SpaceX IPO and NASA Lunar Base: Pioneering the Commercial Frontier of Space Exploration

Table of Contents

- Executive Summary

- Introduction

- 1. SpaceX's IPO and NASA's Lunar Base: Shifting Frontiers of Commercial Space Exploration

- 2. Strategic Implications of SpaceX's IPO for the Future of Space Exploration

- 3. The Evolving Landscape of Commercial Space Activities

- 4. Integration of Advanced Technologies in Space Operations

- 5. Conclusion: Charting the Course for Sustainable Space Commerce

- Conclusion

Executive Summary

This report provides a comprehensive analysis of SpaceX's imminent Initial Public Offering (IPO), valued at approximately $1.75 trillion, and NASA's strategic development of a sustainable lunar base at the Moon’s South Pole. SpaceX's Starship vehicle introduces groundbreaking capabilities, such as a 100 metric ton payload capacity to low Earth orbit and full reusability, poised to revolutionize lunar logistics by substantially reducing mission complexity and cost. The IPO aims to raise an estimated $75 billion to finance critical Starship development milestones and expand SpaceX’s role in NASA’s Artemis lunar missions.

NASA’s lunar base initiative follows a phased roadmap targeting robotic reconnaissance, early habitat deployment, and sustained human presence by the early 2030s. The lunar South Pole’s unique environment, offering extended sunlight exposure averaging 13.5 kWh/m² daily during peak periods, supports robust solar power generation crucial for long-term operations. Concurrently, NASA's Commercial Lunar Payload Services (CLPS) program actively engages private sector providers, fostering competitive growth and enabling affordable payload deliveries that underpin Artemis objectives. Collectively, these developments mark a transformative alignment of public and private investment shaping the future of commercial space exploration.

Introduction

The advent of a new era in space exploration is being shaped by the convergence of innovative commercial capabilities and ambitious government-led lunar initiatives. Central to this transition is SpaceX’s forthcoming public offering, anticipated to be the largest IPO in history, reflecting profound investor confidence in the company’s transformative technologies and strategic positioning within the aerospace sector. Simultaneously, NASA is advancing its Artemis program to establish a permanent human presence on the Moon’s South Pole, leveraging private-sector partnerships and cutting-edge technologies.

SpaceX’s Starship system epitomizes this shift, offering unprecedented payload capacity and full reusability that promise to significantly enhance lunar mission logistics, sustainability, and operational efficiency. The upcoming IPO is expected to inject substantial capital into Starship development and related lunar mission infrastructure, strengthening SpaceX’s competitive edge and aligning corporate financing with national exploration goals.

NASA’s lunar base project adopts a structured, phased approach to infrastructure build-out, emphasizing robotic precursor missions, habitat establishment, and eventual sustained human operations. The Moon’s South Pole was selected for its advantageous environmental conditions, particularly extended sunlight periods essential for solar power generation. Furthermore, NASA’s Commercial Lunar Payload Services (CLPS) program serves as a critical mechanism to stimulate private sector innovation, enabling rapid deployment of robotic payloads and expanding the capacity for lunar surface activities.

This report aims to synthesize the current status and strategic implications of SpaceX’s IPO alongside NASA’s lunar base development plans as of May 2026, elucidating their interconnected roles in shaping the future trajectory of commercial space exploration. The analysis encompasses technological capabilities, investment priorities, programmatic milestones, and the evolving public-private partnership landscape critical to realizing sustainable extraterrestrial operations.

Infographic Image: Infographic

1. SpaceX's IPO and NASA's Lunar Base: Shifting Frontiers of Commercial Space Exploration

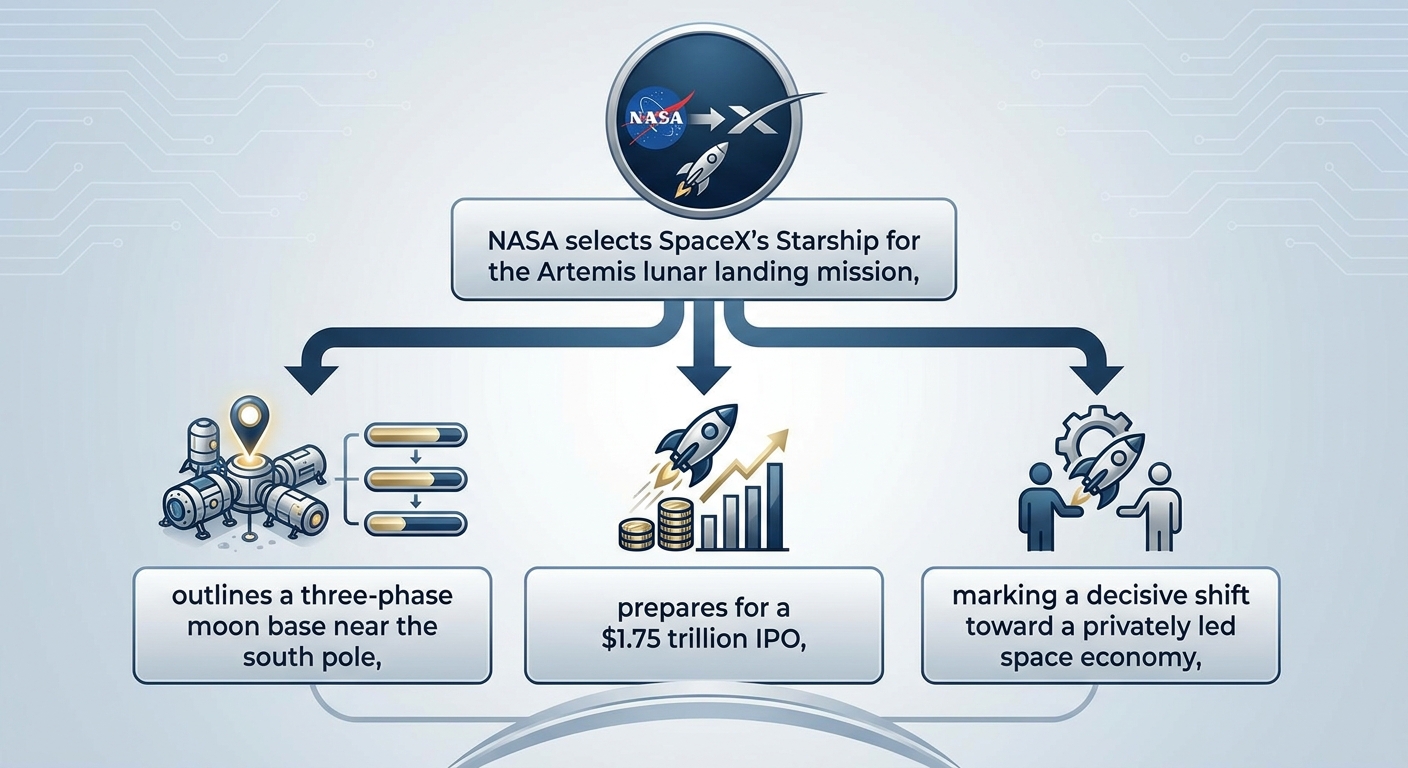

NASA’s Selection of SpaceX’s Starship for Artemis Lunar Landing: A Paradigm Shift in Human Lunar Missions

This subsection examines the critical decision by NASA to select SpaceX's Starship as the primary lunar lander for the Artemis program, illustrating its significance in advancing human exploration of the Moon. It situates Starship’s technical capabilities within NASA’s strategic goals and underscores the broader industry implications of relying on private sector technology for crewed spaceflight.

Starship’s Exceptional Payload Capacity Transforming Lunar Logistics

SpaceX’s Starship system, particularly its latest iteration, boasts a payload capacity of approximately 100 metric tons to low Earth orbit, representing a threefold increase over previous versions. This capability extends directly to lunar missions, allowing substantial cargo and crew delivery in a single flight. By enabling large-volume payloads, Starship fundamentally alters logistical operations on the lunar surface, facilitating rapid assembly of infrastructure and transport of essential supplies with fewer launches.

This leap in payload capacity is pivotal for NASA’s Artemis program, which requires not only human landing systems but also support for sustained habitation and research installations. The ability to deliver heavy and bulky equipment in one mission reduces complexity and mission risk, thereby enhancing overall mission sustainability and scalability.

Demonstrated Reusability and Operational Efficiency Underpin Sustainable Moon Presence

A defining feature of Starship is its full reusability, including both the Super Heavy booster and the upper spacecraft stage. Achieving rapid turnaround times akin to commercial aircraft operations, SpaceX aims to drastically reduce per-launch costs. As of early 2026, Starship has completed over a dozen test flights with ongoing refinements to reliability and operational cadence, reflecting significant progress towards routine and cost-effective lunar missions.

This operational model represents a paradigm shift from conventional expendable launch vehicles, aligning with NASA’s sustainability objectives for long-term lunar exploration. Reusability not only lowers costs but also supports higher launch frequencies that are necessary for establishing and maintaining an enduring lunar presence.

NASA’s Criteria and Strategic Rationale for Choosing Starship as Artemis Human Lander

NASA’s selection process for the Artemis human lander prioritized the integration of capabilities that meet stringent safety, sustainability, and cost-effectiveness requirements. The human-rating certification demands accommodating crew safety through design robustness, hazard mitigation, and successful demonstration of flight reliability under operational stress conditions.

Starship’s large payload capacity, combined with its full reusability and modular variants (including crewed, cargo, and tanker configurations), fulfilled NASA’s criteria for enabling a multi-mission architecture. Furthermore, NASA’s strategy increasingly embraces private-sector solutions to accelerate innovation, reduce programmatic risk, and harness market efficiencies. The choice of Starship reflects this strategic shift, highlighting collaboration as essential to achieving ambitious exploration timelines while controlling taxpayer resources.

Building upon NASA’s choice of Starship as the cornerstone lunar lander, the next subsection will explore the phased roadmap for developing the sustainable Moon Base and how Starship’s capabilities directly facilitate each stage of this ambitious human presence initiative.

Strategic Roadmap and Sustainability of NASA's Lunar Base at the Moon's South Pole

This subsection provides a detailed analysis of NASA's phased approach to establishing a sustained human presence on the lunar surface near the South Pole. By examining the timeline, key milestones, and technological innovations underpinning each development phase, it contextualizes how NASA's strategy integrates critical environmental factors and emerging technologies to foster a viable lunar outpost. This focus is essential to understanding the operational backbone supporting commercial and scientific objectives outlined in this report.

Timeline and Milestones for NASA’s Three-Phase Lunar Base Development

NASA’s lunar base development follows a structured three-phase strategy designed to progressively build capability and infrastructure on the Moon’s South Pole through the mid-2030s. The initial phase, extending through 2029, concentrates on robotic missions aimed at technological validation and surface reconnaissance. These missions will deploy rovers, landers, and autonomous systems to gather data critical for infrastructure planning and early resource utilization demonstrations.

The second phase, from 2029 to 2032, marks the deployment of early habitation modules alongside the establishment of essential power and communication systems. This phase introduces semi-permanent infrastructure supporting limited crewed activities while enabling remote operational control. Notably, NASA plans to build a foundational power grid to support increasing energy demands, factoring in the region’s unique environmental conditions.

Starting after 2032, the third phase envisions transitioning to sustained human presence. This involves the construction of permanent habitats with capabilities for extended surface missions, advanced life support, and comprehensive in-situ resource utilization (ISRU). This phase also amplifies scientific research capacity and lays groundwork for broader commercial engagement and international partnerships.

Extended Sunlight Duration at the Lunar South Pole: A Key Factor for Power Systems

The lunar South Pole was chosen due to extended periods of sunlight that are crucial for solar power generation and stable thermal environments. Unlike equatorial regions, which experience roughly 14 Earth days of continuous sunlight alternating with equivalent darkness, polar regions benefit from nearly continuous illumination during certain periods.

Quantitative irradiance assessments indicate that sunlight at the South Pole can reach approximately 13.5 kWh/m² per day during peak periods, surpassing solar energy availability at the equator. This extended solar exposure reduces reliance on nuclear or battery-based power systems, lowering complexity and cost of lunar base energy infrastructure.

However, challenging terrain with permanently shadowed craters—potentially hosting water ice—necessitates careful base site selection and complementary power strategies to ensure operational continuity throughout the lunar day-night cycle.

Integration of Robotics, Power, and In-Situ Resource Utilization Technologies

Robotic systems form the operational vanguard, particularly in phase one, where autonomous rovers and landers scout terrain, conduct scientific surveys, and test key technologies including mobility, communication, and environmental monitoring. Their data feed directly informs habitat site locational decisions and informs risk assessments for human missions.

Power system development emphasizes leveraging solar arrays optimized for polar illumination conditions, supplemented by emerging compact nuclear power technologies for periods when sunlight wanes. NASA’s strategy also includes establishing a reliable communications network incorporating orbital relays and surface infrastructure to maintain continuous contact with Earth and lunar assets.

ISRU technology development is a critical enabler for sustainability, targeting extraction and processing of lunar water ice for life support and propellant production. Additive manufacturing experiments aim to utilize local regolith for durable structures, shielding habitats from radiation and micrometeorites. Overall, these interconnected technologies create a systemic framework designed to reduce Earth dependency and operational costs, thereby facilitating extended lunar presence.

This phased roadmap underlines how NASA’s lunar base initiative forms an essential platform for expanding commercial and international partnerships, setting the stage for analysis of how SpaceX’s IPO and related activities align with and accelerate these broader exploration and development objectives.

Commercial Lunar Payload Services (CLPS) Program: Catalyzing Private Sector Momentum in Lunar Exploration

This subsection situates the Commercial Lunar Payload Services (CLPS) program as a foundational mechanism through which NASA actively engages and leverages private sector capabilities to advance lunar surface operations. By examining the current contract landscape, financial dimensions, and recent mission outcomes, it highlights how CLPS accelerates innovation, risk-sharing, and commercialization on the Moon, serving as a vital pillar in the evolving architecture of sustainable and competitive lunar activities.

Identifying Active Commercial Players Driving NASA’s Lunar Payload Deliveries

NASA’s CLPS initiative strategically harnesses a diversified pool of private companies to provide robotic lunar lander services, enabling rapid, cost-effective delivery of scientific payloads and technology demonstrators to the Moon. As of mid-2026, key active contractors sustaining this momentum include Intuitive Machines, Firefly Aerospace, Astrobotic, Lockheed Martin, The Charles Stark Draper Laboratory, SpaceX, and Blue Origin. These organizations span established aerospace giants and emerging commercial innovators, blending heritage expertise with agile development strategies.

While early CLPS mission attempts have yielded mixed success—with some missions achieving deployment but others facing failures or setbacks—the program remains a crucial incubator for breakthrough lunar surface capabilities. Notably, SpaceX and Blue Origin’s lander development programs, including the Cargo Human Landing System and Blue Moon lander respectively, signal a growing competitive dynamic and expanded capacity for diverse lunar payload delivery options.

Assessing the Scale and Financial Scope of CLPS Contracts Fostering Commercial Integration

The CLPS program utilizes an innovative procurement framework wherein NASA contracts the delivery of payloads as end-to-end services, a departure from traditional asset-centric mission management. This results in contract task orders with aggregated values that often cover multiple payloads and services, making granular individual cost allocations challenging. For example, the CLPS task order to deliver the VIPER rover constituted an approximate cost addition of $226.5 million above the payload’s own development budget, reflecting the significant financial commitment NASA assigns to private delivery services.

Through this model, NASA aims to lower development timelines and costs by transferring execution responsibilities and risks to private entities while fostering an emergent multibillion-dollar lunar surface operations sector. The procurement volume and contract values reflect NASA’s intent to sustain a cadence of lunar missions that gradually increase in complexity and payload mass, stimulating private investment and commercial ecosystem growth.

Recent CLPS Mission Outcomes and Their Influence on Lunar Surface Operations Progress

The early operational record of CLPS missions underscores the program’s role as a high-risk, high-reward innovation crucible. While foundational efforts have yielded partial successes, including at least one fully successful lunar landing, the program has also witnessed failures such as lander tip-overs and missing the lunar surface. These outcomes provide invaluable engineering and operational data that refine subsequent mission planning and technology maturation.

This experiential learning, though costly, has accelerated the iterative development pace, allowing NASA and the commercial partners to collectively advance surface delivery reliability. Furthermore, the CLPS missions serve as robotic precursors gathering critical reconnaissance and technology demonstrations, preparing the groundwork for Artemis human landings and permanent lunar habitation phases. The incremental delivery of infrastructure elements such as communication relays and power units aligns with NASA’s phased Moon Base strategy, underscoring CLPS’s integral role in enabling sustainable lunar presence.

Collectively, the CLPS program exemplifies a paradigm shift in lunar exploration logistics that embraces private sector innovation and risk-sharing. Its contract structure, active participation by diverse companies, and progressive mission outcomes not only catalyze the immediate delivery of payloads to the Moon but also stimulate a flourishing commercial lunar ecosystem. This foundation sets the stage for the broader strategic implications of SpaceX’s IPO and NASA’s lunar ambitions as articulated in subsequent sections.

2. Strategic Implications of SpaceX's IPO for the Future of Space Exploration

Valuation and Market Positioning of SpaceX's IPO: Unprecedented Scale Meets Investor Scrutiny

This subsection assesses the financial magnitude and positioning of SpaceX's upcoming IPO, highlighting how its unprecedented valuation situates the company within both the aerospace industry and broader capital markets. It examines investor sentiment, benchmark comparisons with past IPOs, and the unique market dynamics shaping expectations as SpaceX prepares to transition from a private pioneer to a publicly traded industry leader.

Investor Sentiment Surrounding SpaceX’s $1.75 Trillion Valuation

The anticipation for SpaceX’s initial public offering, with a targeted valuation near $1.75 trillion, has generated considerable enthusiasm and skepticism among investors. Market sentiment reflects a dual narrative: one driven by confidence in SpaceX’s dominant position across multiple space industry segments—including satellite broadband, launch services, and government contracts—and another marked by caution over the company’s extraordinary valuation multiples. While private market valuations have shown rapid escalation, public investors face uncertainty regarding the rationale behind such a high market capitalization relative to current revenue and profitability metrics.

Retail investors have responded with heightened interest, driving SpaceX-related discussion volumes and bullish expectations in trading communities. However, institutional investors are also highlighting the risks tied to Elon Musk’s overlapping leadership roles and the complex financial structure connecting SpaceX with Musk’s other ventures. These concerns introduce potential governance challenges and cloud the clarity of profitability forecasts, fueling a nuanced market outlook that balances optimism about growth prospects against the volatility inherent in pioneering commercial space enterprises.

Historical Benchmarks and Financial Comparisons for Mega-Sized IPOs

At a projected $1.75 trillion valuation, SpaceX aims to establish the largest IPO in history, surpassing previous high-water marks set by companies such as Saudi Aramco and technology giants throughout the last decade. This scale is unprecedented in the aerospace sector, where few prior public listings approach this magnitude. Comparison with historic IPOs reveals a pattern where sky-high price-to-sales ratios often correlate with early-stage optimism that may not sustain long-term performance, underscoring the high-risk, high-reward nature of such landmark offerings.

Unlike typical aerospace companies with steady earnings and contract backlogs, SpaceX’s valuation is anchored on aggressive projections of future growth driven by emerging markets, including global internet provision via Starlink and interplanetary transportation via the Starship program. This transforms the IPO into a structural re-rating event that not only redefines valuation standards for space companies but also challenges investors to evaluate a revolutionary business model combining vertically integrated infrastructure with multi-domain revenue streams. Consequently, traditional benchmarks provide limited direct comparability, which complicates valuation assessments but confirms the market-setting potential of SpaceX’s public debut.

Understanding SpaceX’s valuation context and market positioning sets the groundwork for analyzing how the capital raised through the IPO will influence the company's strategic investments and growth trajectory in subsequent sections.

Strategic Allocation of SpaceX IPO Proceeds: Focused Investment in Starship and Lunar Missions

This subsection examines how the capital raised through SpaceX's initial public offering is strategically earmarked to accelerate core programs underpinning the company’s leadership in commercial space exploration. It details the specific financial commitments to Starship development, lunar mission contracts, and related infrastructure, aligning financial inputs with operational milestones and NASA partnerships as of mid-2026.

Distribution of IPO Funds Across SpaceX’s Core Programs

The proceeds from SpaceX’s IPO, expected to close in mid-2026, are explicitly prioritizing investments that sustain and extend the company’s competitive advantages in space launch capabilities and extraterrestrial mission architectures. A significant portion of the raised capital is designated for Starship development – the fully reusable super-heavy launch system intended to service NASA’s Artemis lunar program and foundational to future interplanetary missions. This allocation targets critical milestones such as completion of in-orbit refueling demonstrations and human-rating certifications necessary for crewed lunar landings.

Beyond Starship refinement, the IPO funds are also strategically allocated to secure and expand NASA lunar mission contracts, reinforcing SpaceX’s role as the human lunar landing system provider. Investments include the development of lunar-specific Starship variants optimized for surface operations, such as the Human Landing System version designed to transport astronauts to the Moon’s surface during Artemis III and subsequent missions. This commitment ensures alignment with NASA’s cost and schedule baselines and supports ongoing flight tests focused on lunar landing maneuvers and propellant transfer technologies.

Timeline and Phasing of Capital Deployment for SpaceX’s Key Initiatives

Financial planning post-IPO reflects a phased funding approach, calibrated to parallel operational testing and contract milestones. Starship’s development is front-loaded in the immediate 2026–2027 timeframe, prioritizing successful crewed demonstration flights and orbital refueling demonstrations that are prerequisites for Artemis missions. These near-term investments are critical to transitioning from prototype testing to operational readiness.

Concurrent with Starship development, funding is staged to advance lunar mission infrastructure, including ground support systems, mission control capabilities, and integration of reusable propulsion and landing systems. Investment pacing also accounts for anticipated scaling of Starlink satellite internet operations that support data transmission needs for lunar communications and logistics. While Mars-focused ambitions and space-based AI infrastructure remain strategic pillars, their dedicated funding phases are slated beyond initial IPO capital utilization, reflecting the sequencing of corporate priorities aligned with NASA’s lunar-centric timeline. This structured approach aligns with NASA’s phased lunar base development timeline, which plans distinct milestones across Phase 1 (2025-2029), Phase 2 (2029-2032), and post-2032 stages, delineating critical activities for establishing a sustainable presence at the Moon’s South Pole [Chart: NASA's Lunar Base Development Timeline].

Having outlined the focused financial distribution and timing of SpaceX’s IPO proceeds, the subsequent subsection will assess the regulatory environment and market challenges SpaceX faces as it transitions from a private to a publicly traded entity, which will impact execution of these ambitious spacelift and lunar mission plans.

Navigating Regulatory Complexities and Governance Risks in SpaceX’s IPO Transition

This subsection evaluates the critical regulatory and governance challenges SpaceX faces as it transitions into a publicly traded company. It identifies the timeline and nature of regulatory approvals pivotal to operational continuity and examines the unique governance structure centered on Elon Musk’s sustained control. This analysis is essential to understand how these factors might influence investor confidence and strategic flexibility post-IPO.

Regulatory Approval Timelines and Risks Impacting Operational Continuity

SpaceX’s entry into the public markets exposes it to a complex regulatory landscape that directly affects its operational cadence and strategic ambitions. The company must secure and maintain several critical licenses, including Federal Aviation Administration launch and reentry authorizations, as these are single points of failure for its orbital activities. Delays or obstacles in obtaining these permits could disrupt scheduled Starship missions, satellite deployments, and associated commercial services, thereby impacting revenue streams.

Further, licensing from the Federal Communications Commission and analogous international bodies imposes stringent requirements on spectrum allocation necessary for the Starlink satellite network. Failure to obtain or sustain spectrum rights in various jurisdictions could jeopardize service continuity and undermine the viability of SpaceX’s broadband offerings.

SpaceX also operates in a rapidly evolving regulatory environment regarding emerging technologies such as orbital AI compute and lunar industrialization. These nascent fields lack established regulatory frameworks, introducing significant uncertainty. The company itself acknowledges that these initiatives involve unproven technologies with significant commercial risks, potentially complicating regulatory compliance and prolonging approval timelines.

Governance Structure and Concentrated Control: Implications for Investor Confidence

The governance framework outlined in SpaceX’s IPO prospectus is unprecedented in its consolidation of control within the founder’s hands. Elon Musk retains majority voting power through a dual-class share structure that grants him over 85% of voting rights, effectively ensuring he remains unchallengeable as CEO and chairman. This arrangement empowers Musk with veto authority over board composition and corporate decisions, limiting traditional shareholder influence and oversight.

Such concentration of control diverges sharply from typical public company standards, reducing mechanisms for accountability. Provisions including mandatory arbitration for shareholder disputes and restrictions on governance proposals further curtail investor rights. While the prospectus frames these measures as preserving operational agility for breakthrough innovations, they raise concerns regarding corporate governance and risk management resilience.

Market analysts and governance experts caution that this model may deter investors sensitive to the lack of checks and balances, particularly given Musk’s extensive commitments across multiple enterprises and the technical complexities inherent in SpaceX’s ambitious projects. However, many investors simultaneously view Musk’s visionary leadership as a key value driver, illustrating a tension between governance risk and strategic confidence.

Understanding these intertwined regulatory and governance challenges is critical for anticipating how SpaceX will navigate public market scrutiny while advancing its expansive space exploration agenda. The following sections will explore how these factors interface with SpaceX’s funding priorities and the broader commercial space ecosystem.

3. The Evolving Landscape of Commercial Space Activities

Dominance of Private Investment Accelerating Innovation and Reducing Costs in Space Exploration

This subsection contextualizes the ascendancy of private capital within the commercial space sector, demonstrating how the overwhelming majority of funding now originates from non-governmental sources. It elucidates the operational efficiencies and accelerated development timelines achieved under private investment dominance, framing how this shift underpins broader trends in space innovation and commercial viability.

Private Capital Now Constitutes Over Three Quarters of Space Industry Funding

As of early 2026, private investment accounts for approximately 77% of total funding in the global commercial space industry. This figure reflects a fundamental structural transformation where venture capital, private equity, and corporate investment decisively eclipse traditional government expenditure as the primary financial engine of space activity. The predominance of private funding extends across launch services, satellite manufacturing, and space infrastructure development, underpinning a vibrant ecosystem of startups and established firms.

This overwhelming share of private capital inflows signals a market-driven orientation for space sector growth, favoring scalability, diversified business models, and shareholder value. It also indicates intensified investor confidence in space ventures’ commercial viability, fueled by successful technology demonstrations and revenue-generating satellite constellations.

Cost-Effectiveness and Accelerated Timelines of Private Sector Space Projects

Compared with government-managed space programs, privately led projects consistently deliver on more aggressive development milestones while achieving significant cost reductions. The commercial imperative compels private firms to optimize design cycles, embrace reusability, and leverage rapid iteration techniques. These approaches have led to demonstrated reductions in launch costs and time-to-market for novel space systems.

For example, the iterative development of reusable launch vehicles and modular satellite platforms enables compressed production schedules, sometimes achieving design refresh rates within 18 months. This tempo contrasts starkly with lengthier government-led timelines, which often extend due to bureaucratic processes and risk-averse contracting. The agility of private enterprises also facilitates responsiveness to changing market conditions and innovation-driven pivots.

Private Sector Agility Catalyzes Technological Maturation and Market Expansion

Beyond cost and schedule advantages, private capital fosters a competitive environment conducive to rapid technology maturation. Startups and mid-cap companies attract dedicated venture funding, accelerating the development of new satellite communications technologies, propulsion systems, and in-space services. This competition drives down unit costs and broadens deployment scale, fueling downstream commercial demand.

Moreover, private-sector dominance has reshaped the space industrial landscape by relocating strategic initiative-setting from government agencies to entrepreneurial firms. As a result, the commercialization of cislunar infrastructure, Earth observation, and broadband constellations progresses along market-driven trajectories rather than exclusively governmental directives. This paradigm shift expands the addressable market and invites broader investor participation, reinforcing a sustainable growth cycle.

Having established the primacy of private investment and its positive implications for innovation and cost dynamics, the report now transitions to assessing how this evolving investment landscape interacts with competitive dynamics in the emergent lunar economy, particularly underpinned by NASA’s strategic initiatives.

Competitive Dynamics and Market Formation in the Emerging Lunar Economy

This subsection analyzes the current competitive landscape shaping the lunar economy as it evolves under NASA's open procurement approach. It examines contract awards between 2025 and 2026, details the role of established prime contractors, and highlights the emergence of innovative companies energizing lunar transport, habitat, and service capabilities. Understanding these dynamics provides crucial insight into how a commercial lunar ecosystem is rapidly maturing, driven by government demand and private sector ingenuity.

Recent Lunar Delivery Contracts Reflect Vibrant Competition

Between 2025 and 2026, NASA continued to allocate multiple fixed-price, milestone-based lunar delivery contracts under its Commercial Lunar Payload Services (CLPS) program, fostering robust competition among private companies. Notably, task orders valued in the hundreds of millions of dollars were awarded to firms including Blue Origin, Firefly Aerospace, Astrolab, and Lunar Outpost. These contracts focus on delivering robotic landers, rovers, and payloads to scaffold Artemis missions and expand lunar surface capabilities.

This procurement strategy incentivizes innovation by requiring companies to co-invest and compete on system design, accelerating technology readiness and cost efficiency. The competitive environment is underscored by a growing backlog of delivery service contracts and payload deployments linked to CLPS providers. Such vibrancy signals an ongoing shift from sole reliance on government contractors toward a diversified commercial lunar marketplace.

Prime Contractors Maintain Strategic Lunar Services Market Share

Established aerospace contractors maintain a notable presence in lunar surface support and infrastructure development. Companies such as Lockheed Martin and The Charles Stark Draper Laboratory hold key roles in supporting NASA’s Artemis program through systems integration and technology development. Their involvement often complements the activities of smaller commercial firms by providing critical engineering and program management capabilities.

While prime contractors maintain steady contracts, their market influence is tempered by the emergence of nimble commercial entrants that have demonstrated lunar delivery proficiency. The established contractors’ experience and scale confer reliability advantages, crucial for NASA's mission assurance, yet the evolving market structure promotes a multi-provider ecosystem to reduce dependencies and foster sustainable lunar economic growth.

Emerging Companies Driving Innovation in Lunar Transport and Habitat Services

A cohort of smaller, agile companies has gained prominence by developing specialized lunar transport vehicles and surface mobility systems. Companies such as Intuitive Machines and Firefly Aerospace have achieved successful lunar landings and maintain substantial contract backlogs, positioning themselves as leaders in commercial lunar payload delivery. Their technological innovations and operational successes validate the commercial viability of lunar transport services.

Alongside transport providers, firms focused on lunar habitats and infrastructure—exploring expandable habitats and in-situ resource utilization technologies—are beginning to define new market niches. This growing base of innovative participants fosters a dynamic ecosystem where competition stimulates rapid advancement of key technologies, thereby accelerating the timeline for establishing a sustainable human presence on the Moon.

Taken together, the competitive landscape of 2025-26 highlights a lunar economy progressively shaped by diverse commercial actors complementing traditional prime contractors. This evolving ecosystem, driven by NASA’s open contracting and milestone-based payments, creates momentum toward a sustainable lunar market with expanding opportunities across transport, habitats, and surface services.

4. Integration of Advanced Technologies in Space Operations

Strategic Synergies and Operational Integration of SpaceX and xAI for Enhanced Space Missions

This subsection analyzes the strategic rationale, implementation timeline, and operational impacts of the merger between SpaceX and xAI. It focuses on how this integration leverages artificial intelligence to improve mission autonomy, optimize resource allocation, and enhance SpaceX’s space and lunar exploration capabilities, while addressing resource competition concerns with co-owned ventures such as Tesla.

Investment Scale and Timeline of SpaceX-xAI Integration

The consolidation of SpaceX and xAI represents a major strategic investment designed to fuse AI capabilities directly with space operations. As of mid-2026, this integration has been backed by capital injections aligned with SpaceX’s upcoming IPO, which is expected to raise up to $50 billion, supporting accelerated deployment and scaling of AI-powered space infrastructure. Core AI elements and data processing neural architectures from xAI have been earmarked for full operational integration within a 6 to 12 month development window, enabling near-term adaptation into existing launch and satellite command-and-control systems.

This timeline reflects a focused approach prioritizing rapid embedding of AI-driven edge computing and autonomous decision-making modules aboard Starship and the Starlink satellite network. The scale of integration effort surpasses typical tech mergers by emphasizing real-time, on-orbit autonomy, and deep learning application directly affecting mission-critical functions.

Key AI Applications Driving Lunar and Orbital Operations Efficiency

The integration leverages xAI’s Grok neural architectures for advanced telemetry analysis, anomaly detection, and autonomous fault correction within SpaceX’s satellite constellation and lunar landing systems. By embedding edge AI capabilities into satellites, the system enables milliseconds-scale detection and mitigation of operational anomalies such as debris avoidance, solar weather interference, and thruster calibration errors without latency delays inherent in Earth-based processing.

On the lunar surface and transit stages of Artemis missions supported by SpaceX’s Starship, AI is being deployed to optimize life-support systems, real-time environmental monitoring, and resource utilization, including in-situ resource processing feedback loops. Additionally, AI-driven algorithms facilitate dynamic mission planning, autonomous navigation, and predictive maintenance, significantly enhancing reliability and reducing the need for constant human intervention.

These advances constitute a critical competitive advantage, allowing SpaceX to refine mission operations complexity and scale scheduled lunar logistics with higher confidence and reduced operational costs.

Resource Allocation Dynamics and Competitive Considerations with Tesla and Other Ventures

The merger catalyzes a strategic realignment of AI resources within Elon Musk’s enterprise portfolio, prioritizing synergy between space and AI-driven autonomy. Although there has been speculation about fully integrating Tesla into this ecosystem, as of mid-2026, Tesla operates independently, with separate resource allocation for its AI programs. This separation mitigates risks of shareholder dilution and antitrust concerns stemming from cross-industry market dominance.

Nonetheless, shared technological insights and computational infrastructure have produced indirect benefits for Tesla’s autonomous vehicle AI, including leveraging satellite connectivity and real-time AI workloads facilitated via Starlink networks. The anticipated consolidation of core AI expertise within SpaceX and xAI allows for optimized capital deployment, reducing duplicated R&D expenses and accelerating innovation cycles without compromising Tesla’s distinct operational mandates.

However, the competitive tension points remain. SpaceX’s prioritization of AI-driven space mission technology necessitates careful governance to ensure balanced investment across divisions while maintaining compliance with regulatory scrutiny associated with the upcoming IPO and potential market concentration.

Having established the strategic integration and operational use cases of AI within SpaceX's space missions, the report will next explore the broader implications of this merger on SpaceX’s financial positioning and the wider commercial space sector.

Orbital AI Data Centers and High-Performance Computing in Space: Assessing Technical Ambitions and Commercial Viability

This subsection examines SpaceX’s proposal to deploy orbital artificial intelligence (AI) data centers as a transformative extension of its space infrastructure ambitions. Positioned within the broader discussion of advanced technologies integration, it explores the scale, power capabilities, and technical risks associated with these space-based high-performance computing (HPC) platforms. Furthermore, it evaluates the economic rationale underpinning these ventures in the context of current technological and market conditions as of mid-2026.

Proposed Constellation Scale and Power Specifications for Orbital AI Data Centers

SpaceX envisions a modular constellation of satellites designed to host AI and HPC workloads, leveraging the unique orbital environment to provide continuous solar power and thermal management advantages unavailable on Earth. The constellation size under consideration exceeds several hundred satellites, each outfitted with high-specific-power, radiation-tolerant solar arrays and advanced energy storage systems to sustain near-continuous operations despite eclipse periods inherent in low Earth orbit (LEO). Typical orbit altitudes range between approximately 500 and 2,000 kilometers, balancing trade-offs among latency, collision risk, and solar exposure. At the lower edge, orbits enable reduced uplink power and latency critical for real-time AI applications but face increased debris congestion, whereas higher orbits offer greater solar continuity and reduced collision risk at the expense of increased signal latency and shielding requirements. The power architecture is engineered for rapid workload scheduling and intelligent thermal management to mitigate temperature extremes, with conservative power density metrics that align with the constraints of space-grade hardware reliability.

Technical Risks and Engineering Challenges in Deploying Orbital Data Centers

Despite the promising environmental conditions, the technical challenges of operating AI data centers in space remain formidable and are explicitly recognized by SpaceX in its IPO filings. Key risks include the reliability of radiation-hardened high-density computing hardware in an unforgiving thermal regime characterized by wide temperature fluctuations possibly reaching from +120°C to -250°C within a single orbit. Thermal dissipation mechanisms must overcome the vacuum's lack of convection, relying solely on radiative heat transfer and carefully engineered heat spreading systems. Another critical challenge lies in sustaining continuous power during transient eclipse phases, requiring redundant solar array configurations and high-performance energy storage. Additionally, deployment and maintenance constraints limit physical intervention post-launch to software updates, demanding exhaustive pre-deployment testing and fault tolerance measures. The crowded nature of preferred orbital altitudes exacerbates collision risk and necessitates sophisticated maneuvering and active debris mitigation systems. Lastly, reliable high-throughput communication links must be sustained despite the dynamic orbital environment to effectively integrate the orbital data centers with terrestrial networks.

Commercial Viability and Market Demand Forecasts for Orbital AI Infrastructure

While the technical foundation for orbital AI data centers is ambitious, SpaceX’s filings cautiously define these endeavors as unproven from a commercial perspective, emphasizing considerable space-related risks that may impede return on investment. Market demand analyses highlight niche scenarios where orbital computation offers distinct advantages—such as near-continuous solar energy availability, geopolitical resilience, and proximity to space-generated data—that terrestrial facilities cannot replicate. Yet, the high capital intensity and operational complexity currently restrict widespread market readiness. Financial projections remain speculative, reflecting the nascent stage of space-based HPC solutions and dependence on continued advances in hardware miniaturization, radiation tolerance, and launch economics. Industry observers note that the commercialization of such infrastructure will rely heavily on securing initial anchor customers with latency-insensitive, compute-intensive workloads that benefit from the unique space environment. These likely include space situational awareness, Earth observation data processing, and distributed space network management. The broader application in global AI service provision awaits breakthroughs in cost reduction and reliability over coming years.

The distribution of IPO proceeds further illustrates SpaceX’s strategic priorities in funding allocation, with 60% dedicated to Starship development, 25% directed towards lunar mission contracts, and 15% reserved for infrastructure and operations support. This funding breakdown emphasizes the company’s commitment to bolstering core transport capabilities and mission partnerships, which directly underpin the feasibility and scaling of ambitious orbital AI infrastructure projects within its broader space ecosystem [Chart: Funding Distribution for SpaceX IPO Proceeds].

Understanding the complexities and constraints of orbital AI data centers provides critical context for evaluating how SpaceX’s IPO proceeds might be allocated toward advancing such frontier projects, while also setting realistic expectations about near-term commercial outcomes in space-based computing. This lays the groundwork for assessing the broader strategic and financial implications of SpaceX’s evolution as a public company.

5. Conclusion: Charting the Course for Sustainable Space Commerce

Validation of Economic Potential Through IPO Catalyst

This subsection evaluates how SpaceX’s upcoming IPO serves as a key milestone validating the financial viability of commercial space ventures. It ties investor sentiment and capital market activity to NASA’s lunar development plans, illustrating the IPO’s pivotal role in accelerating investment and infrastructure growth in the near term.

Investor Reaction to SpaceX IPO Announcement and Market Sentiment

The market response to SpaceX’s IPO announcement has been broadly enthusiastic, signaling robust confidence in the company’s economic potential and strategic direction. Despite a complex geopolitical and macroeconomic backdrop, institutional and retail investors alike express strong interest, anticipating that the IPO could unlock substantial public capital inflows into the space sector. This enthusiasm has also sparked secondary market rallies in related aerospace and technology equities, demonstrating a contagion effect elevating space industry valuations more generally.

However, there remains cautious skepticism regarding governance structures and potential conflicts arising from Elon Musk’s intertwining leadership across multiple ventures. Some investor factions have voiced concerns about limited shareholder rights and the prospective dilution effects due to cross-company capital flows. While such governance risks may temper initial market exuberance, the overall investor appetite underscores recognition that SpaceX is charting a new frontier in commercial space enterprise financing.

Projected Capital Raised and Financial Scale Validating Commercial Space Activities

SpaceX is targeting a historic IPO raise estimated at approximately $75 billion, with a market valuation hovering around $1.75 trillion. This issuance stands to be the largest initial public offering ever recorded, eclipsing the previous global benchmark. The sheer magnitude of the capital raise not only reflects confidence in SpaceX’s current assets—ranging from launch services and satellite internet to AI operations—but also embodies substantial validation of the commercial space market’s growth trajectory.

The anticipated capital influx will substantially bolster SpaceX’s balance sheet, enabling accelerated development of space infrastructure. Such a financial scale affirms the viability of space exploration and satellite internet provision as mainstream commercial assets rather than niche government endeavors. The record-setting valuation further positions SpaceX as a transformative player poised to reshape both public markets and space industry economics.

NASA's Moon Base Timeline and Funding: Near-Term Context Supporting Commercialization

NASA’s lunar base initiative is currently progressing through its initial phase, focused on robotic exploration and technology validation, with early habitation systems planned for deployment within the coming five years. Despite facing a proposed budget reduction for fiscal year 2027, NASA remains committed to incremental lunar infrastructure build-out aimed at enabling sustainable human presence near the Moon’s South Pole.

The agency’s $20 billion investment plan spans three phases culminating in a permanent, expansive lunar settlement. This phased approach ensures that commercial partners, including SpaceX, play a critical role in delivering cargo, power, communications, and habitation capabilities. The timing of SpaceX’s IPO dovetails strategically with NASA’s near-term plans, suggesting a synergistic ecosystem where public funding and private capital coalesce to expedite lunar development.

Impact of IPO Proceeds on Accelerating Lunar Infrastructure and Commercial Space Growth

The substantial capital raised through SpaceX’s IPO is expected to fuel key programs integral to lunar infrastructure, including maturation of the Starship system optimized for heavy lunar cargo delivery and support of emerging commercial payload service contracts. This financial reinforcement enhances SpaceX’s ability to compete effectively for NASA and Department of Defense lunar contracts and to expand Starlink satellite deployments that support communications for lunar activities.

Beyond direct technological development, the IPO’s success will likely catalyze broader investor interest in space commerce, unlocking secondary funding streams for smaller commercial players and innovation ventures. By validating commercial space as a robust investment class, SpaceX’s public offering stands to accelerate the establishment of a sustainable lunar economy, enabling scientific research, exploration, and eventual resource utilization in a manner aligned with NASA’s strategic roadmap.

With the economic validation of space commerce solidified through SpaceX’s landmark IPO, the subsequent analysis will explore the broader strategic implications this event poses for space industry finance, regulation, and competitive dynamics.

Conclusion

The analysis confirms that SpaceX’s IPO represents a landmark financial event that not only validates the commercial viability of large-scale space enterprise but also serves as a catalyst for accelerating technological advancement and mission execution cadence. With a projected valuation near $1.75 trillion and an anticipated capital raise of approximately $75 billion, SpaceX is positioned to enhance Starship’s readiness for crewed lunar missions, solidifying its role as a strategic partner in NASA’s Artemis program and the broader lunar economy.

NASA’s structured, phased lunar base development strategy underscores a pragmatic progression from robotic exploration to permanent human habitation, leveraging the unique solar advantages of the Moon’s South Pole to enable sustainable energy solutions. The complementary CLPS program has successfully introduced a competitive commercial marketplace for lunar payload delivery, essential for scaffolding Artemis mission architectures and reducing government programmatic risks through diversified service providers.

Together, these developments signify an evolving paradigm wherein commercial innovation and public agency frameworks are inextricably linked to the successful establishment of a permanent lunar presence. The infusion of private capital via SpaceX’s IPO is anticipated to amplify investment flows into lunar infrastructure, enhance operational capabilities, and foster a robust ecosystem of commercial space activities grounded in public-private collaboration.

Looking forward, maintaining this momentum will require vigilant navigation of regulatory challenges, robust governance structures, and sustained technological maturation to ensure mission reliability and investor confidence. Continued alignment of corporate capital deployment with NASA’s evolving mission timelines will be critical in translating current technological promise into realized lunar and broader space exploration objectives, thereby charting a sustainable course for the future of space commerce.

References

- A Galaxy of Opportunities - KPMG agentic corporate services

- SpaceX IPO May 22: Elon Musk's Risk Factor Reshapes Markets | Meyka

- SpaceX, the sprawling company targeting the stars, Mars and an IPO

- Bound for Mars, Elon Musk's SpaceX unveils filing for blockbuster IPO

- SpaceX IPO Filing Signals Potential Wall Street Transformation in 2026

- AST SpaceMobile Shares Plummet: What’s Causing the Satellite Company’s Decline?

- Good News for Space Stocks: NASA Wants 30 Moon Landings

- Good News for Space Stocks: NASA Wants 30 Moon Landings | The Motley Fool

- Exploring the space economy: The present and future of ...

- NASA unveils Moon Base plan for sustained human presence on lunar surface-Xinhua

- SpaceX IPO Could Reshape the Space Industry as Investors Weigh Musk’s Vision and Risks

- SpaceX IPO 2026: Top Space Stocks & ETFs to Watch

- The Global Impact of a SpaceX Public Offering | AI Stocks

- Traded: Venture Capital 🦄 on Instagram: "SPACEX OFFICIALLY FILES FOR IPO SpaceX has officially filed for an IPO, setting Elon Musk’s space and AI empire on course for what could become one of the largest public market debuts in history. The filing reveals new details about SpaceX’s financials and the company’s next phase of growth across

- SpaceX IPO: Aiming for Historic Market Debut

- Musk's SpaceX Files For Blockbuster IPO As Starlink Profits Offset Deep Company Losses | IBTimes

- SpaceX prospectus eyes Moon refuelling, life on Mars and asteroid mining

- SpaceX IPO Prospectus — Summary | ABI Analytics

- SpaceX says unproven AI space data centres may not be commercially viable, filing shows

- SpaceX Weighing IPO Filing: Report Signals Potential Starlink Spin-Off

- The space economy needs these 2 milestones to become solid

- High Gear Moonbase Program Kicks Off With 30 Robotic Moon Missions Starting in 2027 and Nuclear Powered Base by 2030 | NextBigFuture.com

- Investment Insights into SpaceX and Its Impact on the Aerospace Sector

- 5-8-19 HSSTC Space Exploration Hearing NASA Final 2

- MLQ.ai | AI for investors

- Bridging the Cosmos and Code: Inside the SpaceX-xAI Integration | AI Stocks

- Economic Growth and National Competitiveness Impacts of ...

- NASA’s Artemis II launch sparks gains for lunar-linked stocks

- SpaceX Poised for Historic IPO in 2026: Will They Reach the Stars or Get Burned in the Atmosphere? | AI News

- SpaceX Rockets into AI: The $230 Billion Fusion with xAI | AI News

- Resilient Multi‑Agent AI: A Strategic Blueprint for Trustworthy Coordination in Adversarial Environments

- Overcoming AI Implementation Challenges in Enterprise Environments | Blog | Cubet

- PDF The Transformative Impact of AI on Enterprise Cloud Integrations and ...

- PDF The Evolving Landscape of Artificial Intelligence in Cancer Research ...

- AI Pricing Models: Complete Cost Breakdown & Budget Planning Guide

- PDF Unit Economics of AI

- How much money can conversational AI save companies by 2026?

- AI Integration Cost Calculator for Budgeting

- Legacy Systems Are Draining Your Profits: The Urgent Need for AI Integration

- Open Source Intelligence (OSINT) Market: Unveiling Growth Drivers and Strategic Imperatives

- SpaceX debut draws a crowd, but few recent hot IPOs outpace the market

- Interested in Investing in SpaceX Before the IPO? Check Out These 5 Funds That Already Hold Shares.

- SpaceX IPO 2026: How to Buy SPCX Stock & $1.75T Valuation Analysis

- Prediction: Tesla Stock Could Go Parabolic After June 12. Here's Why. | The Motley Fool

- How Big Could SpaceX And Anthropic Get? The Latest Prediction Market Bets Size Up Pre-IPO Valuations.

- Investors Split on Stock Outlook Amid Inflation Concerns

- Viewpoint

- Rs 16.77L cr gone! Market crash over 4 days leaves investors with deep losses; what's next?

- Think Like Warren Buffett as You Near Retirement: Stop the Needless Risks

- The world's hottest stock market just minted a trillion-dollar tech giant

- STATE OF THE SPACE INDUSTRIAL BASE 2021

- Economic Implications of the European Union Space Act

- Is Stellar Aerospace's New Contract a Game-Changer for Mid-Cap Space Stocks

- PDF Start-Up Space 2025

- Space Technology Market Size, Share | Growth Report [2034]

- Start-Up Space Investment 2025 and the New Shape of Private Space Capital - New Space Economy

- Space Market Size, Share [2035] | Research Report

- ESA Report on the Space Economy 2024

- PDF Regional Transformational Opportunities in the Highlands and Islands

- Skyroot Aerospace CEO Targets One Launch a Month from New Facility, Opening up the next era of space in India at Arkam Annual Meet 2026

- SpaceX IPO Buzz Sparks Global Market Excitement - NEPSE Trading

- Nvidia Projects $1 Trillion in GPU Sales by 2027

- SpaceX files to go public in huge IPO deal

- SpaceX IPO 2026: What History Says About The Stock’s Debut And Long-Term Performance

- SpaceX IPO Created a Stir as Elon Musk Tightens Grip and Strips Investor Rights in Historic Market Debut | IBTimes UK

- The $300 Billion Convergence: How SpaceX’s xAI Merger Reshapes Musk’s Corporate Empire

- Elon Musk's Mega Merger: SpaceX and xAI Join Forces in a Bold Move Towards the Future! | AI News

- Nvidia Poised to Exceed Fiscal 2027 Revenue Estimates

- SpaceX IPO Plan: What Investors Need to Know Before July 2026

- The Procure Space ETF®: Space Economy Year-End Review 2025

- Additive manufacturing for space applications

- AI in Space Operation Market Size, Share & Forecast [2034]

- AI Impact Analysis on the Future of the Space Industry

- Moon Trades Technologies: Building the future of climate-conscious mining innovation - Invest Durham

- editors

- Firefly Aerospace Inc. (FLY) Q1 FY2026 earnings call transcript

- PDF Revolutionizing Satellite Communication With Artificial ... - Jetir

- Space AI Leveraging Artificial Intelligence for Space to Improve Life on Earth

- NASA’s Historic Artemis II Launch Paves Way for Moon Exploration - Innovation & Tech Today

- SpaceX Eyes $1.75T IPO, Public Space Stocks Surge

- SpaceX IPO 2026: How to Buy SPCX Stock & $1.75T Valuation Analysis

- SpaceX IPO 2026: Space Venture Capital Exit Math Rewritten

- SpaceX’s $1.75T IPO Filing: How the World’s Largest Listing is Re‑Rating Space Equities

- The Ripple Effect of a SpaceX IPO on Aerospace Stocks | AI Stocks

- Helio Highlights Strategic Positioning Within Expanding Space Market Amid Broader IPO Surge

- Biggest IPO wave in history promises US$3 trillion in value — with no profits

- SpaceX IPO 2026: Everything You Need to Know About the Largest IPO in History | New Space Tracker

- Analysis-How the math works on a $1.75 trillion SpaceX valuation

- SpaceX IPO Guide: $75B Filing This Week Explained | Breaking Update | News | informedclearly

- The relationship between savings and economic growth at ...

- ALTERNATIVE INVESTMENTS: A PRIMER FOR ...

- 25 Economic Analysis and Policy Studies

- Regional Waste Management – Inter-municipal ...

- Regional-Waste-Management-Inter-municipal-Cooperation ...

- Taking Stock of PPP and PFI Around the World

- PDF Revisiting the Cost-benefit Calculus of The Misbehaving Prosecutor ...

- CAPITAL IN THE TWENTY-FIRST CENTURY - Thomas Piketty

- PDF WaterSense at Work Section 1.2 Water Management Planning

- PDF Delays and Cost Overruns in Infrastructure Projects in Cotabato City ...

- SpaceX Set to Launch IPO - Inside Towers

- SpaceX IPO plans include unusually large voting share for Elon Musk

- SpaceX IPO filing brings Musk's interplanetary ambitions to Wall Street | Reuters

- SpaceX to explore "the true nature of the universe" as it plans IPO

- SpaceX files for IPO as Elon Musk's rocket company preps for biggest-ever public market debut

- SpaceX IPO Timeline Accelerates To June 12

- SpaceX Stock: Should You Buy the Biggest IPO Ever?

- SpaceX IPO Project Unlimited Analysis Reviews Reported S-1 Timeline, Orbital AI Data Center Risks, and Infrastructure Market Context

- SpaceX Files for Record $75 Billion IPO, Targeting $1.75 Trillion Valuation | Octagon AI

- SpaceX IPO Aims to Raise $75 Billion -- and 1 AI Stock Should Be a Big Winner From It | The Motley Fool

- 6 ways to use AI in collaborative tools for smarter project management

- PDF Incorporating AI into construction management: Enhancing efficiency and cost savings

- PDF The Future of Construction Planning: Integrating AI for Smarter Decision-Making and ...

- PDF Adaptive Scheduling: Applying AI and Machine Learning to Optimize ...

- PDF Leveraging AI in managerial decision-making: driving innovation and ...

- PDF A comprehensive review on humanoid robots: perspectives from academia ...

- Elon Musk Surprises Everyone by Merging SpaceX With xAI. Is Tesla Next? - 24/7 Wall St.

- Tesla's Model 2: Pioneering AI Innovations in Automotive and Healthcare Sectors

- Revolutionizing the Future: Tesla Model 2, AI Innovations, and Their Transformative Impacts

- PDF NPL - Reallocation of IPO Proceeds - 2024 08 09 - Singapore Exchange

- EY Global IPO Trends 2024

- SEC.gov | Initial Public Offerings (IPOs)

- Innovation Economy update - 2024

- A Review of IPO Activity, Pricing, and Allocations

- PDF 2025 USA IPO INSIGHTS - uniqus.com

- PDF IPOs-Underwriting - Websites

- Fostering Financialisation - Nippon India Mutual Fund

- Initial Public Offerings: Updated Statistics

- How to Participate in an Initial Public Offering (IPO) - Fidelity

- PDF Defect Repair Cost and Home Warranty Deposit, Korea

- PORTFOLIO INSIGHTS — Learning from Case Studies

- PDF A Retrospective Analysis of Distributed Solar Interconnection Timelines ...

- of Public Investment Management - World Bank Document

- Manpower utilization patterns in project management

- UK's £500M Sovereign AI Fund: 7 Companies and the 12B Race [2026]

- Government Backed Advanced Public Development Projects Transform Strategic Resource Security

- U.S. Oil Production Leads the World, Surpassing Russia and Saudi Arabia | Shale Magazine

- NASA reveals new details on plan to build a base on the moon

- Moon base plans revealed as Nasa chief says ‘the grand return is close at hand’

- NASA lays out moon base plans with landers, buggies and drones at the top of the list

- NASA's Moon Base Plans Revealed, And They Include Landers, Buggies And Drones

- NASA targets permanent human living by 2032 at sprawling city-sized moon base

- NASA undergoes restructuring to align with the US National Space Policy

- Artemis II Was a Rousing Success, So What's Next for NASA? - CNET

- Japan to focus on lunar rover after US halts moon space station | South China Morning Post

- NASA Artemis II Day 7: Heading Home After Breaking Apollo 13's Record for Space Travel

- SpaceX’s next-gen rocket is the key to its sky-high valuation, early investor says: ‘Starship also enables all kinds of frontier markets’

- SpaceX IPO and the Big Bang Bubble - The HinduBusinessLine

- Bigger, Faster, Stronger: 3 Reasons Why Starship V3 Will Be a Spaceflight Game Changer

- The Commercial Lunar Economy Field Guide - Air University

- Canada Centre lines up CMs' US to students

- SpaceX Public Investment Guide.pptx

- SpaceX: Pioneering Mars Colonization Dreams

- SpaceX's Mars Vision: Challenges and Innovation

- SpaceX's Ambitious Mars Colonization Plan

- SpaceX's Path to Mars Colonization

- Expendables

- 2023 State Competition Landscape

- NAVSTAR GPS USER EQUIPMENT INTRODUCTION

- Federal Communications Commission FCC 22-91

- PDF Satellite Cybersecurity Reconnaissance: Strategies and their Real-world ...

- China's Remote Sensing

- PDF Network topology design at 27,000 km/hour - GitHub Pages

- PDF Efficient Topology Design for LEO Mega-Constellation Using Topological ...

- PDF LEO-PNT Performance Metrics: An Extensive Comparison Between Different ...

- SpaceX Starship: Artemis, Moon Flights & Mars — What's Confirmed

- GAO-25-107591, NASA: Assessments of Major Projects

- The evolution of the space sector: an insight into the new ...

- GAO-24-106767, NASA: Assessments of Major Projects

- How Much Did SpaceX Raise? Funding & Key Investors | TexA | TexAu

- the POLITICS AND PERILS OF SPACE EXPLORATION who will compete, who will dominate?. [2 ed.] 9783030568351, 3030568350 - DOKUMEN.PUB

- PDF Attachment a Technical Information to Supplement Schedule S

- SpaceX Will Pay Elon Musk To Conquer Mars — No, Really, It's In The Filing

- Mid-July 2025 Global Tech and Business Roundup: Musk’s Empire, Startup Struggles, and Industry Dynamics

- From Moon to Mars: NASA’s Strategic Shift in Space Exploration Under the Trump Administration

- NASA picks Blue Origin, other space firms for moon missions

- Record margins, NATO training deals as Volatus boosts defence investment

- The Bridge Monthly SpaceTech Update

- NGA Expands Access to Commercial Vendors for Satellite Data, AI Analytics

- Contracts for April 8, 2026 > U.S. Department of War > Contract | U.S. Department of War

- NASA's Lunar Exploration Program Overview

- PDF In-Space Economy in 2025 - Analysis and Deep Dives into In-Space ...

- MoD fully utilises capital outlay of ₹1.86 lakh cr for FY 2025-26

- Elon Musk’s SpaceX set for biggest IPO in history: What a $1.75 trillion valuation means for markets

- Planet Ventures. Building a Portfolio Beyond Earth. | Top Stock Report

- Space Investment Quarterly

- Next frontier for ETFs: Getting investors deeper into space

- Ensuring PNT resilience: A global review of navigation ... - STIG

- SpaceX IPO push, Artemis 2 launch draw attention to space-related stocks and ETFs

- PDF Space-x. Pre-ipo

- Elon Musk's SpaceX launches upgraded Starship - ABC News

- SpaceX IPO: everything you need to know | Capital.com EU

- ARK’s Expected Value For SpaceX In 2030: ~$2.5 Trillion Enterprise Value

- SpaceX Public Investment Guide M33 (Q1'24 Update).pptx

- SpaceX Stock Analysis: Valuation Metrics and Financial Health | AI Stocks

- With Starship Flight 10, SpaceX prioritized resilience over perfection | TechCrunch

- NASA should consider switching to SpaceX Starship for future missions - Reason Foundation

- SpaceX's Mars Ambitions: Challenges Ahead

- SpaceX's Mars Colonization Strategy Unveiled

- Global Space Governance: Key Proposed Actions

- PDF NASA Systems Engineering Handbook

- MAY 2026

- Big Tech eyes orbital data centers for "near continuous" solar power

- Star Catcher | The orbital data center power problem — and how to solve it

- PDF Risk Management of Remote Deposit Capture - FDIC

- Techmeme: Netherlands-based ASM, whose deposition tools are used to make advanced chips, projects Q2 revenue of ~€980M, above €886.8M est., driven by AI demand (Sarah Jacob/Bloomberg)

- Techmeme: LinkedIn names COO Daniel Shapero as its new CEO, succeeding Ryan Roslansky, who will retain his position as EVP at Microsoft (Jordan Novet/CNBC)

- Techmeme: Google says 75% of new code created inside the company is now generated by AI and reviewed by human engineers, up from 50% last fall (Hugh Langley/Business Insider)

- PDF On Underwater Data Centers: Surveillance, Monitoring, and Environmental Management in ...

- March 24, 2021 - 10-K: Annual report pursuant to Section 13 and 15(d) | Abeona Therapeutics Inc. (ABEO)

- 424B3 - 05/24/2024

- Wind and Solar Projects Face Increased Oversight as Clean Energy Incentives Fade

- PDF Risk Management in Land Development: Strategies for Mitigating Site-Related Uncertainties

- Restorative Dental Materials Market Size, Growth & Forecast [2034]

- Gilead to Acquire Tubulis Adding Potentially Best-in-Class Antibody-Drug Conjugate and Next Generation Platform to Further Strengthen Oncology Pipeline

- Cross-Border M&A Valuation Under Geopolitical Risk 2026 | US, UK & Australia | Synpact

- FDA's AI Regulation Shift: Innovation Versus Safety - PhysEmp

- Pharmaceutical R&D KPIs: Assessing Investment Prospects in Samjin Pharma

- Tesla's Robotaxi Initiative: Promises, Perceptions, and Prospects

- PDF NEW JERSEY DISPARITY STUDY - The Official Web Site for The State of New ...

- U.S.-Canadian Defense Industrial Cooperation

- A start of a Litany of Research Needs

- The European and Italian Space Ecosystems

- Ukraine

- South Korea's Kospi Records Worst Day Ever with 12% Plunge

- PDF Office of Inspector General - NASA

- NASA Outlines Preliminary Artemis III Mission Plans - NASA

- Jacksonville University The Cryogenic Complex

- Elon Musk’s SpaceX and Jeff Bezos’s Blue Origin in space race for Nasa’s next moon mission

- Artemis

- Timeline: Where is Artemis and how long will it take to get to the moon?

- PDF Aerospace Safety Advisory Panel 2025 Annual Report - NASA

- Dietary Supplements Market: Dynamics and Demand Forecast 2025–2032 | Education

- Blood Banking Media Market Forecast Points Higher Toward 2035 Driven by Cell Therapy Expansion - News and Statistics - IndexBox

- North Korea Agricultural Product Market (2025-2031) | Value & Outlook Growth

- An Essential Guide to Market Feasibility Study | Blackridge Research

- Market Feasibility Study: Uncovering Demand & Mitigating Risk

- Documenting the Inventive Process | Lemelson

- PDF The Role of Market Research in New Product Development

- PDF Resource Mobilization Manual

- defense logistics acquisition directive (dlad)

- Hydrogen Fuel Cells in Transportation

- Elon Musk's plan to keep complete control of SpaceX even after it goes public

- Musk to Hold 85.1% of SpaceX Voting Power After IPO

- SpaceX IPO gives Musk sweeping power and curbs shareholder rights

- Analysis-SpaceX IPO gives Musk sweeping power and curbs shareholder rights

- Exclusive: Only Elon Musk can fire Elon Musk from SpaceX, filing shows | Reuters

- New filing reveals only Elon Musk can fire Elon Musk from SpaceX

- Tesla’s Turning Point: Governance Strains, Tech Pipelines, and Musk’s Controversies in 2025

- Elon Musk in May 2025: From Waning Trump Bromance to Market and Legal Crossroads

- Elon Musk at the Crossroads: Innovations, Governance, and Government Service in 2025

- The future of the European space sector

- SpaceX stock is about to join this growing constellation of public companies building a space-based economy

- Start-Up Space

- A start of a Litany of Research Needs

- Humans may soon live and work on the Moon in groundbreaking 2030 plan

- Cislunar Security National Technical Vision

- Max Space unveils new expandable space habitat for the moon and beyond: 'We need real estate that is scalable' | Space

- ispace Announces Third-Party Allotment of New Shares to Kurita Water Industries | ispace

- [PDF] A methodical approach to the transfer and the integration of design ...

- NASA outlines phased Moon base strategy alongside National Space Policy overhaul

- NASA unveils ambitious $20 billion moon base strategy: What to know

- NASA unveils Moon Base plan for sustained human presence on lunar surface-Xinhua

- New 3D Lunar Maps Reveal Safe Artemis Landing Sites

- Solar Energy Perspectives

- No sunset in this city for the next 84 days. Where is it and why?

- The Sun will not set in this city for the next 84 days. What city is it and why? - India Today

- Time Cycles of Ancient Astronomy

- 1. ARISTOTLE'S COSMOLOGY

- The best photos from NASA's first moon mission in more than 50 years

- PDF NASA Futures Roundtables: Exploring Challenges and Opportunities for ...

- WIPO Technology Trends: Future of Transportation

- 2025’s Defining Currents: Autonomous Tech, Titans of Wealth, and Cultural Shifts

- SpaceX's Mars Dreams: Progress and Hurdles

- SpaceX's Mars Colonization Challenges and Goals

- SpaceX's Mars Colonization Blueprint

- Private 5G Market 2025-2030: Opportunities, Challenges, Strategies & Forecasts

- PDF Contractor Safety and Health Requirements for Prime and Subcontractors ...

- Annual Report of Activities Pursuant to Act 44 of 2010

- Business Status Business Name as of April 2024

- PDF 2024 GAO-OIG Act Report_FINAL_030724 - NASA

- [PDF] Acronyms.pdf - Defense Finance and Accounting Service

- 2014-15 Comprehensive Annual Financial Report ... - CalPERS

- JP 4-10, Operational Contract Support

- Acquisition-Certifications-Program-Handbook- ...

- PDF Briefing Book - NASA

- Nelson Mullins - Space Industry Litigation Trends for 2026

- CLPS Incorporation Announces Share Repurchase Program of Up to 1,000,000 Shares | The Manila Times

- The NASA Artemis Mission: Goals, Technology, and Timeline Explained - New Space Economy

- Country Partnership Framework for Haiti. - Documents & Reports

- Here's what has to happen if NASA wants to land on the Moon every month

- Stability and Change in Personality Disorders

- returning to the moon: keeping artemis on track hearing