Malaysia’s Non-Revenue Water Status and Market Potential for Leak Detection Solutions

An Analytical Overview of NRW Reduction Efforts, Financial Commitments, and Business Opportunities in Malaysia’s Water Sector

Table of Contents

Executive Summary

This analysis provides a comprehensive assessment of Malaysia's Non-Revenue Water (NRW) situation, highlighting that despite ongoing reduction efforts, the national NRW level remains significantly elevated at approximately 34.3% as of 2024. The government has committed to reducing this figure to 28.8% by 2030, which entails multi-billion ringgit investments primarily targeting infrastructure upgrades and operational improvements. Financial frameworks, including recent budget allocations and evolving fiscal policies, demonstrate a clear governmental focus on enabling these NRW reduction initiatives.

Furthermore, this study evaluates the commercial market potential for advanced leak detection solutions within Malaysia’s water sector. Given the critical role of technology in identifying and mitigating water losses, it estimates a promising market size of RM420 million to RM630 million over the next six years, deriving from targeted public investments and technology adoption trends. These insights collectively outline the strategic alignment between Malaysia’s water loss mitigation objectives and the growth prospects for smart leak detection solution providers.

Introduction

Non-Revenue Water (NRW) poses a substantial challenge to Malaysia's water sector, materially impacting water security, revenue generation, and infrastructure sustainability. Elevated NRW levels, currently averaging around 34.3%, reflect systemic issues such as ageing pipelines, physical leakages, illegal connections, and operational inefficiencies spread unevenly across states. The urgency to address NRW is embedded within national frameworks including the National Water Policy and the Water Sector Transformation 2040 strategy, which establish clear reduction targets and performance benchmarks.

Infographic Image: Non-Revenue Water (NRW) Reduction in Malaysia: Challenges and Opportunities

The purpose of this analysis is to rigorously examine the current NRW status, government budgetary and fiscal responses, and the commercial market implications arising from Malaysia’s NRW reduction agenda. It utilizes the latest official data, financial reports, and market intelligence to provide a multifaceted understanding of technical conditions, funding realities, and technology deployment opportunities.

The scope of this document encompasses quantitative measurement of NRW levels and targets, detailed examination of fiscal commitments and policies underpinning NRW programs, and assessment of market size and revenue potential for leak detection technologies aligned with governmental strategies. Methodologically, this analysis integrates data-driven evaluation and industry validation events to ensure comprehensive coverage relevant to policymakers, investors, and technology providers.

1. Current Status and Challenges of NRW in Malaysia

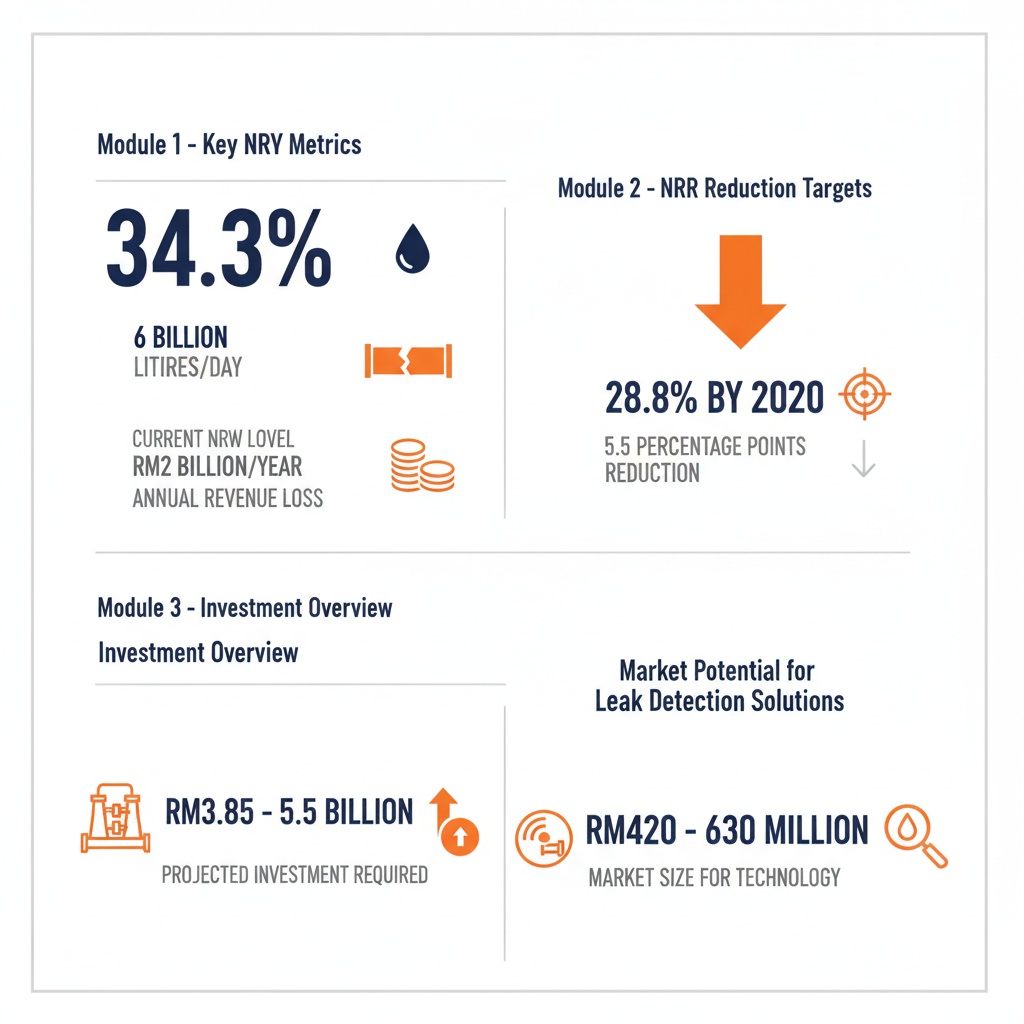

Non-Revenue Water (NRW) remains one of Malaysia’s most pressing and complex water sector challenges, deeply influencing the nation’s water security, economic efficiency, and infrastructure sustainability. Despite sustained governmental focus and substantial efforts over recent years, the national NRW level persists at a high average, estimated at approximately 34.3% by the end of 2024, marginally declined from an even more critical 37.1% level in 2023. This figure implies that over one-third of treated water fails to reach consumers as paid water services, equating to around six billion litres lost daily, and an approximate revenue loss of RM2 billion annually. Such levels underline the urgency and scale of interventions required to sustainably secure Malaysia’s water supply, aligning with the national agenda encapsulated by the National Water Policy and the Water Sector Transformation 2040 framework.

The overarching NRW challenge in Malaysia is inherently multifaceted, rooted chiefly in ageing and deteriorating infrastructure, compounded by physical leakages, commercial losses, and operational inefficiencies. These systemic vulnerabilities are further complicated by diverse socio-economic and regulatory environments across states, accentuating the need for targeted, state-specific mitigation strategies. These components, as identified, require substantial investment, with physical and commercial losses each demanding costs in the range of RM700 million to RM1 billion per percentage point reduction. Operational efficiency improvements also represent an important but variable investment area. This foundational understanding situates NRW not merely as a technical concern but as a high-cost, dynamic infrastructure problem with significant socio-economic ramifications, setting the stage for the financial and market considerations addressed in subsequent analyses.

| NRW Component | Investment Cost (RM per Percentage Point Reduction) |

|---|---|

| Physical Losses | RM700 million - RM1 billion |

| Commercial Losses | RM700 million - RM1 billion |

| Operational Efficiencies | Variable based on intervention |

Breakdown of investment costs associated with reducing Non-Revenue Water (NRW).

Quantitative NRW Levels and Official Reduction Targets

Malaysia’s current NRW level, hovering around 34.3% at the close of 2024, reflects a gradual but insufficient downward trend from preceding years when figures hovered near 37.1% in 2023. The government has officially set a national reduction target of 28.8% by 2030, representing a substantial improvement yet still significantly above global benchmarks for efficient water systems. This 5.5 percentage point reduction encapsulates an ambitious nationwide goal that demands multi-billion ringgit investments. Estimates from government sources suggest that the cost of lowering NRW by each percentage point ranges between RM700 million and RM1 billion, signifying an expected capital mobilization between RM3.85 billion and RM5.5 billion to meet the 2030 target under current cost structures. Notably, authorities acknowledge that these estimates may increase due to inflationary pressures on materials, labour, and civil works, underscoring the financial challenge ahead.

While the initial target to reduce NRW to 31% by 2025 has not been met, largely due to financial constraints among state water operators and pandemic-related project delays, these benchmarks provide critical directional guidance. The National Water Services Commission (SPAN) reports these figures consistently, while federal strategies such as the National NRW Reduction Programme initiated in 2018 outline performance-based approaches to accelerate progress. Crucially, state water operators are the primary executors, with federal oversight providing financial assistance, regulatory frameworks, and performance monitoring to incentivize reductions. The dynamic between federal ambitions and state-level implementation capacity remains a defining factor shaping NRW trajectories.

Breakdown of NRW Components: Infrastructure and Operational Challenges

NRW in Malaysia encompasses several intertwined components that collectively hamper water system efficiency. Physical losses remain the predominant factor, primarily attributed to ageing distribution infrastructure. Vast segments of Malaysia's water pipelines consist of old asbestos cement pipes, many exceeding 50 years in service life, which are prone to cracking, bursts, and leakages. The national inventory indicates approximately 38,000 kilometres of this vulnerable pipe type across the country. These physically deteriorating networks witness frequent bursts and leak points, causing substantial treated water loss before reaching end-users.

Complementing physical losses are commercial losses, which include illegal connections (water theft), inaccurate or degraded metering, and administrative errors in customer billing. These factors diminish revenue capture independent of actual physical water loss. Illegal tapping is an especially serious concern in states with higher NRW rates, necessitating enforcement and metering accuracy improvements. Meter inaccuracies due to wear and degradation result in mismeasurement of consumption, further compounding revenue losses and distorting operational data critical for system management.

Operational inefficiencies, such as uncoordinated pressure management and delayed leak detection, worsen the NRW picture. Pressure management is vital since excessive pressure accelerates pipe bursts and leakages, while insufficient pressure may reduce supply reliability. Malaysia has progressively implemented District Metering Zones (DMZs) to segment networks for better monitoring and localized leak management. Yet, the complexity and scale of Malaysia’s water networks, coupled with climatic variability—including intense rainfall, heatwaves, and flooding—pose ongoing challenges to maintaining operational stability and resilience.

State-Level NRW Reduction Efforts: Selangor and Other High-NRW States

Selangor stands as a national benchmark for NRW reduction, reflecting a rare substantive success in a challenging sector. From an NRW rate of approximately 33.2% in 2017, Selangor has managed to reduce this to around 27% by 2025 through concerted efforts led by Air Selangor. These efforts combine physical loss reduction initiatives—such as active leakage control, pressure management, and pipeline replacements—with commercial loss reduction strategies targeting illegal connections and meter accuracy enhancements. More than 1,000 kilometres of ageing pipelines have been replaced since 2016, and annual pipe replacement rates have recently doubled from 150km to 300km, with ongoing expansion planned through 2034. These infrastructure investments have contributed to an 81% reduction in pipe burst incidents between 2017 and 2024. Selangor’s experience demonstrates the positive impact of systematic, long-term investment and technological adoption.

The Selangor government allocated approximately RM800 million in 2025 for replacing 285km of pipes, which approximates a cost of RM300 million per percentage point reduction in NRW within that state. However, the cost per percentage point reduction escalates as NRW levels decline, with the state estimating up to RM400-500 million required to push NRW below 20%. These costs are driven not only by the physical pipe replacement expenses but also by the complex logistics of installation in densely populated urban areas, including road closures and community disruptions.

Conversely, other states present more severe challenges with significantly higher NRW levels. For example, 2024 data shows Perlis with an alarmingly high NRW rate of 61.5%, Kelantan at 53.7%, and Kedah at 51.1%, with more than half of treated water lost before reaching consumers in these regions. These states face greater infrastructural decay, weaker financial capacity, and operational constraints. The federal government has acknowledged these disparities and is providing matching grant incentives whereby states reducing NRW below specified thresholds can receive reimbursement commensurate with their achievements. Additionally, a dedicated monitoring task force has been established to oversee water-related projects’ execution across states, aiming to address implementation bottlenecks more effectively and coordinate efforts across various jurisdictions.

Further complicating these efforts is the financial fragility observed among water operators such as Air Selangor’s wholly-owned subsidiary, Pengurusan Air Selangor Sdn Bhd (Puas), which has experienced consecutive annual losses over the past five years despite revenue exceeding RM2.5 billion annually. This fiscal weakness constrains the ability to sustain capital-intensive NRW reduction programmes. Moreover, the current water tariff regime generally fails to enable full cost recovery as average tariffs remain below operational and capital expenditure requirements, limiting operators' reinvestment capability. Addressing the complex interplay between financial sustainability and infrastructure renewal remains critical to delivering long-term NRW reductions across all states.

2. Budgetary and Fiscal Analysis for NRW Reduction in Malaysia

Malaysia’s efforts to tackle the persistent issue of Non-Revenue Water (NRW) increasingly hinge on a robust financial framework that aligns ambitious technical targets with sustainable fiscal capacity. The transition from identifying NRW challenges to translating them into actionable investment programs necessitates comprehensive budgetary commitments and sound fiscal policies. This section elucidates Malaysia’s financial landscape surrounding NRW reduction, detailing government expenditure plans, official investment estimates, and key fiscal policy mechanisms to demonstrate the government’s capacity and approach to funding NRW mitigation. By doing so, it bridges the technical assessment of NRW issues with the real-world financial realities shaping implementation potential and strategic decision-making.

Building on the technical and infrastructure challenges outlined previously, it becomes evident that resolving NRW is as much a fiscal challenge as a technical one. The scale of investment required to overhaul ageing water distribution systems and implement advanced monitoring measures is substantial. Therefore, thorough analysis of government budgets, deficit management strategies, and financing models is essential to understand Malaysia’s preparedness and strategic prioritization in advancing NRW reduction programs. This fiscal evaluation underscores the multidimensional nature of NRW remediation, where financial sustainability intersects with infrastructure modernization goals. According to projections, Malaysia's NRW levels are expected to decline gradually from 37.1% in 2023 to 28.8% by 2030, highlighting a slow but steady improvement trajectory that underpins the financial planning for NRW investments [Chart: Trend of Non-Revenue Water Levels in Malaysia (2023 - 2030)].

Official Investment Estimates and Financial Scale of NRW Reduction

The Malaysian government’s official estimates provide a quantitative foundation for appreciating the magnitude of capital needed to achieve NRW reduction targets. Based on recent data, reducing NRW by one percentage point is estimated to require an investment ranging from RM700 million to RM1 billion, depending on the scope and nature of interventions. To meet the national target of lowering NRW from approximately 34.3% in 2024 to 28.8% by 2030, a reduction of 5.5 percentage points is necessary. This translates into a projected investment need between RM3.85 billion and RM5.5 billion over the five-year horizon. However, government sources caution that these figures might be optimistic, as rising material costs, labour expenses, and the condition of existing infrastructure could further escalate costs.

The investment requirements reflect the complexity of addressing both the symptoms and root causes of NRW. While active leakage detection and pressure management form part of the short- to medium-term strategies, the replacement of deteriorated pipes, particularly the approximately 38,000 km of ageing asbestos cement pipes nationwide, dominates capital expenditures. The Minister of Energy Transition and Water Transformation has emphasized that without systematic replacement of these core assets, efforts toward sustainable NRW reduction will be hampered by recurring leaks and bursts. The RM700 million to RM1 billion benchmark, therefore, encompasses expenditures on extensive pipe replacement, civil engineering works, and enhanced operational monitoring systems.

Furthermore, state-level implementation variations influence investment scale. For example, Selangor's experience illustrates the high costs associated even with well-managed NRW reduction programs. The state government allocated approximately RM800 million in 2025 to replace 285 km of pipes, contributing to a reduction of NRW to 27%, down from 34% in earlier years. Notably, the state projects the cost of each one percent NRW reduction to escalate to RM400 million to RM500 million as NRW levels decrease, highlighting the increasing marginal cost of improvement at lower rates of loss. This intensifying investment load at decreasing NRW thresholds informs the financial planning of both federal and state water authorities.

Recent Government Budget Data and Expenditure Allocations

Malaysia’s recent national budgets for 2024 and 2025 reveal dedicated allocations reflecting the government’s commitment to improving water infrastructure, with NRW reduction as a core priority. Although NRW reduction targets have not yet been fully met, such as the 2025 goal of 31%, which appears unlikely to be realized, the scale of allocated funding underscores the strategic importance and urgency of the issue. Budget 2025 allocated approximately RM2.52 billion toward water sector projects directly linked to NRW efforts, emphasizing pipe replacements, leak detection systems, pressure management, and network monitoring.

At the macroeconomic level, the 2025 federal budget, Malaysia’s largest to date with total spending of RM421 billion (approximately USD 98.8 billion), embeds a continuation of infrastructure investment alongside fiscal consolidation. The government intends to reduce the fiscal deficit ratio from an estimated 4.3% of GDP in 2024 to approximately 3.8% in 2025, balancing new investments with deficit management. Public expenditure growth is moderated to support these objectives, with priority sectors including smart infrastructure and utilities receiving targeted funding. The water sector’s allocations are notable within this context because they form a significant proportion of capital outlays supporting sustainability and service delivery improvements.

State-level expenditures further illuminate the financial dynamics of NRW programs. Selangor’s RM800 million pipe replacement initiative in 2025 demonstrates the capital-intensive nature of NRW reduction. However, the financial challenges of water operators remain acute, with entities such as Air Selangor and its subsidiary Pengurusan Air Selangor consistently reporting losses exceeding RM600 million annually, straining operating cash flows and capital investment capacity. These fiscal constraints limit the speed and scale of NRW programs, necessitating government fiscal support and innovative financing mechanisms.

In response, Malaysia’s government has been exploring alternative funding models, such as Private Finance Initiatives (PFI), public-private partnerships (PPP), and potential federal asset management restructuring. These models aim to mobilize private capital while maintaining affordable tariff structures, acknowledging political and social sensitivities regarding water pricing. This fiscal balancing act between investment magnitude and tariff moderation is a pivotal theme shaping budget execution and NRW project financing.

Government Fiscal Policies Impacting NRW Program Financing and Cost Recovery

Malaysia’s fiscal policies play a critical role in enabling sustainable NRW reduction by shaping water operators’ financial viability and investment capacity. A core component is the Tariff Setting Mechanism (TSM) implemented in Peninsular Malaysia and the Federal Territory of Labuan, which governs water tariffs within a regulated framework. Currently, the average water tariff is set at RM2.21 per cubic meter, whereas the total average cost of supplying treated water is RM2.43 per cubic meter, indicating a tariff-cost gap. This mismatch contributes to operating deficits, limiting revenue sufficiency to support both operational expenses and capital investments required for NRW reduction.

The TSM framework mandates periodic tariff reviews every three years, enabling gradual alignment toward full cost recovery. This approach balances financial sustainability with consumer protection, recognizing the socio-political sensitivity of tariff adjustments. The government’s policy trajectory emphasizes improving water operators’ fiscal position via revenue adequacy, which is foundational to self-sustaining NRW reduction programs.

Additional fiscal policies relate to deficit management and subsidy rationalization. Malaysia has historically maintained relatively low water tariffs compared to regional peers, and subsidies have helped moderate end-user prices. However, broad government strategies focus on subsidy rationalization and reallocation, particularly seen in energy and fuel subsidy reforms outlined in the 2025 budget. While not exclusively aimed at the water sector, these measures reflect a broader fiscal environment prioritizing efficient resource allocation and reduced blanket subsidies, indirectly supporting policies to realign water tariffs with actual service costs.

Moreover, innovative financing models are being evaluated to bridge investment gaps while protecting tariff affordability. Proposals for restructuring water supply systems—including federal takeover of assets and expanded PPP schemes—reflect growing recognition that current funding mechanisms may be insufficient or inefficient. Yet, political sensitivities and stakeholder alignment complexities remain significant barriers to rapid transformation.

Finally, the government emphasizes improved financial governance of state water operators, including performance monitoring, expenditure oversight, and alignment with national NRW reduction goals. Strengthening financial management and tariff regimes is viewed as essential to achieving NRW targets sustainably without excessive reliance on recurrent subsidies or ad-hoc budget support.

3. Market Potential and Revenue Estimation for Leak Detection Solutions

The pursuit of non-revenue water (NRW) reduction in Malaysia, underpinned by ambitious targets and substantial government investment frameworks, presents a compelling commercial opportunity for leak detection solution providers. Building upon the significant fiscal commitments elucidated in preceding analyses, this section quantifies the market potential and projects revenue outlooks for advanced leak detection technologies aligned with Malaysia’s strategic water loss mitigation agenda. As Malaysia’s water sector rapidly embraces digital transformation and sophisticated asset management, the convergence of infrastructural renewal and smart technology deployment establishes a fertile environment for innovative solutions that address system inefficiencies, enhance operational transparency, and optimize resource conservation.

Globally, the water pipeline leak detection systems market is experiencing steady growth, driven by environmental imperatives such as water scarcity, ageing infrastructure challenges, regulatory pressures, and the rising adoption of smart water management frameworks. According to recent industry reports, the global market size reached approximately USD 2.4 billion in 2023 and is forecasted to expand to USD 4.0 billion by 2032, reflecting a robust compound annual growth rate (CAGR) of 5.7%. Malaysia’s concerted efforts to reduce NRW from approximately 34.3% in 2023 to a targeted 28.8% by 2030, supported by a multi-billion Ringgit infrastructure replacement and upgrade program, position it as a microcosm of this global trend, with localized demand further stimulated by government policies, regulatory mandates, and increasing stakeholder engagement in cutting-edge leak detection technologies.

Overview of Leak Detection Technologies and Market Size

Leak detection solutions incorporate a range of advanced technologies designed to identify, locate, and monitor water losses within distribution networks. Principal methodologies include ultrasonic sensors, acoustic analysis, smart ball (inline inspection) devices, magnetic flux detection, fiber optic sensing, and non-acoustic systems. Among these, ultrasonic technology commands the largest segment globally due to its high sensitivity in detecting high-frequency leak signals even when not discernible by human hearing. Acoustic sensors remain prevalent for their real-time leak identification capability, whereas smart ball technologies provide proactive and comprehensive pipeline inspection by physically traversing the water network, detecting anomalies associated with pressure, flow, and temperature changes.

In the Malaysian context, these technologies are gaining traction through pilot deployments and scalable projects. High-profile initiatives in states like Johor and Selangor have integrated underground acoustic sensors and smart metering systems to spatially detect leaks with greater precision. Such implementations reflect Malaysia’s embracing of integrated systems that couple sensor outputs with cloud-based analytics platforms and digital twin models, enabling real-time visualization, predictive maintenance, and rapid incident response. This trend aligns with global market movements toward smart water management frameworks that emphasize interoperability, data-driven decision-making, and sustainability.

Market-wise, the Malaysian leak detection sector, while still emerging, aligns with the Asia-Pacific region’s growth trajectory, which is anticipated to outpace global CAGR due to the dual pressures of rapid urbanization and aging infrastructure replacement. Estimates based on government NRW targets, budgetary allocations, and typical expenditure patterns on leak detection components suggest that Malaysia can expect a market size in the low hundreds of millions of Ringgit within the next five years, with steady growth thereafter. This demand is supported by increased procurement of sensor hardware, data analytics platforms, system integration services, and ongoing maintenance contracts.

Revenue Estimation Modeling Based on Government Targets and Budgets

To estimate potential revenue from leak detection solutions in Malaysia, it is crucial to translate government NRW reduction commitments and infrastructure investment plans into market demand parameters. Official targets aim to reduce NRW from approximately 34.6% in 2024 to 28.8% by 2030, a reduction of roughly 5.8 percentage points over six years. Budget documents reviewed indicate that each 1% reduction in NRW roughly correlates with RM700 million to RM1 billion in investment, primarily channeled towards pipe replacement, monitoring infrastructure, and adoption of advanced leak detection and management technologies.

Assuming a conservative allocation model, approximately 10–15% of the total NRW reduction budget is directed specifically toward leak detection hardware and associated digital systems. This derives from international best practices where early detection systems and monitoring command a vital but partial share of comprehensive NRW reduction spending. Applying this ratio to Malaysia’s projected RM4.2 billion investment for NRW reduction between 2024 and 2030, leak detection solutions could represent a RM420 million to RM630 million market opportunity over this period.

Annualized, this translates to an average leak detection market size of RM70 million to RM105 million, with an expected CAGR in line with the global technology adoption growth rates of around 5-7%. The growth trajectory may accelerate as digital water infrastructure matures, enabling more cost-effective deployments, and as utilities increasingly integrate IoT-based continuous monitoring systems and AI-powered predictive analytics.

Furthermore, maintenance, calibration, and after-sales services related to leak detection equipment constitute additional revenue streams. Typically, service contracts amount to 15-20% of initial capital expenditure annually, reinforcing the market’s long-term sustainability and value beyond initial equipment sales.

Validating Market Potential through Industry Engagement and Events

The strong market potential for leak detection solutions in Malaysia is corroborated by multiple industry engagements and government-facilitated platforms. Notably, ASIAWATER 2026—Asia’s premier water and wastewater industry exhibition held in Kuala Lumpur—showcased over 1,000 companies from more than 50 countries, highlighting leak detection, NRW reduction technologies, and smart water management systems as key themes. The active participation and strategic emphasis by government agencies such as the National Water Services Commission (SPAN), the Department of Irrigation and Drainage (DID), and the Malaysia Water Association (MWA) underscore formal institutional validation of this market’s importance.

The presence of country pavilions showcasing digital metering, acoustic and ultrasonic leak detection devices, and integrated analytics platforms attracted substantial interest from municipal utilities and private investors, reflecting the rising commercial focus on such technologies. Launches of pilot projects featuring international partnerships and domestic technology trials further indicate traction in market adoption. The recurring nature of events like ASIAWATER and accompanying technical seminars promote knowledge exchange and reinforce the sector’s momentum.

Government strategic announcements during these events explicitly link NRW reduction objectives with technology investments, emphasizing innovatively designed public-private partnerships (PPPs) and new business models. These frameworks are intended to accelerate commercial deployment of leak detection services, stimulate competitive technology provider ecosystems, and enhance project viability for investors.

Collectively, these real-world activities affirm the emergent yet fast-expanding nature of Malaysia’s leak detection market, bridging policy targets to actionable business opportunities for solution providers capable of delivering integrated, scalable, and adaptive water loss management technologies.

Conclusion

Malaysia’s persistent high NRW levels represent a complex, costly infrastructure challenge that necessitates sustained and substantial financial investment alongside technological innovation. Recent government budgets and fiscal policy reforms demonstrate a strong institutional commitment to mitigating NRW through integrated capital expenditures, tariff reforms, and funding mechanisms designed to enhance water operators’ financial viability. These efforts are essential to bridging the gap between ambitious reduction targets and practical implementation constraints at both federal and state levels.

The commercial market for leak detection solutions emerges as a strategically significant sector intersecting public infrastructure goals and private enterprise innovation. Projected investment flows dedicated to NRW reduction translate into a robust and expanding market opportunity for advanced leak detection technologies, supported by increasing adoption of digital monitoring, data analytics, and IoT-enabled systems. The synergy between government programs and market dynamics positions Malaysia as a promising growth environment for stakeholders engaged in water loss management solutions.

Looking forward, continued monitoring of NRW metrics, fiscal capacity, and technology uptake is recommended to refine investment models and policy instruments. Further analysis should explore optimizing public-private collaboration frameworks, enhancing state-level operational efficiencies, and accelerating digital transformation initiatives. These steps will be critical in ensuring sustainable NRW reductions, financial stability of water service providers, and realization of environmental and economic benefits across Malaysia’s water sector.

Glossary

- Non-Revenue Water (NRW): Water that is produced and lost before it reaches paying consumers, including physical losses (leakages) and commercial losses (theft, meter inaccuracies). A core metric reflecting inefficiencies in water supply systems.

- Asbestos Cement Pipes: A type of water pipe made from asbestos fibers reinforced with cement, widely installed decades ago, now prone to ageing-related deterioration such as cracks and leaks.

- District Metering Zones (DMZs): Small, manageable segments of a water distribution network equipped with meters to monitor and control water pressure and detect leaks more effectively.

- Leak Detection Solutions: Technologies and systems used to identify, locate, and monitor leaks in water distribution networks, including ultrasonic sensors, acoustic analysis, smart balls, and fiber optic devices.

- Tariff Setting Mechanism (TSM): Regulatory framework governing water tariffs, aiming to balance full cost recovery for water supply services with consumer protection via periodic tariff reviews.

- Public-Private Partnership (PPP): A collaborative financing and operational model where public sector entities partner with private companies to deliver infrastructure projects and services.

- Private Finance Initiatives (PFI): A procurement method involving private sector investment in public infrastructure, allowing government entities to leverage private capital and expertise.

- RM (Ringgit Malaysia): The official currency of Malaysia, used as the standard monetary unit for all financial references in this context.

- National Water Services Commission (SPAN): Malaysia’s federal regulatory body responsible for overseeing water services, including monitoring NRW levels and enforcing water policies.

- Smart Ball Technology: An inline pipeline inspection device that physically travels through water pipes to detect anomalies in pressure, flow, and temperature indicative of leaks or defects.

- Revenue Loss: Financial losses incurred by water utilities due to water that is either lost physically (through leaks) or commercially (theft, billing errors), reducing income despite treated water being supplied.

- Operational Inefficiencies: Non-technical factors that decrease water system performance, such as poor pressure management, delayed leak repairs, and inadequate monitoring.

- Water Sector Transformation 2040: Malaysia’s long-term strategic framework aimed at modernizing water infrastructure, improving service quality, and reducing NRW sustainably.

- Water Tariff: The price charged per unit volume of water consumed, intended to cover operational and capital costs of water supply services.

- Asia Water (ASIAWATER): Asia’s premier water and wastewater industry exhibition, showcasing technologies, innovations, and market developments including leak detection solutions.

References

- 환경인의 대표포털 코네틱 (국가환경산업기술정보시스템)

- Ensuring sustainable water supply for over 9 million Malaysians

- National water policy aims to reduce non-revenue water, strengthen water supply, says Fadillah

- [동향세미나] 말레이시아, 재정건전화정책 본격 시동

- 세계의 수도관 누수 감지 시스템 ...

- State govt spends RM800m to tackle NRW

- Move to Plug 28.8% of Water Leakage by 2030 - Asian Water

- 카티

- PDF Measuring Historical Financial Performance - World Bank

- 말레이시아 ASIAWATER 2026 참관기

- 디지털 전환으로 성장하는 말레이시아 물산업

- The long-standing water conundrum in focus

- Malaysia may restructure water supply system to cut non-revenue water losses, full federal takeover considered sensitive — Fadillah

- 2025 말레이시아 예산안(1) - 2025년 경제 전망 및 주요 변화