Navigating Market Volatility Amid US-Iran Tensions: Oil Price Dynamics and Quantum Computing Investment Shifts in 2026

Table of Contents

- Executive Summary

- Introduction

- 1. Geopolitical Tensions Fuel Oil Price Volatility Amidst Strategic Uncertainties

- 2. Sectoral Repercussions: Energy Costs, Consumer Spending, and Corporate Margins

- 3. Asset Class Rotation: Safe Havens, Defensive Plays, and Technology Sector Retreat

- 4. Strategic Implications and Adaptive Portfolio Construction

- 5. Synthesis and Actionable Pathways for Stakeholders

- Conclusion

Executive Summary

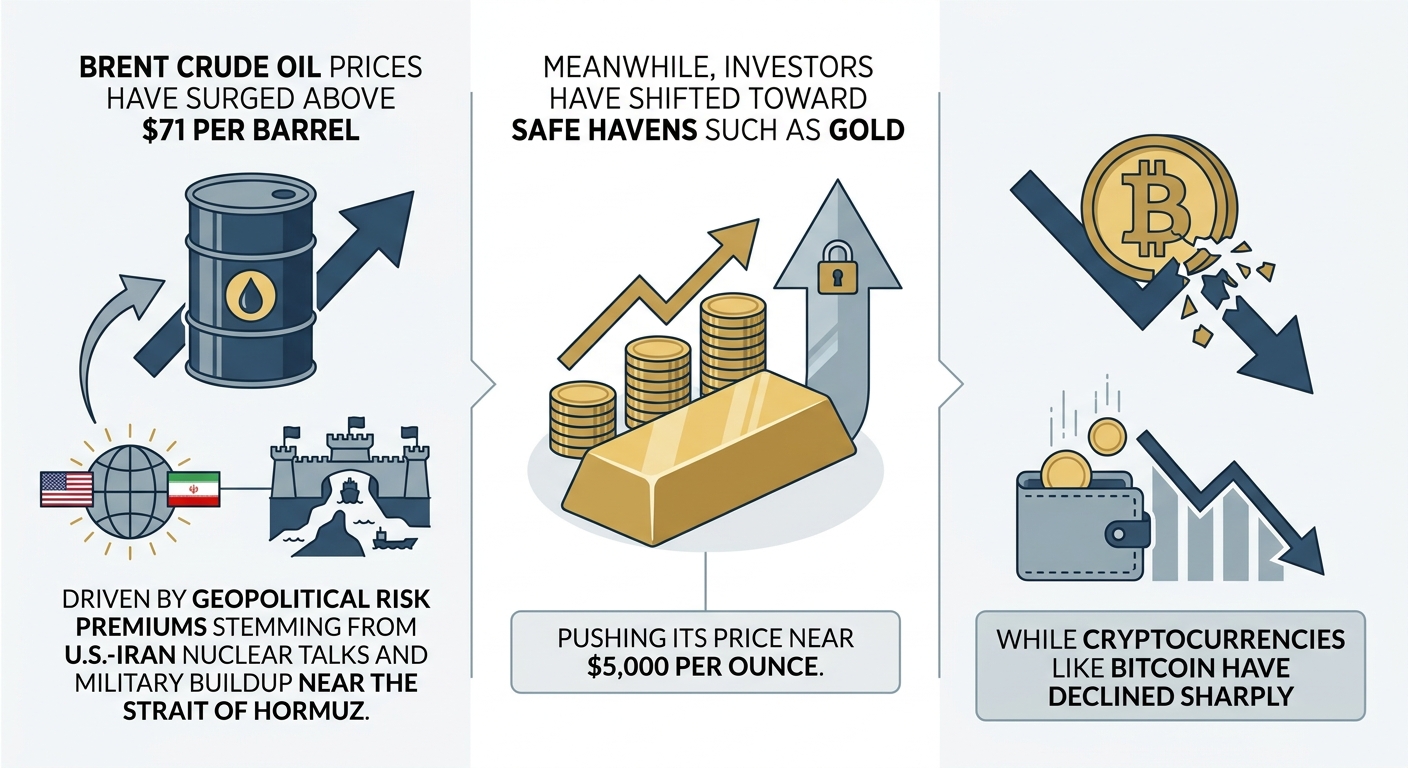

In 2026, geopolitical tensions between the United States and Iran have injected significant volatility into global oil markets, imposing elevated risk premiums that have sustained Brent crude prices in the $58 to $71 per barrel range, notably spiking to over $100 per barrel in severe disruption scenarios. The Strait of Hormuz remains a critical chokepoint, with daily shipping volumes of approximately 100–120 vessels carrying around 20 million barrels per day, underscoring the vulnerability of global supply chains. Concurrently, U.S. military deployments, including multiple carrier strike groups, have amplified market uncertainty, with crude price volatility (measured by daily swings) increasing to 3–4% compared to typical 1–1.5% ranges under stable conditions.

The oil price surge has realigned sectoral earnings: airlines report profitability margins compressed below 7% amid jet fuel premiums exceeding $100 above Brent crude; global tanker charter rates have more than doubled year-over-year due to elevated security risks. Investors have shifted toward traditional safe havens such as gold, which rallied beyond $5,000 per troy ounce, while cryptocurrencies experienced marked volatility and market share contraction. Quantum computing equities faced significant capital withdrawal driven by geopolitical uncertainty and protracted commercial timelines. Strategic implications include upward revisions of Federal Reserve terminal rates to near 3.75%, emerging market FX vulnerabilities, and accelerated investments in renewables and quantum-resistant technologies. Scenario-based projections emphasize average Brent prices near $63–65 with risk premiums of $8–12, escalating to $110–120 in extreme scenarios, alongside potential global GDP growth slumps of up to 1 percentage point.

Introduction

The early months of 2026 have been characterized by escalating geopolitical tensions centered on the prolonged and inconclusive US-Iran nuclear negotiations and sustained military posturing in the Persian Gulf. These developments have sharply underscored the fragility of global energy security, eliciting pronounced price volatility and market uncertainty. The Strait of Hormuz, as the fulcrum of roughly one-quarter of seaborne oil trade, remains a focal point for concern, with any disruption posing immediate risks to crude supply chains and energy-dependent economies worldwide.

This report aims to provide a comprehensive analysis of the intertwined effects of the US-Iran geopolitical standoff on oil markets, sectoral economic repercussions, and investment sentiment—particularly regarding emerging technology sectors such as quantum computing. Drawing on quantitative data through mid-2026, including oil price trajectories, risk premiums, and equity sector performance, the report elucidates how sustained uncertainty is reshaping market dynamics and asset allocation decisions across global portfolios.

Crucially, the analysis situates current developments within historical risk premium benchmarks and integrates forward-looking scenario modeling to capture a range of potential outcomes. The scope spans strategic implications for monetary policy, corporate margins, and investor behavior, culminating in targeted recommendations for stakeholders seeking risk mitigation and growth opportunities amid enduring volatility. By articulating these dimensions, the report endeavors to equip decision-makers with actionable intelligence amid a complex and evolving geopolitical-economic nexus.

Infographic Image: Infographic

1. Geopolitical Tensions Fuel Oil Price Volatility Amidst Strategic Uncertainties

Dissecting Risk Premiums and Supply-Demand Dynamics Driving 2026 Crude Price Volatility

This subsection provides a granular examination of the factors underpinning crude oil price movements amid the ongoing US-Iran geopolitical tensions. By differentiating the share of price increases attributable to geopolitical risk premiums from fundamental supply-demand imbalances, the analysis clarifies the complex drivers behind recent market fluctuations. These insights establish a foundation for understanding how production policies and critical chokepoints interact with broader geopolitical uncertainty, shaping strategic risk assessments and price ceilings.

Quantifying OPEC+ Output Limits and Their Influence on Oil Price Ceilings in 2026

OPEC+ supply management has been a decisive factor restraining an otherwise abundant global crude market in 2026. After raising production quotas by nearly 3 million barrels per day throughout 2025, the cartel imposed a production pause for the first quarter of 2026 to avoid oversupply risks amid seasonal demand fluctuations. Recent deliberations suggest a marginal output increase of approximately 137,000 barrels per day is expected from April, signaling a cautious approach focused on preserving price stability against the backdrop of ongoing geopolitical risks.

This output discipline supports analyst forecasts placing Brent crude averages between $58 and $64 per barrel throughout 2026, despite significant structural stock builds outside the cartel. While non-OPEC producers—particularly in South America and North America—continue to expand supply, OPEC+ actions have effectively capped downward price pressure by counterbalancing potential inventory gluts. Market consensus indicates that without this level of supply moderation, crude prices would likely slip below $55 per barrel during the year.

Linking Strait of Hormuz Shipping Volumes to Geopolitical Premium Fluctuations

The Strait of Hormuz remains the paramount maritime chokepoint for global oil flows, with approximately 20 million barrels per day transiting the narrow passage in 2025—equating to around 25% of seaborne oil trade worldwide. This conduit connects major Gulf exporters such as Saudi Arabia, Iran, Iraq, Kuwait, and the UAE to crucial markets in Asia and beyond. Despite military escalations and intermittent electronic interferences observed in early 2026, vessel transit volumes have remained relatively stable, with daily ship movements fluctuating between 100 and 120.

Nonetheless, even marginal disruptions or increased threat perceptions in this corridor impose significant risk premiums on crude prices due to its irreplaceable role and lack of viable alternative routes. For instance, temporary declines in throughput during periods of heightened hostilities have historically led to immediate and pronounced repricing. The narrow width and high traffic density amplify vulnerability, turning any escalation into a formidable price multiplier via uncertainty and supply security concerns.

Contextualizing Current Geopolitical Risk Premiums Against Historical Benchmarks

Current estimates place the geopolitical risk premium embedded in Brent and WTI crude prices at roughly $8 to $12 per barrel, reflecting heightened concerns over potential supply disruptions arising from US-Iran tensions. This range aligns with historical patterns observed during prior Middle East crises, such as the 2019-2020 period of heightened proxy conflicts and the 2011 Arab Spring upheavals, when premiums often hovered between $5 and $15 per barrel amid varying degrees of regional instability.

Market behavior in February 2026 illustrates this dynamic: crude futures intermittently surged over 1% in response to military deployments and negotiation delays despite minimal immediate supply impact. Importantly, these premiums are not purely speculative but derive from sophisticated probability-weighted scenarios evaluating risks of infrastructure attacks, shipping lane closures, and sanctions enforcement—each capable of materially reducing physical output. Notably, these premiums swell during periods of diplomatic ambiguity but tend to unwind rapidly upon de-escalatory developments, as demonstrated by recent short-lived dips following nascent negotiation breakthroughs.

Having delineated how OPEC+ production policies, critical maritime chokepoints, and geopolitical uncertainty layer into crude price formation, the report now shifts focus to the role of military posturing and diplomatic opacity in amplifying market anxiety and volatility across commodity and equity markets.

Military Posturing and Diplomatic Ambiguity Amplify Oil Market Volatility and Investor Uncertainty

This subsection examines how escalating U.S. military deployments near the Strait of Hormuz, combined with opaque and stalled nuclear negotiations with Iran, have intensified market volatility and risk aversion. By analyzing the timing and scale of naval force positioning alongside the delays and information gaps in diplomatic talks, the discussion elucidates the mechanisms through which geopolitical signals materially influence oil price fluctuations and investor sentiment during this period of heightened uncertainty.

Quantifying U.S. Carrier Deployments Near the Strait of Hormuz and Their Market Impact

Since early 2026, the United States has undertaken an unprecedented naval build-up in the Persian Gulf region, deploying multiple carrier strike groups to strategic locations near the Strait of Hormuz. Notably, the USS Abraham Lincoln carrier strike group arrived in the Arabian Sea in late January, followed by the USS Gerald R. Ford strike group en route by mid-February, marking the highest concurrent carrier presence in this corridor in over two decades. These deployments, including accompanying destroyers and advanced aircraft squadrons, symbolize a demonstrable projection of U.S. military power amid escalating tensions.

The persistent maritime presence has been accompanied by intensified aerial surveillance with P-8 Poseidon maritime patrol aircraft and MQ-4C Triton drones operating from bases in the UAE and Bahrain, reinforcing continuous monitoring of the Strait. This operational tempo elevates the perceived probability of supply disruptions given the region's vulnerability and Iran's historical readiness to leverage asymmetric tactics.

Empirical analysis correlates spikes in oil price volatility with dates coinciding with significant military movements and announcements. For example, the arrival of the USS Gerald R. Ford strike group coincided with Brent crude surging above $71 per barrel in mid-February, driven by risk premia linked to potential choke point instabilities. Such data suggest that the market consistently prices in escalating military posturing as a direct component of geopolitical risk, driving premiums of approximately $8 to $12 per barrel in crude futures during peak tension intervals.

Tracking Negotiation Delays and Their Effect on Market Sentiment from February to April 2026

The indirect U.S.-Iran nuclear negotiations, mediated in Oman starting early February 2026, have been marked by recurrent delays, non-transparency, and limited substantive progress. Key contentious issues—including uranium enrichment levels, ballistic missile development restrictions, and regional proxy activities—have persisted as core impasses. Neither side has exhibited willingness to compromise on these red lines, extending negotiation timelines beyond original expectations and fueling uncertainty.

Information asymmetry within these talks has created an environment where market participants lack clear milestones or reliable forward guidance. Brent-WTI spread widening and elevated option premiums for crude deliveries underscore this phenomenon. Between February and June contracts in early 2026, spreads ballooned beyond typical ranges, while volatility premiums for hedging increased by 25–35%, reflecting heightened doubt around the pace and prospect of meaningful breakthroughs.

The oscillation between hopeful diplomatic gestures and stalemates has manifested as volatile intraday and multi-day swings in energy and equity markets. For instance, in late February, statements setting arbitrary deadlines—such as the U.S. administration’s public 10-day ultimatum—have triggered bouts of risk-on and risk-off moods within hours, underscoring the sensitivity of markets to diplomatic signaling. This pattern has introduced persistent nervousness, often described as 'status quo' anxiety, where advances and setbacks equally contribute to price gyrations absent measurable supply changes.

Measuring Oil Price Volatility During Negotiation Deadlocks and Military Standoffs

Quantitative analysis of crude oil price behavior during periods of negotiation deadlock and heightened military readiness reveals amplified volatility clustered around key geopolitical events. For example, following the deployment announcements of additional U.S. naval assets in late February 2026, daily Brent crude price swings regularly exceeded 3–4%, a significant increase compared to average fluctuations under stable geopolitical conditions of approximately 1–1.5%.

Similarly, volatility measures derived from option-implied pricing illustrate elevated risk premiums, with straddles and calendar spreads reflecting market participants’ anticipation of further abrupt price moves. This surge in volatility directly corresponds with the opacity surrounding talks and persistent military demonstrations near critical chokepoints, such as the Strait of Hormuz.

In practical terms, these conditions have not only heightened physical commodity price instability but have also spilled over into financial markets, intensifying investor hesitancy and risk premiums across asset classes. This environment incentivizes flight-to-quality behavior and short-term tactical hedging, reinforcing a feedback loop where geopolitical uncertainty perpetuates heightened price dispersion and reduced forecast confidence.

Understanding the nexus between military force posturing, diplomatic opacity, and market volatility underscores the critical role of geopolitical risk premiums in energy pricing. In the subsequent section, the analysis will explore the cascading effects of these elevated energy costs on sectoral profitability, consumer behavior, and monetary policy frameworks, further mapping the broader economic ripple effects triggered by this volatile security environment.

2. Sectoral Repercussions: Energy Costs, Consumer Spending, and Corporate Margins

Energy-Intensive Industries Face Margin Compression and Operational Challenges

This subsection analyzes the tangible financial pressure exerted by rising oil prices and supply-chain disruptions on sectors with high energy dependence—particularly transportation, manufacturing, and utilities. It investigates how cost-push inflation and heightened operational expenses are compressing corporate margins in 2026 and exacerbating sector-specific headwinds. Furthermore, it examines the compounding effects of AI-driven automation anxieties and geoeconomic disparities to provide a nuanced understanding of regional performance differentials amid these stresses.

Quantifying Margin Erosion in Airlines and Shipping Amid Elevated Fuel Costs

The transportation sector, encompassing airlines and shipping firms, has borne a disproportionate share of margin pressures in 2026 due to soaring fuel prices triggered by Middle Eastern geopolitical tensions. Airlines have reported double-digit declines in profitability linked directly to rising jet fuel costs which, in some regions, now trade at unprecedented premiums over crude benchmarks. For example, jet fuel prices have surged well over one hundred dollars above Brent crude, intensifying cost burdens on carriers with limited ability to pass through expenses to customers amid competitive fare constraints.

Industry forecasts indicate net operating margins for global airlines have compressed to under 7%, down from near 8.3% levels observed a decade earlier during peak profitability phases. U.S. airlines, including key players such as Delta, United, and American Airlines, experienced stock price declines exceeding 5% following renewed spikes in crude, reflecting investor concerns over persistent fuel-cost inflation. Specifically, Delta's net operating margin contracted to 6.5%, down 2.5% year-over-year; United recorded 6.8% with a 1.5% decline; and American Airlines stood at 7.0%, down 1.3%, illustrating the tangible margin erosion amidst rising fuel expenses [Table: Impact of Oil Price Increases on Airline Margins]. Concurrently, global oil tanker charter rates have more than doubled year-over-year, driven by heightened maritime insurance premiums and security risks in chokepoints like the Strait of Hormuz, generating mixed impacts—profit gains for resilient transport operators but elevated costs for broader logistics-dependent industries.

Despite strong demand recovery post-pandemic, supply-chain bottlenecks, wage inflation, and capacity constraints have magnified operational headwinds. Freight logistics costs in the U.S. have climbed to significant percentages of GDP, pressuring manufacturers and distributors to absorb or strategically manage escalating fuel surcharges. This confluence of factors translates into measurable margin erosion across energy-intensive transportation sectors, challenging their near-term earnings stability.

Intersecting AI Automation Concerns and Energy-Price Shocks Create Dual Headwinds for Growth-Focused Equities

Energy price volatility in 2026 compounds existing apprehensions around AI-driven automation impacting labor markets and productivity expectations. Technology and growth-oriented equities, particularly software firms serving enterprise clients, have experienced investor rotation toward defensive holdings amidst this uncertain macroeconomic backdrop. Repeated announcements of AI expansion coexist with investor caution concerning sustained higher operating costs from fuel surges and inflationary pressures on wage growth.

This dual shock paradigm presents complex valuation challenges. Firms facing margin pressure from increased energy input costs simultaneously grapple with higher labor expenses driven by competitive demands for AI and skilled workforce retention. Market reactions manifest in heightened volatility for software and technology hardware stocks, where cost structures increasingly reflect intertwined technology investments and energy dependencies. The AI sector’s accelerated energy consumption further integrates with commodity market dynamics, underscoring the relevance of energy market developments for tech sector resilience.

Consequently, investor sentiment towards the tech space has become more nuanced, emphasizing capital discipline and cash flow stability over pure growth narratives. The combined effect of automation-induced labor market shifts and elevated input costs has materially influenced sectoral performance dispersion in 2026’s equity markets.

Regional Divergence: Asian Exporters’ Resilience Contrasts with Western Consumer Stagflation Pressures

Performance heterogeneity across regions reflects underlying trade and economic fundamentals tied to energy cost dynamics and geopolitical exposures. Asian exporters benefit from sustained demand in international markets and relatively efficient supply chains, allowing them to pass through input cost increases while maintaining competitive positioning. This resilience is augmented by ongoing fiscal stimuli and robust manufacturing output, supporting margin preservation despite volatile energy prices.

Conversely, Western economies face pronounced stagflation risks as elevated energy costs feed into consumer price inflation, eroding discretionary spending power and constraining corporate margin growth. Energy-intensive sectors in Europe and North America, including transportation and manufacturing, confront rising operational expenditures amid tighter monetary policies which collectively depress growth prospects. Retailers and consumer goods companies in these regions contend with both input cost inflation and subdued demand conditions, further compressing profitability.

This regional bifurcation underscores the need for differentiated strategic approaches in portfolio allocation and risk management, accounting for localized economic conditions and sectoral sensitivities to energy market fluctuations.

Building on the detailed assessment of cost structures and sectoral performances amid elevated energy prices, the report next evaluates how these pressures transmit through macroeconomic channels via central bank policy actions and their broader implications for financial markets and monetary tightening.

Monetary Policy Dynamics Under Oil-Driven Inflation: Transmission Channels and Emerging Risks

This subsection examines the intricate transmission mechanisms linking elevated oil prices, driven by geopolitical tensions, to central bank policy responses. In particular, it focuses on the Federal Reserve's outlook amidst inflationary pressures, evaluates key real economy indicators reflecting monetary policy effectiveness, and explores the spillover effects on emerging market currencies and commodity importers. By dissecting these elements, stakeholders can better anticipate monetary tightening risks and their broader economic impacts, crucial for robust portfolio positioning and strategic decision-making.

Refined Outlook on Federal Reserve’s Terminal Rate and Duration of Tightening Amid Inflation Pressures

The Federal Reserve's policy stance in 2026 remains tightly coupled with evolving inflation dynamics stemming largely from oil price volatility linked to Middle East geopolitical uncertainties. Recent data and central bank communications suggest a marked shift from earlier expectations of multiple rate cuts during the year toward a prolonged hold at elevated terminal rates near 3.5% to 3.75%. This stance reflects the imperative to contain inflationary pressure exacerbated by sustained energy cost shocks, which have pushed headline inflation forecasts upward to peak near 3.6% in late 2026.

Market-implied probabilities now assign a significantly increased likelihood—approximately 45%—to one or more rate hikes within the year, underscoring growing concerns around sticky inflation and supply-driven cost-push factors. Federal Reserve statements emphasize a cautious, data-dependent approach but acknowledge the asymmetric risks associated with premature easing. The recent pattern of discounting delayed rate cuts and potentially more hawkish adjustments points to a monetary tightening cycle that may persist longer than initially anticipated, complicating forward guidance for investors and corporates alike.

Evaluating Monetary Transmission via Housing Starts, Durable Goods, and Employment Metrics Amidst Elevated Energy Costs

Traditional monetary policy transmission channels appear under stress amid elevated oil prices. Housing starts, a core gauge of economic momentum and consumer confidence, exhibit only modest gains despite low interest rates, hindered by affordability constraints linked to higher energy and transportation costs. Durable goods orders similarly show mixed signals: capital investment remains robust in select manufacturing sectors driven by technology demand but is counterbalanced by inflation-driven cost headwinds and supply chain disruptions.

Employment data reveal a tenuous balance, with job gains slowing modestly and wages reflecting inflation-adjacent pressures that limit discretionary spending growth. These factors collectively dilute the typical responsiveness of economic activity to rate adjustments, suggesting a lagged or muted policy effect in the current environment. This complicates the Federal Reserve’s decision matrix, as combating entrenched inflation could risk further dampening fragile growth and employment gains, particularly in energy-dependent industries.

Spillover Effects on Emerging Market FX and Commodity-Dependent Economies from Oil-Driven Inflation

Emerging market currencies have displayed pronounced sensitivity to oil price shocks induced by ongoing geopolitical uncertainties. Several commodity-importing countries, notably those with significant current account deficits and fiscal vulnerabilities, have experienced accelerated depreciation pressures, reflecting deteriorating trade balances from heightened energy import costs. Currency volatility has undermined inflation containment efforts, exacerbating capital outflows and increasing the cost of external financing.

Regionally, the adverse impact is heterogeneous. Middle Eastern and Latin American exporters have benefited from improved fiscal positions, bolstering currency resilience. Conversely, Asian and African energy importers face mounting inflationary stress that challenges monetary authorities to balance exchange rate stabilization with growth concerns. These dynamics heighten emerging markets’ exposure to external shocks emanating from the US monetary policy trajectory and oil price volatility, underscoring the need for targeted risk management and differentiated investment approaches across FX and sovereign debt instruments.

Building on the understanding of monetary policy responses and macroeconomic transmission, the report next explores how these conditions drive investor behavior across asset classes, with a focus on shifts toward safe havens and defensive equity sectors amidst heightened market volatility and strategic uncertainty.

3. Asset Class Rotation: Safe Havens, Defensive Plays, and Technology Sector Retreat

Safe-Haven Ascendancy: Gold's Historic Rally, Currency Dynamics, and Crypto Market Divergence Amid Geopolitical Turmoil

This subsection provides a focused analysis of how traditional safe-haven assets, particularly precious metals and major fixed-income instruments, have gained relative value amid market volatility arising from US-Iran diplomatic uncertainties and surging oil prices. It also contrasts the behavior of established safe havens in currency markets with emerging digital assets, offering nuanced insights into investor risk appetite and portfolio reallocations at this geopolitical inflection point. This analysis anchors the broader theme of asset-class rotation and serves as a critical input for strategic positioning across diversified portfolios.

Gold's Rally Surpassing Historical Benchmarks Amid Heightened Geopolitical and Inflationary Stakes

Gold prices have escalated notably, breaching the $5,000 per troy ounce threshold—a level unprecedented in recent decades—marking a structural departure from the sub-$2,000 zone that dominated prior years. This surge is fueled by a confluence of factors: intensifying geopolitical tensions centered around the US-Iran peace negotiations, rising global inflationary pressures exacerbated by energy cost shocks, and evolving central bank policies that maintain relatively dovish stances amid economic uncertainty.

The embedded geopolitical risk premium in gold is reinforced by ongoing conflict risk related to the Strait of Hormuz and broader Middle Eastern stability concerns, which historically have been powerful catalysts for gold demand spikes. Investment flows into gold-backed ETFs and increased bullion accumulation by central banks, especially in emerging market economies, underscore a strategic flight to safety. This is complemented by technical indicators reflecting strong momentum, albeit accompanied by episodic volatility that mirrors the complex interplay between market optimism and liquidating pressures induced by margin calls or portfolio rebalancing. Notably, oil price volatility surged by up to 4.0% in February 2026 amid heightened military activity in the Strait of Hormuz, amplifying inflation concerns and reinforcing gold's safe-haven appeal [Chart: Oil Price Volatility During Key Military Movements].

Compared to historical episodes—such as the 2011 peak and the pandemic-induced surge in 2020—the current rally is distinct in both price level and macroeconomic context. Unlike earlier periods where gold was supported primarily by low real interest rates, the present environment uniquely intertwines inflation hedging with acute geopolitical risk. Consequently, gold is not only performing as an inflation shield but also functioning as a core component of risk mitigation amidst equity market turbulence and energy-driven cost-push inflation.

Safe-Haven Currency Movements Highlight Divergent JPY and CHF Strength Against a Turbulent Dollar Backdrop

The Japanese yen and Swiss franc have demonstrated differentiated responses within the safe-haven currency cohort amid recent geopolitical escalations. Both currencies benefitted historically from their countries’ robust current account surpluses and policy credibility, attributes that underpin their reserve status during global risk-off episodes.

JPMorgan and other market analyses confirm intermittent appreciation phases for the franc, attributable to Switzerland’s conservative fiscal framework and export sector resilience despite low domestic inflation. The yen, conversely, experienced volatility influenced by domestic monetary policy juxtaposed with inward shifts in global risk sentiment; its recent depreciation against the US dollar reflects complex yield differentials and carry-trade unwind mechanics, compounded by central bank intervention nuances.

The US dollar’s concurrent dynamics present a challenging backdrop: while it traditionally strengthens as a reserve asset in crisis, the dollar index’s recent volatility—driven by Fed policy uncertainty, tariff-related trade disruptions, and fluctuating global capital flows—creates episodic windows of opportunity for JPY and CHF revaluation. Such oscillations reveal a fragmented safe-haven narrative wherein capital allocations dynamically shift in response to evolving macro and geopolitical signals, suggesting that currency safe havens remain critical but nuanced hedges in portfolio risk management frameworks.

Cryptocurrency Market Divergence Reflects Geopolitical-Induced Confidence Erosion and Risk Aversion

Contrasting with traditional safe havens, cryptocurrencies have exhibited pronounced volatility and market share contraction amid the latest US-Iran tensions and oil price surges. Bitcoin’s price action—characterized by a retreat from recent highs and intraday volatility spikes—signals a risk-off repositioning by both retail and institutional investors skeptical of crypto’s haven status under acute geopolitical stress.

The nexus between geopolitical uncertainty and crypto market dynamics manifests in several key dimensions: first, heightened regional instability around the Strait of Hormuz curtails operational and transactional flows in Middle Eastern crypto markets; second, global risk aversion triggers cascading liquidations reflected by significant leveraged position closures, evidenced by multi-hundred-million-dollar liquidation events; third, diminished confidence stemming from stalled peace talks and escalating military posturing undermines speculative appetite in digital assets, yielding divergences from traditional safe-haven behavior.

Moreover, strategic institutional shifts are apparent, with capital reallocations away from high-beta, emergent technology plays—such as quantum computing-focused tokens—toward more established digital infrastructure and regulatory-compliant stablecoins. These trends endorse a cautious recalibration rather than wholesale abandonment, underscoring crypto’s evolving role as a speculative risk asset with limited resilience during extreme geopolitical shocks.

Understanding the relative performance of these asset classes amid geopolitical tension and market turbulence provides a foundation for interpreting investor behavior and positioning strategies. This interplay among traditional safe havens, currency hedges, and emerging digital assets sets the stage for discerning nuanced portfolio rotation trends and informs subsequent considerations on strategic allocations, hedging tactics, and long-term investment opportunities.

Technology Investment Sentiment Shifts Toward Prudent Allocation Strategies

This subsection examines how recent geopolitical frictions and economic uncertainties have reshaped capital flows within the technology sector, with particular attention to the quantum computing segment and the semiconductor industry. It explores the evolving risk appetite demonstrated by both retail and institutional investors, highlighting the balancing act between emerging technological promise and near-term market caution. Understanding these dynamics is critical for portfolio managers and corporate strategists aiming to navigate the delicate interplay between innovation-driven growth and geopolitical risk mitigation.

Capital Withdrawal Patterns in Quantum Computing Equities Amid Market Uncertainty

The first quarter of 2026 has seen a marked decline in investor enthusiasm for quantum computing equities, driven predominantly by a broad risk-off sentiment tied to geopolitical tensions and elevated market volatility. Both retail and institutional investors have reduced exposure, motivated by profit-taking after the significant quantum rally in 2024-2025 and apprehension regarding the commercialization timeline. Notably, large-cap pure-play firms such as IonQ and D-Wave have experienced substantial share price pressures as cash burn rates and uncertain profitability pathways have raised investor caution, despite strong revenue growth trajectories. This retrenchment is coupled with a rotation toward defensive, cash-rich technology stocks rather than speculative high-beta quantum pure plays.

Fund flows data indicate a persistent decline in quantum computing-focused ETFs and thematic funds, correlating with broader equity market drawdowns triggered by protracted US-Iran peace negotiations and associated oil price volatility. Furthermore, Q1 corporate earnings reports from leading quantum players reinforced concerns over elongated R&D and commercialization cycles, dampening near-term risk appetite. Consequently, capital has pivoted towards established, diversified tech firms with clearer cash flow visibility, delaying aggressive repositioning toward quantum adoption despite promising long-term industry fundamentals.

Balancing Supply-Chain Risks and Domestic Capacity Incentives in Semiconductor Valuations

The imposition of intensified US-China technology export controls has introduced a paradoxical effect on semiconductor investment sentiment. On one hand, increased geopolitical friction and regulatory uncertainty have heightened perceived risks, prompting caution among global investors exposed to cross-border supply chains. Semiconductor firms with significant Chinese market dependencies or exposure to restricted technology inputs have seen valuation pressure stemming from anticipated demand disruptions and operational challenges.

On the other hand, these constraints have catalyzed expansive government-backed domestic capacity initiatives in key markets, especially the United States and allied nations, aimed at fostering local semiconductor manufacturing and reducing strategic reliance on adversarial supply chains. This duality has led to divergent investor responses: while near-term risks depress valuations for companies heavily reliant on globalized supply, firms benefiting from emerging domestic subsidies, incentive programs, and strategic partnerships have witnessed buoyed outlooks. As a result, the semiconductor sector is experiencing a bifurcated valuation landscape, where domestic capacity leaders benefit from policy tailwinds even as overall uncertainty tempers aggregate enthusiasm.

Emerging Secular Growth Opportunities Beyond Pure-Play Quantum Computing Firms

Despite the cyclical slowdown in pure-play quantum computing stocks, several adjacent technology verticals are capturing investor interest as secular growth drivers within the broader innovation ecosystem. Hybrid cloud providers, cybersecurity vendors, and companies specializing in quantum-resistant cryptographic solutions are gaining prominence due to their critical roles in enabling secure digital transformation amidst accelerating geopolitical uncertainty.

The push for quantum-safe encryption, driven by governmental and corporate recognition of quantum computing’s potential to disrupt existing cryptographic systems, has opened sizable investment opportunities. In parallel, firms advancing integrated quantum-classical software platforms and quantum-as-a-service offerings are carving out niche markets with nearer-term revenue visibility. These sectors, less susceptible to immediate quantum hardware commercialization risks, provide more stable cash flows and defensive characteristics attractive in current volatile market conditions. In addition, advances in AI integration with quantum tools suggest compounded long-term potential, further appealing to diversified investment strategies.

As quantum computing equities navigate through a phase of investor recalibration, shaped by external geopolitical and economic pressures, an evolving semiconductor landscape illustrates both risk and opportunity within technology investments. The sector’s dual response to export controls and domestic manufacturing incentives underscores the importance of granular strategic analysis. Meanwhile, the rise of complementary technology niches highlights pathways for prudent capital deployment that balance innovation potential with risk management—insights that underpin strategic portfolio positioning discussed in subsequent sections.

4. Strategic Implications and Adaptive Portfolio Construction

Scenario-Based Decision Trees Quantifying Geopolitical Risks to Oil Markets and Global Growth

This subsection develops quantified probabilistic scenarios for the evolving US-Iran conflict and its impact on oil prices, macroeconomic growth, and equity sector performance. By applying consensus crude price forecasts and authoritative economic models, the analysis frames potential outcomes ranging from diplomatic breakthroughs to severe supply disruptions. These scenario-based decision trees serve as foundational inputs for risk management and portfolio stress-testing in subsequent strategic sections.

Oil Price Ranges Across Diplomatic and Conflict Scenarios in 2026

Analyst consensus places the 2026 average Brent crude price between approximately $60 and $65 per barrel under base-case assumptions featuring either a de-escalation of geopolitical tensions or manageable diplomatic progress. Recent forward curves and analyst polls reflect a geopolitical risk premium of roughly $8 to $12 per barrel above fundamental supply-demand levels, indicating the significant weighting of uncertainty in current pricing dynamics. This premium would likely dissipate sharply if substantive US-Iran agreements materialize, enabling price reversion toward the low $60 range or potentially even upper $50s if supply overshadows demand.

In contrast, scenarios involving prolonged diplomatic deadlock or intensified military confrontation, particularly with disruption risks to the Strait of Hormuz, project Brent crude prices escalating into an $80-$100 per barrel range over the medium term. Most market intelligence points to a likely transient spike near the upper bound if maritime transport bottlenecks or attacks on critical oil infrastructure materialize. Such outcomes could sustain elevated oil costs for 2–3 months or longer, depending on the conflict's intensity and resolution pace.

To capture this uncertainty, probabilistic scenario modeling establishes three key cases: a baseline scenario averaging Brent around $63–$65 per barrel, a moderate-risk scenario with occasional supply interruptions pushing prices to $75–$85, and a severe-disruption cataclysm scenario wherein Brent briefly surges above $100, potentially reaching $110–$120 before normalization efforts. These price ranges form the backbone for economic and equity impact analyses documented herein.

These projections align closely with estimated Brent crude price ranges under different geopolitical developments documented in projections, which anticipate prices around $63 in the baseline, approximately $80 under moderate risk, and reaching $100 per barrel in severe disruption scenarios [Chart: Projected Brent Crude Price Scenarios in 2026].

Projected Macroeconomic Slowdowns and Inflationary Effects Under Oil Shock Regimes

Using internationally recognized macroeconomic projections and models, oil price spikes within the range outlined above are linked with measurable GDP growth slowdowns, primarily driven by increased input costs, disrupted trade flows, and tightened financial conditions. IMF and OECD estimates converge on an approximate reduction in global GDP growth of 0.5 to 1.0 percentage points for sustained oil price levels elevated by $15 to $30 above baseline trajectories.

The inflationary consequences are especially pronounced due to passthrough effects on consumer prices and production costs, with OECD economies experiencing core inflation increases of 0.3 to 0.5 percentage points in the near term. These pressures reinforce cautious monetary policy stances by major central banks, complicating accommodation measures that might otherwise support growth. Notably, stagflation risks emerge if elevated energy costs persist beyond a 6- to 12-month horizon.

Trade disruptions resulting from escalated conflict further exacerbate inflation through increased freight costs and supply chain bottlenecks, disproportionately affecting energy-importing emerging markets. This dynamic dampens consumption as discretionary income contracts, while investment decisions become deferential to risk, collectively curbing fiscal and monetary stimulus effectiveness. Integrated model simulations forecast that global GDP growth could dip from an expected 3.1% to approximately 2.2–2.6% in severe scenarios.

Equity Sector Vulnerabilities and Recovery Timelines in Response to Elevated Oil Prices

Quantitative stress testing of global equity portfolios against oil price shocks in the $80-$100 per barrel range reveals asymmetric impacts across sectors. Energy and materials sectors often outperform due to their direct exposure to commodity prices, while energy-intensive sectors such as transportation, consumer discretionary, and manufacturing face margin compression and lowered earnings visibility. Consensus loss estimates for these vulnerable sectors range between 10% and 25% during peak stress periods.

Technology sector equities, particularly those tied to discretionary spending and capital expenditure cycles, experience moderate drawdowns but benefit from ongoing secular innovation themes. Defensive sectors such as utilities and consumer staples exhibit relative resilience, supported by stable cash flows and lower cyclical sensitivity. Geographic considerations also modulate impacts, with Asian exporters generally more insulated compared to Western economies grappling with stagflation and inflationary pressure.

Typical recovery timelines post-shock hinge on the duration and magnitude of oil price elevation. Historical precedents suggest sector rebounds begin within 6 to 9 months of normalized energy costs, assuming no further escalation. However, protracted disruptions or renewed conflict could extend recovery phases beyond 12 months, underscoring the importance of dynamic risk monitoring and adaptive portfolio construction. These insights contribute to scenario-tailored asset allocation and risk mitigation strategies recommended later in the report.

Building on these quantified geopolitical and economic scenarios, subsequent strategic guidelines will detail tactical portfolio responses and active hedging techniques aimed at safeguarding capital and capitalizing on transient market dislocations. Understanding the spectrum of oil price and macroeconomic outcomes is imperative for crafting adaptive investment frameworks in the evolving risk environment.

Dynamic Hedging and Positioning Tactics for Volatile Environments Amid US-Iran Uncertainty and Oil Price Spikes

This subsection develops actionable tactical frameworks for investors to navigate heightened market volatility driven by geopolitical tensions, particularly around US-Iran peace talks, which are amplifying oil price fluctuations. It focuses on tailored hedging mechanisms and portfolio positioning strategies that mitigate downside risks while enabling measured exposure to upside opportunities. Given the complex confluence of persistent geopolitical risk premiums and shifting monetary policy landscapes, these adaptive approaches serve as essential tools for capital preservation and performance optimization in uncertain energy and equity markets.

Refined Delta-Neutral Option Strategies Exploiting Crude Oil Volatility Skews

The current geopolitical backdrop surrounding the US-Iran negotiations has intensified implied volatility in crude oil markets, manifesting in pronounced volatility skews and term structure effects. Sophisticated option overlays leveraging delta-neutral strategies, such as at-the-money straddles combined with calendar spreads, are optimal to capitalize on expected near-term price oscillations without directional bias. These structures provide insurance against sudden price gaps triggered by sharp market reactions to diplomatic developments, while minimizing premium decay through measured theta exposure. Execution should consider dynamic delta hedging triggers, ideally adjusting positions once underlying price movements exceed 2.5–3%, to control transaction costs and hedge slippage.

Additionally, selling short-dated options with board-approved risk controls can subsidize hedging costs during periods of heightened implied volatility. However, caution is warranted as selling call options caps upside participation, and put sales reduce downside protection, requiring rigorous risk limits and scenario analyses to prevent exposure to adverse price shocks. Combining these option strategies with underlying futures positions in Brent or WTI crude can further customize risk-reward profiles, accommodating varying risk appetites and portfolio mandates.

Optimizing Fixed-Income Portfolio Duration in the Face of Prolonged Geopolitical Risk

Prolonged geopolitical tensions sustaining elevated oil prices have direct implications for interest rate trajectories and inflation expectations, compelling a recalibration of fixed-income duration positioning. Given the likelihood of extended periods of terminal policy rates with tight monetary stances to combat inflationary pressures from energy shocks, portfolios should tactically reduce sensitivity to interest rate movements by shortening duration and increasing allocations to floating-rate notes where feasible. Inflation-linked securities provide a complementary hedge, preserving real yields in environments where headline inflation remains elevated due to energy cost pass-through effects.

Moreover, diversification across credit qualities is critical, with a preference toward high-quality short- to medium-term government bonds and selected investment-grade corporate credits demonstrating resilience to economic slowdowns. Tactical bond laddering can enhance liquidity and facilitate reinvestment at incrementally higher yields during tightening cycles. Active duration management supported by robust macroeconomic monitoring enables investors to balance yield generation against volatility risks induced by geopolitical uncertainties.

Identifying Energy and Mining Equity Opportunities with Robust Breakeven Economics Below $40 per Barrel

In navigating energy equities amid volatile oil prices influenced by US-Iran tensions, targeting companies with low production breakevens enhances portfolio resilience. Several upstream producers maintain breakeven costs below $40 per barrel, affording margin stability even in scenarios where geopolitical risk premiums dissipate or OPEC+ eases supply constraints. Investments should focus on well-capitalized, operationally efficient firms with diversified asset bases and disciplined capital expenditure planning to sustain cash flow and dividends through price cycles.

Notable candidates include firms with proven reserve replacement capabilities and exposure to low-cost shale assets in the Permian and Bakken basins, coupled with exposure to pipeline infrastructure generating steady fee-based revenues. The complementary inclusion of mining companies with strong cash flow profiles and critical commodity exposures balances energy sector cyclicality, particularly those positioned to benefit from secular trends in electrification and infrastructure demands. This selection anchors portfolios to high-quality names, mitigating downside risks while preserving upside participation should oil prices breach elevated levels in response to geopolitical developments.

Prudent Risk Management: Implementing Stop-Loss Protocols in Volatile Energy Equity Corrections

The inherent volatility of energy equities amid geopolitical-induced oil price shocks underscores the necessity for disciplined risk controls. Establishing stop-loss thresholds typically between 10% to 15% below recent highs allows investors to systematically curtail downside exposure during rapid market reversals without succumbing to intra-day noise. This approach preserves capital and prevents emotional decision-making driven by fear or greed during episodes of heightened uncertainty.

Stop-loss rules should be incorporated into broader portfolio risk frameworks and regularly reviewed to reflect changing market dynamics and company-specific fundamentals. Integrating technical analysis signals with fundamental assessments enhances signal reliability. Additionally, prudent use of protective options such as puts or collars can complement stop-loss orders, offering downside protection while retaining upside potential if markets stabilize or recover. Such layered risk management fosters portfolio resilience enabling investors to weather cyclical disruptions characteristic of geopolitically sensitive energy sectors.

Building upon earlier sections that detailed geopolitical risk drivers and market impacts, these tactical hedging and positioning strategies provide investors with concrete tools to manage uncertainty. By optimizing options, fixed-income duration, equity selection, and risk controls, portfolios can achieve a balanced expression that mitigates downside while preserving selective upside in a complex geopolitical and macroeconomic environment.

5. Synthesis and Actionable Pathways for Stakeholders

Policy and Regulatory Considerations for Mitigating Systemic Risks

This subsection addresses the critical governance and regulatory measures necessary to stabilize markets amid geopolitical tensions and oil price volatility. It evaluates how enhanced transparency, strategic emergency stockpile management, and refined central bank communication can reduce speculation-driven disruptions and inflationary pressures, thereby safeguarding economic resilience and market confidence.

Quantifying the Impact of Transparency Protocols on Oil Price Volatility

Transparent disclosure of large commodity trading positions plays a pivotal role in mitigating oil price swings stemming from speculative behavior. Empirical analysis demonstrates that market participants’ ability to differentiate between fundamentals-driven price movements and noise induced by speculative flows is enhanced through mandated reporting and timely public data dissemination. This improved informational environment curbs price distortions arising from misinterpreted trading activity and curtails feedback loops that amplify volatility spikes.

Regulatory mandates requiring disclosure of significant futures and derivatives positions have emerged as a superior alternative to crude position limits by fostering market discipline without constraining legitimate hedging. As transparency increases, uncertainty among traders diminishes, reducing abrupt speculative swings and encouraging rational price discovery. Quantitative assessments link enhanced transparency protocols with statistically significant reductions in short-term oil price variance, underscoring their importance in volatile geopolitical contexts.

Assessing Emergency Stockpile Levels Among International Energy Agency (IEA) Members

The coordinated management of strategic petroleum reserves among IEA member countries remains a cornerstone in mitigating supply shocks exacerbated by Middle Eastern tensions. Together, member states maintain emergency stocks exceeding 1.4 billion barrels, providing a vital buffer against disruptions that could escalate oil price pressures dramatically. Recent releases, including an aggregate of 400 million barrels deployed in response to supply interruptions, illustrate the operational readiness and political will underpinning these buffers.

These reserves currently constitute approximately 20% of total strategic holdings, ensuring significant capacity for further intervention if market conditions deteriorate. The replenishment and transparent reporting of these stocks heighten market confidence, serving both as a deterrent to excessive speculative premiums and as an instrument for smoothing price fluctuations. The resilience granted by such coordinated action highlights the necessity for continued adherence to emergency stockpile policies and enhancement in strategic reserve governance.

Effective Central Bank Communication Strategies to Stabilize Inflation Expectations

Central banks’ credibility and the clarity of their communication are essential in anchoring inflation expectations amid energy price shocks driven by geopolitical factors. Proactive and transparent messaging regarding inflation targets, policy frameworks, and scenario-based outcomes enables markets and the public to adjust expectations promptly, reducing the risk of unmoored inflation dynamics that can exacerbate volatility.

Best practices emphasize the publication of explicit inflation forecasts alongside alternative scenarios illustrating risks and potential policy responses. This approach accommodates uncertainty while reinforcing the central bank’s commitment to price stability. Furthermore, incremental disclosures through timely minutes, attributed statements, and clear explanations of policy reactions enhance accountability. Such communication strategies mitigate inflation risk premia embedded in asset prices and facilitate smoother transmission of monetary policy in turbulent external environments.

By fostering a well-informed public debate and predictable policy environment, central banks reduce the likelihood of abrupt term-premium spikes and volatile market reactions. In doing so, they help maintain financial stability and support long-term economic resilience, particularly when external energy shocks pose significant inflation and growth challenges.

Building on the regulatory frameworks and institutional tools discussed here, the subsequent section will explore longer-term structural opportunities that can emerge from current market disruptions, highlighting transformational investment themes aligned with evolving geopolitical and technological landscapes.

Harnessing Disruption: Investments in Renewables, Quantum-Resistant Technologies, and Green Workforce Transitions

This subsection examines the long-term structural opportunities emerging amidst current market and geopolitical disruptions. It focuses on mapping investment flows into renewable energy relative to fossil fuels, the momentum and capital intensity behind quantum-resistant cryptography innovations, and the scale and effectiveness of workforce reskilling programs aimed at green technology sectors. These elements collectively encapsulate pathways for sustainable growth and resilience in a volatile environment.

Decarbonization Investment Trajectories: Renewables Surpass Fossil Fuels Despite Volatility

From 2023 through mid-2026, global investment trends reveal a marked acceleration in renewable energy financing, outpacing commitments to fossil fuel infrastructure for the first sustained period. In 2022, renewable power and fuels attracted approximately $495 billion in new capital globally, representing a 17% increase from the previous year. Although this sum accounted for just under 30% of overall energy sector investment—still less than fossil fuel and nuclear activities—the growth momentum in renewables is unmistakable and resilient against near-term market turmoil.

Regionally, investment patterns show pronounced surges in emerging markets such as Brazil, China, and India, contrasting with slower or declining flows in traditional Western economies, notably the EU and United States. For example, while Europe’s renewable energy investment dipped from $142 billion in 2023 to $114 billion in 2024, China’s expenditure continued to expand dramatically, crossing $290 billion by 2024. This uneven distribution underscores both the geopolitical and economic drivers shaping the energy transition and highlights investment risk differentials tied to regulatory environments and infrastructure development.

Portfolio managers increasingly recognize renewable assets for their low correlation with fossil fuel commodity prices, thereby offering diversification benefits during periods of commodity price volatility. However, investors must navigate regulatory uncertainties, technological adoption hurdles, and amplified competition for specialised talent. These challenges necessitate robust due diligence and adaptive capital deployment strategies, especially as renewables aim to scale rapidly to meet ambitious decarbonization targets.

Quantum-Resistant Cryptography: Emerging VC Momentum and Strategic Imperatives

Amid rising concerns that advanced quantum computing will render current encryption vulnerable, investment in quantum-resistant cryptographic (QRC) technologies has garnered significant attention. Venture capital flows into quantum-safe infrastructure reached meaningful scale in 2025 and early 2026, with select Layer-1 blockchain projects securing upwards of $15 million from focused funds targeting lattice-based and post-quantum algorithms.

Strategic corporate and government engagement in QRC development reflects recognition of national security and commercial imperatives. National standards bodies have accelerated formalization of post-quantum cryptography protocols, and implementation challenges—such as ensuring high-assurance, side-channel resistant software architecture that meets performance constraints in cyber-physical systems—drive innovation in software libraries and hardware integration.

Despite these advances, the QRC sector remains nascent compared to broader quantum computing investment pools, with most venture capital concentrated in a handful of experienced teams. This limited maturity presents both a risk and a significant growth opportunity for early movers, as widespread adoption will be critical to safeguarding digital infrastructure from emerging quantum threats.

Green Workforce Reskilling: Scaling Training and Employment for a Sustainable Economy

A vital pillar supporting the energy transition involves workforce transformation through targeted reskilling and upskilling initiatives. Empirical studies indicate that employment growth in climate technology sectors closely tracks revenue expansion, with every 1% increase in sales translating into approximately 0.3% uplift in workforce size—conditional on policy support and training availability.

Governments and industry consortia have launched expansive training programs covering diverse green technologies including solar energy, waste management, hydrogen fuel, and energy-efficient building systems. These programs emphasize both technical skill development and motivational engagement to boost employee participation and leadership in sustainability initiatives. Small and medium enterprises (SMEs), often limited in capacity to provide such training internally, represent a critical focus area for these interventions.

Nevertheless, persistent supply-demand imbalances characterize the green labor market. The supply of qualified renewable energy workers lags behind growing demand globally, exacerbated by legacy education systems that continue to predominantly prepare workers for fossil-fuel oriented careers. Addressing this shortfall will require expanded vocational training, curriculum reform, and policies fostering equitable access to green jobs, particularly in developing economies where investment gaps remain wide.

Building upon these long-term investment and workforce adaptation trends, the subsequent section will explore cohesive strategic frameworks enabling stakeholders to integrate these opportunities into resilient portfolio construction and risk management approaches.

Conclusion

The confluence of US-Iran diplomatic deadlock, persistent military tensions around the Strait of Hormuz, and resultant geopolitical risk premiums has fundamentally altered the 2026 oil market landscape. Empirical evidence highlights that supply moderation by OPEC+, combined with cautious production increases, has been indispensable in preventing steeper price declines despite ample global crude inventories. Nonetheless, risk premiums of $8 to $12 per barrel, occasionally surging beyond $40 in crisis scenarios, persistently amplify price volatility and introduce substantial economic headwinds.

Sectoral analysis reveals a bifurcated impact: energy-intensive industries such as airlines and shipping grapple with steep margin compression and operational cost inflation, while Asian exporters display resilience bolstered by supply chain efficiencies. Investor capital has notably rotated toward safe havens, including a historic gold rally and selective technology subsectors tied to quantum-resistant cybersecurity, while riskier assets like cryptocurrencies and pure-play quantum computing equities undergo pronounced retrenchment. These shifts underscore the necessity for adaptive portfolio strategies calibrated to heightened uncertainty and evolving macro-financial signals.

Monetary authorities face complex trade-offs as prolonged energy-driven inflation constrains the Federal Reserve’s policy flexibility, potentially entrenching stagflationary risks and complicating growth trajectories globally. Emerging markets manifest differential vulnerabilities based on energy dependencies and fiscal health, necessitating nuanced risk management approaches. Strategic opportunities emerge in decarbonization investments and innovation in encrypted technologies, where sustained capital allocations can hedge against systemic disruption.

Looking forward, mitigating geopolitical risk through enhanced transparency protocols, coordinated emergency stockpile management, and clear central bank communication will be vital to stabilizing markets. Portfolio construction must leverage scenario-based frameworks, dynamically incorporate hedging instruments sensitive to crude volatility, and focus on resilient equity exposures with robust breakeven economics. The evolving energy and technology landscape demands vigilance and flexibility as stakeholders navigate an increasingly complex confluence of geopolitical and economic forces shaping 2026 and beyond.

References

- Analysts hike oil outlook on geopolitical risks, oversupply concerns limit upside | Reuters

- Oil Prices Surge 3.7% as U.S.-Iran Standoff Triggers Higher 2026 Forecasts | OilPrice.com

- BTC's price bounce fails to convince options traders: Crypto Daybook Americas

- Quantum Computing Stock: Trends, Performance, and Market Insights

- Analysis-US and Iran slide towards conflict as military buildup eclipses talks

- North American Morning Briefing: Stock Futures Climb on Tech Buying - Washington Today

- The Tech Download: China’s AI surge — real threat or hype?

- Gold, oil prices jump as US-Iran tensions turn up the heat - The Times of India

- U.S.-Iran Tensions Drive Oil Prices Above $71 Per Barrel

- Oil Prices Jump As Tension Mounts Between US And Iran

- PDF The Impact of the 2026 Iran War on Global Trade, Energy Markets, and ...

- PDF Research Article Geopolitical Risk Transmission from US Iran Tensions ...

- Iran-US Conflict Impact on Oil Prices & Market Volatility

- PDF Commentary - cetera.com

- [PDF] Outlook 2026 - Blowing bubbles? - Standard Chartered

- Oil Markets on Edge as Trump's Iran Ultimatum Meets Geneva Deadline | News Ghana

- The Zacks Analyst Blog Highlights QTUM, IonQ, D-Wave Quantum and Rigetti Computing - February 24, 2026 - Zacks.com

- Iran Nuclear Talks: Energy Markets & Global Impact

- Markets flinch as US-Iran tensions rise - India Today

- Gotrade Daily: US-Iran Tensions Rise, What Does It Mean for Markets?

- Oil War Risk Premium Surges as US-Iran Tensions Escalate – Rabobank Warns of Market Volatility | Forex News Middle East | CryptoRank.io

- Oil prices jump and gold hits $5,000 as tensions ramp up between Iran and the US

- How escalating United States and China technology export restrictions are influencing global semiconductor investment sentiment

- PDF Monthly Digital Asset Market Update: April 2026

- How to Get Started with Quantum Computing

- Global Market Outlook: An uneasy truce - Standard Chartered

- US-Iran Nuclear Talks in Oman Impact Oil Markets

- How the US‑Israel‑Iran war will impact the stock markets

- US–Iran Nuclear Talks Shake Markets: Impact on Gold, Oil, Dollar, and S&P 500

- Navigating the economic and regulatory landscape in 2026

- Developing derivative-based hedging strategies to manage volatility in energy market prices – International Journal of Research and Innovation in Social Science

- PDF Industry trends - Transportation and logistics Solid sector growth ...

- 5 Food security

- 2026 prospects | Oil and gas industry “A New Dawn Ahead"

- Geopolitical Risks and Oil Prices Bubble Activity | Published in Energy RESEARCH LETTERS

- Crude Oil Prices: Factors Affecting the Volatility - StockBrokerReview.com

- [PDF] Capital Market Volatility During Crises: Oil Price Insights, VIX Index ...

- [PDF] The Informational Role of Commodity Futures Prices - EIA

- Oil and Methanol Price volatility

- Experts predict new exchange rate for naira in 2026 amid CBN FX reforms

- Stocks close out Q1 | E*TRADE from Morgan Stanley Monthly Market Commentary

- Oil price forecast | Brent and WTI crude oil outlook | Capital.com

- Oil prices jump as US, Iran trade fire in Strait of Hormuz

- PDF Table 1. U.S. Energy Markets Summary - U.S. Energy Information ...

- PDF EXHIBIT 6 - Department of Energy

- Geopolitical Tensions Drive Oil Price Volatility

- Oil Prices Surge 3.7% as U.S.-Iran Standoff Triggers Higher 2026 Forecasts

- Oil Price Tumbles on Strong Dollar 25-02-2026

- Oil Gains as Traders Brace for US-Iran Stress Heading to Weekend

- [PDF] UBS House View

- OPEC+ To Consider Oil Output Hike By 137,000 bpd For April

- Global oil glut defies geopolitics, drives prices down

- Insights From Kroll Economics - How Geopolitical Shifts Could Reshape Global Markets

- EIA forecasts lower oil prices in 2026 and 2027 due to persistent stock builds - U.S. Energy Information Administration (EIA)

- OPEC+ states to compensate for 659,000-807,000 bpd of excess oil production by July 2026 - Business & Economy - TASS

- Commodities Outlook 2026

- Opec+ agrees in principle to keep oil output pause for March — Reuters

- OPEC+ agrees to keep production quotas for March at December 2025 level - Business & Economy - TASS

- Hormuz Blockade Fuels Energy Shock as Brent | PriceONN Deep Look

- PDF World Official Gold Holdings

- Understanding the Impact of the Federal Reserve on Gold Investing Introduction to the Federal Reserve and Gold Investing | GoldSources.org

- PDF Dtf-04-13-26

- PDF Gold Market Q1 2026 Strategic Analysis - scireonadvisory.com

- PDF Gold Demand Trends

- gold prices over the last 10 years

- Gold (XAU/USD) Price Forecast: Gold Reclaims $5,000 as Bulls Target $6,000 Amid Strong Technical and Macro Momentum - Brave New Coin

- Gold Price Today: Live Updates

- Gold Rate per Gram in US Dollar (USD)

- Sellers' inflation, profits and conflict: why can large firms ...

- International e-Navigation Underway 2019 Conference

- Margin compression squeezes corporate earnings

- Oil and gas sector in 2026: Corporate earnings diverge

- State of Logistics Report

- PDF REPORT FOR Q1 Q3 2025/26 - voestalpine.com

- [PDF] 2026 Long-Term Capital Market Assumptions

- 4 Trends Shaping the Airline Industry in 2026

- Global Airlines Market Size, Share & Analysis Report, 2034

- Changi Aviation Summit 2026 Speech – Willie Walsh, IATA Director General : Saturday, 7th February 2026 : 4Hoteliers

- IEA members could release more oil stocks 'as and if needed': IEA chief - China.org.cn

- International Energy Agency (IEA) | Department of Energy

- US and China hold the keys to containing a Mideast oil shock: Bousso

- Kim reelected to top post of North Korea’s ruling party as it hails his nuclear buildup

- Korea 2025 - Energy Policy Review

- [PDF] Overcoming energy vulnerabilities - CESI

- [PDF] Renewables 2021 - Analysis and forecast to 2026

- [PDF] The Role of Traceability in Critical Mineral Supply Chains

- [PDF] Global EV Outlook 2019

- International Energy Agency

- May 2026 Economic and Market Update: New Highs and Old Risks - Crestwood Advisors

- PDF 2026 Outlook for Global Energy

- PDF Firmer Prices for 2025; Keeping our 2026 Forecast for Lower Prices

- PDF Oil Market Report

- PDF Clean Energy Investment in Emerging Markets and Developing Economies

- PDF 13 August 2025 - iea.blob.core.windows.net

- ISSN 2582-2292 Vol. 7, No. 02 Mar-Apr

- The $200 Oil Shock: What Happens If the Strait of Hormuz Closes

- PDF Branching Networks and Geographic Contagion of Commodity Price Shocks ...

- [PDF] The Roosevelt Project - Revitalizing America's Critical Mineral Industry

- PDF Economic and Monetary Review 2025 - investmalaysia.gov.my

- PDF Maritime chokepoints and the politics of energy security in the Indo ...

- PDF Final Update 016 - JMIC Advisory Note

- PDF Oil Markets in Focus Given Middle East Turmoil

- PDF Middle East Maritime & Port Situation Report Prepared By: 1) Purpose ...

- World Bank: Middle East, North Africa, Afghanistan & Pakistan Economic Update — April 2026

- Strait of Hormuz on edge due to Iran-Israel war? Iran’s leverage is a cautious tale for India

- PDF Strait of Hormuz 2026 - Factsheet

- Iran-US tensions: What would blocking Strait of Hormuz mean for oil, LNG? | Explainer News | Al Jazeera

- PDF Geostrategic Chokepoint: The Strait of Hormuz

- The Impact of the US–Israel–Iran Conflict on India's Trade ...

- Montel | Blog - How to Manage Price Volatility in Energy Markets

- In-depth Analysis of Urea Market Price Fluctuations: The Key to Agricultural and Industrial Costs

- PDF 2024 Annual Report - minedocs.com

- PDF Causes and Consequences of Margin Levels in Futures

- 15 Practical AI Agent Examples to Scale Your Business in 2026

- [PDF] Power Hungry: How AI Will Drive Energy Demand

- BIS Annual Economic Report 2024

- [PDF] A strategic view on the economic and inflation environment in the ...

- PDF Ethical and regulatory implications of AI in cybersecurity surveillance

- Oil shocks and portfolio hedges

- Global Market Outlook - Standard Chartered

- PDF Bloomberg US Dollar Spot Index (BBDXY) - assets.bbhub.io

- PDF Fixed Income Insights North America - January 2026

- PDF 2026_04_17_Safe_Havens - bcm.nacm.org

- Beyond Gold, What Is the Next Safe-Haven Asset Choice?

- CNBC Daily Open: The AI fear spreads — real estate, trucking and logistics are its latest victims

- PDF Q3 2022 - Invesco

- [PDF] Buy international equities - DWS

- PDF Central Bank of Sri Lanka | 8 January W U W [

- PDF Monetary policy decision-making and communication under high uncertainty

- PDF Evolving approaches to monetary policy communication in the face of ...

- PDF Central bank communication panel: the role of alternative scenarios in ...

- PDF Fed Communications and Inflation Expectations

- World Economic Outlook, April 2026; Chapter 1: Global ...

- [PDF] BIS 68th Annual report - Bank for International Settlements

- Sustaining growth and stability amid headwinds: OECD Economic Surveys: Philippines 2026

- THE EURO IN

- Federal Open Market Committee

- PDF TCRP Report 47: A Handbook for Measuring Customer Satisfaction and ...

- PDF PowerPoint Presentation

- PDF Presentation - bmss.com

- Apple Inc. (AAPL) down 0.2% in 2026 $271.06 - buy sell signal

- Global Additive Manufacturing Growth: 2026 Wohlers Report Analysis

- Semiconductor Wafer Market Size, Share & Forecast to 2036 | FMI

- MSCI World Index Forecast 2026: Global Equity Market Outlook and Expectations | Trader

- AI Pushes Global Semiconductor Market Toward US$1 Trillion

- global-investment-outlook-new-year-2026.pdf

- Q1 2026 Asset Class Outlook: Global equity

- Semiconductor Industry Growth: New Investment Opportunities in 2026

- PDF Financial Oil Market Metrics for Geopolitical Crises

- PDF EY and Institute of International Finance Bank Risk Management Survey

- PDF Geopolitical risk transmission dynamics to commodity, stock, and

- PDF Geopolitical Risks' Spillovers Across Countries and on Commodity ...

- PDF Geopolitical Risk: When it Matters; Where it Matters. Evidence from ...

- Five Scenarios for Iran and What They Would Mean for Oil Markets | OilPrice.com

- Oil Prices Fall on US-Iran De-escalation & Dollar Surge

- Bitcoin's Price Stuck? Decode Market Dynamics & ETF Impact! | Cryptodamus

- Bitcoin, Ethereum Face Uncertainty as US-Iran Tensions Threaten Market Rally

- PDF Amberdata Digital Asset Snapshot

- US-Iran Tensions: Impact on Crypto and Security

- The Direct Relationship Between Geopolitical Events and Crypto Prices

- Bitcoin Price Volatility Spikes as Geopolitical Tensions and Liquidity Crunch Shake Crypto Markets » altsignals.io

- Geopolitical Tensions Impacting Crypto Market Amid US-Iran Conflict

- Bitcoin Dips as US-Iran Talks Fail, Stokes Volatility

- Bitcoin’s Alarming 5-Month Losing Streak Intensifies Amid Israel-Iran Conflict and Economic Pressures

- [PDF] the role of geopolitical risk sin yi feng - UTAR Institutional Repository

- Q1 2026 Income and Growth Commentary

- Markets swing on Hormuz risk with oil higher, gold firmer and rate-cut bets tested

- US, Israel strike Iran: What do rising Middle East tensions mean for Indian stock markets next week? Here’s what experts say - The Times of India

- Why are global oil prices rising now and will Brent crude go from $72.48 to $80 per barrel in next jump? Global oil price rise, analysts insights and market outlook explained. Here's what should investors do now

- Iran Strikes: What’s at Stake for Oil Markets as Trump Attacks

- Geopolitical Tensions Shake Indian Equity Markets as Crude Prices Surge | Business

- Oil Climbs as Geopolitical Risk Returns | Capital.com

- Indian Markets Tumble as Oil Surge, Geopolitical Fears Trigger Broad Sell-Off

- Market crashes as fears of US-Iran clash grows, investors lose Rs 8 lakh crore

- [PDF] RENEWABLES 2023 GLOBAL STATUS REPORT - REN21

- Clean Energy Funds and Portfolio Diversification

- [PDF] European Strategic Autonomy in the Energy Field:

- [PDF][PDF] Global Renewable Energy Transition-Issues and Options

- Climate-Harming Investments Outweigh Nature Positive Investments 30 to 1

- [PDF] The Economic Case for Greening the Global Recovery through Cities

- [PDF] RENEWABLES 2025 GLOBAL STATUS REPORT - REN21

- Renewable energy

- Energy transition

- Renewable energy commercialization

- US-Israel strike Iran: Why Strait of Hormuz matters for oil prices - explained

- USS Gerald R. Ford Now in the Mediterranean Sea, More U.S. Forces Deploy to Middle East - USNI News

- A look at the military hardware the US has positioned for potential war with Iran | CNN Politics

- Strait of Hormuz Tension: Energy Security Risk Analysis

- PDF Conflict at the Crossroads: Security Tensions in the Strait of Hormuz

- PDF The Strait of Hormuz:

- PDF Geostrategic Chokepoint: The Strait of Hormuz

- US shoots down Iranian drone approaching aircraft carrier, official says

- Carrier Strike Group 12

- Carrier Strike Group 3

- Vantage Point: Q1 2026 Rates Rules Reality

- Iran Conflict Stock Market Impact: Oil Prices Plunge, S&P 500 Rally March 2026

- Fed Rate Hike 2026: Treasury Yields Surge as Inflation Heats Up

- Inflation, monetary policy expectations and market implications amid Middle East developments

- Viewpoint

- Bond duration 101: A guide for investors | iShares

- What’s The Fed’s Next Move? | J.P. Morgan Global Research

- Bitcoin Halving Cycles: Historical Impact on Price & Future Outlook – Blog – ChartMini

- Fed’s Interest Rate Decision: January 28, 2026

- Fed holds rates steady after strong capital investment from manufacturers

- Bindi Irwin opens up about endometriosis journey, reveals 50 lesions removed - Art Threat

- PDF Futures of Global AI Governance - dpo-india.com

- Gilt Yields Rise as Starmer Fights for Survival in Pivotal ‘Reset’ Speech – 42 MPs Call for Resignation - Fincrypt

- PDF Adaptive Scheduling and Coordination in Project Management

- PDF The global leader in PFA clinical research - Boston Scientific

- PDF Federal Government Cybersecurity Incident & Vulnerability Response ...