent Value ...

- Rise of Intangible Assets, Causal AI, and Cybersecurity | International Insurance Society

- An Empirical Analysis of the Effect of Supply Chain ...

- PDF Econometric analysis of supply chain disruptions: financial performance ...

- Q1 2026 Closing statements: Insights for controllers at quarter end

- The causal effects and policy implications of global supply chain disruptions

- PDF Supply Chain Disruptions, the Structure of Production Networks, and the ...

- Interest Rate Risk Management for Portfolio Managers

- Engine Maintenance: Asset Integration Guide

- Data Visualization for Investment Insights

- Real Estate Valuation Analysis for Hedge Funds

- Investment Analysis in Semiconductor Manufacturing

- Investment Analysis for Real Estate Asset Managers

- PDF The Impact of Rebalancing Strategies on ETF Portfolio Performance

- Portfolio Risk Assessment for Investment Management: A Risk Manager's Guide

- BI tool operating models

- PDF World Bank Document

- Financial Guide for SMEs

- Sound Practices for Managing Liquidity in Banking ...

- PDF Illicit Financial Flows in Mozambique'S Extractive Industry

- PDF Recent advances in the literature on capital flow management

- PDF Evaluating Corporate Currency Risk Management Practices: A Case Study ...

- VOSTF Summer NM Package

- PDF World Bank Document

- PDF The US dollar and capital flows to EMEs - Bank for International ...

- PDF Intraday liquidity around the world - Bank for International Settlements

- INTERNATIONAL JOURNAL OF CENTRAL BANKING

- Climate Action Statement 2024 Annex

- Base Offering Circular

- PDF Greenwashing Monitoring and Supervision

- PDF Presentation for investors Sto SE & Co. KGaA

- PDF The Climate Technology Progress Report 2025

- SUSTAINABLE DEBT GLOBAL STATE OF THE MARKET ...

- 2024 integrated report

- 03 GROUP FINANCIAL STATEMENTS

- Worldwide Capital and Fixed Assets Guide

- Monitoring Capital Flows to Sustainable Investments

- FoodShare Wisconsin Handbook

- Annual report 2024

- PDF Accounting Standards Codification 350 Intangibles- Goodwill

- PDF Fair value measurement handbook - kpmg.com

- PDF Accounting changes and error corrections - EY

- ANNUAL FINANCIAL REPORT

- Handbook: Impairment of nonfinancial assets

- CONSOLIDATED FINANCIAL STATEMENTS AND NOTES ...

- US GAAP versus IFRS: The basics

- Accounting Principles: In-Depth Explanation with Examples | AccountingCoach

- How does AIC account for General Plant?

- Adopted Rules

- Sec. 168. Accelerated Cost Recovery System

- PDF It'S Our Nature to Protec T™ Annual Re

- PDF Manual, Volume 1 : Principles of Water Rates, Fees, and Charges (5th ...

- Book vs Tax Basis Differences 10-25

- Networking Strengths

- Deferred tax | ACCA Global

- Deferred tax

- PDF Office Fit Out Cost Guide 2025 | Americas

- circularity-for-secure-sustainable-products-materials- ...

- POST-DISASTER REDEVELOPMENT PLANNING

- PDF pfritz_FINAL_THESIS_5.26.23_ATS comments 5.31.23 (1)

- Parametric design workflow for solar, context- adaptive and ...

- Adaptive Reuse | W.E. O'Neil Construction

- Adaptive Reuse of Industrial Buildings Saves 65 Years of Carbon: Why Historic Renovation Outperforms New Green Construction

- Green Building Technology

- Cultural Infrastructure Index

- Adaptive reuse

- Construction Defect Litigation, Housing Affordability, and ...

- Risk factors and management of medical disputes: An analysis of preliminary appraisal reports

- AS 2505: Inquiry of a Client's Lawyer Concerning Litigation, Claims, and Assessments

- Litigation Risk Management Through Corporate Payout Policy

- 2016 Annual Report to Congress — Volume One

- Reference Guide on Estimation of Economic Losses in ...

- Corning (GLW) Q1 2026 jumps with 20% sales growth and strong Q2 outlook

- 10-K - 03/12/2025 - Marvell Technology, Inc.

- PDF 0001321655-24-000071

- UNITED STATES SECURITIES AND EXCHANGE ...

- AI in UX Analytics: The Data You Need for User-Centric Decisions

- PDF OECD Pensions Outlook 2024

- Creating (actually) useful dashboards

- Analyzing Blog Visitor Behavior: Understanding User Engagement

- Navigating Divergent Innovation Pathways: A Comparative Analysis of GT Biopharma’s Clinical-Stage Growth and Roblox Corporation’s Platform Resilience in 2026

- Top 10 Loyalty Program Dashboard Templates with Samples and Examples

- PDF The Adaptive Waste Management Assistant (AWMA) An IO and IoT-Based Intelligent System ...

- PDF Predictive AI Model for Remittance Liquidity Optimization in ...

- PDF Sales Dashboard Development for Business Performance Optimization

- Data Analytics KPI Examples: 7 Essential Metrics for Success - ConsultingEdge.net

- Enterprise Resource Planning (ERP): Definition, Modules and ERP vs CMMS

- ERP/Procurement system integrations for Scope 3

- PDF BCG Executive Perspectives AI and the Future of Software

- PDF CONNECTING YOUR WAREHOUSE TO ERP, - provisionwms.com

- Best ERP WMS Systems 2026: Warehouse Management Modules Ranked

- OrbitSailor | Live Ship Tracking

- The Guide to the 10 Financial Management Software of 2025

- PDF Houlihan Lokey 2024 PropTech Year in Review - cdn.hl.com

- Top 10 ERP AI Use Cases & Case Studies