Opportunities in the Financial Sector Amid Slow Economic Growth: Strategic Insights for 2026

Navigating Challenges and Capitalizing on Innovation During Economic Headwinds

Table of Contents

Executive Summary

This analysis examines the financial sector’s strategic landscape amid persistent slow economic growth in 2026, identifying critical opportunities driven by technological innovation, advanced risk management, and emerging market dynamics. Leveraging data from recent economic and banking performance indicators, the study highlights how AI, fintech platforms, and digital assets can unlock new revenue streams and operational efficiencies crucial for navigating subdued growth conditions.

Furthermore, the report underscores the importance of integrating risk and liquidity management frameworks that transform economic headwinds into competitive advantages. Personalized financial services and targeted investments in emerging industries are spotlighted as vital growth vectors, offering financial institutions and investors strategic pathways to resilience and profitability in a challenging macroeconomic environment.

Introduction

The global financial sector in 2026 operates in a complex slow growth environment characterized by subdued GDP expansion, cautious fiscal policies, and evolving regulatory frameworks. These factors have created significant headwinds for traditional banking models, challenging institutions to reevaluate conventional approaches to growth and risk management. Understanding this economic backdrop is essential to contextualizing the strategic opportunities that emerge from persistent macroeconomic constraints.

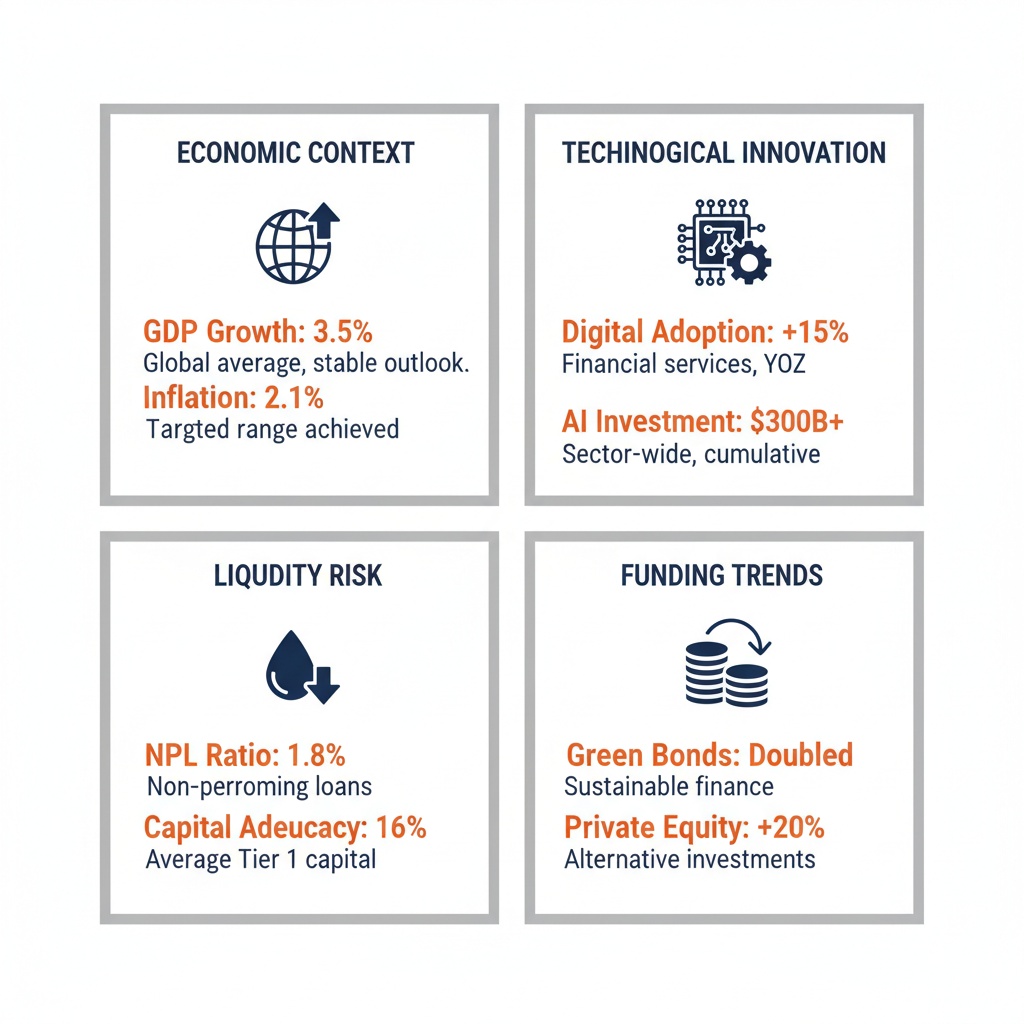

Infographic Image: Navigating Slow Growth: Key Financial Sector Insights for 2026

This analysis aims to explore the multifaceted opportunities available to financial institutions and investors despite slow growth pressures. Drawing on comprehensive data and sectoral insights, it investigates the role of technological innovations—particularly artificial intelligence and fintech ecosystems—in reshaping financial services and enhancing operational agility. It further examines advanced frameworks in risk and liquidity management that enable institutions to not only survive but thrive by converting systemic risks into strategic advantages.

Scope-wise, the report covers key economic drivers affecting finance, detailed assessments of technological disruption and fintech leadership, and strategic investment prospects in emerging sectors and personalized financial solutions. The methodology combines quantitative economic indicators, case study analysis, and risk management principles to present a holistic view of how actors within the financial sector can capitalize on innovation and adaptability in 2026’s slow growth environment.

1. Economic and Market Context of Slow Growth in Finance

In the prevailing global economic environment of 2026, financial institutions operate against a backdrop marked by sustained slow growth and heightened uncertainty. This condition, shaped by geopolitical tensions, persistent inflationary pressures, and cautious fiscal policies, imposes significant constraints on the sector’s traditional performance drivers. Nonetheless, understanding the complex interplay of these macroeconomic factors is essential to frame the strategic imperatives facing banks and financial firms. This section elucidates how subdued GDP expansion, evolving interest rate dynamics, liquidity challenges, and regulatory frameworks collectively define the economic and market context that banks must navigate — a necessary foundation preceding actionable innovation and risk management strategies.

Anchoring the analysis within this macroeconomic and regulatory context, it becomes clear that slow growth is not merely a transitory phase but a structural environment imposing new demands on financial institutions. While headlines may focus on muted economic momentum, an in-depth examination reveals differentiated impacts across banking portfolios and performance metrics, as well as emerging vulnerabilities in liquidity and credit quality. The nuanced understanding of these phenomena shapes the broader narrative of why strategic adaptation is critical and sets the stage for subsequent exploration of growth-driving tools and systemic resilience.

Economic Slow Growth Factors and Fiscal Outlook for 2026

The global economy in 2026 continues to experience a deceleration in growth rates, manifesting prominently in many developed markets where GDP gains remain below pre-pandemic trends. According to the Federal Deposit Insurance Corporation's 2026 Risk Review, U.S. real GDP expanded by only 2.2% in 2025, down from 2.8% the previous year, signaling ongoing moderation attributable to shifts in consumer spending, business investment, and trade balances. The decline in GDP growth reflects broad economic challenges that affect the financial sector [Chart: U.S. Real GDP Growth Trends (2024-2025)]. Similar patterns prevail globally, with fiscal authorities increasingly emphasizing consolidation over stimulus, reflecting a strategic pivot towards long-term resilience rather than short-term expansion.

Malaysia provides a contemporary regional case study illustrating this global trend. The nation’s 2026 fiscal policy, governed by the Thirteenth Malaysian Plan and enacted through deliberate consolidation efforts, balances deficit reduction with targeted expenditure to sustain growth. Total revenue is projected to rise modestly, driven by tax reforms and digitalization of tax administration, while expenditures are carefully reprioritized to maximize impact on infrastructure, health, and education. This prudential approach stems from the need to stabilize elevated debt levels post-pandemic and maintain fiscal sustainability, thus ensuring economic robustness amid global uncertainties. The resulting fiscal stance typifies a broader global movement from expansive deficit financing to calibrated consolidation, which inherently restrains aggregate demand and slows growth momentum.

Key structural factors underpinning this slow growth environment include persistent inflation hovering above targets, tightening labor markets with moderated employment gains, and cautious business investment. While consumer spending has remained a support pillar, uncertainty related to geopolitical frictions and supply chain adjustments continues to temper optimism. Moreover, the stabilization and modest improvement in financial market conditions—characterized by reduced corporate bond spreads and solid equity performance despite volatility—highlight the complex economic tapestry in which banking performance unfolds.

Key Banking Performance Indicators: Interest Rate Impacts and Liquidity Challenges

Within the slow growth macroeconomic framework, the banking sector performance landscape for 2025 and early 2026 mirrors a delicate balancing act. The FDIC’s 2026 Risk Review identifies a generally steady banking performance characterized by strong net income supported by both net interest income and noninterest revenues. However, loan growth remains subdued against pre-pandemic benchmarks, reflecting restrained credit demand amidst economic uncertainty. The response to interest rate dynamics is a critical performance determinant amid these conditions.

Interest rates, particularly on the short end of the yield curve, declined over 2025, reducing banks’ funding costs and partially alleviating pressure on net interest margins (NIMs). The steepness of the yield curve improved margin profiles, which is a key profitability lever. Yet, elevated unrealized losses on securities portfolios persist, posing challenges to balance sheet strengths. The decline in wholesale funding and Federal Home Loan Bank borrowings, alongside steady deposit growth—in particular from uninsured sources—illustrates shifts in funding mix that demand vigilant liquidity management.

Liquidity risk remains a prominent concern under slow growth conditions. Many institutions confront increasing difficulties in maintaining adequate liquid asset buffers without compromising profitability. According to the Interagency Policy Statement on Funding and Liquidity Risk Management, deficiencies such as insufficient liquid asset holdings, overreliance on short-term or volatile funding sources, and inadequate contingency planning continue to be material risks. The imperative for banks is to ensure resilience by sustaining diverse and high-quality liquidity positions, supported by rigorous cash flow forecasting and rapid response capabilities. These liquidity challenges are compounded by market uncertainties and changing regulatory expectations, making liquidity risk management a core focus for institutional stability.

Regulatory and Market Risk Considerations in a Slow Growth Environment

The slow growth economic context directly influences the regulatory landscape and the attendant market risk profile of financial institutions. Regulatory agencies maintain heightened vigilance on risks amplified by economic headwinds, emphasizing the necessity for robust frameworks encompassing credit, market, liquidity, and operational risks. The FDIC and other regulators demand stringent oversight of banks’ risk exposure, particularly in portfolios susceptible to deterioration during prolonged low-growth periods.

Credit risk has manifested unevenly across sectors, reflecting differing sensitivities to economic conditions. For example, commercial real estate (CRE) loan portfolios have experienced modest growth, with concentration risks and borrower stress increasing in certain regions and bank groups. Elevated operating costs, higher interest rates, and rising vacancy rates have challenged CRE debt serviceability, though widespread loan modifications have mitigated near-term losses. Similarly, agriculture and small business lending present pockets of vulnerability, as profitability pressures translate into increased delinquency rates, necessitating proactive risk mitigation strategies.

Market risks linked to interest rate fluctuations remain salient, particularly given the persistence of unrealized securities losses and changing funding profiles. Institutions must navigate the trade-offs between risk-taking and regulatory capital adequacy, compounded by intensified scrutiny of liquidity ratios and stress testing practices. Moreover, evolving regulatory expectations now extend beyond traditional risk metrics to include governance standards, contingency planning rigor, and transparency in reporting, all designed to enhance systemic resilience in a protracted slow growth climate.

Regulatory capital requirements and supervisory guidance continue to prioritize the identification and mitigation of emerging risks exacerbated by economic sluggishness. Financial institutions are expected to institutionalize comprehensive risk management frameworks that align with their complexity and business models, embedding liquidity and funding risk assessments into strategic decision-making. This regulatory emphasis underscores that slow growth is not simply a cyclical issue, but a structural challenge demanding adaptive governance and operational excellence.

2. Technological Innovation and Fintech as Growth Catalysts

In the face of persistent economic slowdowns and subdued growth trajectories that challenge traditional financial models, innovation stands out not merely as a differentiator but as a fundamental catalyst for sectoral resilience and expansion. Technological innovation and fintech are reshaping the very architecture of financial services, unlocking new revenue streams and enhancing operational efficiencies where conventional approaches offer diminishing returns. Against the backdrop of economic constraints previously outlined, this transformative wave enables financial institutions not only to adapt but to proactively pioneer growth in a landscape rife with complexity and uncertainty.

The convergence of artificial intelligence (AI), fintech entrepreneurship, and emergent digital assets signals a paradigm shift. AI-driven capabilities extend beyond automation and analytics, directly embedding intelligence into investment, customer engagement, and risk oversight. Meanwhile, fintech platforms founded by visionary entrepreneurs are disrupting legacy models, creating modular, API-driven ecosystems that prioritize inclusivity, accessibility, and speed. Together with blockchain-enabled products and digital asset innovations, these forces challenge entrenched financial paradigms and create unparalleled value propositions. Understanding these advancements offers a unique vantage into how financial firms can leverage technology as a primary lever—turning economic headwinds into propellers for sustainable growth.

AI Applications in Investment, Risk Management, and Customer Service

Artificial Intelligence (AI) has emerged as an indispensable tool in modern finance, driving sophistication across investment strategy, risk management, and client engagement. In investment, AI’s ability to process and analyze vast, multifaceted datasets facilitates predictive analytics and scenario modeling that transcend human analytical limits. Firms like Tickeron showcase AI brokerage agents employing Financial Learning Models (FLMs) that dynamically adapt to real-time market conditions across multiple timeframes, delivering superior returns—annualized gains exceeding 170% in swing trading strategies underline AI’s precision in optimizing entry and exit points. This adaptive modeling signifies a shift from static rule-based systems to continuous learning machines that can effectively navigate market volatility and emerging asset classes.

On the risk management front, AI tools automate real-time analysis of market data, credit exposures, and behavioral patterns to preemptively flag vulnerabilities and optimize portfolio resilience. Unique AI platforms integrate multiple AI agents to provide interoperable solutions that unify compliance, fraud detection, and risk signaling. This modular functionality elevates risk oversight from reactive mitigation to proactive anticipation, enabling swift, data-driven decision-making. Customer service applications also benefit substantially from AI breakthroughs; conversational AI agents streamline Know Your Customer (KYC) and Anti-Money Laundering (AML) processes by rapidly verifying identities and detecting anomalies with high accuracy and minimal latency, both reducing operational costs and improving compliance standards. Enhanced personalization capabilities powered by natural language processing refine customer interactions, creating tailored financial advice and frictionless digital experiences that boost loyalty and lower attrition.

Collectively, these AI-driven solutions not only improve operational efficiency but also open new revenue opportunities through enhanced client acquisition and retention, optimized asset management, and automated compliance. The strategic embrace of AI thus transforms what was traditionally viewed as overhead functions into scalable, revenue-generating components central to growth amid slow economic momentum.

The Role of Fintech Founders and Platforms in Disrupting Traditional Finance Models

Fintech pioneers are rewriting the rules of finance by addressing systemic inefficiencies through innovative infrastructure, customer-centric platforms, and inclusive business models. Contemporary fintech founders distinguish themselves by focusing beyond surface-level applications; instead, they develop foundational ecosystems that other fintech and traditional finance players build upon. Companies such as Plaid exemplify this infrastructure-first approach by providing APIs that bridge banking data with third-party apps, enabling a vast array of financial products to seamlessly communicate and scale. This composability accelerates innovation waves across the sector by lowering integration barriers and increasing interoperability.

Leading digital banks like Nubank emphasize financial inclusion by targeting underserved demographics through user-friendly interfaces and transparent products, thus unlocking massive new customer bases in Latin America and beyond. Similarly, Stripe’s developer-centric payment infrastructure lowers commercial friction globally, facilitating cross-border commerce and digital entrepreneurship at scale. The near $460 billion fintech market in 2026 illustrates the magnitude and maturity of these platforms in shaping global financial flows.

Moreover, fintech firms prioritize speed, simplicity, and trust—core competitive advantages that challenge legacy institutions hampered by complex systems and slower innovation cycles. Their modular ‘super app’ strategies, as seen with Revolut, bundle a broad range of financial services into cohesive ecosystems that offer payments, trading, credit access, and wealth management within one digital interface. Such approaches not only enhance user engagement but also generate diverse revenue streams and encourage data-driven insights that sharpen product offerings.

The democratizing effect of fintech founders also extends to financial empowerment initiatives. Platforms like Stack World integrate community and education into their fintech solutions, fostering greater financial literacy and tailored engagement for underrepresented groups, including women and minorities. This blending of technology and social impact builds brand equity and addresses long-standing market gaps, highlighting fintech’s evolving role as a catalyst for inclusive economic growth.

Emerging Trends in Digital Assets and Blockchain-Enabled Products

Digital assets and blockchain technologies are accelerating innovation beyond traditional financial instruments, introducing novel classes of products that challenge assumptions about asset ownership, liquidity, and transparency. Financial institutions are increasingly incorporating stablecoins, security token offerings (STOs), and digital asset ETFs into their portfolios and service frameworks, supported by organizational efforts such as the formation of dedicated digital asset task forces (as exemplified by one leading South Korean financial group’s recent initiative). This formal integration signals a maturing market poised for mainstream adoption.

Blockchain’s inherent features—decentralization, immutability, and programmable contracts—enable the development of financial products that enhance settlement speed, reduce counterparty risk, and create new avenues for fractional ownership. The rise of event-driven asset exchanges like Kalshi introduces innovative trading instruments that tie financial outcomes to real-world events, broadening market participation and hedging options.

Additionally, the digital asset ecosystem fosters transparency and auditability through distributed ledger technologies, addressing longstanding challenges in trust and regulatory compliance. By integrating AI with blockchain solutions—such as AI-enhanced security monitoring and automated compliance workflows—financial firms can realize synergistic efficiencies and improve operational risk control.

The expanding utility of digital assets as both investment vehicles and transactional mediums further incentivizes financial institutions to embed blockchain-enabled products into their strategic growth plans. This integration not only diversifies offerings but also positions institutions at the forefront of a rapidly evolving financial landscape, poised to capture emerging demand from technology-savvy consumers and institutional investors alike.

3. Risk, Liquidity, and Strategic Investment Opportunities

In an era marked by persistent economic sluggishness, financial institutions and investors face the dual challenge of safeguarding capital while pursuing growth amid constrained market dynamics. This environment magnifies the importance of a nuanced and integrated approach to risk and liquidity management that transcends traditional siloed frameworks. Rather than merely reacting to uncertainties, leading firms are embedding risk-aware capabilities into their core strategic planning processes, transforming potential threats into avenues for competitive differentiation and resilience. By bridging the insights drawn from macroeconomic realities and technological innovations, they are crafting adaptable strategies that bolster operational agility and investment precision in a low-growth milieu.

The slow growth context requires firms to pivot towards frameworks that integrate comprehensive risk management with strategic resilience, ensuring both survival and targeted expansion. Liquidity management emerges as a pivotal focus, as constrained cash flows and tighter capital markets elevate the stakes of funding adequacy and asset liquidity. Concurrently, identifying and capitalizing on emerging industries, especially those aligned with personalization and financial inclusion, opens promising fronts for strategic investment. These sectors, resilient to commoditization and increasingly driven by evolving consumer demands, offer distinct growth vectors that align with risk-calibrated capital deployment. Notably, investment opportunities in 2026 are concentrated in green finance and digital healthcare—each representing 30% of the emerging sectors share—while personalized finance accounts for a significant 25%, underscoring investor focus on tailored financial solutions and sustainable investments [Chart: Key Areas of Investment Opportunity in 2026]. Synthesizing risk controls with forward-looking investment tactics is, therefore, critical for financial actors aiming to thrive rather than merely endure within the slow growth paradigm.

Frameworks for Integrating Risk Management with Strategic Resilience

Modern risk management frameworks extend beyond traditional loss prevention to actively enable strategic resilience, which is the capacity for organizations to absorb shocks while exploiting emerging opportunities. Drawing on the Enterprise Risk Management (ERM) principles and advanced resilience models, financial institutions are adopting a holistic approach that aligns risk appetite with corporate strategy to maintain effective governance and operational continuity. This integration requires continuous risk identification, quantification, and scenario planning, supported by robust governance structures that embed risk culture throughout the organization. A leading example can be found in the application of COSO’s integrated ERM framework complemented by the 'Three Lines of Defense' model, which partitions risk ownership and oversight among operational management, risk control functions, and independent assurance providers, enhancing risk transparency and accountability.

Strategic resilience is operationalized through adaptive risk appetite frameworks that not only define acceptable risk thresholds but also guide decision-making processes under uncertainty. Quantitative techniques such as Monte Carlo simulations allow firms to model aggregated risk profiles incorporating correlations and dependencies between risk factors, enabling proactive capital allocation that balances risk and reward effectively. Furthermore, scenario planning—enhanced by AI-enabled predictive analytics—equips management with actionable insights into potential disruptions and emerging trends, facilitating contingency planning and rapid response capability. The institutionalization of continuous risk monitoring using real-time data feeds ensures that evolving risk exposures are identified promptly, enabling rapid recalibration of strategies and preserving business continuity in volatile conditions.

Crucially, this integrated approach transforms risk management from a defensive function to a value driver by informing strategic investment decisions, optimizing portfolio risk-adjusted returns, and enhancing stakeholder confidence. By embedding risk considerations into strategic planning cycles, organizations enhance their agility, maintaining alignment between long-term objectives and an ever-shifting risk landscape. This comprehensive integration not only mitigates downside impacts but also identifies upside potential within controlled risk boundaries, turning uncertainty into a catalyst for innovation and growth.

Liquidity Risk Management Tactics in Slow Growth Cycles

Liquidity risk management confronts heightened complexity in slow growth environments, where diminished economic momentum constrains cash flows and raises refinancing challenges. Firms must adeptly manage both funding liquidity—the ability to meet short-term obligations—and market liquidity—the capacity to convert assets to cash with minimal loss. Effective liquidity management hence demands multilayered tactics that combine careful cash positioning, rigorous forecasting, and optimized working capital management to safeguard solvency and operational flexibility.

Maintaining adequate cash reserves calibrated to cover at least three to six months of operating expenses serves as a foundational defense against liquidity shocks. However, static buffers alone are insufficient in today’s dynamic landscape. Liquidity planning increasingly relies on integrated, technology-driven platforms that provide real-time visibility into cash positions across global subsidiaries, currencies, and bank accounts. AI-enabled forecasting models augment traditional approaches by dynamically identifying cash flow risks and potential opportunities, allowing treasury to anticipate shortfalls and surpluses with enhanced accuracy and speed.

A diversified funding strategy is essential to mitigate concentration risk, reducing dependence on single credit sources or instruments. This includes maintaining multiple lines of credit, utilizing capital markets such as commercial paper programs, and exploring alternative financing structures under prudent risk parameters. Simultaneously, tactical management of the cash conversion cycle—including accelerating receivables, extending payables, and optimizing inventory—unlocks internal liquidity and enhances resilience without increasing external debt. Stress testing and contingency funding plans provide rigor by simulating adverse scenarios and establishing predefined response protocols, ensuring preparedness for sudden market disruptions.

Advanced liquidity risk management frameworks also emphasize continuous measurement using a suite of indicators such as current ratio, quick ratio, cash ratio, and operating cash flow ratio, supplemented by dynamic metrics like the cash conversion cycle. These metrics assist treasury and risk managers in tracking liquidity health consistently and aligning it with strategic goals. Overall, liquidity management in slow growth cycles requires a balanced combination of prudent capital buffers, technological enablement, and strategic flexibility to sustain operations while positioning for future opportunities.

Identification of Emerging Industries and Personalized Finance as Investment Opportunities

In a slow growth environment where traditional financial sectors face margin compression and saturated markets, discerning investors are turning towards emerging industries and personalized financial services as critical growth vectors. These sectors benefit from structural tailwinds such as demographic shifts, technological evolution, and rising consumer expectations for customized solutions, thus presenting unique risk-return profiles aligned with the subdued economic context.

Among emerging industries, green finance and sustainable infrastructure have gained exceptional prominence. Driven by regulatory momentum and increasing ESG-conscious capital flows, investments in renewable energy, climate adaptation technologies, and green bonds offer promising returns while aligning with global sustainability objectives. Additionally, sectors such as digital healthcare, biotech, and next-generation cybersecurity exhibit resilience to economic cyclicality owing to their essential nature and innovation-driven growth trajectories. These industries often require tailored risk assessment frameworks due to higher volatility and regulatory complexities, but advances in data analytics and scenario modeling facilitate more precise valuation and portfolio integration.

Personalized finance capitalizes on the evolving demand for bespoke financial solutions tailored to individual risk tolerance, life stage, and behavioral preferences. AI-powered wealth management platforms, micro-investment products, and tailored lending solutions exemplify this trend, targeting underpenetrated segments and enhancing financial inclusion. Investors leveraging this vector benefit from capturing recurring revenue streams and customer loyalty within fragmented markets, albeit with careful attention to data privacy and regulatory compliance risks. Furthermore, personalization extends to product innovation in insurance, retirement planning, and credit delivery, where granular risk segmentation allows for more efficient capital allocation and optimized pricing models.

Strategic investments into these opportunity zones require integrating risk-aware frameworks that balance growth aspirations with liquidity and capital preservation imperatives. Dynamic portfolio construction techniques, augmented by modern risk analytics and AI-driven insights, enable investors to navigate uncertainties while capitalizing on asymmetric upside potential. Ultimately, the confluence of emerging industry themes and personalized finance innovation shapes a distinctive frontier for risk-calibrated, strategic capital deployment in 2026 and beyond.

Conclusion

In summary, while the financial sector faces inherent challenges stemming from slow economic growth and heightened uncertainty, these conditions simultaneously catalyze transformational opportunities. Embracing AI-driven technologies, fintech platform innovations, and blockchain-enabled products allows institutions to unlock efficiencies and diversify revenue streams beyond traditional paradigms. This technological shift, paired with robust risk and liquidity management frameworks, forms the cornerstone of adaptive resilience and competitive differentiation.

Investors and financial firms are encouraged to integrate dynamic risk assessment and strategic liquidity planning with proactive identification of emerging industries and personalized finance as focal points for growth. This approach not only manages downside risks effectively but also leverages asymmetric upside potential in a subdued macroeconomic context. Looking ahead, continuous analysis of evolving market conditions and technology adoption will be crucial to sustaining agility and capturing newly arising opportunities in the financial sector’s slow growth landscape.

Future analysis should emphasize monitoring regulatory developments, the maturation of digital asset classes, and AI’s expanding role in predictive risk modeling to refine strategy execution further. Ultimately, the convergence of data-driven decision-making, innovation diffusion, and comprehensive risk governance will define how financial actors navigate and excel amid ongoing economic headwinds.

Glossary

- Artificial Intelligence (AI): Computer systems capable of performing tasks that typically require human intelligence, such as data analysis, predictive modeling, and automation, extensively applied in finance for investment strategies, risk management, and customer service.

- Enterprise Risk Management (ERM): A holistic framework used by organizations to identify, assess, and manage risks across all operational areas, aligning risk appetite with strategic objectives to enhance resilience and governance.

- Liquidity Risk: The risk that a financial institution cannot meet its short-term financial obligations due to insufficient liquid assets or difficulty in accessing funding, particularly challenging during slow economic growth.

- Net Interest Margin (NIM): A key banking performance metric representing the difference between interest income generated and interest paid out relative to the bank's earning assets, reflecting profitability from lending activities.

- Personalized Finance: Financial products and services tailored to individual customers' risk tolerances, preferences, and life circumstances, often enabled by AI and data analytics to enhance customer engagement and inclusion.

- Fintech: Financial technology companies and innovations that disrupt traditional financial services through digital platforms, APIs, blockchain, and customer-centric models to increase accessibility and efficiency.

- Monetary Policy: Central bank actions that influence interest rates and liquidity conditions in the economy to achieve macroeconomic objectives such as inflation control and economic growth.

- Regulatory Capital Requirements: Minimum amounts of capital financial institutions must hold as mandated by regulators to cover risks and ensure stability and solvency under adverse conditions.

- Stress Testing: Simulated analyses conducted by financial institutions to evaluate their ability to withstand adverse economic scenarios and shocks to assess resilience and risk exposures.

- Digital Assets: Financial assets that exist in digital form, including cryptocurrencies, stablecoins, security tokens, and blockchain-enabled products, representing a new class of investment and transactional mediums.

- Monte Carlo Simulation: A quantitative risk modeling technique that uses repeated random sampling to compute the probabilities of different outcomes in complex systems, widely used for portfolio and risk analysis.

- Three Lines of Defense Model: A risk management and governance framework dividing responsibilities among operational management, risk control functions, and independent assurance entities to enhance accountability and oversight.

- Financial Inclusion: The effort and processes aimed at making financial services accessible and affordable to all individuals, particularly underserved or marginalized populations, often driven by fintech innovations.

- Credit Risk: The possibility that borrowers may fail to meet their loan obligations, leading to losses, particularly significant in sectors sensitive to economic slowdowns such as commercial real estate and small business lending.

- Cash Conversion Cycle: A metric that measures the time taken by a firm to convert its investments in inventory and other resources into cash flows from sales, crucial for liquidity management.

References

- Key characteristics of the risk management and internal control system - Fresenius Annual Report 2024

- PDF 2026 Risk Review - FDIC

- Managing Investment Risk: Traditional vs Modern Approaches

- Liquidity Risk | Definition and Mitigation Strategies

- [산업분석] 은행/증권 - 자금운용/중개, 자본 배분의 효율성과 잠재적 건전성 리스크 점검(KB금융, 한국금융지주, 메리츠금융지주, 미래에셋증권)

- Interagency Policy Statement on Funding and Liquidity Risk Management

- 금융 AI 도구 모음: 분석·예측·리스크 관리·회계 자동화 | AiTing AI

- AI Agent Applications in Finance: KYC/AML, Investment Insights, and RFP/DDQ

- AI and the Future of Finance: Automating Investment and Risk Analysis

- 하나금융, 디지털자산·AI로 '금융 대전환 시대' 청사진 - 오늘경제

- AI Brokerage Agents: Tickeron’s Edge in Trading

- PDF Five ways to make risk a competitive advantage

- PDF Investment Risk Analytics in Asset Management - kpmg.com

- AI in finance

- PDF Investment Risk Analytics in Asset Management

- 7 Fintech Founders Quietly Reshaping the Future of Finance

- 10 Most Influential Financial Companies in 2026 Driving Global Growth

- What is cash and liquidity management? A treasury FAQ.

- PDF Fiscal Policy Overview