Strategic Market Dynamics and Investment Insights: Nvidia’s AI Dominance, SpaceX’s Record IPO, and Institutional Crypto Adoption in 2026

Table of Contents

- Executive Summary

- Introduction

- 1. Executive Overview: Tech Titans and Crypto Shifts Driving Strategic Decisions in May 2026

- 2. Deep Dive: Nvidia’s AI Chip Leadership and Strategic Positioning in 2026

- 3. Roadmap to IPO: SpaceX’s Ambitious Path Toward a $1.75–$2 Trillion Valuation

- 4. Institutional Crypto Adoption: From Speculation to Strategic Allocation Frameworks

- 5. Macro Environment and Cross-Sector Implications: Trade Tensions, AI Integration, and Stablecoin Evolution

- 6. Synthesis and Strategic Recommendations: Prioritizing Opportunities Amidst Complexity

- Conclusion

Executive Summary

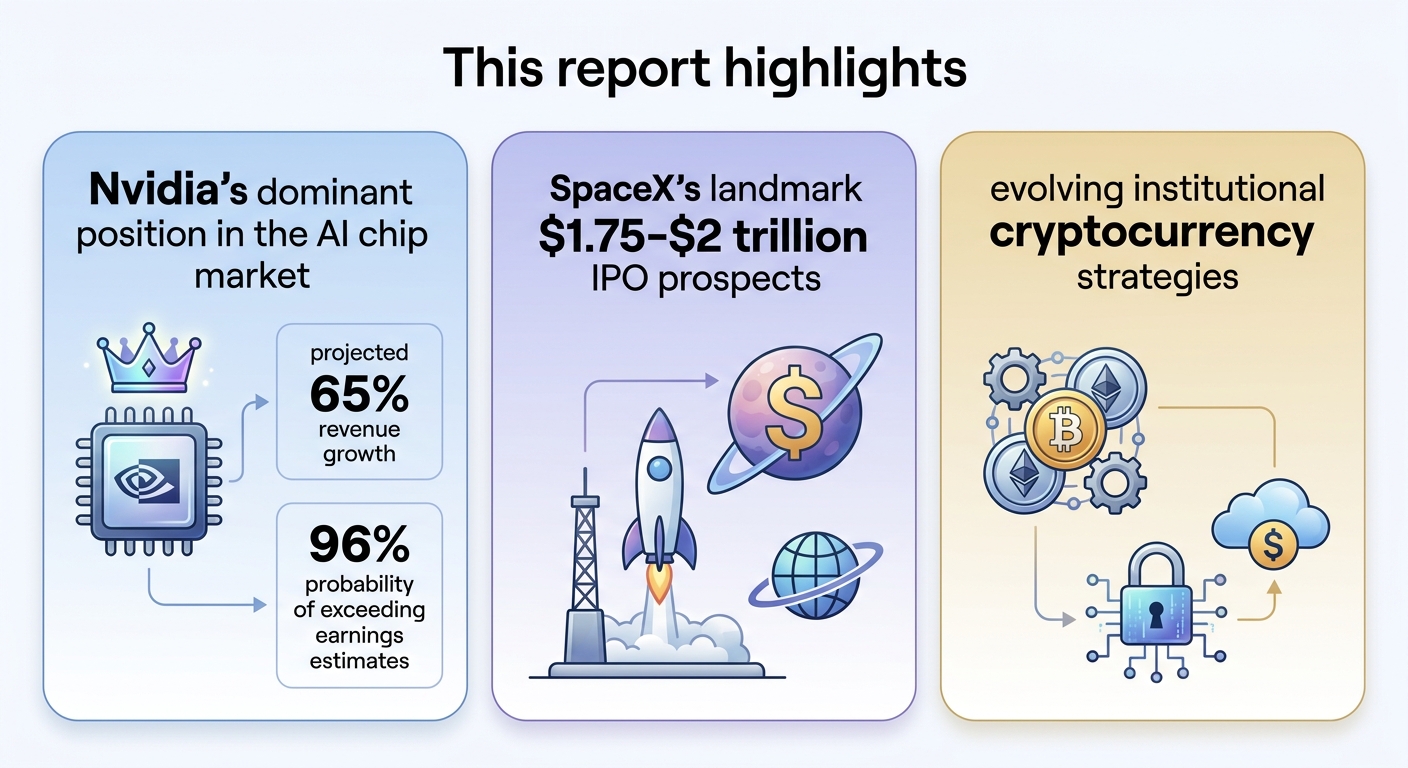

This report presents a comprehensive analysis of three pivotal market trends shaping strategic investment decisions in mid-2026: Nvidia’s commanding growth in AI semiconductor infrastructure, SpaceX’s imminent record-breaking IPO, and the accelerating institutional adoption of cryptocurrencies. Nvidia’s fiscal Q1 2027 outlook projects revenues nearing $79 billion, a 77% year-over-year surge supported by strong demand for Blackwell architecture AI chips. Despite competitive and geopolitical pressures, Nvidia maintains an estimated 81% share of the AI data center market with forward P/E ratios ranging between 24x and 26x. The company’s partnerships with IREN and Corning underscore strategic vertical integration, including a targeted deployment of 5GW AI data center capacity and substantial optical connectivity manufacturing expansions.

SpaceX’s highly expedited IPO, anticipated on Nasdaq by June 12, 2026, targets an unprecedented $75 billion raise and a valuation between $1.75 and $2 trillion, reaffirming its leadership in aerospace and orbital AI computing. Critical milestones include the $60 billion acquisition of AI coding platform Cursor post-IPO and integration of xAI assets. However, execution risks persist around orbital data center deployment, regulatory licensing, and energy provisioning. Institutional crypto investment continues its maturation trajectory, evidenced by Bitcoin ETF inflows surpassing $56 billion in Q1 2026 and expanding altcoin engagement, particularly in Solana and XRP. Regulatory frameworks such as MiCA and evolving SEC policies have catalyzed institutional portfolio integration, supported by advanced volatility-targeting strategies, tail-risk hedging, and tokenized yield products.

Introduction

In the rapidly evolving landscape of technology and finance, 2026 stands as a landmark year marked by transformative developments spanning AI semiconductor innovation, aerospace investment, and digital asset adoption. This report synthesizes critical intelligence concerning Nvidia’s sustained leadership in AI data center chips, SpaceX’s strategic public listing, and the shifting paradigm of institutional cryptocurrency engagement. Collectively, these dynamics reflect the intersecting forces of technological advancement, regulatory evolution, and capital market innovation shaping investment decision-making in a globally interconnected environment.

Nvidia’s fiscal performance and strategic positioning epitomize the accelerating AI deployment cycle, fuelled by the unparalleled demand for specialized chip architectures. Concurrently, SpaceX propels the aerospace and AI cloud market fusion through an accelerated IPO process, underpinned by its ambitions to operationalize orbital data centers and integrate novel AI coding platforms. Parallel to these corporate narratives, institutional investors are transitioning cryptocurrency exposure from speculative to systematic portfolio components, enabled by robust regulatory frameworks and sophisticated risk management methodologies.

The purpose of this report is to deliver actionable insights across these focal points, offering quantitative data, market context, and risk assessments to inform portfolio construction, tactical timing, and strategic allocation decisions. We evaluate financial forecasts, valuation metrics, competitive threats, and macroeconomic influences—including the effect of easing U.S.-China trade tensions on AI-capex and crypto flows. By integrating these threads, the report equips professional stakeholders with a holistic framework to navigate complexity, capitalize on emerging trends, and mitigate material risks in a dynamic investment environment.

Infographic Image: Infographic

1. Executive Overview: Tech Titans and Crypto Shifts Driving Strategic Decisions in May 2026

Market Snapshot: AI Powerhouses, Mega IPOs, and Institutional Crypto Allocations Define 2026

This subsection establishes a foundational overview of the converging market forces in May 2026 that set the strategic context for the report. By synthesizing the latest financial forecasts for Nvidia, critical milestones for SpaceX’s landmark IPO, and quantifiable data on institutional cryptocurrency inflows, it frames the interplay among AI infrastructure growth, space-tech market evolution, and digital asset adoption that will shape investment and operational decision-making.

Nvidia’s Q1 2027 Financial Outlook and Earnings Expectations

Nvidia is positioned to report remarkable fiscal first-quarter results on May 20, 2026, reflecting sustained strength in AI-related demand. Market consensus projects revenues approaching $79 billion, anticipating year-over-year growth near 77%, driven largely by ongoing shipments of Blackwell architecture chips underpinning AI data center workloads. EPS estimates converge around $1.78 per share, marking a substantial increase relative to prior periods. Investor confidence centers on Nvidia's continued leadership in AI infrastructure, as the chipmaker fortifies its dominance with consistent earnings beats and bullish forward guidance.

The upcoming earnings call is viewed as a pivotal moment for reaffirming Nvidia’s growth trajectory amidst intensifying competitive pressures. Analysts and investors are closely monitoring management commentary for insights on the Vera Rubin GPU rollout timeline and the sustainability of hyperscaler spending, given recent indications of increased in-house silicon development by major cloud providers. Market derivatives imply elevated volatility around the earnings event, underscoring the critical nature of Nvidia’s disclosures in influencing near-term equity performance.

SpaceX IPO Timeline and Valuation Milestones

SpaceX is progressing rapidly toward one of the most significant initial public offerings in history, with regulatory filings expected imminently and a Nasdaq listing targeted for June 12, 2026. The company aims to raise approximately $75 billion within a valuation range estimated between $1.75 and $2 trillion, potentially eclipsing all previous IPO records in size and valuation. This accelerated timeline results from an expedited review process by the U.S. Securities and Exchange Commission, condensing the conventional multi-month cadence into a matter of weeks.

Critical events include a roadshow launch planned for early June and share pricing scheduled on June 11, positioning SpaceX’s public debut as a landmark transaction that underscores the growth prospects of combined aerospace, satellite communications, and integrated AI technology businesses. Analysts emphasize that the offering’s scale and valuation reflect confidence in SpaceX’s market dominance across global rocket launches and its strategic expansion into orbital data centers and AI-driven satellite services.

Institutional Crypto ETF Inflows and Evolving Market Adoption

Institutional adoption of cryptocurrency investment products continues to accelerate, with spot Bitcoin ETFs alone recording cumulative inflows exceeding $56 billion in the first quarter of 2026. This unprecedented capital inflow signals a transition from speculative trading toward broad-based portfolio integration. Notably, the launch of major new ETFs from established financial institutions, including Morgan Stanley’s Bitcoin Trust, underscores mainstream acceptance and the increasing regulatory maturation of digital asset markets.

While Bitcoin remains the cornerstone asset, there is marked enthusiasm for regulated altcoin exposures, led by assets such as Solana and XRP. Surveys indicate that a significant proportion of institutional investors currently hold Solana and plan to increase exposure, drawn by its scalable throughput and cost-effective transaction capabilities. Simultaneously, XRP benefits from clearer regulatory frameworks and strong enterprise partnerships, fostering confidence in its liquidity and adoption potential within institutional portfolios.

Having established the broad market landscape with strong fundamentals in AI hardware, groundwork for a historic space-tech equity offering, and the crystallizing pattern of institutional crypto integration, the report proceeds to a detailed examination of Nvidia’s financial performance and strategic positioning. This focus will dissect the nuances behind Nvidia’s growth and market capitalization, laying the foundation for understanding its influence on adjacent markets and investment frameworks.

Strategic Imperatives: Balancing High Growth with Execution Risks and Evolving Institutional Crypto Adoption

This subsection explores the critical strategic tensions that shape the investment landscape in May 2026, focusing on how leading technology players must navigate formidable execution risks amid robust growth trajectories, while institutional investors recalibrate cryptocurrency allocations from speculative ventures toward integrated portfolio components. By examining competitive pressures on Nvidia, regulatory and technical challenges confronting SpaceX, and the maturation of crypto investment frameworks, this analysis identifies key decision points for long-term positioning in converging tech and digital asset domains.

Competitive Pressures and Execution Risks in Nvidia’s AI Chip Leadership

Nvidia’s anticipated 65% year-over-year revenue growth underscores an exceptional expansion driven primarily by demand for its Blackwell AI chips and sustained data center investments. However, this growth narrative coexists with mounting competitive pressures from hyperscalers increasingly developing their own custom silicon to optimize AI workloads. These custom chips, designed to deliver significant cost and efficiency gains at hyperscale, pose a structurally disruptive threat by potentially eroding Nvidia’s long-term market share in key segments. While Nvidia’s entrenched CUDA ecosystem and integrated hardware-software stack remain formidable barriers to entry, the pace at which hyperscalers like Google and Amazon mature their in-house solutions will critically influence Nvidia’s margin sustainability and market leadership.

From a strategic risk perspective, Nvidia must also contend with customer concentration among hyperscale cloud providers, whose evolving chip strategies may reduce dependency on external suppliers. Concurrently, geopolitical dynamics, including U.S.-China export restrictions, threaten approximately one-fifth of Nvidia’s addressable market, compelling the company to innovate compliant product variants without compromising competitive advantages. These factors collectively introduce execution risks that could moderate the company’s exceptional growth projections, necessitating vigilant monitoring of hyperscaler chip adoption rates and regulatory developments to validate bullish investment theses.

SpaceX’s Orbital Data Center Ambitions: Regulatory and Technical Hurdles Impacting Valuation Trajectory

SpaceX’s anticipated IPO, targeting a valuation between $1.75 trillion and $2 trillion, hinges heavily on its ambitious orbital data center strategy. These data centers aim to harness space-based infrastructure for large-scale AI computing, a vision that could redefine the AI cloud market landscape. However, critical uncertainties surround the commercial viability of deploying and sustaining data centers in orbit. Technological challenges include ensuring hardware reliability under harsh radiation exposure, managing thermal dissipation in microgravity, and the absence of on-site repair capabilities, raising substantial execution risks.

Regulatory compliance compounds these technical challenges, with SpaceX requiring extensive coordination with U.S. and international agencies to manage spectrum use, orbital debris, and environmental impacts. Delays in securing FAA licenses or FCC approvals could materially affect launch cadence and infrastructure deployment, directly influencing investor confidence. Furthermore, partnerships like the high-profile contract with Anthropic represent significant revenue streams but include termination clauses that reflect the nascent and rapidly evolving nature of the AI compute market. Overall, while SpaceX’s roadmap reflects visionary potential, these intertwined regulatory and operational complexities warrant cautious valuation calibration and careful IPO risk assessment.

Institutional Cryptocurrency Allocation: From Speculation to Systematic Portfolio Integration

Institutional investors are transitioning from viewing cryptocurrencies as speculative instruments toward embracing them as strategic portfolio components that provide diversification and asymmetric return profiles. This maturation is exemplified by Bitcoin ETF inflows surpassing $56 billion and a notable shift toward regulated and compliant investment vehicles, accelerating adoption across pension funds, family offices, and hedge funds. Regulatory clarity, notably through frameworks like the EU’s MiCA and the U.S. SEC’s evolving stance on digital assets, has mitigated previously prohibitive compliance barriers, fostering greater institutional comfort and facilitating increased allocations.

Beyond Bitcoin, altcoins like Solana and XRP are gaining traction among institutional portfolios due to their scalability, utility in decentralized finance, and favorable regulatory outlooks. Surveys indicate that Solana leads altcoin allocations with substantial planned expansions, driven by its high throughput and low-cost transactions, which align with institutional scalability requirements. Sophisticated strategies, including volatility-targeting models, tail-risk hedging through out-of-the-money options, and yield overlays via tokenized money-market funds, exemplify the enhanced tactical complexity institutions now apply, reflecting a fully integrated and risk-managed engagement with the crypto ecosystem.

Having established the strategic tension between robust growth projections and execution risks across Nvidia’s AI chip dominance and SpaceX’s groundbreaking but technically nascent space infrastructure, alongside institutional crypto’s shift toward systematic adoption, the analysis proceeds to a detailed examination of Nvidia’s financial outlook and strategic positioning. This progression offers granular insights into how competitive dynamics and partnerships underpin Nvidia’s sustained leadership amidst evolving market challenges.

2. Deep Dive: Nvidia’s AI Chip Leadership and Strategic Positioning in 2026

Financial Performance and Investor Sentiment: Q1 FY2027 Outlook and Valuation Metrics

This subsection critically evaluates Nvidia's current financial trajectory and market valuation as it approaches the fiscal Q1 2027 earnings announcement. By synthesizing consensus revenue and EPS forecasts with detailed valuation ratios and market sentiment indicators, it offers insight into investor expectations and the broader implications of macroeconomic conditions, including Federal Reserve policies, on Nvidia's premium valuation. This analysis contextualizes Nvidia's financial positioning within the report’s broader strategic framework, setting the stage for assessing execution risks and competitive dynamics in subsequent sections.

Consensus Revenue and Earnings Projections Signal Sustained High-Growth Momentum

Nvidia is poised to report an extraordinary fiscal Q1 2027 performance, with consensus revenue estimates ranging between $78 billion and $81.6 billion. This represents a year-over-year increase exceeding 65%, driven primarily by surging demand for AI accelerators and data center infrastructure products. Analysts widely anticipate earnings per share to climb sharply, with estimates centering around $1.76 to $1.87, translating to approximately 77% year-over-year growth. This remarkable performance underscores the company’s central role amid an accelerating AI-driven capital expenditure cycle.

Market enthusiasm is underpinned by Nvidia's track record of consistently beating forecasts each quarter over recent years, solidifying investor confidence. The underlying growth is fueled by robust deployments of the Blackwell GPU generation and an expanding data center revenue base that now accounts for over 90% of Nvidia's total sales. Forward-looking guidance for Q2 FY2027 also remains buoyant, with revenue expected to approach $86–91 billion, further reflecting optimism among hyperscale cloud providers ramping AI infrastructure investments.

Valuation Metrics: Forward Price-to-Earnings and Market Sentiment Amid Fed Policy Influences

Nvidia's forward price-to-earnings (P/E) ratio currently hovers around 24x to 26x, reflecting a premium valuation relative to the broader semiconductor industry and the S&P 500 index. This premium is indicative of sustained investor confidence in Nvidia's dominant market positioning and growth trajectory. However, it also embeds expectations of continued robust earnings growth driven by AI-infused demand cycles. Market-implied volatility surrounding the May earnings event anticipates a single-day price move exceeding 10%, signaling heightened sensitivity to earnings outcomes and guidance.

Federal Reserve monetary policy remains a key external factor influencing Nvidia’s valuation. The prevailing 'higher-for-longer' interest rate environment applies downward pressure on growth stock multiples, including Nvidia. However, Nvidia’s earnings momentum and cash flow generation capacity have so far proven resilient against this macro backdrop. Analysts suggest any easing or pivot in Fed policy could catalyze multiple expansions, adding upward pressure to valuation. Conversely, sustained rate elevated levels would likely restrain valuation expansion despite strong fundamentals.

Investor sentiment also reflects cautious optimism balanced with competitive and execution risks. Options markets and prediction platforms currently assign a roughly 90% probability that Nvidia will beat revenue expectations, yet the magnitude of upside price reaction may be tempered given the substantial gains the stock has realized leading into earnings. Technical indicators show the stock trading within prior support zones, with resistance near $228–$240, and overbought signals tempered by strong fundamental catalysts.

Interplay of Fed Policy, Interest Rates, and Growth Premium: Navigating Valuation Complexities

Nvidia's valuation dynamic exemplifies the tension between high growth expectations and the restrictive financial conditions imposed by current Fed policy. Although value compression is typical under elevated interest rates, Nvidia’s sector-leading earnings growth partially offsets this effect, resulting in sustained premium pricing. The company's ongoing transition from Blackwell to Vera Rubin architectures adds a nuanced layer to market anticipation, where successful execution would validate future growth narratives and justify high multiples.

Macro factors such as inflation, geopolitical trade considerations, and interest rate trajectories shape investor risk tolerance and appetite for growth stocks like Nvidia. As a bellwether for AI sector momentum, Nvidia serves as both a beneficiary and barometer of broader market trends. The resilient demand for AI semiconductors amidst this environment supports a narrative that Nvidia’s premium valuation can be maintained, but the margin for upside surprises is narrowing compared to prior quarters. Strategic investors will therefore monitor not only reported financial metrics but also guidance tone and competitive disclosures for signals on sustainability.

Having established Nvidia’s robust financial outlook and valuation context, the analysis naturally progresses to exploring competitive pressures and margin sustainability challenges arising from emerging custom silicon initiatives and customer diversification strategies. Understanding these dimensions is essential for assessing the durability of Nvidia’s growth premium and its strategic posture within the AI semiconductor ecosystem.

Competitive Landscape and Margin Sustainability: Custom Silicon Disruption and Customer Diversification Risks

This subsection examines the evolving competitive dynamics in the AI chip sector as Nvidia confronts growing challenges from established rivals and hyperscaler-customized silicon initiatives. It quantifies the emerging market share shifts and evaluates margin pressures stemming from customer diversification, providing a critical lens on the sustainability of Nvidia's premium positioning and the credibility of its ambitious revenue projections.

Market Share Dynamics: AMD, Broadcom, and Hyperscaler Custom Silicon Adoption in 2026

Nvidia commands approximately 81% of the AI data center chip market, maintaining a dominant position but facing mounting competitive incursions. Advanced Micro Devices (AMD) has secured around 10% market share, reflecting significant gains propelled by its growing footprint in data center GPUs and AI accelerators. Broadcom has emerged as a formidable player in the custom AI chip niche, especially ASICs, witnessing a remarkable 106% year-over-year revenue growth in Q1 2026 and positioning to exceed $100 billion in AI chip revenue by 2027. Hyperscalers such as Google, Meta, and Amazon aggressively advance their respective in-house silicon strategies, deploying tailored ASICs and TPUs designed to optimize inference workloads and specific AI applications. These bespoke chips have achieved roughly 28–30% penetration of the AI chip market, rapidly shaping the landscape by offering up to 40–60% cost advantages over general-purpose GPUs.

The increasing adoption of custom silicon chips by major hyperscalers indicates a structural pivot in AI infrastructure procurement. IDC and independent market analyses forecast that hyperscaler in-house silicon adoption rates in data centers could surpass one-third of server AI chip deployments by the end of 2026. This shift challenges Nvidia to reinforce its product differentiation through performance leadership, ecosystem integration, and scalable architectures such as Blackwell and Vera Rubin. Alphabet’s TPU family, closely developed with Broadcom, exemplifies this trend, achieving substantial operational scale that encroaches on Nvidia’s traditional market segments. Despite this, Nvidia’s broad software ecosystem and its entrenched CUDA framework continue to serve as key barriers to rapid displacement.

Margin Pressure and Customer Diversification: Analyzing Risks of Hyperscaler Silicon Insourcing

The rise of hyperscaler custom silicon introduces tangible risks to Nvidia’s margin profile. While Nvidia’s data center GPUs enjoy gross margins in excess of 70%, bespoke chips operated by hyperscalers often come at significantly lower per-unit costs, optimized for specific workloads with aggressive cost-efficiency targets. This commoditization pressure jeopardizes Nvidia’s pricing power, particularly in inference domains where custom silicon has demonstrated up to 30% improved performance-per-dollar ratios in lab benchmarks. Industry insiders highlight that inference workloads constitute the majority of production AI compute, where margin erosion is expected to materialize over the next two to four years as customers diversify supply chains.

Customer concentration risk likewise intensifies. Nvidia’s top hyperscaler clients account for the majority of its AI chip revenue, but the same customers now operate competitive silicon programs or partner with rivals like Broadcom for custom ASIC development. This creates a duality where Nvidia remains a preferred vendor but is exposed to potential volume reallocations or contract term renegotiations. Market data indicates that approximately 20% to 25% of AI data center revenue historically linked to China has been impacted by export controls, compelling Nvidia to further adjust product portfolios and pricing strategies. Despite these headwinds, Nvidia’s integrated hardware-software approach, combined with anticipated revenue exceeding $1 trillion from Blackwell and Vera Rubin chip families, signals a robust long-term growth narrative. However, ongoing execution in product innovation and customer retention will be pivotal to offset emerging margin and share pressures.

Validating the $1 Trillion Revenue Forecast: Assumptions Behind Nvidia’s Blackwell and Vera Rubin Platforms

Nvidia’s forecast of over $1 trillion in cumulative revenue for its Blackwell and Vera Rubin architectures across 2026 and 2027 embodies both strong demand validation and aggressive scaling assumptions. This projection rests on a combination of factors: accelerating hyperscaler AI-capex cycles, adoption of next-generation GPUs capable of handling larger and more diverse AI workloads, and sustained expansion beyond hyperscale data centers into edge computing and enterprise deployments. Blackwell-based systems have demonstrated strong early traction, contributing upwards of $11 billion in recent quarterly revenues, with Vera Rubin expected to deliver substantial performance uplifts that justify premium pricing levels.

Analysts consider Nvidia’s estimation credible though challenging, factoring in projected shipment volumes approximating tens of thousands of Blackwell racks globally. These calculations imply that Nvidia will capture a significant portion of the growing AI infrastructure spend, which itself is forecast to exceed $720 billion in 2026. Nonetheless, sensitivity analyses caution that the forecast’s realization hinges on successful counteraction of competitive incursions, maintenance of supply chain robustness, and regulatory landscape stability. Margins could compress if hyperscaler silicon adoption accelerates beyond current estimates or if geopolitical trade restrictions exacerbate market fragmentation. The guiding principle for investors and strategic decision-makers remains vigilance in monitoring customer migration trends and continuous innovation cycles tied to Nvidia’s advanced GPU architectures.

Having dissected Nvidia’s competitive pressures and margin dynamics, the subsequent section will explore how the company is leveraging strategic partnerships and vertical integration initiatives to fortify its AI cloud platform leadership and mitigate these risks.

Securing AI Cloud Dominance: Evaluating IREN Partnership, Optical Capacity Expansion, and Strategic Financing in NVIDIA’s 2026 Blueprint

This subsection analyzes critical strategic expansions underpinning NVIDIA’s leadership in AI infrastructure. It dissects the scope, timeline, and financial underpinnings of the landmark IREN partnership for large-scale AI data center deployment, alongside the ambitious Corning optical manufacturing capacity increase. The evaluation highlights how these vertical integration initiatives enhance NVIDIA's supply chain resilience and market control amidst intensifying AI compute demand.

Tracing the Scale and Timeline of IREN’s 5GW AI Infrastructure Deployment

NVIDIA's strategic alliance with IREN represents a cornerstone in securing critical AI compute infrastructure, targeting deployment of up to 5 gigawatts (GW) of DSX-aligned AI capacity across IREN’s global data center network. This buildout centers on a staged expansion, with initial focus on the pivotal 2GW Sweetwater campus in Texas, anticipated to become the hallmark site exemplifying NVIDIA’s DSX AI factory architecture. While the partnership does not commit to immediate full-scale deployment, the gradual ramp is planned over the next five years, aligning with market demand and supply chain maturation.

IREN’s transition from cryptocurrency mining to high-performance AI computing resources signifies a strategic pivot, leveraging its 23,000 GPU fleet and access to 3GW of renewable-driven power in North America. The company’s vertically integrated model—from power procurement to GPU cloud operations—positions it to serve as an AI infrastructure hub for both startups and enterprise clients. However, execution challenges persist, including the complex coordination of power allocation, land acquisition, and GPU supply chain dynamics across diverse geographies. Near-term milestones, such as completion of the Horizon 1 liquid-cooled facility and Sweetwater energization targeted for 2026, will serve as critical performance barometers.

The partnership also grants NVIDIA a five-year warrant option to invest up to $2.1 billion in IREN equity, exercisable under specified regulatory and milestone conditions. This financial commitment solidifies NVIDIA's stake in the partnership’s success, enhancing collaboration incentives while providing capital to accelerate expansion phases.

Unpacking Corning’s Optical Capacity Expansion: Investment Scale, Manufacturing Timelines, and Strategic Significance

In tandem with computational infrastructure growth, NVIDIA’s investment in Corning underscores a decisive push to fortify optical connectivity capacity—a critical component enabling high-bandwidth, low-latency AI data center operations. Corning’s planned tenfold increase in U.S.-based optical connectivity manufacturing, alongside a greater than 50% expansion in fiber production capacity, addresses escalating demand driven by AI workloads that generate unprecedented data transmission requirements.

This massive scale-up hinges on construction of three advanced manufacturing plants strategically located in North Carolina and Texas. Although exact completion timelines are undisclosed, standard industry benchmarks project a 24 to 36-month horizon to reach full production capacity. The endeavor is expected to create over 3,000 new U.S. manufacturing jobs, reflecting not just technological ambition but also substantial economic and employment impact.

NVIDIA's embedded investment includes an initial $500 million prepayment and equity investment rights totaling up to $3.2 billion, including warrants to acquire shares at elevated strike prices. This financial structure both secures supply chain exclusivity and aligns incentives for innovation in fiber optic materials tailored for AI factory demands. The partnership effectively accelerates the transition away from legacy copper wiring to optical solutions, mitigating heat dissipation and resistance constraints that impair contemporary data center scalability.

Assessing the Financial Terms: Warrants, Service Contracts, and Multiyear Strategic Commitments

The financial architecture underpinning these strategic expansions reflects a layered approach combining equity options, long-term service contracts, and operational synergies. NVIDIA’s warrant rights over IREN—exercise price set at $70 per share for up to 30 million shares over five years—equip the firm with potential to deepen capital commitment contingent on regulatory approvals and performance milestones, mitigating risk while preserving option flexibility.

Complementing equity stakes, NVIDIA has secured a $3.4 billion AI cloud services contract with IREN, spanning five years and encompassing GPU cloud management and AI compute services. This contract aligns with IREN’s infrastructure expansion, providing recurring revenue stability and fostering a tightly integrated supply chain reflecting full-stack AI infrastructure control.

Similarly, the Corning partnership’s financial design includes a $500 million advance payment along with rights to invest up to $3.2 billion in stock acquisitions and warrants, collectively anchoring supply chain access. The multiyear collaboration signals a long-term commitment to co-developing optical communication technologies optimized for NVIDIA’s AI processor ecosystem, critical for sustaining platform differentiation and margin preservation against rising competitive pressures.

These strategic expansions with IREN and Corning illustrate NVIDIA's deliberate progression beyond silicon design into owning critical components of the AI infrastructure stack. The combined execution of large-scale AI cloud deployments and optical connectivity manufacturing provides NVIDIA with a defensible moat, integrating hardware production with expansive service contracts and equity exposure. This foundation sets the stage for assessing competitive threats and margin sustainability, topics examined in subsequent subsections.

3. Roadmap to IPO: SpaceX’s Ambitious Path Toward a $1.75–$2 Trillion Valuation

Timeline and Structural Highlights: From SEC Filings to Nasdaq Listing in a Record-Breaking IPO

This subsection provides a granular analysis of SpaceX’s accelerated IPO timeline and unique structural elements that underpin the offering’s historical significance. It anchors the broader discussion of SpaceX’s $1.75–$2 trillion valuation pathway by clarifying critical milestones, financing tranches, regulatory facilitation, and listing mechanisms. This precise timing and share structure context is essential for institutional investors and market strategists preparing for anticipated market impact and allocation management.

Confirming the Accelerated IPO Timeline and Key Date Milestones

SpaceX has established a compressed and accelerated timeline for its highly anticipated initial public offering. The company is expected to publicly release its IPO prospectus as early as the week of May 18, 2026, allowing for a narrow window to conduct due diligence before investor engagement. Subsequently, the investor roadshow is scheduled for the week commencing June 4, 2026, with the formal pricing anticipated as soon as June 11, and public trading poised to begin on Nasdaq on June 12, 2026. This timeline reflects a significant acceleration from typical IPO processes owing primarily to a faster-than-expected review and approval pace by the Securities and Exchange Commission (SEC), which has facilitated this unprecedented schedule.

The advancement in filing and approval processes is exceptional, as IPO reviews historically span several months. Confidential filings occurred in early April 2026, with public disclosures mandated to precede the roadshow by at least 15 days, consistent with regulatory requirements. The rapid progression from confidential to public filing and from roadshow to listing compresses key market windows but enables SpaceX to capitalize on favorable market sentiment and investor appetite in mid-2026.

Deconstructing the $75 Billion Offering and Tranche Allocation Strategy

SpaceX plans to raise up to $75 billion in what is projected to be the largest IPO ever conducted globally. This capital raise would place the company's valuation range between $1.75 trillion and $2 trillion, a figure surpassing all prior global IPO records by a wide margin, including Saudi Aramco’s $29.4 billion raise in 2019. The offering size magnifies SpaceX’s market footprint instantly, elevating it to the top echelon of public companies by market capitalization.

The planned share sale is structured across multiple tranches to balance investor demand and facilitate broad market participation, while also maintaining strategic allocations. Notably, a sizable retail tranche aims to allocate approximately 20% to 30% of the offering to retail investors, markedly higher relative to typical mega-IPOs. Institutional participation is orchestrated through a syndicate of 23 underwriters led by Goldman Sachs and Morgan Stanley, ensuring robust placement across asset managers, pension funds, and sovereign wealth entities. This tranche strategy plays a pivotal role in managing subscription risk and price stability during the early trading phase.

Nasdaq Listing and Share Class Structure: Founder Control and Investor Rights

The IPO will see SpaceX list under the ticker symbol SPCX on the Nasdaq exchange. The company has adopted a concentrated dual-class share structure designed to preserve founder control post-listing. Specifically, Class B shares, held predominantly by Elon Musk and close insiders, carry ten votes per share, while publicly offered Class A shares confer one vote per share. This governance framework grants Musk approximately 79% voting power despite holding around 42% economic equity, effectively centralizing decision-making authority.

This dual-class arrangement, while consistent with trends among leading tech IPOs, raises considerations regarding limited shareholder influence over corporate governance, strategic direction, and potential activist interventions. In addition to concentrated voting power, the governance framework includes provisions that limit shareholder litigation rights, mandate arbitration for disputes, and restrict venue to specified jurisdictions, further circumscribing investor control. From a liquidity perspective, the single security representing multiple business lines—satellite internet, launch services, government contracts, and AI platforms—offers a diversified exposure but complicates pure-play investment theses.

Regulatory Factors Accelerating IPO Pace and SEC Review Considerations

A critical enabler of SpaceX’s accelerated timeline has been an unusually rapid review process by the SEC. The confidential S-1 registration occurred in early April, with public filings scheduled for mid-May, squeezed between standard regulatory disclosure minimums. The SEC’s prioritization reflects both the significance of the offering and broader institutional reforms aimed at streamlining IPO approvals for strategically important technology companies.

Nonetheless, the compressed review cycle presents potential risk vectors, including last-minute SEC comment letters or data requests that could temporarily delay pricing or issuance. The company’s extensive disclosures on multi-billion-dollar capital expenditures for AI infrastructure and orbital data centers also attract enhanced regulatory scrutiny. Market participants should monitor for any material developments in the subsequent two weeks leading into the roadshow to assess whether regulatory factors could influence pricing or initial trading volatility.

With the IPO timeline, capital structure, and regulatory context clearly delineated, the next subsection will examine SpaceX’s strategic acquisitions and technological synergies. This will deepen understanding of how these corporate maneuvers enhance SpaceX’s core competencies and position it for sustained growth post-listing.

Strategic Acquisitions and Technological Synergies: Cursor and xAI Integration

This subsection evaluates the timing, financial implications, and strategic rationale behind SpaceX’s $60 billion acquisition option for Cursor, alongside the integration of xAI’s AI capabilities. These moves are pivotal in positioning SpaceX as a leader in converging AI and aerospace technologies, directly influencing its IPO valuation and future operational profile.

Clarifying the $60 Billion Cursor Acquisition Timeline Post-IPO

SpaceX has structured the acquisition of AI coding platform Cursor to occur approximately 30 days following its planned public listing, which is slated for Nasdaq debut in mid-June 2026. This deliberate sequencing aims to avoid premature regulatory complexity and the need to amend IPO disclosures while enabling the company to utilize freshly issued public shares as consideration for the transaction. The separation between the IPO event and acquisition closing stabilizes investor sentiment by preserving valuation clarity during the offering period and facilitates smoother capital allocation post-listing.

Cursor’s rapid valuation ascent—from $2.5 billion eighteen months ago to a negotiated $60 billion price tag—as well as its strong customer base generating substantial recurring revenue, underscore the strategic value of this acquisition. The timing also ensures that SpaceX can focus investor attention on the IPO before integrating Cursor’s advanced AI coding capabilities into its broader space and data infrastructure ecosystem.

Understanding the $10 Billion Breakup Fee: Deal Certainty and Financial Risk

The acquisition agreement includes a $10 billion breakup fee payable by SpaceX to Cursor if the acquisition right is not exercised by year-end 2026. This sizable contingent liability acts both as a strong incentive for deal consummation and as financial protection for Cursor against deal failure after significant joint development efforts. The breakup fee encompasses a $1.5 billion termination component plus an $8.5 billion deferred fee, reflecting the substantial value of collaboration and lock-in achieved during the IPO and post-offering period.

From a risk perspective, the $10 billion breakup fee represents a material cash or stock outflow that could impact SpaceX’s liquidity post-IPO, particularly given the expected capital expenditures necessary for orbital data center projects. Nonetheless, given SpaceX’s approximately $25 billion anticipated cash position at IPO and its strategic prioritization, market consensus strongly favors deal completion, rendering the fee a strategic deterrent rather than a probable loss. This mechanism also preserves IPO timeline integrity by preventing acquisition-related delays or costly financial restatements.

Quantifying xAI’s Integration Impact on Orbital Data Center Ambitions

The incorporation of xAI, acquired by SpaceX earlier in 2026, into SpaceXAI consolidates AI development efforts and enhances the company’s capability to develop and deploy large-scale generative AI workloads optimized for space-based data centers. This vertical integration reduces fragmentation across Musk’s AI ventures and contributes a highly sophisticated LLM infrastructure (including Grok AI models) directly linked to Starlink’s satellite network, enabling real-time AI inference in orbit.

xAI’s operational costs, projected at approximately $1 billion per month, reflect the magnitude of compute power being marshaled, complementing Cursor’s rapid-growth AI coding tools. Such integration enhances the feasibility of SpaceX’s orbital compute objectives by aggregating software innovation, hardware deployment, and network connectivity. While xAI’s revenue contribution remains under $1 billion for 2026, its synergy effects substantially increase the strategic optionality associated with orbital data centers, feeding into investor expectations for long-term value creation above and beyond SpaceX’s core launch and satellite businesses.

Assessing AI Tool Deployment Timelines and Execution Risks in Aerospace Operations

Deploying advanced AI coding tools like those developed by Cursor and integrated with xAI into aerospace workflows represents a multi-year initiative marked by considerable complexity. The aerospace domain demands highly reliable AI solutions capable of processing voluminous engineering data, regulatory documents, maintenance records, and safety-critical information under stringent traceability and compliance requirements.

Effective deployment requires continuous model retraining and specialized AI/ML operations infrastructure to ensure performance stability amid evolving aerospace protocols and regulatory frameworks. Moreover, integrating AI-generated outputs into operational and maintenance decision-making imposes high staffing overhead and risk mitigation costs. Given the nascent state of AI in aerospace and orbital environments, timeline estimates currently span several years, with early adoption focusing on knowledge management and decision support before extending to real-time autonomous operations.

These execution risks—ranging from technical integration hurdles to regulatory constraints—underscore the necessity of phased rollout strategies, robust security protocols, and stakeholder alignment, which directly influence SpaceX’s IPO valuation assumptions and future investor confidence.

With the Cursor acquisition framework and xAI’s integration dissected, the analysis naturally progresses to assessing how these technological synergies and strategic investments interface with SpaceX’s broader IPO roadmap, risk profile, and market reception.

Risk Assessment and Market Reception: Orbital Data Centers and Defense Contracts

This subsection provides a critical evaluation of the risks related to SpaceX’s orbital data center ambitions alongside an examination of tangible external validations—particularly the strategic U.S. Department of Defense partnership—that underpin investor sentiment and valuation dynamics ahead of the upcoming IPO. By quantifying energy demands, dissecting defense contract implications, and assessing regulatory sensitivities, this analysis contextualizes the sustainability challenges and strategic endorsements shaping market reception and investment risk calculus.

Quantifying Energy Consumption and Sustainability Challenges for Orbital Data Centers

SpaceX’s visionary deployment of orbital data centers aims to leverage continuous solar energy to power large-scale AI compute in space, targeting a capacity potentially exceeding 100 gigawatts. However, this ambitious infrastructure faces formidable power supply constraints. Without advanced orbital energy solutions, gigawatt-scale facilities would require terrestrial-scale solar arrays exceeding several hundred football fields, imposing prohibitive capital and supply chain costs. Power storage, thermal regulation, and radiation-hardened hardware further compound these energy challenges, threatening margin sustainability and deployment timelines.

Emerging innovations such as orbital energy grids promise to amplify solar flux intensity by a factor of up to ten, thus increasing efficiency and enabling near-constant operation with optimized thermal management. Yet, these technologies remain nascent, and the path to scalable, cost-effective energy provisioning remains fraught with technical, financial, and regulatory uncertainty—introducing significant execution risk that investors must weigh when considering SpaceX's IPO valuation projections.

Strategic Validation through U.S. Department of Defense Partnership and Contract Scale

The U.S. Department of Defense’s endorsement via a high-profile partnership enhances SpaceX’s credibility, offering meaningful external validation ahead of its public market debut. This collaboration focuses on integrating AI capabilities into secure military communications and battlefield decision systems, providing SpaceX with substantive defense revenue visibility and reputational capital.

SpaceX’s reported contract with Anthropic epitomizes the tethered revenue streams anticipated from enterprise AI clients, with commitments of approximately $15 billion per year through 2029 for access to SpaceX’s Colossus AI training centers. Concurrently, cooperative efforts within the DoD’s broader AI initiatives signal a robust, multi-year contract pipeline. This partnership portfolio is reflected in high strategic evaluations indicating strong financial health and capability to deliver advanced technology solutions across defense sectors, bolstering investor confidence.

Nonetheless, contracts include exit provisions and capacity ramp-up phased fee reductions, underscoring the sector’s volatility and the need for contending with technological, geopolitical, and procurement risk factors.

Regulatory Delays, Infrastructure Approval Challenges, and Valuation Sensitivities

Orbital infrastructure development is subject to rigorous regulatory oversight across agencies governing space traffic management, telecommunications, and environmental impact, all of which intricately influence deployment schedules and capital expenditures. Delays in obtaining necessary licenses for orbital satellites, laser communications, and inter-satellite networking can stall revenue generation and dampen market valuations.

SpaceX’s valuation and IPO timing exhibit high sensitivity to these regulatory timelines. Bottlenecks in securing approvals for constellation expansion or orbital data center operations could defer cash flows by months or years, amplifying discount rates applied by investors and instigating valuation downward revisions. Market signals post-DoD partnership announcements reflect cautious optimism but highlight increased volatility in response to regulatory news flow and infrastructure progress updates.

Further, the scalability and economic viability of orbital data centers hinge on overcoming these regulatory barriers in tandem with technical maturation, reiterating that SpaceX’s ambitious valuation range is conditioned upon execution against a complex approval landscape.

Investor Sentiment and Market Reception Following U.S. Defense Endorsement

Investor sentiment towards SpaceX has notably improved subsequent to formal announcements of its defense contracts and AI infrastructure partnerships. The DoD’s high financial strength score and robust strategic interest serve as critical green lights for institutional investors assessing risk-reward profiles of the forthcoming IPO.

Market reactions also reflect awareness of SpaceX’s dual-sector positioning—both as a pioneering aerospace enterprise and as a provider of cutting-edge AI compute infrastructure. This bifurcated narrative enhances the company’s attractiveness by offering diversified revenue streams and aligning with key technological megatrends. However, prudent investors remain cognizant of the execution risks inherent in pioneering orbital data solutions and the regulatory hurdles that may cause valuation variability.

Overall, the confluence of U.S. defense validation and innovative, albeit high-risk, orbital data center ambitions creates a nuanced market reception characterized by guarded enthusiasm, conditional on forthcoming regulatory progress and operational milestones.

AI Infrastructure Market Outlook and Comparative Validation

Supporting this optimistic investor stance is the broader AI infrastructure market momentum evidenced by leading sector incumbents. Nvidia’s projected revenue growth for Q1 2027, estimated between $78 billion and $81.6 billion, signals sustained demand and expansion in AI compute capabilities, which are integral to SpaceX’s orbital data center positioning.

This market backdrop provides a comparative validation of SpaceX’s technological and commercial aspirations, underscoring the plausible scalability of AI-driven infrastructure ventures within aerospace contexts and strengthening investor confidence in SpaceX’s multi-trillion-dollar valuation ambitions.

Building on the in-depth risk and market analysis of SpaceX’s orbital data center strategy and defense partnerships, the report now transitions to examining institutional cryptocurrency trends, which complement the portfolio considerations tied to emerging technological investment themes explored herein.

4. Institutional Crypto Adoption: From Speculation to Strategic Allocation Frameworks

ETF Inflows Surge Amid Regulatory Maturation: Bitcoin Cementing Institutional Portfolio Roles

This subsection details the robust momentum in Bitcoin ETF inflows throughout early 2026, examining how regulatory developments, particularly under Europe's MiCA framework and evolving SEC policies, have transformed crypto from a speculative asset into a core institutional allocation. Understanding these dynamics is essential to appreciating institutional shifts towards systematic crypto exposure and the broader impact on portfolio construction strategies.

Sustained Bitcoin ETF Inflows Validate Growing Institutional Confidence

Bitcoin exchange-traded funds (ETFs) have experienced accelerated capital inflows in the first half of 2026, establishing a strong institutional presence that underpins market stability. Cumulative net inflows into U.S. spot Bitcoin ETFs surpassed $56 billion by April, with monthly inflows reaching approximately $2 billion in April alone, the highest in 2026. This surge reflects a transition from episodic speculative interest to sustained strategic allocation within diversified institutional portfolios. Notably, leading products such as BlackRock’s iShares Bitcoin Trust maintained dominance, accounting for over 60% of ETF market share, highlighting concentration in trusted vehicles favored by asset managers and wealth custodians.

April and May inflows were further buoyed by new market entrants like Morgan Stanley’s Bitcoin Trust ETF, which rapidly captured over $160 million without recorded outflows during the initial launch weeks. Daily inflow patterns have shown resilience even amidst short-term market volatility, with institutional investors leveraging ETFs as efficient, regulated vehicles to obtain Bitcoin exposure without the operational complexities of direct custody. This trend fortifies Bitcoin’s role as a foundational digital asset within mainstream investment frameworks.

MiCA Regulation Catalyzing Institutional Transition from Speculation to Strategic Adoption

The full enforcement of the European Union’s Markets in Crypto-Assets (MiCA) regulation by mid-2026 marks a pivotal regulatory milestone that has accelerated institutional adoption of cryptocurrency. MiCA’s comprehensive framework harmonizes compliance standards across member states, creating legal clarity and investor protections critical to institutional risk management. This regulatory certainty has expanded the pool of crypto-asset service providers vetted for operational integrity, directly supporting regulated investment products like ETFs and fostering greater confidence among pension funds, insurers, and wealth managers.

MiCA’s requirements for mandatory white papers, licensing, custody standards, and governance have reduced fragmentation and mitigated the operational and reputational risks historically associated with digital assets. Consequently, institutions have moved beyond purely speculative positions into deliberate and sizable crypto allocations embedded within diversified portfolios. The regulatory momentum has also encouraged innovation, enabling the growth of Ethereum and other asset-linked ETFs and promoting integration with traditional finance infrastructure.

This progression from experimental exposures to strategic portfolio components is evident in asset allocation surveys revealing heightened institutional preference for regulated Bitcoin products, consistent with risk-adjusted mandates and long-term digital asset theses.

U.S. SEC Rule Changes Facilitate Larger ETF Adoption and Broaden Market Access

In the United States, regulatory advances have substantively lowered barriers for institutional engagement with bitcoin exposure via ETFs. The SEC’s adoption of streamlined rulemaking for ETFs, including Rule 6c-11 under the Investment Company Act, has created a more consistent and transparent regulatory environment. These rules eliminate the need for individual exemptive reliefs, reducing product launch times and compliance costs, which leads to greater competition, innovation, and variety of Bitcoin ETF offerings.

Additionally, the recent removal of 25,000 contract position limits on options tied to major Bitcoin and Ether ETFs by NYSE Arca and NYSE American in early 2026 has unleashed substantial liquidity in crypto derivatives markets. This expansion allows institutional investors to establish larger hedging and risk management positions, deepening the derivatives landscape surrounding ETF products and enhancing market efficiency.

The outcome is a reinforcing feedback loop whereby enhanced product availability and regulatory clarity attract more institutional capital, which in turn strengthens price stability and widens acceptance of Bitcoin as a mainstream asset class. Notwithstanding these gains, some innovative crypto ETF categories, including prediction market products, face regulatory delays as the SEC carefully assesses risks associated with novel derivatives, reflecting a calibrated approach balancing innovation and investor protection.

Having established Bitcoin’s foundational role through ETF inflows and regulatory clarity, the report proceeds to examine institutional diversification beyond Bitcoin, focusing on altcoin preferences and the strategic rationale shaping secondary digital asset allocations.

Diversification Beyond Bitcoin: Altcoin Preferences and Utility Drivers

This subsection delves into the evolving preferences among institutional investors as they expand their cryptocurrency allocations beyond Bitcoin, focusing on altcoins with distinct utility and growth profiles. By examining recent data on Solana and XRP, this analysis reveals how technological strengths, ecosystem development, and shifting regulatory landscapes influence portfolio construction strategies. Understanding these dynamics is essential for institutions seeking diversified exposure with an optimal risk-return balance in an increasingly mature crypto market.

Institutional Surveys Highlight Solana’s Dominance and Increasing Allocation Plans

Recent comprehensive surveys among large institutional investors indicate a clear momentum toward diversifying crypto portfolios beyond Bitcoin and Ethereum. Solana stands out as the leading altcoin choice with a notable existing institutional footprint and aggressive plans for expansion. Approximately 36% of surveyed firms currently hold Solana exposures, while an additional 38% intend to increase holdings during 2026. This level of engagement indicates a shift from experimentation toward strategic incorporation in institutional vaults and treasury allocations.

The appeal of Solana among institutions is primarily driven by its combination of high transaction throughput and cost-efficiency, making it a viable platform for decentralized finance, gaming, and NFT ecosystems. Institutional investors increasingly recognize Solana’s rapid finality and scalable infrastructure as core components that reduce operational friction and enhance portfolio diversification benefits. Furthermore, the expansion of institutional-grade staking and yield products tailored for Solana has been a critical factor in attracting long-term, risk-managed investments.

Quantifying Solana’s Technical Edge and Its Portfolio Impact

Solana’s technical architecture, featuring a hybrid Proof-of-History consensus mechanism combined with Proof-of-Stake, enables throughput exceeding 600,000 transactions per second, placing it among the fastest Layer 1 blockchains. This performance translates into meaningful competitive advantages for institutional users aiming to deploy scalable decentralized applications with minimal latency and transaction costs.

Empirical data demonstrates that Solana’s ecosystem supports over 41% of decentralized exchange volume in early 2026, with daily active dApp usage reaching unprecedented levels. Market capitalization recovery and growing Total Value Locked (TVL), which soared from just over $1 billion in late 2025 to approximately $9 billion by Q1 2026, underscore robust developer activity and capital inflows. These technological and economic metrics align with increased institutional allocations, as investors seek assets with proven utility and adoption trajectories rather than purely speculative profiles.

Regulatory Clarity Spurs Renewed Institutional Interest in XRP as a Payment-Centric Asset

XRP’s institutional allure is closely tied to recent milestones in regulatory clarity and enterprise adoption, positioning it distinctly as a blockchain optimized for cross-border payments and real-world asset tokenization. Following the conclusion of the long-standing legal dispute with the U.S. Securities and Exchange Commission, XRP was classified under more favorable regulatory designations, significantly alleviating prior uncertainties that limited institutional deployment.

The launch and sustained growth of multiple XRP spot ETFs have been pivotal in legitimizing institutional market access, with cumulative inflows surpassing $1.3 billion by early 2026. Adoption by major financial institutions and integration into tokenized asset frameworks contribute to XRP’s narrative as a practical, payment-focused digital currency. Surveys indicate that while only 18% of institutions currently hold XRP, 25% plan to initiate or increase exposure contingent upon further regulatory developments, signaling cautious yet growing confidence in XRP’s role within diversified crypto portfolios.

Comparative Risk-Return Profiles: Solana’s Growth Potential Versus XRP’s Stability and Utility

From a strategic asset allocation standpoint, Solana and XRP represent complementary exposures with differentiated risk-return profiles. Solana’s comparatively smaller market capitalization and dynamic developer ecosystem suggest higher upside potential driven by innovation and ecosystem expansion. Its ability to support emerging use cases in DeFi, stablecoins, and NFT infrastructure caters to investors targeting aggressive growth within the altcoin segment.

Conversely, XRP offers relatively greater stability anchored by its entrenched payment use cases, regulatory momentum, and real-world assets integration. The institutional embrace of XRP is underpinned by expectations of its consolidation as a core settlement and liquidity layer in global finance, reducing speculative volatility risks. Market experts advocate for portfolio frameworks that balance these dimensions, leveraging Solana for convexity and XRP for stable cash flow-like crypto exposure.

Having examined institutional preferences for altcoins beyond Bitcoin, with particular attention to Solana’s technical scalability and XRP’s evolving regulatory and enterprise profile, the subsequent section will explore advanced allocation strategies. This includes dynamic volatility targeting, tail-risk hedging, and yield generation techniques that institutions increasingly adopt to optimize crypto portfolio performance.

Advanced Strategies: Dynamic Volatility Management, Tail-Risk Hedging, and Institutional Yield Enhancements in Crypto Portfolios

This subsection examines the sophisticated risk mitigation and yield optimization techniques increasingly adopted by institutional investors integrating cryptocurrency assets. Building on the growing institutional embrace of digital assets covered earlier, it delves into how portfolio managers actively manage crypto volatility, hedge against extreme downside events, and enhance returns through layered yield overlay strategies. Understanding these advanced approaches is essential for strategic allocation decisions that balance crypto’s asymmetric upside with disciplined downside control in volatile market regimes.

Growing Penetration of Volatility Targeting Models in Institutional Crypto Portfolios

The persistence of elevated and clustered volatility in cryptocurrency markets has driven institutions to adopt volatility-targeting allocation frameworks as a core risk management strategy in 2026. These models dynamically adjust exposure weights based on real-time and forecasted volatility regimes, aiming to stabilize portfolio risk contributions and enhance risk-adjusted returns across full market cycles. Survey data from leading asset managers indicate that nearly 70% of institutional crypto desks incorporate either rule-based or AI-enhanced volatility targeting algorithms, a significant increase compared to prior years.

These strategies often leverage advanced econometric models such as Exponential GARCH variants that capture the nonlinear, autocorrelated nature of crypto volatility, providing nuanced inputs for tactical weighting decisions. The institutional embrace reflects improved data availability and computational capacity, allowing for sophisticated regime detection and proactive position sizing. This dynamic approach reduced drawdowns during the crypto market turbulence of early 2026, enabling investors to maintain strategic crypto exposure while managing portfolio risk budgets effectively.

Institutional Usage and Effectiveness of Out-of-the-Money Bitcoin Options for Downside Protection

Out-of-the-money Bitcoin (BTC) options have emerged as a prominent tail-risk hedging tool employed by sophisticated institutional investors during Q1 2026. Usage statistics reveal that over 45% of surveyed institutional portfolios with crypto exposure include systematically purchased protective put options, primarily on BTC, designed to cap losses during severe market drawdowns while preserving upside participation.

These option overlays benefit from the deepening liquidity and maturities available on regulated derivatives venues, which have matured alongside increasing institutional demand. The ability to finely calibrate strike prices and maturities has enabled managers to execute cost-efficient hedges aligned with specific risk tolerance and portfolio mandates. Data shows that these hedges became particularly active during heightened volatility spikes in Q1 2026, mitigating realized losses during rapid BTC price corrections.

Portfolio stress tests incorporating these options consistently demonstrate improved Value at Risk (VaR) metrics and Sharpe ratios, underscoring their effectiveness in managing asymmetric downside risks while supporting strategic crypto allocation longevity.

Adoption of Tokenized Money-Market Fund Overlays to Enhance Yield and Liquidity Profiles

Tokenized money-market funds (MMFs) have gained rapid traction among institutional investors as a complementary yield overlay within crypto portfolio strategies. These instruments, often backed 1:1 by short-dated U.S. Treasury securities and high-quality commercial paper, provide on-chain yield generation with minimal credit or liquidity risk, effectively bridging traditional fixed-income characteristics into crypto-native portfolios.

Market analysis indicates that issuance and assets under management in tokenized MMFs more than doubled in the first five months of 2026. Institutional adoption rates reached 35% among digital asset desks, reflecting a rising preference for secure, cash-like instruments to manage portfolio buffer allocations or reduce overall volatility.

Integrating tokenized MMFs allows investors to monetize idle capital within crypto wallets while maintaining rapid liquidity for opportunistic redeployment during market dislocations. This approach enhances systemic portfolio resilience, smoothing emission curves of returns and enabling a multi-dimensional yield overlay complementary to staking or lending activities.

Having explored these sophisticated strategies for volatility management, downside protection, and yield enhancement, the report will next broaden the lens to assess how macroeconomic and regulatory dynamics influence cross-asset implications and portfolio construction frameworks.

5. Macro Environment and Cross-Sector Implications: Trade Tensions, AI Integration, and Stablecoin Evolution

U.S.-China Trade Truce Catalyzes Market Rally and Crypto Stabilization in Mid-2025

This subsection situates the pivotal geopolitical event of May 2025 within the broader market context, demonstrating how the temporary de-escalation in U.S.-China trade tensions served as a catalyst for robust equity gains in AI-driven technology stocks and triggered renewed institutional confidence in digital assets. Understanding this phase is critical to framing the macroeconomic environment that underpins current valuations and investment flows addressed later in the report.

Quantifying the May 2025 S&P 500 and Nasdaq Surge Linked to Trade Policy Easing

The announcement of a tentative U.S.-China trade truce in May 2025 marked a decisive inflection point for equity markets, particularly in the technology sector. During the five-day period following May 12, the S&P 500 Index experienced a cumulative gain of approximately 4.5%, with the initial spike on May 12 alone registering a 3.26% increase. Concurrently, the Nasdaq Composite outpaced the broader market with a gain exceeding 6% across the same timeframe, reflecting concentrated buying interest in tech-related equities.

These gains effectively erased earlier losses incurred in 2025, signaling restored investor optimism amid the reduction in tariff-related uncertainties. The rally was characterized not merely by breadth but by a renewed concentration of capital into technology leaders, especially those with direct exposure to AI chip manufacturing and cloud infrastructure, setting the stage for sustained sector dominance.

Tariff Adjustments and Export Policy Reform Boost AI-Capex and Semiconductor Stocks

Integral to the market uplift was the substantive easing of tariffs implemented by both the U.S. and China as part of the trade truce agreement. Tariff rates on critical technology components and semiconductor exports were reduced from an effective peak of approximately 24% to 10% for a provisional 90-day window, alleviating immediate cost pressures on key supply chains and enabling freer movement of goods essential to AI hardware production.

Export control relaxations additionally facilitated new deals, notably enabling Nvidia to secure a landmark order for 18,000 AI chips from Saudi Arabia. This contract underscored the growing international demand for AI hardware and accentuated the critical role U.S. export policy plays in sustaining the global expansion of American semiconductor firms. The resulting stabilization of supply chains allowed technology firms to accelerate capital expenditure plans, fueling the AI infrastructure buildout.

Institutional Crypto ETF Inflows: A Consequence of Improved Market Sentiment Post-Trade Truce

The improved macroeconomic backdrop fostered by the trade truce translated beyond equities into digital asset markets via renewed institutional confidence in regulated crypto investment vehicles. Aggregate inflows into Bitcoin ETFs surged, with net contributions reaching tens of billions of dollars in the months following the announcement, including a significant $18.7 billion inflow in the first quarter of 2026 alone.

This influx was driven largely by institutional reallocations favoring regulated crypto exposure amidst ongoing regulatory clarity and the maturation of digital asset frameworks globally. The truce alleviated risk premia and stabilized capital flows, enabling larger institutional players to increase their footprint in the crypto space with a growing preference for flagship assets such as Bitcoin and Ethereum, while maintaining vigilance over geopolitical and systemic risks.

Correlating AI Sector Equity Resurgence With Eased Trade-Related Export Restrictions

The relief from trade tensions directly correlated with pronounced rebounds in AI-capex driven stocks, led by Nvidia and other semiconductor manufacturers. After previous half-year stagnations attributed partly to export control uncertainties, prices surged over 3% immediately post-announcement, buoyed by contract wins and announcements of expanded buyback programs by competitors.

This resurgence played a pivotal role in sustaining the broader technology index rallies, with the 'Magnificent Seven' tech leaders driving over 60% of S&P 500 gains during this period. The impact underscored the market’s growing dependence on AI innovation as a growth engine and its sensitivity to geopolitical developments affecting supply chains and export regulations.

Having established the catalytic role of the U.S.-China trade truce in powering AI-centric equity rallies and institutional crypto inflows, the following sections delve into the financial and strategic dynamics of key technology players and crypto market participants operating within this evolving macroeconomic framework.

Tokenization and Stablecoin Integration: Institutional Cryptocurrency’s Bridge to Traditional Finance

This subsection explores the accelerating integration of tokenized assets and stablecoins within institutional portfolios, emphasizing how these technologies serve as critical conduits linking conventional financial systems and digital asset frameworks. By dissecting XRP’s institutional adoption, evaluating stablecoin volumes supporting decentralized finance on-ramps, and analyzing crypto-denominated debt instruments, this analysis contextualizes the evolving regulatory environment that facilitates seamless capital flows and broadens institutional crypto exposure in 2026.

XRP's Rising Institutional Adoption and Market Penetration in 2026

XRP has solidified its status as a pivotal asset within institutional digital finance through marked increases in ETF inflows and adoption by leading financial entities. By early 2026, XRP-linked ETFs amassed over one billion dollars in net assets under management, underscoring growing institutional appetite supported by clearer regulatory classification as a digital commodity. Several top-tier institutions, including prominent global banks, maintain significant XRP ETF positions, emphasizing sustained conviction in XRP's role as a settlement asset. Quantitative blockchain data reinforce this trend, with transaction volumes on the XRP ledger surging by more than 60% year-over-year, signaling heightened on-chain economic activity linked to enterprise usage and liquidity provisioning.

Market participant surveys further validate institutional interest, revealing that a growing segment of asset managers plans to increase XRP allocations contingent on regulatory clarity and compliance advancements. Key catalysts include the successful rollout of stablecoin variants tied to the XRP ledger and partnerships with major payment and banking institutions, which collectively anchor XRP's expanding utility in cross-border settlements and decentralized finance protocols.

Stablecoin Volumes Powering DeFi On-Ramps and Institutional Market Entry

Fiat-backed stablecoins have become the backbone of institutional cryptocurrency entry, facilitating efficient and reliable on-ramp/off-ramp mechanisms across DeFi and broader digital asset ecosystems. Transaction volumes for leading stablecoins such as USDT and USDC have exceeded $5 trillion annually in 2026, rivaling traditional payment processors and effectively serving as ‘digital dollars’ in markets with limited banking access. This immense throughput is bolstered by institutional adoption of transparent, fully backed stablecoin variants that align with compliance standards.

Stablecoins' integral role in decentralized finance extends to lending, borrowing, and treasury operations, where their near-instant settlement and stability reduce counterparty risk and improve liquidity management. The rapid expansion in stablecoin market capitalization and usage underscores their function as critical instruments for traditional financial institutions navigating digital asset adoption. Moreover, algorithmic stablecoins and crypto-collateralized variants offer a spectrum of risk-return profiles, enabling nuanced portfolio construction and risk mitigation within institutional frameworks.

Growth in Crypto-Denominated Debt Instruments and Tokenized Securities

Institutionally focused crypto lending markets have experienced significant growth, particularly in tokenized asset-backed debt instruments, which now account for tens of billions of dollars in outstanding loan volume. These instruments provide new avenues for portfolio diversification and yield generation while harnessing blockchain’s transparency and efficiency benefits. Crypto-collateralized loans underpin much of this market, with stablecoins dominating as collateral, enabling firms to access liquidity without traditional credit intermediaries.

Simultaneously, regulatory progress has paved the way for tokenized securities that represent traditional equities and fixed income on blockchain platforms. Jurisdictions such as the United States and South Korea are advancing legal frameworks to standardize issuance, trading, and settlement of these assets, enabling 24/7 market access, fractional ownership, and reduced settlement latency. The anticipated launch of SEC-compliant tokenized stock trading platforms later in 2026 is expected to catalyze institutional participation, with key financial players integrating these instruments into treasury management and issuance pipelines. This convergence of real-world assets and crypto infrastructure marks a transformational step in embedding digital assets within mainstream financial ecosystems.

Regulatory Advances Underpinning Tokenized Finance Accessibility

The maturation of regulatory frameworks around tokenization has been pivotal to institutional adoption, enabling secure and compliant access to digital securities. Key developments include the SEC’s upcoming rules permitting third-party issuance of tokenized stocks without issuer consent, effectively lowering barriers for market entry and fostering innovation in securities trading infrastructure. South Korea’s legislative reforms have cemented blockchain-based securities as recognized financial instruments, setting comprehensive standards for custody, issuance, and investor protections.

Globally, regulatory bodies continue to adopt a ‘same risks, same rules’ approach for tokenized assets, ensuring these instruments adhere to existing securities laws despite their technological wrapper. Enhanced risk management requirements around technology, custody, and cybersecurity further reinforce investor safeguards. As tokenized securities move from experimental stages to institutional-grade assets, regulatory clarity provides the confidence necessary for traditional financial institutions to allocate capital and integrate tokenized products into their strategic frameworks.

Having established how tokenization and stablecoins are bridging the divide between traditional finance and digital assets through institutional adoption, regulatory advancements, and robust market infrastructure, the report will now transition to synthesizing these insights with broader macroeconomic factors and strategic portfolio implications to inform decision-making in a complex investment landscape.

6. Synthesis and Strategic Recommendations: Prioritizing Opportunities Amidst Complexity

Portfolio Construction Frameworks: Balancing Growth, Stability, and Convexity