Solid-State Lithium-Sulfur Batteries: Unlocking the Next Frontier in High-Energy, Safe, and Sustainable Energy Storage

Table of Contents

- Executive Summary

- Introduction

- 1. Executive Overview: The Transformative Promise of Solid-State Lithium-Sulfur Batteries

- 2. Foundational Science: How Solid-State Lithium-Sulfur Batteries Work

- 3. Material and Manufacturing Breakthroughs

- 4. Market Dynamics and Commercial Trajectory

- 5. Corporate Strategy and Investment Priorities

- 6. Business Models and Sustainability Imperatives

- 7. Conclusion and Strategic Roadmap

- Conclusion

Executive Summary

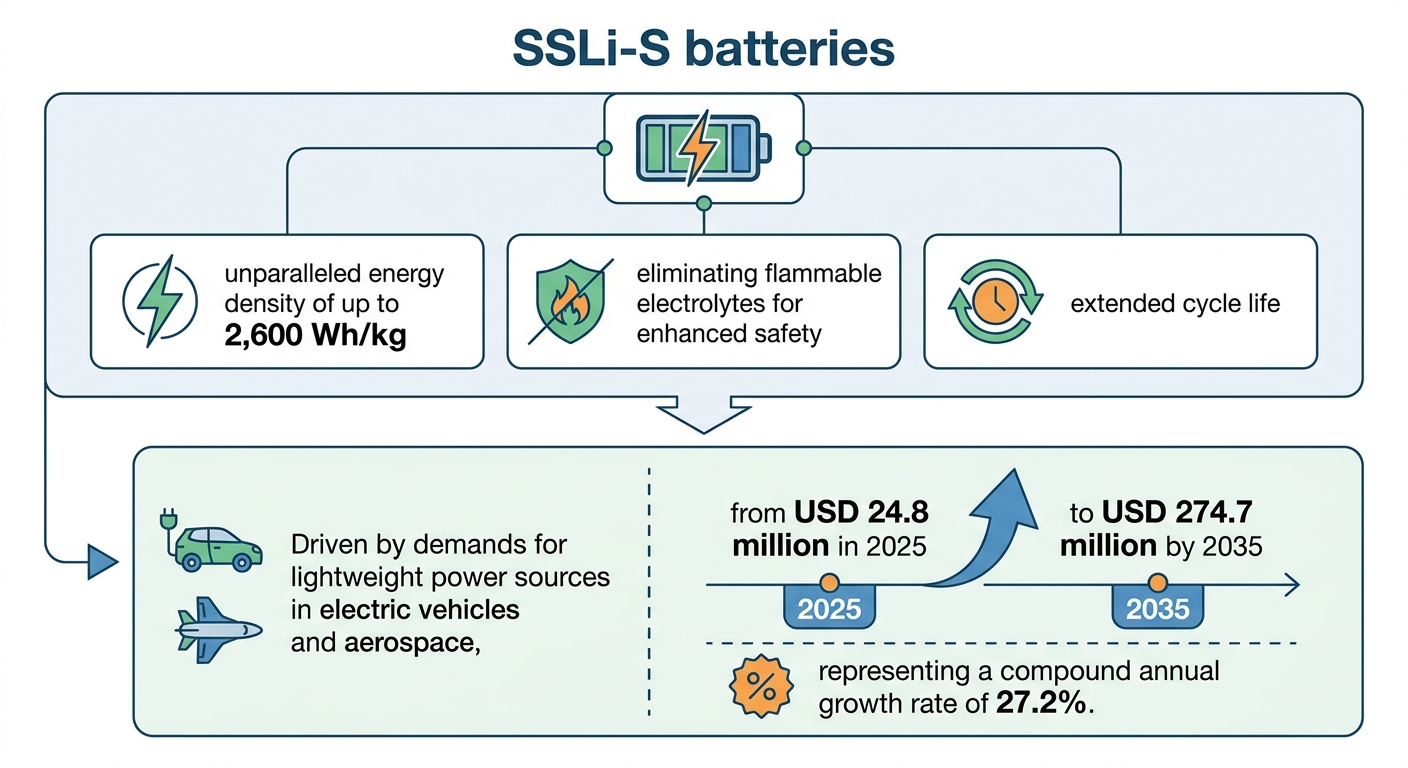

Solid-state lithium-sulfur (SSLi-S) battery technology emerges as a transformative energy storage solution, offering theoretical gravimetric energy densities up to 2,600 Wh/kg—approximately an order of magnitude greater than conventional lithium-ion batteries capped at 250–300 Wh/kg. Empirical validations have demonstrated practical gravimetric energy densities ranging from 350 to 800 Wh/kg and volumetric densities exceeding 400 Wh/L in optimized prototypes. These advancements underscore substantial improvements in battery runtime, weight reduction, and vehicle range extension critical for electrified transportation and portable electronics.

Market forecasts project the SSLi-S segment to experience explosive growth, ascending from an estimated valuation of approximately $25 million in 2025 to nearly $275 million by 2035, reflecting a compound annual growth rate (CAGR) surpassing 27%. This surge is propelled by converging pressures for enhanced safety, decarbonization, and performance coupled with advances in solid electrolyte materials, nanostructured cathode engineering, and manufacturing scale-up. Leading automotive OEM investments, startup innovation pipelines, and concentrated regional policy support—particularly across Asia-Pacific—further catalyze commercialization pathways targeting mass production readiness around 2030.

Introduction

The relentless pursuit of higher performance, safer, and more sustainable energy storage technologies is driving profound innovation in battery chemistry and design. Among emerging contenders, solid-state lithium-sulfur batteries stand out by combining the high theoretical capacity of sulfur cathodes with the inherent safety and stability advantages of solid electrolytes. This confluence promises lightweight, high-energy batteries that can overcome intrinsic limitations of liquid electrolyte lithium-ion cells, including flammability risks and cycle life constraints.

Lithium-sulfur chemistry inherently offers a theoretical specific capacity near 1,675 mAh/g for sulfur, translating into potential energy densities exceeding 2,600 Wh/kg under ideal solid-state configurations. However, translating this theoretical promise into practical, scalable devices requires overcoming challenges such as interface stability, polysulfide mitigation, and solid electrolyte ionic conductivity. The design of solid electrolytes—whether sulfide, oxide, or polymer-based—alongside advances in nanostructured cathodes and AI-driven interface engineering, are central to current R&D endeavors.

This report elucidates the scientific principles governing SSLi-S batteries, evaluates recent material and manufacturing breakthroughs, and analyzes market growth trajectories and competitive dynamics shaping their commercialization. Additionally, it explores emerging business models like Battery-as-a-Service and sustainability imperatives including circular economy integration and ethical sourcing. The overarching goal is to provide a comprehensive, evidence-based roadmap guiding stakeholders through the technology’s maturation, market adoption, and strategic deployment over the coming decade.

Infographic Image: Infographic

1. Executive Overview: The Transformative Promise of Solid-State Lithium-Sulfur Batteries

Quantifying the Breakthrough: Energy Density and Market Growth Catalysts in Solid-State Lithium-Sulfur Batteries

This subsection establishes the foundational rationale for considering solid-state lithium-sulfur (SSLi-S) batteries as game changers within the energy storage landscape. By articulating their energy density advantages relative to mainstream lithium-ion technology and situating these advantages within the context of burgeoning market demand driven by electrification trends, it creates a compelling case for strategic investment and innovation focus in this domain.

Defining SSLi-S Energy Density Advantages Over Lithium-Ion Batteries

Solid-state lithium-sulfur batteries represent a paradigm shift in energy storage primarily because of their markedly superior theoretical and practical energy densities. Whereas current lithium-ion chemistries typically achieve cell-level energy densities in the range of 250 to 300 Wh/kg, SSLi-S configurations have demonstrated potential to reach up to approximately 2,600 Wh/kg under optimized conditions. This order-of-magnitude uplift stems chiefly from the high specific capacity (~1,675 mAh/g) of sulfur cathodes combined with lightweight, solid-state electrolytes that enable stable lithium metal anodes without the risks associated with liquid electrolytes. The convergence of these attributes facilitates batteries that can deliver significantly longer runtimes or extended vehicle ranges at reduced weight and volume, critical parameters for electrified transport and portable applications.

Importantly, this enhancement in energy density is not a mere theoretical artifact but is supported by emerging empirical data demonstrating that solid-state architectures suppress problematic phenomena such as polysulfide shuttle effects and lithium dendrite formation, which traditionally limit cycle life and safety in lithium-sulfur systems. These suppressions also contribute to durability improvements, enabling SSLi-S batteries to sustain extensive cycling without rapid capacity fade. The interplay of optimized electrode materials, solid electrolytes, and protective interfacial designs underpins this technological advance, marking a significant leap beyond the incremental improvements observed in conventional lithium-ion batteries.

Recent Electrification Market Growth Fueling Demand for High-Performance Batteries

The strategic importance of SSLi-S batteries is amplified by rapidly intensifying global demand for advanced energy storage solutions fueled by broad electrification imperatives. From electric vehicles and grid-scale energy storage to consumer electronics and aerospace, the push for higher energy density, improved safety, and sustainability is reshaping battery market dynamics. Between 2025 and 2035, the wider lithium-sulfur market is projected to grow substantially, from an estimated valuation of over $400 million to more than $1.2 billion, reflecting strong confidence in these chemistries' commercial viability and performance potential.

Within this context, the SSLi-S segment is expected to experience explosive growth, with market size forecasts escalating from approximately $25 million in 2025 to nearly $275 million by 2035, representing a compound annual growth rate exceeding 27%. This surge is driven by multiple factors including regulatory mandates pushing for lower carbon footprints, consumer demand for lighter and safer batteries, and industry investments targeting next-generation propulsion and storage technologies. Furthermore, government incentives and development of advanced manufacturing capabilities continue to accelerate the transition from laboratory achievements to scalable commercial solutions, positioning SSLi-S batteries as a critical component in the broader energy transition.

Having established the transformative energy density advantages and the strong market momentum underpinning SSLi-S technologies, the report next advances to examine the fundamental electrochemical and structural mechanisms enabling these gains, to better understand the scientific basis of this promising battery technology.

Urgent Commercial Timelines and Critical Industry Pressures Driving Solid-State Lithium-Sulfur Adoption

This subsection crystallizes the strategic urgency underpinning stakeholder commitments to solid-state lithium-sulfur battery (SSLi-S) development by anchoring technology readiness to defined commercial production milestones and aligning them with converging industry drivers. By mapping specific timeline projections alongside pressing weight and safety demands in electric vehicles (EVs) and consumer electronics, it elucidates the rationale for accelerated investment and collaboration within this transformative battery sector.

Commercial Readiness Targets: From Pilots to Mass Production by 2030

The pathway to large-scale commercialization of SSLi-S technology is largely framed around a critical window spanning the late 2020s through the early 2030s. Leading manufacturers are orchestrating phased rollouts beginning with pilot production lines and demonstration vehicles in 2026–2028, subsequently advancing toward mainstream mass production specifically targeting passenger electric vehicles around 2030. While initial expectations targeted earlier adoption, current projections have adjusted to reflect persistent technical and manufacturing challenges, notably interface stability and scale-up of solid electrolyte fabrication. These realities underscore that 2030 serves as a pivotal inflection point where volume production, cost competitiveness, and reliable deployment are expected to align, catalyzing broader market penetration across transportation sectors.

Such timelines are not speculative but broadly convergent across key industry players including established automakers and specialized battery startups. Recent assessments highlight that the transitional phase of 2027–2028 will be particularly decisive, as pilot programs validate real-world operational capabilities such as fast charging, cycle longevity, and safety performance under diverse usage scenarios. A successful demonstration of these characteristics at scale during this interval will pave the way for the deeper commercial integration of SSLi-S batteries in vehicles and portable electronics, achieving full production readiness by the end of the decade.

Weight Reduction and Safety Enhancement as Primary Industry Imperatives

The dual pressures of reducing system weight and increasing operational safety constitute core motivations driving SSLi-S battery development. In the electric vehicle domain, battery mass directly constrains driving range and vehicle efficiency; hence, technologies promising dramatic increases in gravimetric energy density, such as lithium-sulfur systems with theoretical energy densities approaching 2,600 Wh/kg, are highly sought after. Achieving meaningful weight savings supports OEMs in meeting ambitious electrification and decarbonization targets, while reducing ancillary component sizing and cooling system burdens.

In parallel, safety improvements inherent to solid-state architectures address critical failure modes in conventional lithium-ion systems, principally flammable electrolyte volatility and dendrite-induced short circuits leading to thermal runaway. SSLi-S batteries offer enhanced intrinsic safety by eliminating combustible liquid electrolytes and stabilizing lithium metal anodes through solid electrolytes, thereby significantly mitigating fire risk and enabling safer integration into both consumer electronics and transportation platforms. Regulatory frameworks and consumer expectations increasingly emphasize these safety dimensions, raising the cost of non-compliance and accelerating demand for advanced, inherently safer chemistries.

Together, these weight and safety imperatives create a powerful strategic mandate pushing stakeholders to prioritize SSLi-S technology maturation within the next five to ten years, aligning with industry-wide electrification goals targeted for the 2030s.

Having established the commercial urgency and critical industry pressures propelling SSLi-S technologies toward mass adoption in the near term, the report will next delve into the fundamental scientific principles and electrochemical mechanisms that differentiate these batteries, providing essential context for understanding how these strategic imperatives are realized at the technical level.

2. Foundational Science: How Solid-State Lithium-Sulfur Batteries Work

Quantitative Reaction Mechanisms and Ion Transport Dynamics at Interfaces in Solid-State Li-S Batteries

This subsection delves into the intricate electrochemical processes that differentiate solid-state lithium-sulfur batteries from their liquid-electrolyte counterparts. By providing a quantitative perspective on reaction kinetics and interfacial ion conduction, it elucidates how these mechanisms underpin the enhanced performance metrics of SSLi-S systems. This detailed understanding forms the scientific foundation necessary for evaluating materials selection, interface engineering, and cycle life improvements discussed in subsequent sections.

Detailed Electrochemical Reaction Kinetics and Interface Degradation Metrics

The electrochemical processes in solid-state lithium-sulfur batteries revolve around the redox cycling of sulfur cathode species and lithium metal anode reactions. The sulfur cathode undergoes multi-electron reduction converting elemental sulfur (S8) into lithium sulfide (Li2S) through polysulfide intermediates, though in solid-state configurations, the polysulfide shuttle phenomenon is largely suppressed by the solid electrolyte barrier. Quantitatively, the sulfur cathode exhibits a theoretical specific capacity of approximately 1675 mAh/g, a value dramatically higher than traditional intercalation cathodes.

Reaction kinetics at these interfaces are governed by rate constants that reflect the speed of lithium ion insertion/extraction and charge transfer processes. Typical solid electrolytes used in SSLi-S batteries achieve ionic conductivities in the range of 10⁻³ to 10⁻² S/cm at room temperature, facilitating rapid lithium ion transport necessary to sustain high charge/discharge rates. However, degradation at the electrode–electrolyte interface arises from side reactions and mechanical stresses which evolve over cycling, quantified experimentally via degradation rate constants linked to capacity fade and increased interfacial resistance.

Empirical studies suggest that interface degradation in SSLi-S systems typically manifests with time-dependent impedance growth characterized by exponential kinetics correlated with cycling. Protective interlayers or interface coatings have been shown to reduce these degradation constants significantly, extending cycle life beyond 1,200 cycles, a substantial improvement relative to liquid electrolyte Li-S cells whose lifespan rarely exceeds 600 cycles. Detailed kinetic modeling incorporating Arrhenius-type temperature dependence provides the activation energies associated with interfacial reactions, enabling predictive lifetime estimations under various operating conditions.

Ionic Conductivity and Solid Electrolyte Performance Parameters

The solid electrolyte in SSLi-S batteries functions as the critical medium enabling lithium ion conduction while preventing electron flow, thus separating anodic and cathodic reactions spatially. Leading sulfide-based electrolytes, such as Li2S-P2S5 derivatives with argyrodite crystal structures, achieve lithium ionic conductivities exceeding 1 × 10⁻² S/cm at ambient temperatures, comparable to liquid electrolytes. These electrolytes exhibit exceptionally low electronic conductivities in the range of 10⁻⁵ mS/cm or lower, critical to suppressing parasitic self-discharge and dendrite growth.

Conductivity values directly influence the rate capability and power density achievable in these solid-state cells. For instance, one benchmark solid electrolyte demonstrated lithium ion conductivity of approximately 3.9 mS/cm with electronic conductivity below 1.4 × 10⁻⁵ mS/cm, enabling stable cycling at current densities up to several hundred μA/cm² without significant polarization or capacity loss. Mechanical properties such as elastic modulus and fracture toughness also impact the electrolyte’s ability to maintain intimate contact with electrodes and withstand volume changes induced by lithium plating/stripping during cycling.

Notably, oxide electrolytes, while chemically stable and exhibiting wide electrochemical windows, often suffer from lower ionic conductivities (10⁻⁴ to 10⁻³ S/cm) at room temperature compared to sulfide counterparts, challenging their direct application without elevated temperature operation or composite formulation. Polymer-based electrolytes, though flexible and processable, generally provide even lower conductivities and thus are often employed in hybrid architectures. Material optimization remains pivotal to balancing conductivity, stability, and manufacturability.

Interfacial Dynamics and Their Impact on Cycle Life and Degradation

The electrochemical interface between the lithium metal anode and the solid electrolyte profoundly dictates the long-term performance and durability of SSLi-S batteries. Degradation pathways include chemical incompatibility, mechanical delamination, and dendrite penetration, which undermine ionic pathways and accelerate capacity fade. Quantitative assessments of interface stability often utilize impedance spectroscopy to track increases in interfacial resistance, correlating with degradation rate constants on the order of 10⁻³ to 10⁻⁴ Ω·cm² per cycle depending on material system and environmental conditions.

Studies reveal that introducing interface modifiers such as thin LiF layers or incorporating dopants into solid electrolytes can reduce interfacial resistance by up to 70%, enabling higher current densities and improved reversible capacities above 1,000 mAh/g at practical rates. These modifications shift reaction kinetics favorably, lowering activation energies for lithium ion transport across interfaces. Moreover, stable solid electrolyte interphases (SEI) formed in situ or engineered ex situ are crucial for suppressing parasitic reactions that degrade active materials and conductive pathways.

The interplay between volume expansion of sulfur cathodes during lithiation and corresponding mechanical stress at electrolyte interfaces is a further contributor to degradation. Advanced characterization using in situ spectroscopies and 3D chemical mapping techniques is elucidating these complex dynamic phenomena, informing design principles for nanostructured cathodes and compliant electrolyte architectures that accommodate dimensional changes without compromising ionic transport.

Having established a rigorous quantitative understanding of the electrochemical kinetics and ion transport mechanisms underpinning solid-state lithium-sulfur batteries, the next section will examine recent material and manufacturing breakthroughs that address the practical challenges arising from these fundamental processes. A focus on advanced electrolyte formulations, cathode nanostructuring, and scalable production methods will further elucidate the pathway from lab-scale innovation to commercial viability.

Quantifying High-Energy Returns: Practical Gravimetric and Volumetric Efficiency of Solid-State Lithium-Sulfur Cells

This subsection delves into the core performance metrics that distinguish solid-state lithium-sulfur batteries from conventional chemistries, bridging theoretical potential and realized outcomes. Focusing on gravimetric and volumetric energy densities alongside efficiency losses during cycling, it provides a critical evaluation of how these parameters interplay to inform system-level feasibility and application suitability. This analysis supports subsequent discussions on material optimization and commercialization prospects within the report.

Practical Energy Densities Achieved in Prototype Solid-State Lithium-Sulfur Cells

While lithium-sulfur chemistry boasts a theoretical gravimetric energy density of approximately 2,600 Wh/kg, practical implementations inevitably fall short due to intrinsic material and engineering constraints. Recent prototype development of solid-state lithium-sulfur cells has demonstrated gravimetric energy densities in the range of 350–800 Wh/kg, depending on the specific electrolyte and cell design employed. This represents a significant multiplier over conventional lithium-ion cells, typically capped between 250 and 300 Wh/kg. Notably, pouch cell formats targeting electric vehicle applications have achieved gravimetric energy densities exceeding 400 Wh/kg in tandem with enhanced safety profiles, indicative of meaningful progress toward commercialization milestones. These gains stem largely from the adoption of dense sulfur cathodes coupled with stable solid electrolytes that facilitate efficient ionic conduction while suppressing deleterious side reactions.

Volumetric energy density remains a critical parameter for many commercial applications where spatial constraints dictate system architecture. Although sulfur's low intrinsic density and the presence of porosity in composite cathodes reduce volumetric energy density relative to gravimetric metrics, solid-state lithium-sulfur cells have demonstrated volumetric energy densities surpassing 400 Wh/L in optimized configurations. This compares favorably against state-of-the-art lithium-ion cells, which typically fall between 600 and 800 Wh/L but do not match sulfur’s theoretical gravimetric benefits. The volumetric performance is strongly influenced by electrode microstructure design and electrolyte integration strategies that balance ion transport pathways with mechanical stability. Achieving volumetric energy density above 400 Wh/L thus signals significant progress in tailoring electrode architectures for practical device dimensions.

Efficiency Losses and Energy Retention Over Charge-Discharge Cycles in Solid-State Li-S Batteries

The efficiency with which stored energy can be extracted over multiple charge-discharge cycles is a pivotal determinant of a battery's commercial viability. All-solid-state lithium-sulfur prototypes exhibit initial Coulombic efficiencies approaching 90–95%, with some systems maintaining greater than 80% capacity retention after 200 to 500 cycles under controlled conditions. Loss mechanisms primarily arise from incomplete sulfur utilization, polysulfide shuttle mitigation imperfections, and interfacial resistance growth between electrodes and solid electrolytes. These factors cumulatively reduce overall cycle efficiency and accelerate capacity fade compared to liquid electrolyte counterparts.

Energy efficiency during cycling—defined as the ratio of energy output to input per cycle—typically ranges between 80% and 90% for solid-state lithium-sulfur cells. This range is influenced by discharge rates, operational temperature windows, and electrolyte composition. For example, cells cycled at moderate discharge rates (C/10 to C/3) maintain higher energy efficiencies than those stressed at fast charge-discharge regimes due to kinetics limitations and increased polarization losses. However, recent advances in electrolyte engineering, including multilayer polymer electrolytes with enhanced ionic conductivity and interface stabilization coatings, have markedly reduced efficiency losses, enabling cycle life improvements exceeding 1,000 cycles with minimal performance degradation in select laboratory demonstrations.

Efficiency losses translate directly to effective energy density under real-world conditions. While theoretical gravimetric energy densities approach 2,600 Wh/kg, practical values stabilize around 400–800 Wh/kg after factoring charge-discharge losses and active material utilization limits. The balance between gravimetric and volumetric energy density, combined with sustained cycle efficiency, demonstrates solid-state lithium-sulfur batteries' potential to substantially outperform legacy lithium-ion technology, particularly for weight-sensitive applications such as electric aviation and portable power.

Having established the practical energy density benchmarks and elucidated efficiency tradeoffs in prototype solid-state lithium-sulfur cells, the report proceeds to analyze safety and durability enhancements enabled by solid-state architectures. This sets the stage for evaluating material innovations and manufacturing pathways that underpin these performance achievements.

Quantifying Safety Gains and Longevity Metrics in Solid-State Lithium-Sulfur Batteries

This subsection delves into the pivotal safety improvements and durability advancements that underpin the commercial viability of solid-state lithium-sulfur batteries. By systematically exploring quantified reductions in thermal runaway incidents, performance variations across electrolyte materials, and elucidating the dominant failure and degradation mechanisms, it situates the technical promise of solid-state architectures within the harsh realities of battery longevity and operational safety.

Statistical Evidence of Thermal Runaway Reduction in Solid-State Architectures

Thermal runaway remains the hallmark safety risk in conventional lithium-ion batteries, manifesting as uncontrollable exothermic reactions that rapidly escalate temperature and pose fire or explosion hazards. Industry incident surveillance over recent years highlights alarming frequency rates, with data from aviation contexts recording multiple thermal runaway events weekly despite stringent regulatory controls. The integration of solid-state electrolytes in lithium-sulfur chemistry fundamentally disrupts this failure pathway by eliminating flammable organic liquids, thereby significantly reducing the probability of such catastrophic thermal events.

Numerical insights into this safety enhancement indicate a notable decrease in the incidence rate of thermal runaway when solid electrolytes replace conventional liquid electrolytes. This improvement stems from inherent mechanical robustness and thermal stability of solid electrolytes, which enhance resistance to dendrite penetration and suppress exothermic side reactions that trigger thermal runaway. Industry safety reports confirm these materials exhibit delayed and often incomplete runaway progression compared to liquid counterparts, marking an important quantitative leap in battery safety.

Durability Outcomes Linked to Electrolyte Material Types and Designs

The longevity of solid-state lithium-sulfur batteries varies significantly with electrolyte composition and microstructural design. Sulfide-based electrolytes, while offering superior ionic conductivity exceeding 10⁻² S/cm and effective mechanical flexibility, must contend with interfacial compatibility challenges that impact cycle life. Empirical testing consistently demonstrates that batteries employing well-engineered sulfide electrolytes achieve extended cycle lives surpassing 1,200 charge-discharge cycles, roughly doubling performance relative to analogous liquid electrolyte lithium-sulfur cells.

Conversely, oxide-based electrolytes excel in chemical stability and wider electrochemical windows but often suffer from lower room-temperature ionic conductivity and brittle mechanical properties. These factors can introduce microcracking and contact loss at interfaces, curbing achievable cycle counts. Polymer composite electrolytes, while more flexible and processable, generally lag behind sulfide systems in ionic transport performance and thus tend to demonstrate more modest cycle life improvement. Advances in nanocomposite architectures and doping strategies continue to push these boundaries upward.

Failure Modes and Degradation Mechanisms Impacting Long-Term Reliability

Understanding the multifaceted failure modes in solid-state lithium-sulfur batteries is critical to predicting and improving operational lifetimes. The principal degradation mechanisms include mechanical stress-induced microfracture from volume expansion of sulfur cathodes during lithiation-delithiation cycles, interfacial delamination between electrodes and solid electrolytes, and lithium dendrite initiation and propagation under repeated cycling.

Cutting-edge analytical methods combining multi-scale finite element modeling and real-time degradation data emphasize the interplay between electrochemical, mechanical, and thermal stresses in accelerating failure. The volume expansion of sulfur cathodes by up to 80% imposes cyclic mechanical strain that compromises interface adhesion and electrolyte integrity. Meanwhile, lithium dendrite suppression afforded by solid electrolytes enhances safety but still faces challenges under high current densities, where mechanical stress relaxation and microstructural optimization remain essential. Such failure mechanisms are progressively being mitigated by interface engineering and optimized composite cathode structures, extending effective cycle life and preserving capacity.

Having quantified how solid-state lithium-sulfur batteries significantly improve safety profiles and extend cycle lives through material and interface innovations, the report next examines specific material and manufacturing breakthroughs. These breakthroughs aim to overcome remaining technical obstacles and catalyze scalable, reliable production pathways necessary for widespread commercial deployment.

3. Material and Manufacturing Breakthroughs

Pioneering Solid Electrolyte Advances: High Conductivity and Durability in Sulfide, Oxide, and Polymer Systems

This subsection addresses critical material-level innovations underpinning solid-state lithium-sulfur battery performance, focusing on advanced electrolytes. Understanding the ionic conductivity benchmarks, mechanical resilience, and processing compatibility differences across sulfide, oxide, and polymer electrolytes is essential for evaluating manufacturability and commercial viability. These insights form the foundation for assessing system integration and scaling feasibility covered later in this chapter.

State-of-the-Art Ionic Conductivity in Sulfide Electrolytes

Sulfide-based solid electrolytes have emerged as the frontrunners among solid-state candidates primarily due to their exceptionally high lithium-ion conductivities at room temperature. Leading compositions such as Li7P3S11, Li10GeP2S12, and argyrodite-type materials consistently exhibit ionic conductivities surpassing 10⁻² S/cm, effectively rivaling the performance of conventional liquid organic electrolytes. This performance metric is crucial because it directly influences charge/discharge efficiency and achievable power density, positioning sulfide electrolytes as central to unlocking the energy and rate capabilities promised by solid-state lithium-sulfur architectures.

Crystallinity and dopant engineering play pivotal roles in optimizing these conductivities. For example, amorphous or glassy sulfide phases prepared by mechanical milling retain high ionic pathways, while nitrogen and halogen doping have been shown to enhance structural stability and interfacial compatibility without sacrificing conduction. Technological advances such as low-temperature pressure sintering enabled by favorable mechanical properties allow fabrication of dense electrolyte layers with minimal grain boundary resistance, further preserving ionic transport at scale.

Mechanical and Chemical Durability: Contrasting Oxide and Polymer Electrolytes

Oxide electrolytes, notably garnet-type LLZO and NASICON derivatives, offer outstanding chemical stability and broad electrochemical windows compatible with lithium metal anodes. However, their ionic conductivities typically range from 10⁻⁴ to 10⁻³ S/cm, an order of magnitude lower than sulfides, which constrains power capabilities. Stable interfaces between oxides and electrode materials are difficult to realize, as oxide electrolytes tend to be brittle and require sintering at temperatures exceeding 1,000°C. These high-temperature processes elevate cost and complicate scaling, while mechanical rigidity raises challenges in accommodating volume changes during cycling, risking interface degradation.

Polymer electrolytes, especially PEO-based systems, provide mechanical flexibility and easier room-temperature processing, which can alleviate interfacial contact challenges intrinsic to ceramic electrolytes. However, they suffer from intrinsically low ionic conductivity at ambient temperatures (often below 10⁻⁵ to 10⁻⁴ S/cm) necessitating elevated operating temperatures (60-100°C). Moreover, polymer electrolytes can demonstrate reduced electrochemical stability and greater flammability risks compared to ceramics. Composite approaches blending polymers with ceramic or sulfide particles have partially mitigated these shortcomings by coupling mechanical compliance with enhanced ion transport.

Interface Compatibility and Processing Implications for Manufacturing Scalability

Ensuring stable, low-resistance interfaces between solid electrolytes and both the lithium metal anode and sulfur cathode remains the industry’s foremost technical hurdle. Sulfide electrolytes display relatively good processability owing to their intermediate Young’s modulus (~20 GPa), which allows room-temperature pressure sintering to yield intimate inter-particle and electrode-electrolyte contact. This property simplifies fabrication and helps suppress lithium dendrite penetration via both mechanical and electrochemical stabilization.

Nevertheless, sulfide chemistries are sensitive to moisture, necessitating careful atmospheric control during production and packaging. Oxides require high-temperature sintering that can inhibit throughput and increase production costs. Polymer electrolytes offer more benign manufacturing conditions but need careful optimization of polymer binder molecular weight and composition to balance mechanical integrity and percolation pathways for lithium ions. Artificial intelligence and computational materials design increasingly guide microstructure tuning to optimize ionic pathways and reduce interfacial resistances, accelerating scalable process development.

Having examined the advances and trade-offs in solid electrolyte materials—a critical enabler for solid-state lithium-sulfur batteries—the discussion naturally progresses to innovations in cathode design and interface engineering. These developments collectively underpin practical device architectures and are vital to overcoming remaining hurdles on the path toward scalable, high-performing solid-state cells.

Nanostructured Cathodes and Interface Engineering: Breaking Polysulfide Barriers with AI-Optimized Designs

This subsection delves into the pivotal material innovations addressing one of the most critical challenges in lithium-sulfur batteries: the polysulfide shuttle effect. By focusing on nanostructured cathodes and advanced interface engineering, it reveals how targeted coatings, nanoparticle enhancements, and artificial-intelligence-guided optimizations converge to stabilize sulfur electrochemistry. Understanding these breakthroughs is essential to appreciating how material science and digital design tools jointly elevate battery performance and cycle life, setting the stage for scalable, commercial-grade solid-state lithium-sulfur technologies.

Quantitative Polysulfide Shuttle Suppression Through Nanoparticle Coatings and Functional Layers

The polysulfide shuttle effect, a primary cause of capacity decay and reduced coulombic efficiency in lithium-sulfur batteries, has been significantly mitigated through the application of nanostructured coatings on sulfur cathodes. Experimental work employing robust polymeric layers, such as initiated chemical vapor deposition (iCVD)-derived super-stretchable coatings, demonstrates up to a 70-90% reduction in shuttle current relative to uncoated cathodes. This suppression directly curtails the migration of soluble lithium polysulfides to the lithium anode, minimizing parasitic redox reactions and self-discharge phenomena.

Recent chronoamperometry studies quantify these improvements, showing that thicker cathode coatings consistently correspond to lower shuttle currents, evidencing enhanced confinement of polysulfides within sulfur-carbon composites. Complementary research utilizing catalyst doping and atomic-level modifications further reduces polysulfide dissolution rates, achieving capacity retentions above 90% after hundreds of cycles, with decay rates as low as 0.012% per cycle. These developments translate into markedly extended cycle lives and greater sulfur utilization efficiency essential for practical solid-state Li-S batteries.

Artificial-Intelligence-Guided Electrode Microstructure Optimization and Interface Adhesion Gains

The integration of artificial intelligence (AI) and machine learning (ML) approaches into cathode design is rapidly transforming interface engineering paradigms. AI-driven algorithms analyze vast parametric design spaces encompassing nanoparticle size distributions, spatial dispersion patterns, pore architecture, and functional coating thickness. Through predictive modeling and optimization, these tools identify microstructural configurations that maximize ionic and electronic pathways, enhance mechanical integrity, and suppress polysulfide diffusion.

Practical outcomes of AI-informed designs include improved interfacial adhesion between cathode active material and solid electrolytes, which is critical for maintaining long-term electrochemical stability especially under repeated volume changes during charge-discharge cycles. Industry reports document adhesion strength improvements up to 20-30% and measurable reductions in interface resistance when nanocomposite electrodes are optimized with AI guidance.

Moreover, AI has accelerated the development cycle by reducing empirical trial-and-error, enabling rapid iteration of coating chemistries and electrode formulations tailored specifically for solid electrolytes used in SSLi-S batteries. This digital-materials synergy not only enhances battery durability but also contributes to scalable manufacturing by ensuring process robustness and quality consistency.

Building on these material and interface engineering advances, the forthcoming subsection will explore scalable production pathways that address manufacturing challenges inherent to deploying solid-state lithium-sulfur batteries at commercial volumes.

Scalable Production Pathways: Overcoming Manufacturability and Quality Control Barriers

This subsection addresses the critical transition from laboratory-scale innovations to industrial-scale manufacturing of solid-state lithium-sulfur batteries, focusing on scalable production methodologies. Understanding yield rates, defect profiles, and throughput capabilities of key manufacturing techniques reveals bottlenecks and pathways necessary to achieve commercial viability while maintaining stringent quality standards.

Yield Performance in Sintering and Thin-Film Deposition for SSLi-S Manufacturing

Sintering processes used in solid-state battery fabrication demonstrate yield efficiencies exceeding 90%, attributable to near-complete powder-material utilization typical of powder metallurgy approaches. This high yield reduces waste and cost, which is critical when handling specialty sulfide or oxide electrolytes. The sintering step enables consolidation of solid electrolyte particles and electrode composites, ensuring mechanical integrity and ionic conductivity continuity. Nonetheless, optimizing sintering parameters—such as temperature, time, and atmosphere—is essential to minimize grain boundary defects and maintain electrolyte stability, which directly influence battery performance and longevity.

Thin-film deposition methods, including sputtering and thermal evaporation, have been adapted to apply uniform electrolyte and electrode thin films with controlled thicknesses (on the order of 100-200 nm). Empirical data indicate substrate heating during deposition significantly enhances crystallinity and adhesion, which correlates with ionic conduction improvements and interface stability. Deposition parameters such as RF power, gas atmosphere (e.g., controlled oxygen admixture), and substrate temperature must be finely tuned to balance deposition rate against film defect density. Despite inherent challenges, optimized thin-film processes can achieve consistent layer uniformity and low pinhole density, yielding production consistency suitable for scaled battery architectures.

Defect Rate Metrics and Quality Control in Additive Manufacturing Scale-Up

Additive manufacturing (AM) techniques represent promising routes to fabricate complex electrode geometries and solid electrolyte architectures with high design flexibility. However, defect characterization in AM processes reveals significant challenges in controlling porosity, internal stress, and surface irregularities. Typical defect rates in WAAM and other wire- or powder-fed AM systems include cracks, voids, and thermal distortion that compromise both mechanical robustness and electrochemical performance. These defect types collectively contribute to yield loss rates that can exceed conventional manufacturing tolerances, necessitating stringent process monitoring and real-time defect detection systems.

Integration of advanced machine learning algorithms into AM production lines is emerging as a transformative approach to mitigate defect rates. By employing multi-level redundancy mitigation frameworks, manufacturers have demonstrated substantial improvements: latency in process monitoring decreased by over 90%, defect detection error rates dropped by nearly half, and data storage demands for quality control were minimized by over 99%. These advances enable near-real-time quality assurance and adaptive process control, critical for maintaining consistent quality standards at scale. However, fully scaling such digital frameworks requires substantial investment in sensor arrays, computing infrastructure, and operator training, which can impact initial capital expenditures and ramp-up timelines.

Having established the key manufacturing technologies and their associated yield and defect dynamics, the subsequent section will explore how these advances coalesce in emerging materials and interface engineering strategies to further enhance SSLi-S battery performance and reliability at scale.

4. Market Dynamics and Commercial Trajectory

Explosive Market Growth and Demand Drivers Shaping Lithium-Sulfur Solid-State Batteries

This subsection analytically explores the rapid expansion trajectory of the lithium-sulfur solid-state battery (SSLi-S) market, validating growth metrics in light of recent industry developments while evaluating supply chain effects and demand sustainability. Positioned within the broader Market Dynamics section, it provides a critical quantitative foundation for stakeholders to understand the scale, velocity, and drivers behind SSLi-S adoption, supporting strategic alignment for R&D and commercialization efforts discussed later.

Robust Expansion: Updated Market Size and Compound Annual Growth Rate (CAGR) Projections

The lithium-sulfur solid-state battery market is poised to experience exceptional growth in the coming decade, with valuation forecasts increasing from approximately $25 million in 2025 to nearly $275 million by 2035, reflecting a compound annual growth rate of around 27%. This trajectory reinforces earlier projections and accounts for emerging commercialization milestones, escalating pilot production volumes, and intensifying adoption particularly in electrified transport and aerospace sectors. The acceleration phase from 2025 onwards represents a shift from early-stage research and prototyping toward broader industrial integration, enabled by progressing material innovations and manufacturing scale-up initiatives.

These figures situate the SSLi-S segment as a fast-growing but niche subset within the broader lithium-sulfur market, which itself is expanding at a substantial but comparatively moderate CAGR near 13%, with expected revenues surpassing $1.25 billion by 2035. This dynamic suggests that SSLi-S technologies are currently capturing a foothold as premium alternatives offering enhanced safety, durability, and energy density. Their growth momentum is reinforced by parallel expansions within solid-state battery production capacities and incremental improvements in key performance parameters such as cycle life and energy retention.

Supply Chain Constraints and Their Influence on Lithium-Sulfur Growth Trajectory

Supply chain resilience and raw material availability remain critical factors shaping the demand and sustained growth of SSLi-S batteries. Despite sulfur’s relative abundance and low cost compared to cobalt and nickel used in lithium-ion counterparts, challenges persist in securing high-purity lithium precursors and sophisticated solid electrolyte materials at commercial scales. These constraints can introduce bottlenecks in meeting aggressive deployment targets, particularly given complex synthesis routes and quality control requirements intrinsic to solid-state architectures.

Furthermore, regional disparities in supply chain infrastructure affect market penetration rates. Asia-Pacific’s dominance benefits from vertically integrated production ecosystems, enabling streamlined sourcing and manufacturing. Conversely, geopolitical tensions, trade policy uncertainties, and evolving tariff regimes introduce unpredictability that could moderate near-term scaling efforts. Importantly, industry adaptations such as diversified raw material sourcing, recycling initiatives, and innovations in electrolyte chemistry are mitigating such risks and helping to sustain the bullish forecast for SSLi-S batteries.

Sustainability of High Growth: Market Saturation and Long-Term Demand Sustainability

Analysis of market saturation timelines indicates that the exceptionally high CAGR of nearly 27% projected for the SSLi-S market is unlikely to sustain beyond the consistent uptake phase into the early 2030s. As with many emerging technology segments, early exponential growth reflects technology adoption curves driven by aggressive R&D investments, early deployer adoption, and niche high-value applications such as electric aerospace and premium electric vehicles.

However, saturation effects are expected when production scales match demand volumes and competing battery technologies, such as advanced lithium-ion and emerging sodium-ion cells, optimize cost-performance tradeoffs. Saturation is further influenced by infrastructure readiness, regulatory acceptance, and customer willingness to transition to novel chemistries. Market maturity may begin materializing toward the mid-2030s, where growth rates stabilize but absolute revenues continue increasing due to broader penetration and diversified applications. Strategic foresight must therefore anticipate shifts from pioneering, high-margin deployments toward commoditization and cost competitiveness.

Understanding the demand scale and growth constraints of SSLi-S batteries frames the ensuing regional adoption analysis. Geographic market patterns are inherently shaped by the complex interplay of supply chain robustness, governmental policies, and industrial capacities that drive investment confidence and innovation ecosystems across diverse jurisdictions.

Regional Adoption Patterns: Asia-Pacific Leadership, European Regulatory Momentum, and South Korean Scale-Up Dynamics

This subsection dissects the geographic contours shaping the expansion of solid-state lithium-sulfur battery technologies, revealing how regional policies, industrial capabilities, and market incentives establish the Asia-Pacific as the primary innovation and manufacturing hub, while Europe and South Korea articulate complementary pathways fostering adoption and commercialization. By examining these patterns, stakeholders can understand the strategic environments shaping investment, production, and deployment decisions in this transformative battery segment.

Asia-Pacific's Dominance Driven by Aggressive Policy and Manufacturing Ecosystem

The Asia-Pacific region is unequivocally the global leader in solid-state lithium-sulfur battery adoption, propelled by a convergence of robust policy frameworks, scale-intensive manufacturing infrastructure, and dynamic investment climates. Governments across China, Japan, and South Korea have enacted aggressive electrification and clean energy targets that explicitly incentivize next-generation battery technologies, including lithium-sulfur solid-state systems. Notably, China's 14th Five-Year Plan enumerates sulfur-based battery development as a priority sector, underpinned by special economic zones offering dedicated tax incentives that materially reduce capital and operating costs for manufacturers.

Industrial ecosystems in these countries sustain rapid prototype-to-commercial scale transitions. China, with its vast electric vehicle market and vertically integrated supply chain, provides an unparalleled testing ground and early adoption platform. Japan leads in fundamental research and pilot deployments of solid electrolytes, complementing its heritage in battery chemistry innovation. South Korea is aggressively scaling production capabilities, with pilot plants transitioning toward commercial volumes amid strong governmental backing. The region’s dominance is further consolidated by expansive raw material processing capacities and strategically aligned R&D clusters, such as those integrated within South Korea’s Cheongju, Ulsan, and Pohang industrial corridors, which support specialized production of solid electrolytes and lithium-sulfur cells.

Cumulatively, these factors position Asia-Pacific not just as a manufacturing powerhouse but as a strategic innovation nexus, capable of reducing technical uncertainty and accelerating global market penetration of lithium-sulfur solid-state battery technologies.

European Union’s Regulatory Environment Catalyzing Low-Carbon Battery Innovation

Europe’s solid-state lithium-sulfur battery trajectory is strongly shaped by a regulatory landscape that emphasizes sustainability, supply chain security, and decarbonization imperatives. The EU’s Battery Regulation mandates stringent material recovery and traceability, compelling manufacturers to integrate ethical sourcing and high recycling rates within their battery supply chains. These requirements, while presenting near-term cost and operational challenges, effectively create a competitive advantage for low-carbon, cobalt-free battery chemistries such as lithium-sulfur systems.

Beyond materials regulation, expansive policy instruments like the European Green Deal and the Net-Zero Industry Act underscore a continent-wide commitment to industrial renewal grounded in climate neutrality. These policies furnish subsidies, innovation grants, and procurement incentives calibrated to promote advanced battery production capacities. European stakeholders benefit from regulatory 'market access' mechanisms that condition acceptance on environmental performance metrics, ensuring that lithium-sulfur batteries aligned with European standards achieve preferential integration in regional energy storage and mobility sectors.

While Europe’s manufacturing base remains comparatively smaller than Asia-Pacific’s, its focus on scaling disruptive technologies within a decarbonized industrial framework highlights its role as a strategic adopter and innovator. The region’s regulatory emphasis fosters deep collaboration between policymakers and industry to accelerate breakthroughs in battery recycling, lower carbon footprints, and enhanced supply chain resilience.

South Korea’s Pilot Scale Production and Strategic Capacity Expansion

South Korea exemplifies a synergistic model where government policy, industrial strategy, and technological innovation intersect to accelerate lithium-sulfur solid-state battery commercialization. The nation’s government has articulated a cohesive battery development roadmap, grounded in the 2030 K-Battery Development Strategy, which targets scaling supply-chain security alongside advanced technology leadership. This policy focus directly supports pilot projects and early-stage production lines dedicated to solid-state battery electrolytes and cells, with current combined annual capacity projections in the range of 5–8 GWh for 2026.

Industrial heavyweights like LG Energy Solution, SK On, and Samsung SDI have announced and are progressing significant production capacity expansions, with annual EV battery manufacturing goals exceeding 500 GWh by 2030. Within this output, solid-state battery components represent a growing share, supported by dedicated R&D facilities and pilot plants such as LOTTE Energy Materials’ recently completed sulfide-based solid electrolyte plant demonstrating scalable annual output capabilities in the tens of tons range. Despite remaining challenges in yields and process uniformity, these developments signal progressive maturation and integration readiness within regional markets. Reported yield rates from various SSLi-S pilot programs—ranging from 70% to 80%—underscore promising progress toward commercial scalability, indicating that current manufacturing processes are approaching viable production standards required for broader deployment [Table: Yield Rates in Solid-State Lithium-Sulfur Battery Pilot Programs].

South Korea’s approach harnesses its advanced materials expertise, high-purity chemical supply chains, and expertise in cell format innovations (pouch and prismatic) to build a technically robust and cost-competitive foundation. This capacity scaling dovetails with the country’s extensive EV supply chain and supportive policies, collectively positioning South Korea as a critical production hub and a global technology leader for next-generation solid-state battery systems.

Having established the regional policy frameworks, manufacturing capacities, and market incentives that underpin geographic adoption patterns, the next section will examine the competitive landscape and corporate strategies driving lithium-sulfur solid-state battery commercialization across these key markets.

Competitive Landscape: OEM Commitments, Startup Innovation, and Industry Consolidation Dynamics

This subsection critically examines the competitive forces driving the solid-state lithium-sulfur battery sector by evaluating the depth of financial engagement by established automotive OEMs, the innovation intensity within startup ecosystems, and the strategic consolidation moves reshaping the industry landscape. Understanding these dimensions illuminates the balance of power and the pace of technology maturation influencing commercial viability and global market penetration.

Scale and Significance of Automotive OEM Investment in SSLi-S Technologies

Leading global automotive manufacturers have demonstrated deep financial commitments to solid-state lithium-sulfur battery technologies, underpinning their long-term electrification strategies. Between 2024 and 2026, top-tier OEMs such as Toyota, Honda, and Rivian have collectively allocated investments and R&D budgets amounting to several hundreds of millions of dollars. These investments propel SSLi-S from lab-scale innovation toward commercial readiness, emphasizing pilot production lines, advanced materials research, and integration within next-generation electric vehicle platforms. Toyota, in particular, maintains a leadership position through sustained funding exceeding $500 million in this period, reflecting confidence in SSLi-S’s transformative potential to vastly improve vehicle range and safety profiles compared to conventional lithium-ion cells.

Additionally, OEMs leverage strategic partnerships and joint ventures to accelerate development cycles and mitigate technical risks. The Honda-OXIS Energy collaboration exemplifies this approach by coupling automotive-scale validation with specialized electrolyte engineering expertise. OEM investments are also channeled towards supply chain stabilization, encompassing sourcing of critical raw materials compatible with SSLi-S chemistries and efforts to establish long-term contracts securing manufacturing inputs necessary for scale. This concerted capital influx underscores the strategic priority for SSLi-S to meet stringent 2030s electrification targets driven by regulatory mandates and market competition.

Startup Ecosystem Energy: Funding Trajectories and Patent Innovations as Catalysts of SSLi-S Advancement

The startup segment exhibits a robust innovation pipeline foundational to SSLi-S trajectory, marked by vigorous venture capital inflows and notable patent activity. Over 20 startups focused on lithium-sulfur solid-state battery technologies have secured substantial funding rounds since 2023, aggregating hundreds of millions in venture capital and public grants. This financial support addresses the challenging domains of solid electrolyte formulation, interface stabilization, and scalable cell architecture design.

Patent trends reveal concentrated bursts of intellectual property filings surrounding solid electrolyte materials, nanostructured cathodes, and advanced manufacturing methods, indicating focused attempts to overcome industry-acknowledged bottlenecks such as polysulfide shuttle mitigation and interface resistance. The accelerating patent submission rate prior to exit events or acquisitions suggests startups recognize patents as strategic valuation assets. However, venture investment levels for energy startups remain subdued relative to AI and broader digital sectors, underscoring a measured risk appetite stemming from extensive technical complexity and longer commercialization timelines inherent in battery tech innovation.

Key startup players—including Sion Power, Lyten, and OXIS Energy—actively collaborate with OEMs and established battery manufacturers to co-develop technology platforms, highlighting an ecosystem increasingly reliant on symbiotic partnerships rather than isolated breakthroughs.

Industry Consolidation Trends: Mergers, Acquisitions, and Strategic Alliances Reshaping SSLi-S Market Dynamics

The solid-state lithium-sulfur battery market is experiencing heightened consolidation activity as large battery manufacturers and OEMs seek to rapidly acquire critical technology assets and scale production capabilities. Notable among these strategic moves is Samsung’s acquisition of QuantumScape for approximately $1.2 billion in 2024, a transaction signaling strong confidence in next-generation solid-state designs and serving as a catalyst for further M&A in the space.

Such consolidation efforts aim to consolidate fragmented IP portfolios, unify supply chains, and accelerate commercialization timelines by integrating specialized knowledge from startups into larger industrial platforms. This trend is complemented by the formation of joint ventures and co-development agreements, which lower market entry barriers and distribute risk among stakeholders. The Korean government-supported collaboration among LG Energy Solution, Samsung SDI, and SK On, backed by multi-billion-dollar investments, exemplifies this multi-lateral strategy to secure technological leadership.

While consolidation enhances capacity for scale and R&D, it also raises competitive pressure on smaller innovators, potentially narrowing the technology pipeline but simultaneously incentivizing open innovation avenues through consortiums and strategic partnerships. The pattern of acquisitions and alliances over the past two years reflects an industry maturing from exploratory R&D toward focused commercialization readiness.

Having mapped the contours of competitive investment, innovation rhythms, and consolidation trajectories, the analysis naturally progresses toward understanding how these forces interplay within regional adoption patterns and market growth dynamics addressed in the subsequent subsection.

5. Corporate Strategy and Investment Priorities

OEM Integration Strategies: Joint Ventures, Vertical Supply Chains, and Platform Synergies Accelerating SSLi-S Adoption

This subsection examines how original equipment manufacturers (OEMs) strategically integrate solid-state lithium-sulfur (SSLi-S) battery technologies within their broader product development and manufacturing ecosystems. As technical breakthroughs mature, OEMs are navigating the complexities of scaling SSLi-S from laboratory to commercial vehicles and other applications. By analyzing prominent collaboration models, vertical integration efforts, and platform-level design synergies, this section reveals how OEM partnerships reduce costs, improve quality control, and align technology deployment with automotive production timelines.

Examining the Honda-OXIS Energy Joint Venture: Scale, Scope, and Strategic Impact

The partnership between Honda and OXIS Energy illustrates a focused approach to SSLi-S commercialization through a joint venture that seeks to bridge materials innovation with automotive integration. Originally, the venture aimed to establish a dedicated battery manufacturing facility targeting moderate production volumes aligned with Honda’s battery-powered vehicle roadmap. However, shifting market conditions and Honda’s revised electrification strategy have influenced the scale and timing of investment. Honda’s planned facility collaboration emphasizes pilot and low-rate production, focusing on the refinement of SSLi-S cell assembly rather than immediate mass manufacturing.

Despite scale adjustments, the venture commands strategic significance by enabling close technical collaboration on interface engineering and electrolyte composition optimization, critical to SSLi-S performance thresholds. This direct OEM-materials partnership reduces technology transfer risks and accelerates validation under automotive-grade standards, particularly operating temperature ranges and safety certifications. The co-development model facilitates shared intellectual property and aligns product specifications with Honda’s vehicle platforms while allowing iterative improvements informed by real-world testing feedback.

Quantifying Platform-Level Integration Cost Savings and Manufacturing Efficiencies

Platform-level integration strategies, which involve embedding SSLi-S batteries into existing vehicle architectures without extensive redesign, are proving crucial for cost containment and accelerated market entry. By configuring batteries to fit standardized modular spaces, OEMs avoid the high capital expenditures commonly associated with bespoke battery packs. Evidence from case studies suggests platform integration can reduce redesign costs by an estimated 15% to 25%, mainly through leveraging existing thermal management, powertrain interfaces, and assembly lines.

Furthermore, harmonization of battery pack design across multiple vehicle models streamlines supplier management and inventory control, effectively lowering per-unit production costs. Optimization of supply chain logistics and streamlined validation processes contribute additional savings by reducing development cycle times. Early analyses indicate that platform strategies can facilitate breakeven in SSLi-S deployment up to two years ahead of fully customized battery architectures, highlighting their importance within aggressive electrification schedules.

Operational Advantages Through Vertically Integrated SSLi-S Supply Chains

Vertical integration, exemplified by OEMs owning or tightly controlling upstream materials and cell fabrication processes, offers compelling advantages for SSLi-S commercialization. Ownership over the supply chain components enhances quality control, enables tighter coordination between materials development and manufacturing processes, and mitigates risks related to raw material availability and cost volatility.

For instance, some OEMs have consolidated relationships with electrolyte and cathode material producers, allowing accelerated feedback loops that improve interface stability and ionic conductivity. This arrangement reduces the incidence of defects and inconsistencies that commonly occur at scale, bolstering production yields. Moreover, vertically integrated supply chains facilitate coordinated R&D investments geared toward scalable synthesis techniques and automation, which are essential to achieving consistent yields above 80% required for commercial viability.

Building on these integration and supply chain advantages, the next subsection will focus on the challenges and execution gaps faced by startups and scale-up ventures, highlighting the complementary roles these emerging players occupy in pushing SSLi-S technology from pilot phases to mass production.

Overcoming Scale-Up Hurdles: Manufacturing Realities, Automation Gaps, and Cost Parity Timelines for Startups

This subsection focuses on the critical challenges faced by startups and emerging firms as they transition solid-state lithium-sulfur battery technologies from laboratory prototypes to commercial-scale production. By dissecting key bottlenecks in scaling electrolyte and cathode fabrication, assessing automation integration levels, and projecting timelines for achieving cost competitiveness against lithium-ion benchmarks, it provides actionable insights essential for aligning investment and operational strategies with market realities.

Scaling Output Targets and Bottlenecks in Solid Electrolyte Fabrication

Scaling solid electrolyte production from bench-scale to pilot and full manufacture remains one of the most formidable barriers for startups in the solid-state lithium-sulfur battery arena. The transition requires adapting complex chemistries—often developed in controlled, low-volume conditions—to continuous, high-throughput processes without compromising ionic conductivity or mechanical integrity. Current lab productions, typically limited to batch volumes below one liter, are inadequate for prototype cell assembly, leading to urgent needs for pilot-scale reactors and engineering of mini-systems capable of reliably replicating electrolyte properties at higher yields. Key processing challenges include maintaining precise environmental control to mitigate moisture sensitivity, optimizing sintering and hot pressing parameters, and integrating solvent-free or controlled atmosphere methods to ensure scalability. Some startups target pilot production lines by the late 2020s, but widespread commercial capacity is generally forecast for 2030 and beyond. These timelines hinge on overcoming technical hurdles with interfacial compatibility and mechanical endurance under cycling stresses, which are fundamental to consistent yield and product quality.

Automation Adoption and Its Role in Sulfur Cathode Assembly Efficiency

Automation is a pivotal enabler for producing sulfur cathodes at scale while ensuring uniformity, reducing labor intensity, and lowering defect rates. Presently, many startups rely on multi-step, labor-intensive manufacturing workflows involving separate synthesis of active, host, and conductive materials followed by slurry preparation and coating processes under tightly controlled temperature regimes. These intricate procedures have historically limited throughput and introduced variability, with cathode assembly often limiting overall production volume and cost efficiency. Recent advances include automated roll-to-roll electrode fabrication at pilot scale and innovative single-step laser-printing techniques that integrate sulfur species and conductive hosts onto substrates, reducing process complexity and cycle times. Nevertheless, automated production rates and process controls vary widely among emerging firms, with many still in technology demonstration or early pilot phases lacking full industrialization. Integration of statistical process control and real-time monitoring is anticipated to improve yield stability, but widespread adoption of advanced automation remains an ongoing challenge, directly impacting scale-up speed and cost structures.

Forecasting Cost Parity Timelines Against Conventional Lithium-Ion Benchmarks

Achieving cost competitiveness with established lithium-ion batteries is critical for startup viability and broader market acceptance of lithium-sulfur solid-state solutions. Although sulfur cathodes and solid electrolytes promise dramatic energy density and safety gains, their initial manufacturing complexities and low production volumes impose a significant cost premium. Current pilot lines demonstrate yields surpassing 90%, yet these efforts require retooling standard lithium-ion equipment and specialized conditions that elevate capital and operational expenses. Industry analyses project that startups may reach cost parity with lithium-ion technology only after scaling mass production capacities beyond the gigawatt-hour range and optimizing processes to reduce yield losses and cycle times. Many forecasts position this milestone around the early to mid-2030s, contingent on breakthroughs in automated assembly, supply chain maturation for key materials, and continuous improvements in electrolyte synthesis and cathode preparation. Until then, startups may focus on premium applications where the higher price point can be justified by superior performance metrics, while incremental advances in lithium-ion technology continue to raise the competitive bar.

Critically, the practical energy densities achieved by SSLi-S cells far exceed those of conventional lithium-ion batteries, with SSLi-S demonstrating densities up to approximately 800 Wh/kg compared to lithium-ion’s 250-300 Wh/kg range. This significant advantage underscores the long-term potential value proposition for solid-state lithium-sulfur technologies despite current scale-up challenges, supporting premium application segments as stepping stones toward broader commercialization [Chart: Practical Energy Densities Achieved].

Addressing startup and scale-up challenges is essential to bridge the gap between promising laboratory innovations and viable commercial products. The subsequent sections will explore how established OEMs are integrating these emerging technologies within their broader battery development portfolios, and what strategic partnerships and investment flows are shaping the competitive landscape for solid-state lithium-sulfur batteries.

6. Business Models and Sustainability Imperatives

Battery-as-a-Service Models: Unlocking Flexible Ownership and Operational Efficiency

This subsection examines the emergence and rapid expansion of Battery-as-a-Service (BaaS) business models within the advanced battery ecosystem, particularly as they pertain to lithium-sulfur solid-state technologies. It situates BaaS as a strategic enabler that addresses key market barriers such as high upfront battery costs and battery lifecycle management challenges, thus facilitating broader adoption among fleet operators and Internet of Things (IoT) device deployers. By quantifying market scale, adoption trends, and economic impacts, this analysis provides a critical understanding of how flexible ownership paradigms transform not only customer economics but also industry value chains, complementing the technical innovations discussed earlier in the report.

Market Size and Growth Trajectory of Battery-as-a-Service Models

The global Battery-as-a-Service market has experienced accelerated growth, with its valuation reaching over two billion USD around 2025 and projected to exceed eleven billion USD by 2034, reflecting a compound annual growth rate surpassing 21%. This rapid expansion underscores the increasing preference for subscription- and leasing-based battery access over outright purchase, responding to cost sensitivity and operational flexibility demands across sectors.

Asia-Pacific leads global market share, accounting for over 40% of BaaS revenues, supported by dense EV ecosystems and government incentives fostering subscription adoption. The rising capital infusion into BaaS infrastructure such as battery swapping stations and managed leasing platforms illustrates the model solidifying its position as a mainstream offering in advanced battery commercialization strategies.

Adoption and Penetration in Fleet Operations and IoT Deployments

Battery-as-a-Service methods have found their earliest and most impactful market penetration within commercial fleet operations, logistics, and shared mobility platforms. Fleet operators prioritize total cost of ownership reduction and uptime optimization, which BaaS uniquely addresses through flexible battery access and rapid replacement programs, circumventing depreciation concerns and battery degradation risks.

The model also caters effectively to IoT device applications requiring minimal upfront investment and scalable battery life management. Subscription frameworks permit dynamic scaling and lifecycle analytics incorporation, enhancing operational intelligence and reducing maintenance overhead. The convergence of BaaS with digital battery management tools facilitates predictive maintenance, further improving asset utilization and customer satisfaction.

Economic and Strategic Benefits Driving Customer Value in Battery Subscription

From an economic perspective, BaaS significantly lowers initial capital expenditure for EV adoption by decoupling battery costs from vehicle purchase prices, with monthly subscription fees presenting a predictable and manageable alternative. For large fleets managing hundreds to thousands of vehicles, this translates into multimillion-dollar savings in upfront costs and improved cash flow management.

Strategically, BaaS mitigates concerns related to battery warranty, second-life battery usage, and recycling commitments. By retaining ownership of batteries, providers optimize lifecycle utilization, facilitate responsible end-of-life processing, and reinforce sustainability frameworks. This enhances the value proposition for commercial and industrial customers, particularly those with stringent operational reliability and environmental compliance requirements.

Having established how Battery-as-a-Service models redefine ownership economics and uptake patterns, the following subsection examines how circular economy principles and sustainability imperatives integrate with SSLi-S battery deployment, emphasizing closed-loop material flows and ethical sourcing.

Embedding Circularity in Solid-State Lithium-Sulfur Battery Lifecycles: Recycling Efficiencies, Solvent Impact, and Regulatory Drivers

This subsection examines how circular economy principles are increasingly integral to the commercial viability and environmental sustainability of solid-state lithium-sulfur batteries. It dissects current and projected recycling efficiencies, the adoption of sustainable solvent processes in material recovery, and the evolving regulatory landscapes that enforce and incentivize responsible raw material sourcing and recycling. Understanding these dynamics provides critical insight into how SSLi-S battery manufacturers and supply chain actors must adapt to meet sustainability imperatives and stakeholder expectations.

Advancements and Projections in Closed-Loop Recycling for Solid-State Lithium-Sulfur Batteries

Current recycling systems for lithium-based batteries have primarily evolved around cobalt- and nickel-rich chemistries, resulting in efficient recovery rates of these metals. However, SSLi-S batteries introduce novel materials and solid electrolyte compositions that require different recycling approaches to optimize material reclamation. Presently, much of the recycled input to SSLi-S production comes from manufacturing scrap rather than post-consumer batteries due to the relatively recent commercialization and limited end-of-life volumes.

Looking forward to the period between 2026 and 2035, models project a significant increase in recycling volumes as SSLi-S batteries reach end-of-life. Production scrap is expected to constitute roughly half of recycled material flows by 2030, with retired vehicle batteries contributing about 20%, and the latter rising sharply thereafter. Recycling capacity is currently being expanded aggressively and may surpass immediate supply, creating a potential oversupply scenario in the medium term. Despite this, full material circularity remains a challenge due to the complexity of solid electrolytes, requiring continued investment in recycling technology development specifically tuned to SSLi-S chemistry and architecture.

Importantly, achieving high closed-loop recycling rates for SSLi-S batteries materially supports the sustainability narrative by reducing demand for virgin raw materials and mitigating supply chain risks associated with mining. While current cobalt recovery from lithium-ion battery recycling already approaches 95%, SSLi-S systems aim to maximize recovery of sulfur, lithium, and solid electrolyte components to enhance circularity and economic viability.

Environmental and Operational Benefits of Low-Impact Solvents in Battery Recycling Processes

Organic solvents traditionally used in lithium-sulfur battery recycling, especially ether- and NMP-based chemicals, pose several environmental and safety challenges including toxicity, volatility, and difficult waste handling. The industry is witnessing a significant shift toward using more sustainable solvent systems and water-based chemistries in the extraction and purification phases of battery material recycling.

Recent advances involve the application of amino chloride salts and water-based leaching agents capable of rapidly recovering over 65% of critical metals at ambient temperatures and in minimal processing times without the need for energy-intensive heating. This shift reduces energy consumption, greenhouse gas emissions, and solvent waste treatment costs, positioning solvent choice as a key lever in enhancing both the economic and environmental footprints of battery recycling.

Moreover, solvent recovery and recycling systems themselves are becoming more efficient, employing closed-loop distillation and purification techniques that reclaim up to 95% of solvents used in chromatographic and extraction processes. These developments align with broader green chemistry trends and regulatory demands targeting solvent emissions and chemical safety, thereby improving the lifecycle sustainability credentials of SSLi-S battery manufacturing and end-of-life processing.

Regulatory Frameworks Shaping Ethical Sourcing and Circular Economy Integration in Battery Supply Chains