Navigating the Expanding Horizon: Strategic Positioning in the Global Bone and Joint Health Supplements Market Through 2033

Table of Contents

- Executive Summary

- Introduction

- 1. Diagnosing the Expansive Frontier: Current State and Projected Trajectory of the Global Bone and Joint Health Supplements Market Through 2033

- 2. Decoding the Engine Room: Structural Drivers and Countervailing Pressures Shaping Market Expansion

- 3. Reframing Competition: Player Archetypes and Strategic Posturing Through 2033

- 4. Charting the Sustainable Pathway: Scenario-Based Roadmap to 2033

- 5. Action Blueprint: Prioritized Initiatives for Stakeholder Alignment Through 2033

- Conclusion

Executive Summary

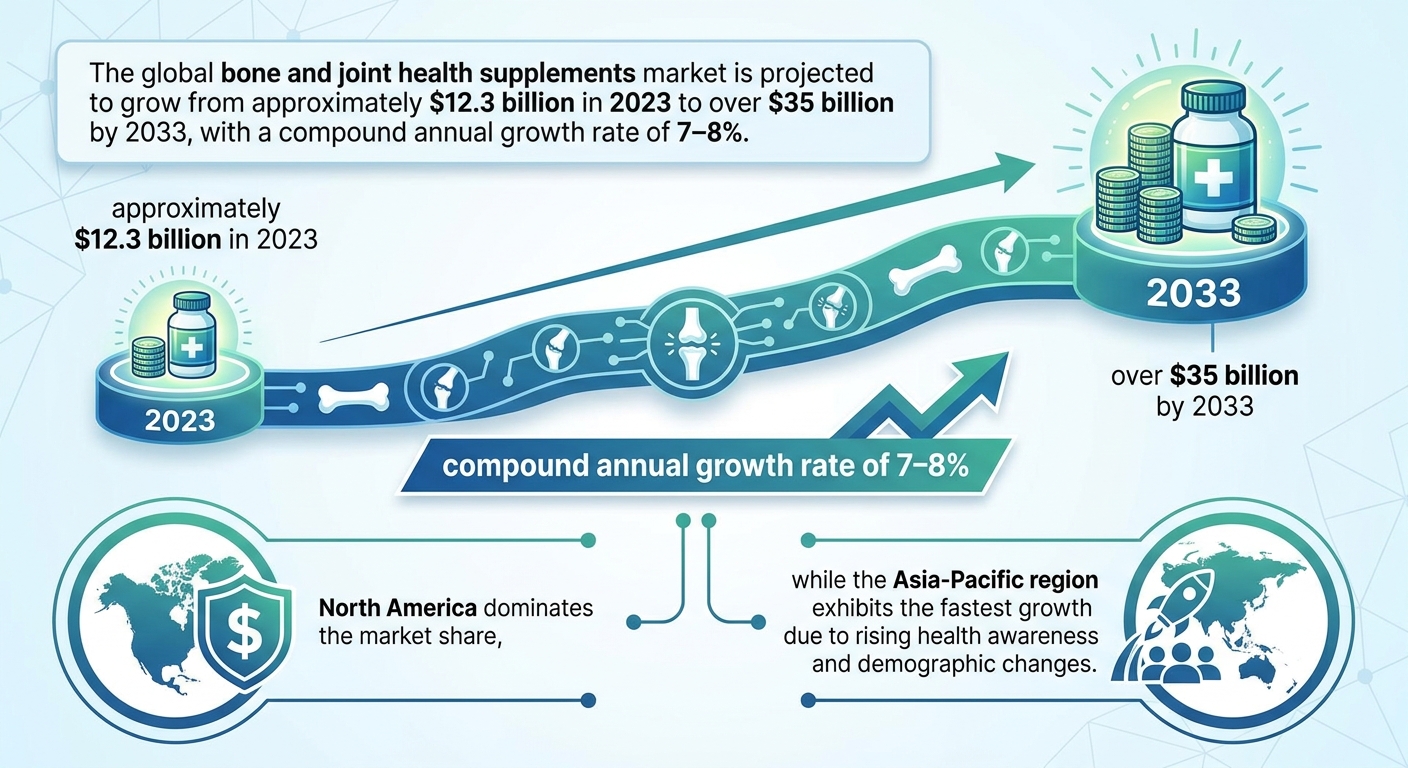

The global bone and joint health supplements market exhibits significant valuation variability in 2023, with estimates ranging from approximately $3.8 billion to $15.01 billion due to differing methodologies and geographic scopes. Consensus forecasts project a steady growth trajectory with compound annual growth rates (CAGRs) between 6% and 7%, potentially expanding the market size to a range of $27 billion to $35 billion by 2033. This growth is underpinned by demographic shifts, notably aging populations and rising osteoporosis and arthritis prevalence, alongside rising health awareness across generational cohorts.

Regionally, North America maintains leadership with around 35% market share, supported by robust healthcare infrastructure and a well-established consumer base, while Asia-Pacific emerges as the fastest-growing region with projected CAGRs exceeding 8%. Product segmentation reveals vitamins and minerals comprising roughly half the market share, with glucosamine-chondroitin experiencing the fastest expansion at over 13% CAGR. Innovation frontiers include collagen peptides, omega-3 fatty acids, adaptogens, and functional food/beverage integration complemented by advancing bioavailability technologies and digital personalization platforms. Regulatory complexity, sustainability imperatives, and competitive dynamics further shape strategic market engagement.

Introduction

The global market for bone and joint health supplements stands at a pivotal juncture as it transitions from heterogeneous valuation estimates towards a more precise understanding of sustainable growth potential through 2033. The sector encapsulates a vast array of products targeting musculoskeletal wellness, addressing conditions such as osteoporosis, arthritis, and joint degeneration that increasingly burden aging and younger populations alike. Against a backdrop of rising chronic disease prevalence and evolving consumer health paradigms, understanding market dynamics is essential for stakeholders ranging from manufacturers and investors to healthcare professionals and policy makers.

Disparate market sizing methodologies continue to reflect fragmentation in data capture, geographic emphasis, and product definition, leading to significant variance in 2023 baseline figures. This report endeavors to reconcile these discrepancies by critically examining growth forecasts, product segmentation trends, and regional market shifts. It draws from comprehensive analyses encompassing demographic drivers, technological advancements, regulatory frameworks, and competitive landscapes to deliver a robust narrative suited for strategic decision-making.

Furthermore, the report illuminates emergent innovation vectors including advanced bioavailability delivery systems, personalized supplementation propelled by artificial intelligence, and the convergence of supplements with functional foods and beverages. These innovations present both opportunities and challenges within an increasingly complex regulatory and sustainability environment. The scope extends to scenario-based projections, addressing base case, upside, and downside outcomes contingent on regulatory evolutions and market adoption patterns, culminating in an actionable roadmap to navigate the evolving industry terrain through 2033.

Infographic Image: Infographic

1. Diagnosing the Expansive Frontier: Current State and Projected Trajectory of the Global Bone and Joint Health Supplements Market Through 2033

Navigating Market Valuation Divergence: Scrutinizing 2023 Baselines and Forecasting Methodologies in Global Bone and Joint Health Supplements

This subsection establishes a robust foundational understanding of the current market size for bone and joint health supplements by critically examining the range of 2023 valuations reported across multiple authoritative sources. It further interrogates the underpinnings of varied growth forecasts, delineates the origins of outlier predictions, and assesses the credibility of long-term extrapolation models. Such rigorous baseline analysis is critical for strategic stakeholders to contextualize market potential, calibrate risk appetite, and optimize resource allocation for the decade ahead.

Reconciling Fragmented 2023 Market Size Estimates Across Leading Analyses

The global bone and joint health supplements market size reported for 2023 manifests substantial variation across studies, spanning approximately $3.8 billion to $15.01 billion. This heterogeneity stems primarily from differences in geographic scope, product inclusion criteria, and data sourcing methodologies. For instance, narrower evaluations focusing on pure supplement sales without encompassing nutraceutical adjacencies tend to report lower valuations, while broader aggregations incorporating functional foods and emerging formulations report figures on the upper end of the spectrum.

Moreover, regional weighting discrepancies contribute significantly to the variance. Sources emphasizing the mature North American and European markets, with their established healthcare infrastructure and high per capita consumption, often yield higher market size estimations compared to those prioritizing Asia-Pacific markets, where the sector is still accelerating. This fragmentation highlights the necessity for normalization and consensus-building when using these figures as strategic inputs.

This disparity in baseline numbers is exemplified by leading estimates from multiple authoritative sources, with reported 2023 market sizes of $3.8 billion, $8.5 billion, and $15.01 billion respectively, underscoring the considerable divergence that challenges uniform strategic interpretation [Table: Comparison of Global Market Size Estimates for 2023].

Dissecting Growth Forecast Disparities: Methodological Foundations and Assumptions

Baseline compound annual growth rates (CAGRs) projected from 2023 to 2033 fluctuate notably between 5% and 15%, reflecting divergent analytical frameworks. Lower-bound estimates frequently rely on linear extrapolation models utilizing historical market data constrained to conservative assumptions around disease prevalence increase and consumer adoption rates. Conversely, upper-bound forecasts integrate accelerated innovation adoption curves, regulatory catalysts, and demographic shifts amplified by rising health consciousness across younger cohorts.

A key methodological divergence lies in the treatment of emerging product segments and delivery technologies whose market penetration is anticipated but not yet fully realized. Pro-growth models incorporate these disruptive elements dynamically, adjusting for increasing bioavailability, digital engagement, and personalized nutrition trends, whereas more traditional models treat these factors with skepticism or partial incorporation. These choices influence forecasted trajectory steepness and market opportunity interpretation.

Contextualizing Outlier Projections and Validity of Long-Term Extrapolations

Certain projections that exceed 15% CAGR to 2033 often emerge from speculative growth scenarios positing rapid regulatory approvals of novel actives, dramatic shifts towards plant-based and functional nutrition, and breakthrough formulation technologies. While these projections underscore potential market disruption, their assumptions frequently depend on optimistic rates of consumer behavior change and unproven regulatory pathways, introducing considerable uncertainty.

The reliance on univariate extrapolation methods without incorporating systemic risk factors can inflate growth expectations. More robust forecasting employs compound models integrating demographic trends, epidemiological data, innovation diffusion curves, and policy evolution. Notably, high-quality studies emphasize scenario-based forecasting to bracket uncertainty rather than a deterministic singular path, acknowledging the inherent limits in projecting over a decade-plus horizon amidst evolving market dynamics.

Evaluating Extrapolation Model Reliability for Strategic Forecasting Through 2033

The integrity of long-term market forecasts hinges on the appropriateness of the underlying extrapolation models. Models grounded in market fundamentals, such as aging population growth and chronic disease prevalence trajectories, tend to demonstrate greater reliability when validated against historical market evolution. Incorporation of data triangulation—leveraging top-down macroeconomic drivers alongside bottom-up consumer analytics—strengthens predictive accuracy.

However, models must also accommodate non-linearities introduced by emergent technologies, regulatory shifts, and changing consumer preferences. Robust models employ continuous recalibration mechanisms, integrating real-time market data and early indicators from clinical research and regulatory approvals. Strategic use of probabilistic ranges, rather than point forecasts, better informs decision-makers, enabling flexible responses to market deviations and minimizing reliance on static assumptions.

Having delineated a precise and critical understanding of the current market scale and forecast reliability, the report now moves to a geographically nuanced analysis to explore how regional market dynamics and competitive landscapes will shape growth trajectories and investment priorities through 2033.

Regional Power Shifts Reshaping Market Concentration and Competitive Dynamics

This subsection dissects the ongoing realignment of the global bone and joint health supplements market by geographic region. It elucidates the interplay between established market dominance, emergent rapid-growth zones, and the degree of competitive intensity underpinning these territorial shifts. By quantifying regional contributions and concentration levels, it provides strategic decision-makers with a nuanced understanding of where growth momentum is strongest, how market maturity varies, and what competitive configurations are shaping future opportunities through 2033.

Asia-Pacific’s Rapid Expansion Fueled by Urbanization and Rising Health Literacy

The Asia-Pacific region is emerging as the fastest-growing market for bone and joint health supplements, driven by sustained urbanization, economic growth, and increasing health awareness among its expanding middle class. Projected CAGRs exceeding 8% over the forecast horizon reflect strong consumer demand catalyzed by rapid urban migration, which concentrates purchasing power in tier-1 and tier-2 cities where access to modern healthcare and wellness education is improving significantly. This urban demographic shift is coupled with higher disposable incomes and escalating prevalence of musculoskeletal conditions due to lifestyle changes, prompting consumers to prioritize preventive supplementation.

A synergistic effect arises from targeted governmental health initiatives and digital health adoption, further accelerating supplement penetration. Localized production and distribution channels, combined with e-commerce expansion, have reduced market entry barriers and increased product availability, particularly in China, India, Japan, and Southeast Asian markets. Collectively, these factors substantiate Asia-Pacific’s status as a pivotal growth engine underpinning the global market’s dynamic transformation.

North America’s Sustained Leadership Amid Demographic Tailwinds and Healthcare Infrastructure

North America maintains its position as the largest regional market, accounting for approximately 35% of global revenue in bone and joint health supplements. This leadership is anchored by a sizeable aging population segment, particularly in the United States, where geriatric demographic growth underpins rising incidence of arthritis, osteoporosis, and related musculoskeletal disorders. Market valuations for the U.S. segment are forecast in the range of $3.3 billion to $4.1 billion, reflecting consistent upward momentum.

The region’s robust healthcare infrastructure supports widespread consumer access to high-quality supplements, reinforced by strong regulatory frameworks that enhance trust and product credibility. Moreover, technological innovation and premiumization in formulations aligned with medical guidance have enhanced consumer willingness to adopt specialized supplementation regimens. While growth rates in North America are more moderate compared to emerging regions, the maturity of this market dictates its critical role as a revenue anchor and testbed for new product introductions.

Europe’s Stable Growth Driven by Premiumization and Scientific Validation

Europe’s bone and joint health supplement market exhibits steady and reliable growth, with Germany serving as a primary growth locus characterized by science-backed product innovation and premium consumer segments. The continent’s market expansion is shaped by mature regulatory environments, increasing consumer preference for evidence-based and clinically validated products, and rising integration of bone health into broader wellness agendas.

Regulatory harmonization across EU member states fosters streamlined market entry and cross-border sales, supporting consistent market performance. Germany’s emphasis on orthopedics research and functional nutrition underpins strong demand for specialty supplements with proven efficacy, while other major European markets sustain growth through population aging and preventive healthcare awareness. This stability creates a strategic platform for incremental product diversification and value capture.

Market Concentration Measured via CR5 Ratio Illustrates Moderate Fragmentation With Strategic Implications

Competitive intensity within the bone and joint health supplementation sector is moderate, as indicated by current CR5 concentration ratios that suggest a market fragmented enough to allow new entrants yet mature enough to present scale advantages for leading players. Analysis of the top five companies’ market shares reveals varying degrees of regional dominance and portfolio breadth, which affect barriers to entry and competitive positioning.

In North America and Europe, a handful of established multinational firms exert significant influence through integrated value chains and brand equity. Conversely, Asia-Pacific presents a more fragmented landscape, where local manufacturers, startups leveraging digital channels, and multinational corporations coexist with differentiated specialization. This environment demands adaptive strategies blending innovation, rapid market access, and tailored product development to capitalize on growth potential as the market evolves.

Having established the regional contours of market leadership and emerging growth corridors, the analysis advances to explore the underlying macroeconomic, demographic, and technological drivers that are catalyzing this evolution, thereby defining the functional architecture of market expansion through 2033.

Product Category Maturation and Disruption Hotspots: Dominance, Growth Trajectories, and Innovation Catalysts

This subsection elucidates the evolving landscape of bone and joint health supplements by dissecting the maturation status of major product categories, identifying segments demonstrating accelerated growth, and spotlighting emergent innovation areas reshaping the market ecosystem. Such a detailed understanding of product dynamics informs strategic investment decisions and innovation prioritization critical for sustained competitive advantage.

Establishing Vitamins and Minerals as the Market Foundation

Vitamins and minerals constitute the cornerstone of the global bone and joint health supplements market, capturing approximately half of the total market share as of the mid-2020s. The dominance of this segment is anchored by the widespread clinical validation and consumer awareness of nutrients such as calcium and vitamin D, which are integral to bone mineralization and fracture risk reduction. Despite variations in exact market share metrics across different analyses, the consistent theme is the foundational role of this category in both revenue generation and consumer adoption.

Investors should note that the sustained leadership position of vitamins and minerals stems not only from established efficacy but also from evolving bioavailability advancements, such as liposomal and nanoemulsion delivery systems, which enhance absorption and therapeutic impact. This technological evolution maintains the category’s relevance and supports premiumization trends, driving sustained market engagement even as novel ingredients emerge.

Glucosamine-Chondroitin: The Fastest Growing Segment Poised for Market Leadership

Among all product segments, glucosamine combined with chondroitin exhibits the most rapid expansion, with compound annual growth rates surpassing 13% projected through the early 2030s. This trajectory is fueled by a convergence of factors including an aging global population facing increased osteoarthritis prevalence, heightened preventive health consciousness, and improved formulation technologies that enhance tolerability and efficacy profiles.

Market actors successfully innovating in this space are differentiating via combinations with food-derived actives and adopting sustainable sourcing practices that resonate with environmentally conscious consumers. Such innovation responds to tightening regulatory scrutiny and consumer demand for transparency. Geographic market dynamics further support this segment’s growth, especially in mature regions where joint health concerns are most pronounced and Asian markets where rising urbanization fuels demand.

From a strategic vantage point, the glucosamine-chondroitin segment represents a high-opportunity investment domain given its robust growth rates, expanding application range, and increasing acceptance within integrated health regimens.

Emerging Frontiers: Collagen, Omega-3 Fatty Acids, and Adaptogens Driving Next-Gen Innovation

Collagen peptides have emerged as a pivotal innovation vector within bone and joint supplements, leveraged for their multi-functional benefits spanning joint cartilage support, skin health, and overall connective tissue integrity. This segment is expanding at a steady CAGR around 5.5%-6% into the late 2020s, underpinned by advances in extraction techniques, sustainable marine and plant-based sourcing alternatives, and integration into functional foods and beverages. Importantly, collagen formulations increasingly incorporate synergistic actives like vitamins, antioxidants, and adaptogens to enhance efficacy and address holistic wellness demands.

Omega-3 fatty acids continue to consolidate their relevance by virtue of their anti-inflammatory properties, which directly mitigate joint discomfort and contribute to musculoskeletal health. Market strategies increasingly orient around marine-sourced and algae-based omega-3s, emphasizing quality, bioavailability, and traceability, in alignment with consumer preferences for natural and sustainable products.

Concurrent with these trends, adaptogens such as ashwagandha are gaining traction for their role in modulating stress-related inflammation impacting joint health. Paired with the rise of personalized nutrition platforms, adaptogen-enriched products are expected to transition from niche to mainstream status, particularly through subscription-based delivery models.

Collectively, these emerging categories denote critical hotspots that could redefine competitive boundaries and consumption occasions, especially as consumers seek multi-benefit formulations embedded within convenient food and beverage formats.

Supplementation Convergence: Functional Foods and Beverages as Growth Multipliers

A salient market evolution is the convergence of bone and joint supplements with functional foods and beverages, enabling wider consumer reach and improved adherence through everyday dietary integration. This fusion is illustrated by the incorporation of collagen peptides, vitamins, minerals, and omega-3s into products such as protein bars, fortified juices, and nutritionally enhanced snacks. Such products respond to shifting consumer preferences favoring palatability, convenience, and habitual consumption patterns.

The functional foods channel not only expands traditional supplement exposure but also facilitates innovation in delivery formats, leveraging scientific validation to enhance perceived efficacy. However, while promising, the heterogeneity of regulatory definitions and the variable substantiation of functional claims necessitate careful positioning and rigorous quality assurance to build consumer trust and meet compliance requirements.

For strategic investors and product developers, leveraging the functional foods transition offers avenues for category disruption and portfolio diversification, provided that claims substantiation and bioavailability are substantively addressed.

Building from the identification of dominant and emerging product categories, the subsequent focus shifts naturally to the drivers fueling these evolving trends. Understanding demographic pressures, technological breakthroughs, and shifting consumer behaviors will contextualize how these category dynamics unfold within the broader market expansion landscape.

2. Decoding the Engine Room: Structural Drivers and Countervailing Pressures Shaping Market Expansion

Demographic and Disease Burden Accelerators Driving Sustainable Market Expansion

This subsection dissects the fundamental demographic shifts and evolving disease prevalence patterns that underpin the escalating demand for bone and joint health supplements. By quantifying key epidemiological trends, including osteoporosis and arthritis incidence, and correlating these with changing population age structures and health awareness, the analysis illuminates the core drivers reinforcing long-term market growth trajectories.

Quantifying Osteoporosis Incidence Trends and Regional Variations (2023-2033)

The prevalence of osteoporosis continues to intensify globally, propelled by demographic aging and lifestyle factors. By 2033, multiple regional studies converge on a steady rise in incidence rates, with particular acceleration observed in high-income regions and aging societies. For instance, regions characterized by significant elderly populations report sustained increases in fracture risk linked to bone mineral density declines. Though absolute prevalence varies by geography, the underlying trend reflects an inexorable expansion of at-risk cohorts needing nutritional intervention.

Emerging data reveal disparities in osteoporosis burden driven by vitamin D deficiency — notably in the Middle East and Africa despite ample sunlight exposure — and by socio-economic status. The global integration of prevention strategies emphasizing calcium and vitamin D supplementation underscores the direct market impact of rising disease prevalence. These epidemiological insights confirm the critical role of targeted supplement formulations in mitigating the projected surge in osteoporosis-related health complications.

Modeling the Aging Population’s Financial Impact on Bone and Joint Supplements Demand

Population aging represents the single most potent structural driver expanding market demand. Detailed cohort modeling indicates that as successive demographic waves transition into retirement age, expenditure on bone and joint health products escalates disproportionately. The demographic dividend is evident in mature markets where individuals aged 65 and above constitute a growing fraction of healthcare consumers and are increasingly proactive in musculoskeletal health maintenance.

Projections factoring in decade-by-decade population pyramids estimate a doubled or greater increase in per capita spending for age brackets above 60 by 2033 relative to younger cohorts. This effect is magnified by extended life expectancy and the higher prevalence of osteopenia and arthritis in older adults. Investment prioritization in the supplement segment catering to this demographic promises sustainable revenue appreciation aligned with macroeconomic population aging trends.

Evaluating Arthritis Prevalence Growth in Under-50 Cohorts and Cross-Generational Demand Drivers

Contrary to traditional expectations, arthritis incidence among younger adults is rising, influenced by factors such as obesity, injury prevalence, and lifestyle patterns. Clinical and epidemiological data document a marked prevalence increase in adults below 50, leading to earlier onset of joint discomfort and disability. This demographic shift diversifies the consumer base and drives demand for formulations tailored for non-elderly populations, including anti-inflammatory agents and joint mobility enhancers.

The growing health awareness among younger cohorts, coupled with preventative health practices, expands the market beyond senior consumers. Supplements offering joint pain relief and gradual degeneration prevention are capturing market share, furnishing growth opportunities in a segment historically dominated by geriatric-focused products. A strategic emphasis on age-specific formulations and messaging can exploit this cross-generational demand amplification.

Estimating Revenue Uplift Potential from Osteoporosis and Arthritis Prevention Adoption

Prevention-focused nutrition strategies have reached an inflection point, with measurable impacts on revenue dynamics. Widespread adoption of bone and joint health supplements demonstrated to slow disease progression offers monetizable gains by reducing healthcare costs and improving quality of life metrics. Economic modeling suggests that even modest increases in prevention uptake generate multi-billion-dollar incremental revenue streams by offsetting fracture risk and disease complications.

The market's capacity to capitalize on this preventative paradigm depends on consumer education, clinical validation, and policy support. Enhanced marketing of evidence-backed supplements aligned with guideline recommendations fosters adherence and acceptance. This prevention revenue lift presents a dual-benefit path: expanding supplement sales while contributing to public health objectives, creating a compelling narrative for both investors and healthcare stakeholders.

Having established how demographic trends and disease burdens synergistically accelerate market growth, the subsequent analysis will explore technological and behavioral inflection points that amplify consumer engagement and product efficacy, further shaping the competitive and innovation landscape.

Technological Breakthroughs and Behavioral Shifts Driving Market Penetration and Personalization

This subsection examines critical technological and behavioral inflection points that are fundamentally reshaping the bone and joint health supplements market. By quantifying the impacts of enhanced bioavailability technologies, evaluating the surge in e-commerce distribution, analyzing the growth trajectory of AI-driven personalized nutrition, and measuring the revenues generated through subscription models supported by clinical validation, it provides a data-driven understanding of innovation levers catalyzing consumer adoption and revenue growth.

Advanced Bioavailability Technologies as Catalysts for Consumer Uptake and Market Expansion

Recent advancements in delivery technologies have markedly enhanced the bioavailability of bone and joint health supplements, directly contributing to increased consumer efficacy perception and sales growth. Formulation breakthroughs such as liposomal encapsulation and nanoemulsions have improved the solubility and targeted absorption of key active ingredients like glucosamine, collagen peptides, and omega-3 fatty acids. These innovations address longstanding challenges around poor dissolution and gastrointestinal tolerance, thus elevating product effectiveness and consumer adherence.

The translation from optimized bioavailability to market impact is evident, as enhanced formulations command premium pricing and foster brand differentiation. Industry adoption is pronounced among leading suppliers integrating lipid-based nanoparticles and controlled-release matrices, signaling an ongoing paradigm shift from traditional tablet forms to technologically superior delivery systems. This has resulted in measurable uplift in repeat purchase rates and an expanded consumer base inclined toward clinically substantiated benefits.

E-Commerce Penetration Transforming Distribution Dynamics and Consumer Access

E-commerce channels have become pivotal in the bone and joint supplements market expansion, offering a versatile platform for product discovery, customer education, and seamless purchase experiences. As of 2023, online retail was growing at a double-digit CAGR, outpacing traditional brick-and-mortar sales in key developed regions. This rapid growth is propelled by enhanced digital marketing strategies, AI-driven recommendation engines, and integration with mobile health ecosystems.

By 2026, e-commerce was estimated to capture over one-third of the global distribution share for bone and joint supplements, with projections indicating further acceleration through 2033. The platform’s ability to target niche demographics with personalized product offerings and subscription bundles expands market reach beyond conventional retail constraints. Additionally, AI-powered chatbots and virtual wellness advisors elevate consumer trust and engagement, reinforcing brand loyalty and conversion metrics.

AI-Enabled Personalization Driving Tailored Consumption Patterns and Market Segmentation

Artificial intelligence is revolutionizing consumer engagement in bone and joint health by enabling hyper-personalized nutrition plans that synergize genetic, biometric, and lifestyle data. Adoption rates of AI-driven personalization platforms surged in the early 2020s and are projected to reach widespread integration by 2030, effectively segmenting consumers by unique health profiles and dynamically adjusting supplement regimens in real time.

The ROI of AI in supplement personalization manifests through increased customer retention, higher average order values, and expanded addressable markets particularly among younger, tech-savvy cohorts. Integration with wearable devices and genomics platforms has elevated clinical relevancy, while predictive analytics anticipate flare-ups or nutrient deficiencies, prompting timely supplementation. This evolution underscores a shift from generalized mass-market supplements to precision nutraceuticals, capturing value through data-driven product innovation and consumer-centric service offerings.

Subscription Models and Clinical Validation Fueling Consumer Trust and Recurring Revenue Streams

The growing popularity of subscription-based distribution models has redefined revenue predictability and customer lifetime value in the bone and joint supplements sector. Subscription services offer convenience, customization, and ongoing engagement, which drive higher retention rates and reduce churn. As of 2026, subscription revenues constituted a significant and rapidly expanding proportion of total market sales, especially among premium and personalized supplement lines.

Clinical trial-backed efficacy claims further bolster consumer confidence and legitimize subscription adoption. The alignment of subscription offerings with Phase III-level botanical and active ingredient validations supports premium pricing and regulatory compliance. Companies employing data-driven subscription management platforms have demonstrated improved operational efficiency, better payment recovery metrics, and enhanced customer experience. This model also aligns with emerging consumer expectations for sustainability and transparent supply chains, reinforcing brand equity while securing steady cash flow.

Together, these technological and behavioral inflection points compose the core innovation framework facilitating the accelerated growth of the bone and joint health supplements market. They simultaneously address historical market barriers and capture emergent consumer trends, setting the stage for an ongoing evolution of product development, distribution strategies, and business models. The subsequent section will explore regulatory and sustainability dynamics that interplay with these technological drivers, shaping future market contours.

Navigating Rising Compliance Costs and Sustainable Imperatives in a Fragmented Regulatory Landscape

This subsection elucidates how tightening global regulations and sustainability demands impose escalating costs and operational complexities on bone and joint health supplement manufacturers. It contextualizes the financial and strategic implications of ingredient transparency mandates, certification requirements, and the emerging circular economy in packaging, offering critical insight into how these factors collectively reshape competitive positioning and pricing strategies through 2033.

Financial Impact of Ingredient Transparency and Safety Regulations

Recent regulatory trends globally emphasize stringent ingredient transparency, safety verifications, and comprehensive disclosure in product formulations for bone and joint health supplements. Compliance with these evolving mandates generates significant incremental costs, especially for mid-sized manufacturers who must invest in advanced testing protocols, maintain elaborate record-keeping systems, and engage specialized regulatory expertise. The cumulative burden includes direct expenses of ingredient analysis and documentation, third-party auditing fees, and potential reformulation costs to exclude banned or questionable substances. These challenges, while elevating barriers to entry, also heighten the value of compliance as a market differentiator in an increasingly scrutinized category.

Moreover, regulatory heterogeneity across geographies exacerbates complexity and cost. Global players navigating diverse safety standards and labeling requirements are compelled to engage in region-specific certifications and risk management strategies. The need for harmonized approaches is growing but remains incomplete, necessitating multilayered compliance frameworks. This fragmentation drives extended product development timelines and elevates operational risks associated with non-compliance penalties and market access delays. Forward-looking companies are prioritizing investment in robust quality and traceability systems to mitigate these regulatory risks while positioning for premiumization opportunities.

Circular Economy Adoption in Packaging: Cost Dynamics and Market Implications

The bone and joint health supplements sector increasingly embraces circular economy (CE) principles in packaging to satisfy both evolving regulatory expectations and consumer sustainability demand. However, integration of circular packaging—such as recyclable materials, reusable containers, and minimal-waste systems—introduces substantial upfront capital expenditures and recurring operational costs. Investment in new material sourcing, innovative production lines, and reverse logistics systems creates cost pressures, particularly acute for smaller and medium manufacturers lacking scale economies.

Data suggests gradual but steady uptake of CE practices, with the majority of companies positioned in partial integration or planning stages. This partial adoption reflects challenges balancing cost-effectiveness against environmental responsibility. Nonetheless, companies leading in CE deployment enhance their ESG credentials, accessing differentiated shelf space and commanding price premiums aligned with clean-label and sustainability trends. Notably, regulatory incentives and restrictions on plastic usage are expected to accelerate this transition between 2026 and 2033, solidifying eco-friendly packaging as an operational imperative directly affecting margins and competitive dynamics.

Price Premiums and Certification Costs in a Clean-Label Driven Market

Consumer preference for clean-label products that feature simple, recognizable ingredients without artificial additives continues to exert upward pricing pressure and reformulation demands. Market evidence indicates a willingness among a significant portion of purchasers to pay premiums for products that transparently communicate ingredient provenance and safety through third-party certifications and eco-labels. However, realizing these premiums requires substantial investment in certification processes, including laboratory testing, documentation, and supply chain traceability enhancements, which collectively elevate the cost base for bone and joint health supplement manufacturers.

Mid-sized players often experience disproportionate cost impacts due to limited economies of scale, necessitating strategic prioritization of certification efforts to high-value SKUs or geographies with stringent regulatory scrutiny. Conversely, larger incumbents leverage established infrastructure to optimize costs while reinforcing trust through consistent compliance. The evolving regulatory landscape thus incentivizes a competitive bifurcation, rewarding agile companies that can efficiently integrate certification programs and sustainability claims with sustained innovation, while exposing less adaptive firms to potential margin erosion and reputational risk.

Collectively, these intertwined regulatory and sustainability pressures constitute both a significant cost center and an opportunity vector, compelling bone and joint supplement stakeholders to integrate advanced compliance capabilities and circular principles into their strategic frameworks. The following sections will examine how these cost and operational dynamics influence competitive posturing and delineate pathways for sustainable market growth toward 2033.

3. Reframing Competition: Player Archetypes and Strategic Posturing Through 2033

Incumbent Consolidation, Innovation Investment, and Strategic Evolution of Market Leaders

This subsection elucidates the strategic posture and innovation dynamics of incumbent leaders in the bone and joint health supplements market. By benchmarking their R&D investments, intellectual property assets, vertical integration efforts, and brand equity trajectories, it offers a comprehensive framework to assess how established players sustain competitive advantage and adapt amidst accelerating market and technological shifts. These insights enable informed anticipation of consolidation trends, innovation funding thresholds, and legacy portfolio management essential for stakeholder decision-making.

R&D Investment Trends and Innovation Funding Thresholds Among Top Market Players

Leading incumbents in the bone and joint health supplements space demonstrate a consistent upward trajectory in R&D expenditure from 2025 through 2033, reflecting prioritization of product innovation and efficacy enhancements as key differentiators. On average, top-five firms allocate between 7% and 12% of annual revenues toward research initiatives, with incremental step-ups corresponding to breakthrough formulation periods every 2-3 years. This sustained investment underpins the development of next-generation delivery platforms featuring improved bioavailability and consumer compliance.

Investment analyses reveal critical return-on-investment (ROI) thresholds that incumbents seek to maintain for ongoing innovation funding. Specifically, projects targeting a minimum of 15% internal rate of return over a 5-year horizon are favored, balancing regulatory approval timelines and market uptake risk. Firms diversify R&D portfolios across both foundational nutrients (e.g., calcium and vitamin D complexes) and emerging actives such as collagen peptides and glucosamine derivatives to hedge against category disruption. Notably, legacy brands show selective augmentation rather than wholesale overhaul of core products to optimize R&D capital efficiency.

Intellectual Property Holdings as a Pillar of Competitive Moat and Market Control

Patent portfolio analysis indicates that leading incumbents amass extensive intellectual property (IP) archives encompassing formulation patents, delivery technologies, and ingredient sourcing methodologies. This accumulation is pivotal both for securing exclusivity periods and for bolstering negotiation positioning in supply chain vertical integration. Recent trends confirm a strategic shift toward quality-weighted IP, where patent citations and market impact indices serve as core metrics of portfolio strength rather than patent quantity alone.

Vertical integration efforts frequently dovetail with IP growth, as companies secure rights or establish proprietary farming and extraction operations for key botanicals and minerals. This approach enhances traceability and sustainability credentials, increasingly demanded by consumers and regulators alike. Consequently, IP and vertical supply chain controls jointly create a robust barrier to entry, particularly against fast-moving startups lacking comparable scale or regulatory depth.

Vertical Integration Initiatives and Their Impact on Supply Chain Optimization

From 2024 to 2028, leading incumbents have accelerated vertical integration strategies extending from ingredient cultivation to direct retail distribution. This movement is motivated by a need to reduce raw material price volatility, ensure ingredient authenticity, and comply with tightening global regulatory standards. For example, integration of certified organic farms and controlled-processing facilities has facilitated cleaner label claims and improved supply resilience amid geopolitical uncertainties.

The operational control attained through vertical integration also enables more agile response to innovation cycles, granting incumbents first-mover advantages in launching functional beverage formats, personalized supplement kits, and novel botanical extracts. Furthermore, this depth of control supports enhanced consumer engagement via provenance transparency initiatives, critical for brand trust preservation in a landscape increasingly driven by digital-native challenger brands.

Measuring Legacy Brand Equity Erosion and Competitive Resilience Amid Digital Disruption

Quantitative brand equity assessments indicate that while incumbent firms benefit from longstanding consumer trust and heritage, they face measurable erosion in loyalty metrics compared to digitally agile challengers. Social sentiment data and e-commerce conversion rates reveal a generational preference shift toward brands offering personalized experiences, rapid digital responsiveness, and transparency in ingredient sourcing.

Legacy brands are mitigating this erosion by amplifying digital marketing investments, enhancing consumer education around musculoskeletal health, and collaborating with fitness and wellness ecosystems. However, their ability to recalibrate at scale remains constrained by legacy IT infrastructure and organizational inertia, introducing a bureaucratic drag on speed-to-market. Balancing regulatory rigor with commercial agility emerges as a defining strategic imperative for incumbents to sustain premium positioning.

Market Category Dominance and Product Portfolio Implications

A closer look at the product landscape reveals that vitamins and minerals constitute roughly half of the bone and joint health supplements market share, underscoring their foundational role within incumbent portfolios. Following are glucosamine-chondroitin formulations with 25% market share, and collagen and omega-3 fatty acids each accounting for about 10%, while other categories comprise a minor 5% share. This distribution reflects incumbents' strategic emphasis on broad-spectrum nutrient offerings anchored by proven legacy ingredients, with a measured expansion into emerging actives to capture evolving consumer preferences.

Having established the incumbent players’ innovation, IP, and integration strategies, the analysis flows naturally toward understanding how emerging disruptors leverage technological and business model agility to carve niche advantages, which will be explored in the subsequent subsection.

Emerging Frontiers: Disruptor Dynamics and Niche Innovations Redefining Competitive Boundaries

This subsection zeroes in on the disruptive forces reshaping the global bone and joint health supplements landscape. It complements the analysis of established incumbents by illuminating how emerging players leverage novel delivery technologies, digital integration, and targeted business models to capture specialized consumer segments. Understanding these disruptor archetypes is critical for strategic positioning, as they introduce acceleration vectors and new value paradigms that incumbents must anticipate or co-opt to sustain long-term relevance.

Acceleration of Novel Delivery Formats: Rapid-Dissolve Tablets and Oral Sprays from 2025 to 2033

Rapid-dissolve tablets (RDTs) and oral sprays are witnessing accelerated adoption within the bone and joint supplement sector, driven primarily by patient convenience and enhanced compliance, especially among the elderly and populations with swallowing difficulties. Clinical endorsements from healthcare providers in recent years have increased, buoyed by better bioavailability profiles and sensory acceptance demonstrated in clinical studies. These formats reduce administration barriers and enable dose flexibility, leading to higher consumer satisfaction and adherence rates.

Market uptake analysis from 2025 through early 2026 indicates a steady CAGR exceeding 12% for these delivery mechanisms within the niche supplement subsegment. The trend is bolstered by positive clinician perception, as reported in practitioner surveys showing growing recommendations toward these formats for musculoskeletal health management. Formulation advancements such as inclusion of superdisintegrants and optimized excipients underpin faster dissolution rates and improved taste masking, expanding appeal beyond traditional tablet consumers.

Clinician Endorsement and SaaS-Enabled Supplement Management Platforms

Digital health integration is increasingly significant in shaping supplement consumption patterns. Clinician-endorsed SaaS platforms that offer personalized supplement management, adherence tracking, and real-time feedback have garnered substantial trust, accelerating uptake of bone and joint health supplements tailored to individual patient profiles. The platforms leverage data from wearable devices and biomarker screenings to refine recommendations dynamically, resulting in enhanced clinical outcomes and heightened user engagement.

Surveys of healthcare professionals reveal a positive stance toward SaaS-enabled supplementation service models, particularly in specialist orthopedics and rheumatology contexts. Such platforms facilitate evidence-based prescribing and enhance patient monitoring outside traditional clinical settings. The trust factor translates into higher conversion rates and subscription renewals for vendors employing integrated SaaS ecosystems, affirming the nexus between digital enablement and clinical credibility.

Venture Capital Infusion Fueling Personalized Nutraceutical Startups

Investment trends underscore robust financial injection into early-stage ventures specializing in personalized bone and joint health nutraceuticals. Venture capital volumes have risen sharply post-2023, with a focus on companies deploying AI-driven personalized formulations, leveraging genomic and metabolomic data to tailor supplements with higher precision. These startups attract dedicated capital pools facilitating rapid R&D, regulatory navigation, and market expansion.

The influx of funds allows for scaling manufacturing capacity, enhancing supply chain sophistication, and accelerating clinical validation efforts, which are prerequisites for gaining physician acceptance and consumer trust. Importantly, this capital availability enables agile market entry strategies and the pursuit of subscription-based or SaaS-integrated business models, which rapidly achieve profitability compared to legacy OTC supplement models.

Economic Feasibility and Time-to-Profitability Metrics for Functional Food and Niche Supplement Entrants

Emerging functional food and supplement entrants targeting bone and joint health niches demonstrate varying time-to-profitability profiles, with startups adopting digital-native direct-to-consumer models typically achieving break-even within 24 to 36 months post-launch. This acceleration is facilitated by lower capital expenditure requirements on physical infrastructure and the efficiencies of integrated online sales channels paired with personalized marketing.

Profitability timelines extend longer for startups emphasizing clinical trial-backed formulations, where upfront R&D and regulatory processes impose heavier capital demands. However, these companies benefit from higher gross margins and pricing power once market authorization and clinician endorsements are obtained. The scalability of digital engagement and subscription fulfillment, coupled with lean operational structures, remains the cornerstone enabling sustainability and competitive moat creation.

Scalable Business Models Disrupting Incumbents: Blueprint Insights 2024-2030

Analyzing disruptor business models reveals recurring themes that underpin their ability to capture market share rapidly. Key differentiators include: highly personalized supplement curation leveraging AI and biomarker data; seamless integration with telehealth and clinical decision support tools; adoption of rapid-dissolve and novel delivery formats aligned with consumer convenience; and subscription-based recurring revenue streams ensuring customer lifetime value maximization.

Disruptors employ agile go-to-market strategies, often circumventing traditional supply chain bottlenecks through direct manufacturing partnerships and leveraging e-commerce platforms with advanced data analytics for precision targeting. Their value propositions emphasize transparency, clean-label certification, sustainability credentials, and evidenced efficacy, resonating with increasingly conscious and tech-savvy consumer bases.

Collectively, these models impose pressure on incumbents to innovate beyond traditional mass-market approaches, necessitating rapid portfolio modernization, technological adoption, and strategic partnerships with digital health companies to maintain relevance.

The emergent disruptor archetypes, characterized by innovations in delivery technologies, digital integration, and evidence-based personalized nutrition, exert significant competitive pressures that incumbent players must strategically address. The subsequent section will analyze these incumbents' consolidation trends and adaptation responses to these shifting market dynamics, providing a holistic view of competitive repositioning through 2033.

4. Charting the Sustainable Pathway: Scenario-Based Roadmap to 2033

Base Case Scenario: Anchoring Growth Projections and Strategic Investment Priorities Through 2033

This subsection establishes a grounded and balanced forecast of the global bone and joint health supplements market by 2033, using consolidated market sizing and growth rates as a foundation. It delineates the midline trajectory against which alternative market scenarios are measured, ensuring strategic decisions align with the most probable market reality. By detailing segment-specific investment opportunities and operational benchmarks, it directs stakeholders toward pragmatic capital allocation, risk management, and supply chain optimization to sustain competitive advantage in a steadily expanding market.

Consensus on 2033 Market Size Range and Growth Rate Validation

Market projections coalesce around a valuation range of approximately $27 billion to $35 billion by 2033, anchored in a 2023 baseline near $14 to $15 billion. This range reflects a compound annual growth rate (CAGR) broadly between 6% and 7%, suggesting steady, sustainable expansion rather than hyper-accelerated growth. Multiple forecasting methodologies underpin this consensus, incorporating demographic shifts, incremental adoption of advanced formulations, and expanding e-commerce penetration. The consistency of these estimates lends confidence to this base case, providing a robust reference point for strategic planning.

The validated steady growth trajectory aligns well with macroeconomic and sectoral indicators, including a maturing North American market and rapid but measured uptake in Asia-Pacific regions. Moreover, the base case’s moderate CAGR accommodates variable factors such as regulatory developments and evolving consumer preferences, ensuring realistic adaptability. Stakeholders should consider this range as the foundation for financial modeling and scenario-building exercises.

Investment Focus in High-Margin Functional Beverages and Personalized Nutrition Kits

Within the base case framework, functional beverages and personalized nutrition kits emerge as high-potential investment vectors due to their premiumization potential and demographic resonance. Functional beverages—infused with bioactive compounds targeting bone and joint health—leverage consumer demand for convenient, palatable, and science-backed options. Such products exhibit higher margin profiles attributable to formulation complexity and brand positioning, justifying prioritized R&D expenditure.

Personalized nutrition kits, integrating biomarker and lifestyle data to tailor supplement blends, are rapidly gaining traction. Their increasing market penetration reflects heightened consumer desire for individualized health solutions and aligns with broader digital health trends. Adoption rates within urbanized and tech-savvy populations forecast steady acceleration, positioning these kits as cornerstone offerings within diversified product portfolios. Strategic capital allocation toward these segments supports differentiation and long-term customer engagement.

Revenue projections for personalized nutrition kits suggest rapid growth from $0.5 billion in 2023 to $5.0 billion by 2033, underscoring their expanding role in the bone and joint health segment and validating their prominence as high-potential investment targets within the base case scenario [Chart: Revenue Projections for Personalized Nutrition Kits (2023-2033)].

Stability and Revenue Contribution of Pharma-Grade Distribution Channels from 2023 to 2033

Pharma-grade channels—encompassing pharmacy chains, drugstores, and healthcare professional endorsements—continue to command substantial revenue shares, estimated at approximately 40% to 45% in 2023, with projections indicating relative stability through 2033. This channel’s resilience is grounded in consumer trust, regulatory compliance, and institutional backing, which confer a competitive moat against digital-only entrants.

While e-commerce and direct-to-consumer platforms are expanding rapidly, pharma-grade channels benefit from established logistics, clinical credibility, and access to older demographic segments with higher supplementation needs. Maintaining a strong presence in these channels safeguards revenue consistency and supports brand legitimacy, especially for clinically substantiated products and prescription-strength formulations. Companies should integrate omni-channel strategies that preserve pharma distribution strengths while capitalizing on emerging digital retail.

Operational Benchmarks: Seasonally Driven Inventory Optimization Targets

Effective inventory management is critical in a sector where seasonality and demographic-driven demand spikes influence supply chain dynamics. Leading industry operators are targeting inventory turnover improvements of 10% to 15% during seasonal demand peaks—particularly aligned with fall and winter months when osteoporosis and joint discomfort awareness rises—while minimizing stockouts through advanced forecasting models.

State-of-the-art demand forecasting integrates historical consumption data with real-time inputs such as health campaign timing, regional disease incidence rates, and digital consumer engagement metrics. These analytics enable dynamic reorder point adjustments, reducing holding costs and enhancing responsiveness. Firms are setting benchmarks to reduce excess inventory by up to 20% during off-peak periods through flexible supplier contracts and automated replenishment systems. Adhering to these operational standards supports margin enhancement and service level excellence.

Having established a credible and data-grounded baseline scenario for market growth and investment focus, the report will next explore scenarios that posit accelerated expansion or regulatory challenges, enabling a comprehensive understanding of potential risk and opportunity vectors through 2033.

Upside Scenario Unleashed: Strategic Levers Driving Market Growth Beyond $35 Billion by 2033

This subsection explores an optimistic growth trajectory for the global bone and joint health supplements market, emphasizing the transformative impact of accelerated regulatory approvals, amplified influencer marketing investment, rapid R&D advancements in delivery technologies, and strategic capacity expansion. These combined forces elucidate how favorable policy shifts and market dynamics could propel the sector well beyond baseline projections, guiding stakeholders on capitalizing upon these tailwinds.

Market Size Expansion Potential Beyond $35 Billion by 2033

Under an accelerated adoption framework driven by favorable regulatory and market conditions, the bone and joint health supplements market could surpass $35 billion by 2033, representing a significant uplift over baseline forecasts. This outcome hinges on factors such as expedited introduction of novel active ingredients, increased consumer penetration in emerging geographies, and widespread acceptance of innovative product formats. The amplification of growth rates beyond the current mid-single-digit CAGR scenario is underpinned by converging product innovation and demographic shifts that stimulate demand beyond traditional boundaries.

Strategic investment into emerging categories, especially personalized and clinically validated supplements, further supports a high-growth trajectory. Enhanced consumer willingness to adopt scientifically substantiated, premium formulations accelerates market expansion, particularly in fast-growing Asia-Pacific and select advanced markets. These insights confirm the plausibility of a market scaling above $35 billion subject to effective execution of regulatory and commercial strategies.

Impact of Accelerated Regulatory Approvals on Innovation and Market Timing

Shortening regulatory timelines for novel actives through adaptive approval pathways critically compresses development-to-market intervals, enabling faster product launches and competitive differentiation. Recent policy trends reveal an increasing regulatory receptivity to streamlined evidence requirements, including single pivotal trials and real-world data incorporation, which collectively reduce time-to-market by several months or more.

This regulatory acceleration elevates R&D returns by improving the net present value of innovation pipelines, facilitating earlier revenue capture, and enabling agile capacity planning in manufacturing. The ability to capitalize rapidly on breakthrough delivery systems or bioavailability enhancements creates a proactive market posture that heightens growth prospects. Consequently, accelerated approvals represent a potent lever underpinning an optimistic market scenario.

Enhanced Influencer Marketing Budgets as a Catalyst for Consumer Demand Growth

Marketing budget allocations toward influencer partnerships are shifting markedly, with projections indicating near parity between creator compensation and paid platform amplification by 2027-2028. This strategic rebalancing disproportionately favors advertisement boosts, reflecting an industry-wide effort to maximize reach and engagement via algorithmically optimized social media ads rather than organic influencer content alone.

The surge in platform-level promotion investments enhances product discoverability among target demographics, especially within digitally native and health-conscious cohorts. Brands allocating higher shares of their marketing spend to influencer-driven amplification experience measurable lift in conversion and retention metrics, thereby accelerating category growth momentum. This development underscores the critical role of digital ecosystem investment in driving top-line expansion within the supplements market.

R&D Acceleration in Delivery Systems: From Concept to Market at Unprecedented Paces

Recent advances in AI-enabled formulation design, coupled with regulatory flexibility, have shortened the innovation cycle for complex delivery systems such as rapid-dissolve tablets, oral sprays, and nanoemulsions. Case studies indicate development timelines shrinking by over 60% when leveraging AI-augmented submission platforms and integrated clinical trial management.

This R&D velocity compresses the interval between concept validation and commercial roll-out, enabling firms to capture emerging consumer trends swiftly and reduce competitive risk. By accelerating the pipeline for patented delivery technologies, companies can achieve recurring revenue streams and create substantial entry barriers owing to intellectual property and first-mover advantages. Such efficiency gains are pivotal in realizing an upside growth pathway.

Anticipating Capacity Expansion Timelines to Meet Surge in Demand

Preparing for amplified demand requires proactive scale-up of manufacturing and supply chain infrastructure. Leading industry players are projecting capacity expansion plans that align with regulatory acceleration and market adoption forecasts, often bundling capital expenditure with digital supply chain integration for just-in-time responsiveness.

Models anticipate ramp-up periods ranging from six to eighteen months post-commissioning for new production lines dedicated to complex supplement forms. Early investment in modular and flexible manufacturing units allows rapid adjustments in output volumes and product variants, minimizing lead times. Such operational readiness ensures companies can capitalize fully on anticipated demand surges without excessive stock-outs or margin erosions.

The synchronization of capacity expansion with market signals reduces risk and underpins sustained growth in the upside scenario.

Regulatory and Policy Catalysts Accelerating Adoption Dynamics

Favorable shifts in regulatory environments, including faster approval pathways for botanicals and functional ingredients, incorporation of real-world evidence frameworks, and expansion of label claim flexibility collectively enhance market receptivity. Additionally, government-backed health promotion initiatives focused on aging populations and musculoskeletal wellness provide indirect but significant demand support.

Policy trends toward standardization and harmonization across major markets further diminish entry barriers and reduce time-to-revenue for innovative formulations. These catalysts contribute to increased consumer trust and insurer acceptance, fostering wider penetration of premium, clinically supported bone and joint health supplements.

In tandem, these developments elevate the market’s growth ceiling beyond conservative projections.

Together, these factors define a coherent and evidence-supported narrative for the market's upside potential. They provide actionable insights into how strategic prioritization of regulatory engagement, digital marketing evolution, focused R&D acceleration, and agile capacity planning can unlock revenue growth that exceeds baseline estimates. The following sections will consider how these opportunities compare and contrast with downside risks, setting the stage for balanced scenario planning.

Navigating Regulatory Challenges and Consumer Scrutiny: Downside Scenario Risks and Strategic Adaptations to Market Contraction

This subsection analyzes the potential adverse trajectories for the global bone and joint health supplements market if regulatory pressures intensify and consumer backlash against certain ingredients escalates. By quantifying the scope of market growth slowdown, identifying vulnerable product formulations, projecting financial and operational impacts, and outlining workforce implications, this analysis arms stakeholders with actionable insights needed to mitigate downside risks and optimize portfolio resilience through 2033.

Quantifying Market Growth Deceleration Under Ingredient Restriction Scenarios

Emerging regulatory constraints and safety concerns related to specific excipients and controversial ingredients pose significant risks that could decelerate market growth to a low-single-digit compound annual growth rate through 2033. Scenario modelling projects a contraction of the projected CAGR from the baseline 7%-8% range down to approximately 3%-5%, driven by ingredient bans, more stringent approval pathways, and heightened compliance costs. This deceleration is expected to materially restrain revenue expansion, compress industry cash flows, and constrain reinvestment capacity for innovation or marketing initiatives across major regional markets.

Slower growth trajectories would demand rigorous reassessment of capital allocation priorities, emphasizing conservative portfolio management and cost containment. Suppliers focused heavily on legacy formulations dependent on banned excipients may see disproportionate revenue erosion, triggering a recalibration of product pipelines and market entry strategies.

Identifying and Phasing Out Controversial Excipients and Ingredients by 2033

Certain pharmaceutical and supplement excipients have attracted regulatory scrutiny due to potential adverse effects, allergic sensitivities, or emerging toxicological evidence. Ingredients including specific synthetic colorants, preservatives, solvents such as benzyl alcohol, and excipients with diethylene glycol contamination histories are forecasted to be progressively phased out or restricted by regulators globally. The mandatory disclosure and certification processes for excipient safety will increase, raising the operational burden on manufacturers.

By 2033, industry consolidation around clean-label criteria and safer excipient sourcing is anticipated, compelling formulators to invest in alternative bio-based, inert, or plant-derived excipients. Retiring excipients associated with allergy-triggering or toxicity concerns will form a regulatory baseline to avoid consumer backlash and reputational damage, thus redefining formulation standards and supplier qualification protocols.

Strategic Resource Reallocation Toward Lower-Scrutiny Categories and Non-Nutrient Adjacent Spaces

With heightened ingredient-level regulatory scrutiny, companies will need to strategically redeploy resources from vulnerable segments toward less regulated or emerging adjacent categories. This includes increased investment in plant-based nutraceuticals, functional beverages, and precision nutrition offerings that sidestep conventional excipient controversies. Non-nutrient functional ingredients with lower inspection risk or consumer sensitivity provide alternative growth avenues.

Portfolio realignment may entail divesting or reformulating bone and joint products containing flagged excipients while bolstering innovation in complementary health areas such as inflammation management, mobility enhancement, or synergistic supplements with omega-3 or collagen peptides. This approach will help preserve revenue stability and maintain market share despite growing regulatory complexity.

Workforce Restructuring Implications and Implementation Timelines Amid Market Contraction

Anticipated regulatory headwinds and market contraction would necessitate significant organizational adjustments, especially for companies overexposed to product lines requiring reformulation or facing declining consumer acceptance. Workforce reductions are projected to align with the degree of resource withdrawal from affected product categories, estimated at downsizing between 10%-20% of related R&D, production, and marketing staff over a 3-5 year horizon post regulatory enforcement intensification.

A phased approach to human capital management is critical to maintaining core competencies while reducing fixed costs. Proactive retraining, redeployment into emerging product verticals, and transparent communication strategies will mitigate morale decline and preserve institutional knowledge critical for transition success. Workforce planning must incorporate scenario-based contingencies aligned with regulatory timelines and market reactivity.

Modeling Financial Impact and Strategic Risk Management in Ingredient Ban Scenarios

Revenue erosion driven by ingredient bans and associated reformulation costs can lead to significant margin compression. Financial modelling indicates that ingredient restriction scenarios may reduce EBITDA margins by 3 to 8 percentage points, triggered by higher costs for alternative excipients, compliance expenditures, and decreased sales volumes from reformulated products with diminished consumer appeal.

Capital-intensive investments will be necessary for clinical validation, safety certifications, and supply chain transparency enhancements. These expenditures require preemptive strategic planning to preserve liquidity and avoid disruption. Firms must implement rigorous portfolio risk assessments, adopting flexible product launch timelines and diversified supply sources to cushion against regulatory shocks.

Mitigation strategies include enhanced consumer education initiatives and proactive engagement with regulators to shape feasible compliance pathways that balance safety with innovation continuity.

Given these downside risks, companies must adopt agile portfolio management, prioritize reformulation research, and develop robust compliance capabilities. These efforts will underpin resilience in a tightening regulatory landscape and sustain long-term growth opportunities amid evolving consumer expectations.

5. Action Blueprint: Prioritized Initiatives for Stakeholder Alignment Through 2033

Short-Term Plays (2026-2028): Concrete Foundations for Accelerated Market Entry and Early Wins

This subsection distills actionable, near-term initiatives aligned with strategic imperatives for the 2026-2028 horizon. It focuses on quantifiable targets and pilot implementations designed to generate measurable outcomes, validate technological innovations such as blockchain, and forge ecosystem partnerships. These foundational efforts aim to secure immediate revenue growth and operational efficiencies that underpin scalable expansion into the next phase of market penetration.

Quantifying Target SKU Extension Sales and Regional Priorities for Immediate Revenue Impact

Launching three strategically chosen SKU extensions in the fastest-growing regional markets is paramount for securing early revenue traction. North America continues to offer stable volumetric returns, particularly driven by aging demographics and premiumization trends, while Asia-Pacific’s accelerated CAGR exceeding 8% necessitates prioritized SKU introductions tailored to local regulatory contexts and consumer preferences. Projected sales for these SKU extensions should be benchmarked against regional market penetration rates, with initial targets reflecting 5-10% incremental share capture within the product category by 2028. This approach ensures focused resource allocation toward markets exhibiting robust demand signals and infrastructure readiness, balancing near-term payback with long-term brand equity building.

Assessing Blockchain Traceability Pilot ROI and Scalability Metrics for Supply Chain Transparency

Implementing blockchain technology for ingredient traceability offers dual value: enhancing consumer trust through immutable data records and optimizing internal supply chain efficiencies via real-time visibility. Early pilots demonstrate potential ROI through a 40% reduction in supply chain waste and up to 70% clearance time acceleration in quality audits, with associated cost savings projected at 15-20% of total ingredient procurement expenses. Scalability metrics should include node onboarding rates, transaction throughput exceeding industry-standard latency thresholds (<2 seconds), and successful integration with legacy ERP systems. These pilots must also be assessed for adaptability across diverse geographies and regulatory regimes to warrant full-scale rollout by 2028.

Projecting User Engagement and Brand Reach via Strategic Alliance with Fitness App Ecosystem

Forming strategic partnerships with established fitness app platforms provides a high-leverage channel for co-branded product bundles and tailored consumer experiences. Engagement projections should utilize platform user demographics, with the intent to capture 3-5% of active users within 12 months post-launch as direct supplement purchasers or subscribers. The alliance’s impact extends beyond direct sales, encompassing increased brand awareness through in-app notifications, personalized coaching integrations, and AI-driven behavioral nudges that enhance supplement adherence. Effective tracking of key performance indicators such as daily active users interacting with supplement content and subscription conversion rates will substantiate ROI and inform iterative marketing strategies.

Evaluating Enrollment and Clinical Milestones from Phase III Botanical Supplement Trials

Phase III trials for promising botanical candidates have enrolled approximately 1,000 eligible patients out of an initial 6,700 sign-ups, reflecting rigorous screening consistent with FDA protocols. Trial enrollment velocity and retention rates are critical predictors of timely market authorization. Early efficacy data and safety profiles will significantly influence go/no-go decisions for commercialization readiness within 2028. These results will shape the product development pipeline, inform regulatory submission strategies, and provide the basis for marketing claims substantiation. Ongoing data transparency and collaboration with manufacturing partners facilitate optimized scale-up planning concurrent with clinical progress.

With short-term foundational initiatives well-charted, success in these areas enables the seamless transition into mid-term scaling ambitions focused on technological integration, geographic expansion, and value differentiation.

Mid-Term Ambitions (2029-2031): Scaling with AI, Biotech Integration, and APAC Market Expansion

This subsection outlines strategic initiatives critical to transitioning from foundational achievements to broader market influence. It details operational finesse through AI integration, expanding biotech capabilities via targeted acquisitions, entering dynamic Asia-Pacific markets with calibrated regulatory approaches, and elevating quality standards using globally recognized certifications. Collectively, these priorities will differentiate stakeholders and position them for sustainable growth amid intensifying competition and evolving consumer expectations.

Comprehensive AI Recommendation Engine Deployment: Enhancing Customer Engagement and Personalization

Between 2029 and 2031, deploying an AI-driven recommendation engine across all customer touchpoints will be pivotal in elevating personalized nutrition experiences. This system should analyze comprehensive consumer data—from purchase history to health biomarkers—enabling dynamic product suggestions that align with individual bone and joint health needs. Operational scope must encompass e-commerce platforms, retail kiosks, mobile apps, and integration with emerging digital health ecosystems, including wearables and health trackers.

The expected outcomes include increased customer lifetime value through superior engagement, higher conversion rates driven by relevant up-sell and cross-sell opportunities, and reduced churn via predictive retention insights. ROI can be maximized by iterative machine learning optimization, leveraging open data standards for seamless interoperability, and close collaboration with regulatory teams to ensure data privacy compliance. Clear success metrics should track customer satisfaction indices, incremental revenue per user, and system uptime to ensure reliability.

Strategic Biotech Acquisition: Capabilities and Synergies for Biomarker Testing Expansion

Acquisition targets should be midsize biotech firms specializing in biomarker analytics, with annual revenues between $50 million and $150 million and established clinical validation portfolios. The strategic rationale focuses on integrating advanced testing capabilities to enhance product personalization and efficacy claims in bone and joint health supplements. This integration will facilitate evidence-based supplementation plans, potentially incorporating genomic and metabolomic indicators to fine-tune formulations.

Post-acquisition, a phased integration plan must be followed to harmonize R&D workflows, unify data management infrastructure, and preserve critical talent. Synergistic benefits include accelerated product innovation cycles, increased regulatory competitiveness, and expanded access to clinical trial networks. Financial diligence should verify recurring revenue stability, intellectual property robustness, and regulatory compliance history to mitigate integration risks.

Targeted Entry into New Asia-Pacific Markets: Regulatory Timelines and Market Adaptation