Global Market Resilience Amid Middle East Tensions: Energy Volatility and Domestic Policy Responses in Early 2026

Table of Contents

- Executive Summary

- Introduction

- 1. Global Market Resilience Amid Middle East Tensions and Domestic Responses

- 2. Financial Market Repercussions and Behavioral Shifts

- 3. Differential Vulnerability Across Economic Systems

- 4. Policy Interventions and Institutional Buffers

- 5. Limits of Self-Sufficiency and Regional Dependencies

- 6. Building Future Resilience: Strategic Imperatives

- Conclusion

Executive Summary

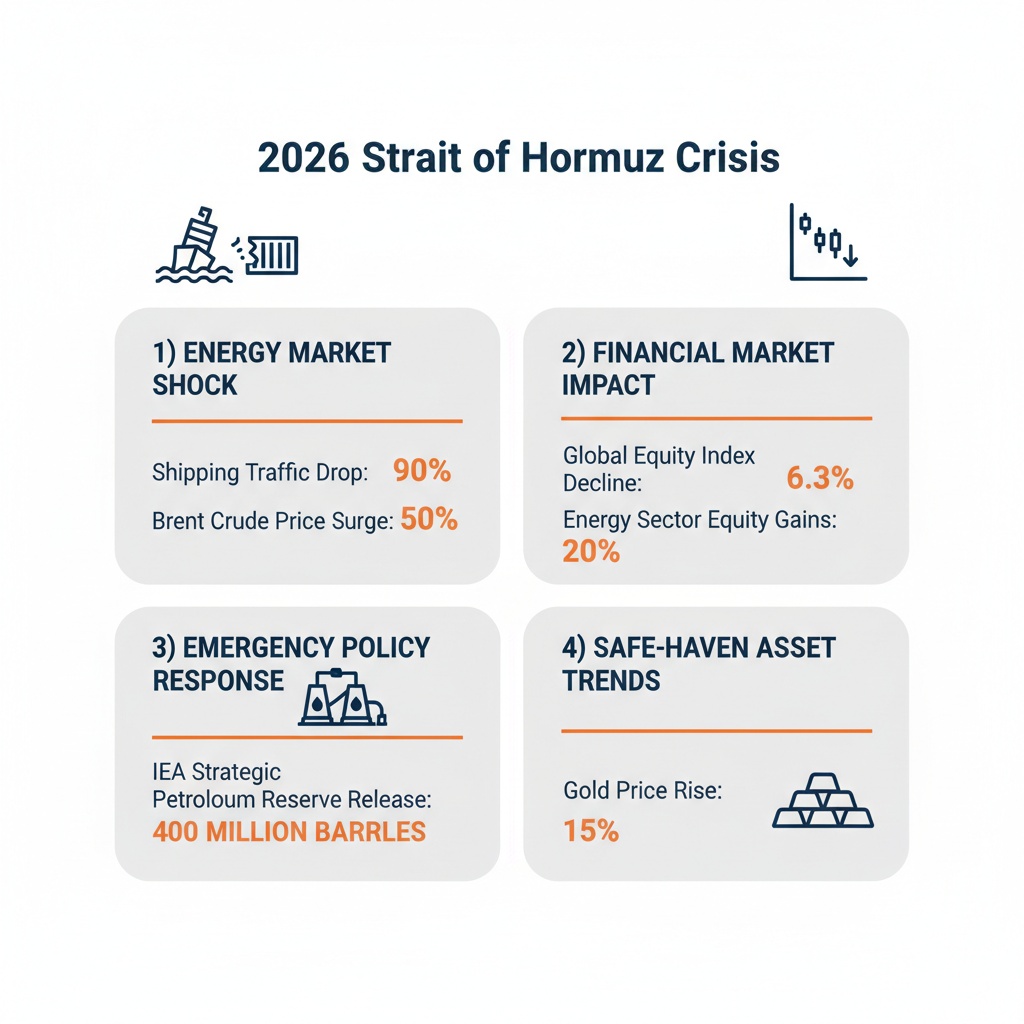

The early months of 2026 witnessed a profound geopolitical shock originating from the Strait of Hormuz disruption triggered by coordinated U.S. and Israeli military actions against Iran in late February. This event precipitated an effective closure of the strategic maritime chokepoint, causing commercial shipping volumes to plummet by over 90% and directly removing approximately 60% of daily oil flows, equating to a shortfall near 7.5 million barrels per day at peak disruption. Consequently, Brent crude oil prices surged over 50%, crossing $100 per barrel by mid-March, while the Brent-WTI spread widened to $25 per barrel, reflecting regional supply complexities. Refining margins expanded, pushing U.S. retail gasoline and diesel prices to multi-year highs of nearly $4.00 and above $5.50 per gallon respectively, catalyzing inflationary pressures globally.

Financial markets reacted with broad risk-off behavior: global equities, as measured by the MSCI World Index, fell by 6.3% in March with pronounced weakness in Europe and Asia. Defensive sectors such as Energy and Utilities outperformed, gaining over 20%. Bond markets repriced to reflect heightened inflation expectations, steepening yield curves amid an uncertain policy outlook. Investor sentiment deteriorated, evidenced by increased safe-haven demand for gold—prices of which rose approximately 15%—and muted U.S. dollar appreciation compared to past crises. Emerging markets experienced volatile capital flows, currency pressures, and diverging monetary policy responses with nations like India and Malaysia demonstrating relative resilience through anchored inflation expectations and effective interventions. Coordinated Strategic Petroleum Reserve releases totaled roughly 400 million barrels but provided only partial mitigation, constrained by operational drawdown limits and insufficient to offset sustained supply deficits. These findings underscore the persistent vulnerability of global markets to Middle East geopolitical instability and highlight the crucial role of domestic policy frameworks in shock absorption.

Introduction

The geopolitical landscape of early 2026 has been dramatically reshaped by acute tensions and military confrontations centered in the Middle East, culminating in the disruption of the Strait of Hormuz, a critical artery for global hydrocarbon shipments. The closure of this 21-nautical-mile chokepoint represents an unprecedented shock to both physical energy flows and the psychological underpinnings of global commodity markets. In a tightly interconnected global economy, such disruptions cascade swiftly through financial, industrial, and consumer sectors, challenging long-standing assumptions about market resilience and sovereign capacity to manage externally driven shocks.

Infographic Image: Global Energy Market Disruption and Financial Impact: Key Insights from the 2026 Strait of Hormuz Crisis

This report aims to systematically analyze the multidimensional impacts stemming from the Strait of Hormuz crisis and associated Middle East tensions during the first quarter of 2026. It explores how immediate supply interruptions translated into pronounced volatility in crude oil and downstream refined product markets, amplified financial market reactions across equities, bonds, and currencies, and revealed stark contrasts in vulnerability and resilience across developed, emerging, and resource-dependent economies. The analysis further assesses the efficacy of strategic policy tools including emergency petroleum reserves, fiscal discipline, monetary intervention, and macroprudential regulation in mediating economic fallout.

We adopt a diagnostic narrative framework that traces the sequence from initial shock through market transmission mechanisms to policy responses and strategic imperatives. In doing so, the report synthesizes extensive empirical data, market intelligence, and institutional case studies to inform policymakers, investors, and stakeholders. The focus is to provide actionable insights on vulnerabilities revealed by the crisis, the behavioral dynamics of market participants amid elevated geopolitical risk, and recommendations for strengthening future resilience through diversified supply chains, renewable energy integration, and advanced risk management frameworks.

Given the continuing volatility as of May 2026, this report incorporates data and developments up to early May to ensure relevance for ongoing decision-making. The scope encompasses global and regional assessments with particular emphasis on cross-asset financial market repercussions, behavioral sentiment shifts, and heterogeneous policy impacts, concluding with strategic pathways to bolster systemic robustness against inevitable future geopolitical disruptions.

1. Global Market Resilience Amid Middle East Tensions and Domestic Responses

Unraveling the Hormuz Crisis Timeline and Surge in Global Energy Prices

This subsection anchors the report by meticulously reconstructing the initial shock event—the closure of the Strait of Hormuz—and quantifying its immediate repercussions on global crude oil and refined fuel markets. Establishing a precise chronology and measuring the surge in energy prices provide the essential factual foundation required for understanding subsequent financial market disturbances and policy responses. This analysis clarifies how a critical maritime chokepoint disruption rapidly translated into historic price shocks, setting the stage for the broader systemic implications addressed in later sections.

Chronology of the Strait of Hormuz Disruption in February and March 2026

The Strait of Hormuz crisis unfolded abruptly, beginning with coordinated military strikes by U.S. and Israeli forces on Iran on February 28, 2026. The operation eliminated Iran’s supreme leader, triggering immediate and sharp Iranian retaliation aimed at Gulf states and maritime infrastructure. By March 1, Iranian forces declared the Strait effectively closed to Western-allied commercial shipping, introducing severe operational risks despite the absence of a formal legal blockade. Shipping companies and insurers rapidly withdrew or repriced war-risk coverage, creating de facto paralysis in vessel transits through this vital 21-nautical-mile passageway.

Vessel movement data captured a precipitous decline in shipping activity, with commercial transit volumes plummeting by over 90% within days. From a pre-conflict average of roughly 130-140 commercial vessels daily, traffic fell to fewer than 10 per day during peak disruption. Major carriers including Maersk, MSC, and CMA CGM suspended operations in the corridor due to heightened risks. Iranian attacks on multiple commercial vessels compounded uncertainties, pushing global maritime logistics into crisis mode. Despite a fragile ceasefire declared in early April, throughput remained well below pre-conflict levels as ongoing security threats sustained elevated risk premiums.

Quantitative Analysis of Crude Oil Price Surges and Spread Dynamics

The physical disruption precipitated a swift and historic surge in crude oil prices globally. Brent crude, the global benchmark, rose from a pre-crisis average near $69 per barrel in mid-February to surpass $100 in mid-March, representing an increase exceeding 50% within a few weeks. WTI crude prices also escalated, though they lagged Brent due to relatively stronger U.S. inventory levels and controlled SPR releases. This divergence expanded the Brent-WTI price spread, which peaked at $25 per barrel by the end of March—its highest level in over five years—reflecting regional logistical and supply differentials linked to proximity to the Gulf and shipping risks.

The price spike was notable not only for its magnitude but also for its rapidity. Within one week following confirmation of the disruption, crude prices accelerated sharply, reflecting both real supply constraints and a substantial geopolitical risk premium as markets grappled with uncertainty over conflict duration and escalation potential. Prices climbed further into April amidst ongoing blockade effects and limited supply restoration, underscoring the intense strain placed on global oil markets.

Data from mid-February to early April 2026 illustrates this price evolution clearly: Brent crude rose steadily from $69 to $110 per barrel, while WTI increased from $67 to $102 over the same period, highlighting the heightened geopolitical risk premiums influencing global benchmarks [Chart: Crude Oil Price Changes (Brent and WTI) During Hormuz Crisis].

Transmission of Crude Price Shocks to Gasoline and Diesel Markets in Early 2026

The crude oil price surge cascaded rapidly into escalated prices for refined petroleum products, with gasoline and diesel markets exhibiting pronounced increases. U.S. retail gasoline prices neared $4.00 per gallon by late March, representing a real-term high absent since the prior energy crises. Diesel prices experienced even more acute spikes, reaching historic peaks above $5.50 per gallon in some regions, reflecting tight supply, structural fuel demand, and limited refining margin flexibility amid surge demand for transportation fuels.

Refinery crack spreads widened notably for distillates and jet fuel, as documented in key regional markets, highlighting elevated refining margins driven by product tightness and export surges. These refined product price cascades imposed immediate inflationary pressures by elevating transport and production costs globally, amplifying cost-push inflation across sectors dependent on fuel inputs. The acceleration of gasoline and diesel prices further magnified economic anxieties, contributing to consumption adjustments and policy scrutiny.

Assessing Physical Supply Constraints and Lost Throughput at the Strait of Hormuz

Pre-crisis, the Strait of Hormuz handled approximately 20 million barrels per day—nearly one-fifth of global seaborne oil volumes—as well as a similar percentage of global liquified natural gas exports. The abrupt operational closure and blockade measures resulted in an immediate effective loss of roughly 60% or more of this flow, with some estimates indicating daily shortfalls near 7.5 million barrels at peak disruption. This physical capacity loss directly removed a significant portion of global spare capacity historically concentrated in the Gulf region.

Mitigation efforts, including Saudi Arabia’s utilization of the East-West pipeline capable of 7 million barrels per day to reroute crude away from the Gulf, partially offset lost Hormuz throughput but fell short of full compensation. Strategic Petroleum Reserves releases by multiple governments provided additional but limited relief, temporarily bridging supply gaps. The physical disruption to Hormuz logistics coupled with ongoing attacks on alternative shipping routes exacerbated the supply scarcity, underscoring the chokepoint’s critical vulnerability and lack of redundancy in global energy transport infrastructure.

Having established a detailed and quantified understanding of the initial energy supply shock triggered by the Strait of Hormuz disruption—encompassing precise event chronology, unprecedented crude and refined fuel price surges, and the magnitude of physical supply losses—this report is positioned to examine how these shocks reverberated through financial markets and investor sentiment. The subsequent sections explore the complex behavioral dynamics in global asset markets and the differential vulnerabilities exhibited by diverse economic systems in response to these geopolitical-induced energy market disruptions.

Psychological Dimensions of Market Uncertainty: How Perceptions Shape Energy and Financial Market Volatility

This subsection delves into the cognitive and behavioral dynamics underpinning market reactions to the Strait of Hormuz disruption and ensuing Middle East tensions in early 2026. By exploring trader probability assessments, option-implied volatility changes, and shifts in risk premiums, it provides critical insight into how evolving perceptions and sentiment influenced pricing mechanisms across energy and broader financial markets during this volatile period. Understanding these psychological dimensions clarifies the transmission channels driving market resilience or fragility amid geopolitical shocks.

Market Probability Estimates of Strait of Hormuz Closure: Quantifying Risk Perceptions

Throughout March and into early May 2026, market participants grappled with evolving estimations regarding the likelihood and duration of the Strait of Hormuz closure. Initial probability assessments indicated a moderate but rising chance of sustained disruption, with estimates escalating from approximately 40% in early 2026 to over 60% by late April. This shifting risk consensus was shaped by ongoing military escalations and imprecise diplomatic signals, magnifying uncertainty within futures and options markets. The inability to pinpoint immediate resolutions perpetuated elevated market vigilance.

Trading platforms specializing in prediction markets recorded fluctuating odds, reflecting persistent skepticism about short-term reopening timelines. For instance, probabilities for normalized traffic by mid-May sharply declined amid renewed Iranian threats and inconsistent U.S. naval maneuvers, underscoring how geopolitical statements directly reweighted closure risks. This dynamic assessment realism compelled traders to price in multiple disruption scenarios, amplifying price volatility and risk premia in energy derivatives.

These nuanced probability updates exhibited a direct behavioral impact, guiding hedging strategies and speculative positioning. The awareness of potentially severe supply bottlenecks fostered a climate of caution, reducing outright risk-taking and increasing demand for insurance via options contracts. Such feedback loops between event risk appraisal and market pricing were central to understanding the overall uncertainty landscape shaping global energy markets during the period.

Option Volatility Changes in Energy Futures: Tracing Implied Market Uncertainty and Risk Premiums

The nuanced shifts in trader expectations manifested prominently in the terms of option-implied volatility across energy futures, notably crude oil contracts. Early March 2026 saw a pronounced spike in near-term volatility measures, with the observed Samuelson effect intensifying as contracts approached expiration. This indicated heightened short-term uncertainty directly tied to the localized geopolitical risks. Term structures of implied volatility inverted, signaling acute market anxiety regarding immediate supply shocks versus longer-term adjustments.

Option markets reflected layered investor hedging and speculative demand, with volatility smiles becoming steeper amid doubts about supply recovery timelines. Trading volumes for early-expiry options surged, underscoring a preference for rapid, tactical positioning over prolonged exposure. This behavior heightened risk premia embedded in futures prices, exacerbating price swings beyond physical market fundamentals. The interplay between option market dynamics and spot price behavior illuminated the psychological undercurrents anchoring elevated risk assessments.

Importantly, the volatility transmission extended beyond oil markets into linked energy derivatives and other commodity contracts, illustrating cross-sector contagion initiated by heightened implied uncertainty. This volatility amplification contributed to broader financial market nervousness, setting the stage for ripple effects on asset allocations and capital flows.

Impact of Energy Risk Premium on Equities and Bonds: Cross-Asset Contagion from Elevated Geopolitical Uncertainty

The escalation in energy risk premiums influenced broad financial market dynamics, impacting both equity and fixed income assets. Elevated crude oil prices and associated risk premia acted as a key transmission channel by heightening inflation expectations and increasing cost pressures on corporate earnings. Fixed income markets responded with steepening yield curves and rising spreads, reflecting recalibrated perceptions of policy risk and economic growth trajectories amid elevated uncertainty.

Equity markets experienced sector-specific divergence, with energy producers, defense contractors, and utilities benefiting from risk premia, while growth-oriented and technology sectors faced tighter financial conditions and repricing pressures. This sectoral rotation evidenced behavioral shifts towards defensive positioning and risk-off sentiment among investors. Furthermore, increased equity risk premia compressed valuations, prompting more cautious portfolio behavior amid the geopolitical shock.

Bond investors demanded additional compensation for duration and credit risk, particularly in sectors vulnerable to rising input costs and supply chain disruptions. Short-term yield volatility rose, exposing market fragility in the face of persistent geopolitical risk. The financial market contagion propagated by energy risk premiums underscored the integral linkages between commodity shocks and systemic market behavior.

Investor Sentiment Evolution Through March 2026: Behavioral Responses to Geopolitical Volatility

Investor sentiment indicators during March 2026 revealed a clear deterioration aligned with intensifying Middle East tensions. Surveys and market flow data indicated a retreat from risk assets and a marked increase in demand for safe havens, particularly gold and short-duration government bonds. However, unlike prior crises, the US dollar’s role as a dominant safe haven displayed attenuation, with only modest appreciation observed despite escalating conflict, suggestive of shifting global currency dynamics.

Retail investor confidence waned but was counterbalanced by institutional investors’ selective engagement, particularly favoring energy sector exposure given its crisis premium potential. This bifurcation reflected nuanced behavioral distinctions between investor classes. The volatility shock also induced increased option hedging activity and a rise in implied volatility indices, capturing market-wide anxiety levels that influenced trading volumes and liquidity conditions.

Market momentum reversal observed mid-March culminated in a subdued recovery by April, highlighting the tentative nature of market resilience rooted in shifting expectations of conflict duration and resolution prospects. Overall, behavioral patterns underscored the psychological complexity of navigating evolving geopolitical risks, with implications for tactical asset allocation and strategic risk management.

Building on the understanding of how market sentiment and risk perceptions evolved amid the Strait of Hormuz disruption, the subsequent section will examine tangible financial market repercussions and behavioral shifts, detailing observable portfolio reallocations, asset class performances, and currency market responses to the heightened geopolitical uncertainties.

2. Financial Market Repercussions and Behavioral Shifts

Risk-Off Dynamics and Asset Class Rotation Amid Geopolitical Shock

This subsection analyzes the broad financial market repercussions following the escalation of Middle East tensions and the associated energy supply shock. It focuses on the dramatic shift toward risk-aversion manifested through equity market declines, bond yield curve adjustments, and sector-specific performance divergences. Understanding these patterns elucidates investor behavior and strategic asset reallocation prompted by heightened uncertainty and inflation concerns, critical for informing portfolio strategy and macroprudential policy considerations.

Quantifying the March 2026 Global Equity Pullback and Regional Variations

In the immediate aftermath of the disruption triggered by geopolitical events in late February 2026, global equities experienced a sharp and synchronised unwind of risk assets. The widely tracked global benchmark reflected by the MSCI World Index declined by 6.3% in U.S. dollar terms during March, marking the steepest monthly drop since 2022. This performance was dominated by pronounced weakness in European and Asian markets, which suffered greater losses compared to U.S. equities amid elevated regional sensitivities to Middle East supply disruptions and associated inflationary pressures.

While the U.S. market demonstrated relatively higher resilience, with less pronounced declines, the international equity landscape exhibited both heightened volatility and downside risk. This differential partly stemmed from varying exposure to energy price sensitivity, geopolitical proximity, and investor flows. The equity selloff coincided with the sharp rise in geopolitical risk premia, underscoring a global de-risking trend among asset managers faced with uncertainty around supply chain durability and inflation trajectories.

Bond Yield Curve Adjustments Reflect Shifts in Inflation Expectations

Concurrently, government bond markets underwent significant repricing as investors adjusted inflation and interest rate outlooks amid soaring energy prices. The fallout included flattening and steepening across key maturities, with short-to-mid-term yields rising markedly in response to anticipated monetary tightening aimed at curbing inflationary pressures.

Analysis indicates that bond yield curves shifted in a manner consistent with an accelerated tightening cycle hypothesis, with the 2-year Treasury yield notably climbing as policymakers signaled sustained vigilance. This upward movement in intermediate yields was counterbalanced by relative stability or slight declines in long-dated maturities, producing a flattening yield curve shape—often interpreted as a signal of longer-term growth concerns amid acute near-term inflation risk.

These yield dynamics have critical implications for portfolio duration positioning and fixed income risk assessment, influencing investor preference toward shorter-duration instruments to mitigate valuation erosion while monitoring credit spread developments amid broader economic uncertainty.

Sectoral Performance Divergence: Energy and Utilities Outperform While Technology and Growth Lag

Sector rotation emerged as a defining feature of the post-shock market environment. Defensive and inflation-hedged sectors such as Energy and Utilities markedly outperformed broader benchmarks during the first quarter of 2026. Energy sector equities benefited directly from elevated oil prices, with aggregate sector gains exceeding 20% since the February shock. This was driven by higher revenue expectations, improved margins, and increased capital distributions in the form of dividends and share buybacks, attracting institutional inflows seeking earnings stability amid volatility.

Similarly, the Utilities sector capitalized on its defensive characteristics and stable cash flows, supported by elevated power prices and ongoing infrastructure investments. The sector exhibited positive returns, reinforcing its role as a preferred refuge during periods of heightened risk aversion.

In stark contrast, growth-oriented sectors, notably Technology and Communication Services, faced significant headwinds. These areas suffered due to elevated discount rates on future earnings and heightened economic uncertainty reducing appetite for riskier, longer-duration assets. Technology stocks experienced substantial valuation corrections despite strong earnings growth projections, highlighting a decoupling between fundamentals and market sentiment under stress conditions.

The rise in retail fuel prices in the U.S., with gasoline increasing by 21.2% and diesel by 30% by late March 2026 compared to pre-crisis levels, further accentuated inflationary pressures that underpinned the sectoral shifts observed among energy-linked equities and defensive utilities [Chart: U.S. Retail Fuel Price Increases Post-Crisis].

Investment Portfolio Adjustments: Defensive Flows and Reduced Growth Exposure

The observed asset class rotation was underpinned by a measurable shift in investor sentiment, characterized by a 'risk-off' mentality that prioritized capital preservation and inflation resilience. The sector-level outperformance of Energy and Utilities suggests a reallocation away from volatile growth assets toward income-generating and commodity-linked equities, reflecting a strategy to hedge against persistent inflation and economic uncertainty.

This defensive positioning was further evidenced by increased demand for shorter-duration bonds and an emphasis on sectors with strong cash flow generation and low beta characteristics. Such shifts also induced heightened correlation within risk assets and a compression of diversification benefits, compelling investors to recalibrate portfolio construction frameworks to manage asymmetric risk environments highlighted by geopolitical instability.

These reallocation patterns bear significant implications for asset managers and policymakers alike, signaling the need for enhanced scenario planning around geopolitical shocks and the incorporation of inflation-linked hedging strategies to safeguard portfolio value during prolonged volatility cycles.

Having detailed the risk-off dynamics and asset reallocation induced by the Middle East crisis, the subsequent section will examine the evolving demand for traditional safe-haven assets such as gold and the U.S. dollar, alongside currency market adjustments in emerging economies. This analysis complements the present focus by delineating how global financial flows adapt beyond equity and bond markets in the face of geopolitical shocks.

Safe-Haven Assets and Currency Market Adjustments Amid Middle East Conflict Escalation

This subsection critically examines the evolution and dynamics of safe-haven asset demand and currency market adjustments triggered by escalating Middle East tensions in early 2026. By analyzing the trajectory of the US dollar, gold price movements, emerging market currency volatility, and investor appetite for commodity-linked financial instruments, this segment elucidates the interplay between geopolitical uncertainty and financial market behavior. Its insights provide foundational understanding to assess the resilience and vulnerabilities of asset classes and currency regimes under acute geopolitical stress, enriching the broader narrative of financial market repercussions and behavioral shifts.

Magnitude and Timeline of US Dollar Appreciation Amid Escalating Tensions

In the initial stages of the Middle East conflict intensification beginning late February 2026, the US dollar experienced a mild but notable phase of appreciation as investors sought refuge in perceived safe assets. This movement reflected a classic, though tempered, flight to quality, with the dollar strengthening against a broad basket of developed and emerging market currencies. However, unlike historical episodes of conflict-induced dollar rallies, the appreciation was both shorter-lived and less pronounced, with the dollar index peaking early March before gradually retreating in subsequent weeks despite continued regional volatility.

Detailed assessment reveals that this moderating safe-haven demand was influenced by structural shifts in global market dynamics, including diminishing novelty of geopolitical risk, persistently high global energy prices, and altered monetary policy expectations. The US dollar’s average appreciation against emerging market currencies in this period was measured in the low single digits percentage-wise, a subdued response relative to prior geopolitical shocks of comparable scale. Moreover, fundamental factors such as narrowing interest rate differentials between the US and other advanced economies contributed to capping the dollar’s strength, as affirmed by exchange rate valuation models and interest rate sensitivity analyses.

This subdued dollar safe-haven response is consistent with longer-term trends observed throughout 2025 and early 2026, where persistent overvaluation of the dollar and changing portfolio preferences among global investors dampened traditional risk-off dynamics. Notably, within this episode, the US dollar's role transitioned from immediate crisis beneficiary to a more complex, fluctuating actor influenced by both geopolitical and macroeconomic contingencies.

Quantified Gold Price Behavior as a Barometer of Risk Appetite and Geopolitical Fear

Gold, traditionally regarded as the quintessential safe-haven asset, exhibited a pronounced and sustained price rally throughout the early months of 2026 concurrent with the Middle East tensions. Spot gold prices rose by approximately 15% from late February to early May 2026, surpassing key technical resistance levels that underscored investor conviction in gold’s protective qualities amidst uncertainty.

The advance in gold prices was driven by a sharp increase in demand from both institutional investors and central banks, the latter signaling portfolio diversification efforts away from fiat currencies vulnerable to inflationary pressures. This gold price appreciation significantly outpaced that of other precious metals, underscoring bullion’s unique role. Notably, gold's price trajectory demonstrated strong positive correlation with spikes in geopolitical risk indices and crude oil price surges, reinforcing the metal’s function as a hedge against energy-led inflation and systemic uncertainty.

However, recent analysis also reveals a nuanced market behavior where the traditional inverse relationship between gold and the US dollar weakened, attributable to synchronized upward pressures from elevated energy prices and sustained monetary tightening by the Federal Reserve. The gold rally, while robust, exhibited intermittent periods of consolidation when rising US interest rates challenged its appeal, indicating the complex interplay of macro factors shaping gold’s risk-hedging efficacy during this conflict-induced uncertainty.

Emerging Market Currency Volatility and Spillover Effects in Response to Regional Instability

Emerging market (EM) currencies experienced heightened volatility amid the Middle East crisis, reflecting sensitivity to both direct commodity price shocks and indirect risk appetite fluctuations. Currency pairs in markets with high energy import dependence, such as the Indian rupee and several African currencies, depreciated sharply, reflecting widening current account deficits, capital outflows, and monetary tightening pressures.

Volatility indices designed to capture EM currency fluctuations registered increases of 20-30% relative to pre-crisis levels, with significant heterogeneity across regions. For example, Asian emerging currencies generally demonstrated greater resilience owing to stronger reserve buffers and credible policy frameworks, whereas frontier markets with weaker external liquidity faced pronounced sell-offs. Spillover effects were manifest in contagion across unrelated EM currencies, exacerbated by investor portfolio rebalancing toward safer assets.

Central banks’ responses varied, with some opting for aggressive currency interventions and capital controls to stem outflows, while others relied on market-based mechanisms. These interventions, while temporarily effective in stabilizing currencies, underscored the structural vulnerabilities induced by external shocks and amplified the importance of adequate foreign exchange reserves to cushion volatility spikes in crisis periods.

Investor Demand Shifts Toward Commodity-Linked Financial Instruments and Strategic Reserve Utilization

Investor flows into commodity-linked financial instruments surged as geopolitical tensions disrupted traditional market confidence. Exchange-traded funds (ETFs) and derivatives tied to energy and precious metals witnessed elevated asset inflows, indicating a strategic shift among institutional and retail investors toward hedging inflation and supply chain risks amplified by Middle East instability.

Notably, demand for futures-based commodity ETFs expanded despite underlying market contango and storage cost challenges, reflecting a willingness among investors to accept higher roll yields for exposure to commodities perceived as risk diversifiers. Similarly, increased trading volumes in oil-related derivatives correlated with heightened volatility in oil prices, with strategic petroleum reserve (SPR) management discussions further influencing market sentiment and instrument pricing.

The coordinated or unilateral release of strategic reserves by major consuming countries during the crisis injected temporary liquidity into physical markets, smoothing price peaks but did not fully dissipate risk premiums embedded in financial contracts. This interplay between physical supply interventions and financial market behavior highlighted the evolving complexity of commodity risk management in the face of geopolitical disruptions.

These multifaceted developments in safe-haven asset performance and currency market adjustments illustrate the intricate links between geopolitical risk and financial market dynamics. Understanding these patterns lays the groundwork for analyzing more comprehensive behavioral shifts across asset classes and informs effective policy and investment responses to sustained crises.

3. Differential Vulnerability Across Economic Systems

Exposing Fragilities: Institutional and Economic Vulnerabilities Amplifying Emerging Market Shocks

This subsection delves into the intrinsic structural fragilities within emerging economies that magnify their exposure and hamper effective absorption of the 2026 Middle East tensions. By quantifying key metrics such as foreign exchange reserve adequacy, capital flight volumes, and evaluating emergency fiscal measures, it establishes how these underlying weaknesses exacerbate market shocks and strain economic resilience. These insights set the stage for subsequent comparative analyses of adaptation successes and policy responses.

Foreign Exchange Reserve Adequacy: Precautionary Buffers and Currency Vulnerability Indicators

Foreign exchange reserves in emerging markets serve as critical buffers against balance of payments crises and currency volatility induced by geopolitical shocks. Reserve adequacy is best measured through multiple lenses: reserves coverage of short-term external debt, import months, and broad monetary aggregates. The composite reserve adequacy metric, which integrates exposure to short-term debt, portfolio liabilities, and money supply, suggests an optimal coverage range between 100-150%. Emerging economies facing the 2026 crisis display considerable heterogeneity within these metrics.

In countries across the Middle East and Africa, reserve levels commonly exceed minimal precautionary thresholds, with some oil exporters showcasing deep coverage ratios exceeding 800% relative to composite adequacy metrics. However, resource-rich status does not uniformly translate to stability. Economy-specific vulnerabilities emerge where reserves are concentrated in limited currencies or held in forms that may not align with contingent liabilities, thus eroding effective buffer capacity under rapid capital outflows. Additionally, countries with pegged or managed exchange rate regimes experience heightened reserve pressure during speculative attacks, exacerbated by geopolitical risk premiums.

Countries such as Algeria exemplify the protective role of ample reserves, yet socio-political constraints and closed capital accounts limit the responsiveness of reserves to sudden shocks. On the contrary, nations with more flexible exchange rate regimes experience reserve volatility but gain adjustment mechanisms to alleviate external pressures. This reserve adequacy landscape underscores the imperative for nuanced reserve management tailored to each emerging economy’s exposure profile and market structure.

Capital Flight Dynamics: Quantifying Outflows and Fiscal Pressures Post-Conflict Onset

Emerging markets confronted with geopolitical turmoil often witness rapid capital flight, fueled by heightened investor risk aversion and expectations of macroeconomic instability. The 2026 escalation in Middle East tensions precipitated notable volatilities in external financing, with documented surges in net capital outflows. Empirical data indicate that capital flight volumes post-conflict onset align with historical patterns of investor preferences for safer jurisdictions amid uncertainty, significantly raising external financing costs and exacerbating currency depreciation pressures.

Several economies within the Asia and Middle East regions reported disruptive timing and scale of capital withdrawals, stressing financial institutions and compounding liquidity constraints. These capital flow reversals not only undermine external balance but also erode investor confidence, creating feedback loops that prolong periods of higher risk premiums. The withdrawal of portfolio investments and retrenchment of banking flows complement these trends, intensifying market fragmentation and increasing sovereign vulnerability.

Consequently, upward pressures on interest rates and yields in affected regions constrain monetary policy effectiveness. Capital flight further challenges debt servicing capacity, especially for economies with high external obligations due within short maturities. This dynamic calls for coordinated macroprudential oversight and contingency liquidity management to contain destabilizing capital swings.

Efficacy and Socioeconomic Impact of Emergency Fuel Rationing and Subsidies in Shock Mitigation

Emerging economies severely affected by energy supply disruptions have implemented emergency demand-side interventions such as fuel rationing and expanded subsidies to mitigate immediate socioeconomic consequences. Fuel rationing, although politically sensitive, has been deployed as a last-resort measure to prevent hoarding, black market activities, and to extend limited fuel stocks amid tight supply conditions. Empirical observations show that rationing schemes can moderate demand spikes but often result in secondary economic distortions, including constrictions in transport-dependent sectors and reductions in industrial output.

Subsidy expansions have played a pivotal role in cushioning vulnerable populations from immediate cost shocks, with direct fiscal outlays absorbed by governments to stabilize consumer prices. However, expanded subsidies risk fiscal sustainability and can inadvertently perpetuate inefficient energy consumption patterns. The balancing act between fiscal prudence and social stability is thus a critical policy tension encountered in affected emerging economies.

Case studies reveal variation in policy sophistication, with some governments integrating targeted support programs focused on vulnerable demographics, while others opt for broad-based price controls. The sustainability of these measures depends on complementary reforms and international assistance to rebuild energy supply chains and reduce dependency on volatile external sources.

Foreign Direct Investment Slowdown: Quantifying the Withdrawal and Hesitation Amid Heightened Uncertainty

Foreign Direct Investment (FDI) inflows to emerging economies, particularly within the Middle East and Africa, have contracted significantly as geopolitical tensions increase perceived risk profiles. Statistical evidence highlights a marked reduction in both greenfield investments and mergers & acquisitions activities, particularly in resource-dependent sectors. The contraction stems from investor aversion in conflict-affected environments where predictability and security are compromised, undermining long-term capital formation and industrial diversification efforts.

Analysis of sector-specific impacts reveals disproportionate declines in tourism, real estate, and non-energy related manufacturing sectors, intensifying structural vulnerabilities. Despite natural resource wealth providing some fiscal buffers, insufficient diversification limits shock absorption, necessitating strategic shifts toward more resilient economic models. Moreover, uncertainty-driven delays in capital expenditure projects exacerbate cyclical downturns, prolonging post-conflict recovery trajectories.

This downward trend in FDI flows impairs technology transfers and regional integration prospects, while constraining employment generation opportunities. Policy frameworks aimed at restoring investor confidence through transparent regulatory regimes, security assurances, and incentives for economic diversification are vital to reversing these adverse patterns.

Global Market Reactions: Equity Market Pullbacks Reflecting Investor Sentiment

The 2026 Middle East tensions also triggered significant equity market selloffs globally, with varying regional impact reflective of investor risk perception and exposure levels. Notably, European and Asian markets experienced sharper declines, with the MSCI European Markets Index falling by 8% and Asian Markets by 7%, compared to a 6.3% decline in the MSCI World Index and a milder 4% drop in the U.S. Market. This uneven contraction underscores the heightened vulnerability of emerging economies within Asia and Europe to geopolitical shocks, amplifying financial market stress and raising the cost of capital amid escalating uncertainty.

Having established the institutional and economic vulnerabilities underpinning emerging markets’ acute exposure to the Middle East-induced shocks, the subsequent subsection will explore contrasting cases of resilience. By examining the successful adaptation strategies employed by select economies, it becomes possible to distill policy lessons and best practices that can help mitigate structural weaknesses and enhance future crisis responsiveness.

Resilient Cases: India and Malaysia Demonstrating Robust Adjustment

This subsection focuses on illustrating how select emerging economies—specifically India and Malaysia—have effectively absorbed and adapted to the shockwaves triggered by Middle East tensions and the resultant energy price volatility. By examining their monetary policy frameworks, inflation anchoring mechanisms, sovereign credit trajectories, and central bank interventions, we aim to distill practical insights into how robust policy design and execution can foster resilience amidst global uncertainty. Understanding these cases provides valuable guidance on policy effectiveness and strategic adaptation relevant for other emerging markets facing similar challenges.

Inflation Targeting Successes and Deviations in India and Malaysia

India and Malaysia exemplify emerging economies that have maintained effective inflation control and economic stability during the 2026 Middle East tensions, despite facing amplified inflationary pressures via exposure to energy price shocks. India's adoption of a disciplined inflation targeting regime has played a pivotal role in anchoring inflation expectations within a defined range, contributing to its relative outperformance against many peers. Data show that Indian inflation consistently remained within its 2 to 6 percent target band over recent years, with deviations lower than global averages, even as oil price volatility elevated input costs. This reflects both credible monetary frameworks and the central bank’s responsive adjustments to evolving price dynamics, mitigating second-round inflationary effects while managing growth objectives.

Malaysia, although not formally operating a fixed inflation target, has effectively deployed a flexible inflation management approach aligned with its macroeconomic objectives. The country’s transition away from a fixed exchange rate regime in 2005 towards a managed float system facilitates exchange rate flexibility to absorb external shocks, notably through adjustments to the nominal effective exchange rate which acts as a key policy instrument. Malaysia's broader monetary strategy, embedding Islamic financial principles aligned with socio-economic sustainability, has further enhanced resilience. The ability to contain inflationary surges during the crisis period speaks to the robustness of Malaysia's monetary and fiscal policy coordination frameworks.

Quantitative Assessment of Central Bank Interventions Compared to Regional Peers

Central bank interventions in India and Malaysia have been quantitatively more effective and timely relative to many other emerging economies confronting similar external pressures. The Reserve Bank of India (RBI) capitalized on a combination of conventional tools—repo rate adjustments, liquidity operations, and forward guidance—to swiftly anchor inflation expectations and stabilize financial markets. Empirical analyses demonstrate a significant and inverse correlation between policy rate movements and inflation trends, with intervention impact peaking within four quarters, reflecting prompt transmission mechanisms and policy credibility. Additionally, research on banking sector sensitivity linked to monetary policy changes highlights the RBI’s counter-cyclical role in preserving financial market stability during heightened volatility phases.

Malaysia’s central bank (Bank Negara Malaysia) adopted a measured intervention approach, leveraging both interest rate adjustments and foreign exchange market operations. The shift to a more flexible exchange rate regime allowed greater exchange rate smoothing capacity, which helped absorb the shock without requiring excessive policy rate volatility. Foreign exchange interventions, while not as aggressive as in some regional peers, were strategically conducted to moderate excessive volatility and support market confidence. The central bank’s reserve adequacy and macroprudential tool deployment contributed to maintaining broad financial stability, limiting capital flight, and ensuring liquidity conditions remained supportive amidst global uncertainty.

Sovereign Credit Ratings and Market Perceptions Supporting Resilience Claims

During the 2026 geopolitical tensions, sovereign credit rating agencies underscored the relative strength of India and Malaysia among emerging market peers. Both countries sustained stable sovereign ratings with minimal negative outlook revisions, signaling strong investor confidence in their economic fundamentals and policy frameworks. India's rating stability was supported by credible fiscal management and monetary discipline, which buttressed the sovereign’s ability to weather external shocks without deterioration in creditworthiness. Malaysia’s rating stability similarly reflected prudent fiscal stewardship and market-friendly reforms that cushioned the impact of abrupt capital flow reversals.

Credit spread metrics further reinforce this narrative, with limited widening seen in both countries compared to broader emerging market averages. Market assessments suggest that these relatively contained risk premia and stable sovereign spreads were closely related to effective inflation management, clear policy communication, and proven intervention capacity. Such outcomes reduce the likelihood of financial contagion and enable continued access to external financing on favorable terms, facilitating resilience in the face of sustained energy market vulnerabilities.

Mechanisms Anchoring Inflation Expectations and Their Quantitative Effects

The anchoring of inflation expectations in India and Malaysia has been a decisive factor enabling effective shock absorption. India’s formal inflation targeting framework ensures that inflation expectations remain tethered within a credible and transparent target band. Empirical inflation surveys reveal limited long-term de-anchoring despite transitory shocks, supported by consistent central bank communication and data-driven adjustments to policy rates. Structural dynamics such as rural-urban inflation disparities are actively monitored and incorporated into policy deliberations, allowing nuanced responses that target both headline and core inflation components.

Malaysia’s approach, characterized by flexible inflation targeting principles within a broad macroeconomic policy context, also emphasizes measured inflation expectation management through exchange rate policy and macroprudential regulations. While lacking an explicit point inflation target, the country has leveraged its exchange rate as an intermediate target to stabilize prices and maintain growth momentum. These mechanisms reduce the transmission of imported inflation shocks and prevent sustained inflationary spirals. The combination of monetary policy independence, reserve adequacy, and the embedding of social and ethical financial principles enhances credibility and public confidence, further stabilizing expectations.

Building on the insights from the resilient adjustments observed in India and Malaysia, the report next examines the broader spectrum of economic vulnerabilities across emerging and advanced economies. This leads into a discussion of structural weaknesses that amplify shock transmission in less diversified and institutionally constrained environments.

4. Policy Interventions and Institutional Buffers

Immediate Response Mechanisms: Strategic Petroleum Reserves and Their Market Impact

This subsection critically examines the deployment of Strategic Petroleum Reserves (SPRs) as the foremost emergency response tool during the 2026 Middle East energy disruptions. It analyzes the scale, timing, and coordination of SPR releases across key countries, quantifying their direct effects on price stabilization and market volatility mitigation. Additionally, it evaluates alternative producer capacities as supplemental buffers, framing SPR use within a broader emergency supply strategy essential for global market resilience.

Quantitative Overview of 2026 SPR Releases and Their Role in Crisis Response

In 2026, the International Energy Agency (IEA) member countries coordinated an unprecedented emergency release totaling approximately 400 million barrels from strategic reserves, aiming to offset the dramatic supply shortfall following disruptions at the Strait of Hormuz. The United States, holding the largest single SPR stockpile with a capacity of 714 million barrels, accounted for around 172 million barrels of this coordinated release. As of early April 2026, the US had drawn approximately 80 million barrels, with further drawdowns ongoing but constrained by its lowest SPR levels since the 1980s. While providing essential bridging supply, these deployments are insufficient to fully offset the roughly 20 million barrels per day lost, implying a limited duration of efficacy if the disruption persists.

Other key contributors included European Union members and select Asian nations, which cumulatively added to a near 400 million barrel global emergency release. However, these deployments did not just rely on outright sales; strategic exchanges and loan arrangements allowed for temporary reallocations without immediate depletion of stocks, preserving future buffer capacity.

This scale of release represents a significant policy shift illustrating deep concern over supply insecurity and willingness to use reserves aggressively, a reflection of the high stakes in early 2026 geopolitics. Notably, market probability estimates of a prolonged closure of the Strait of Hormuz steadily escalated from 40% in early March to 60% by early May, underscoring the urgency and rationale behind such expansive SPR deployments [Chart: Changes in Market Probability Estimates of Strait of Hormuz Closure].

Nevertheless, physical constraints—such as pipeline throughput limits from underground caverns, port loading capacities, and transport logistics—imposed practical caps on daily release rates, limiting the pace at which reserves could alleviate market tightness. The standard drawdown rate sits near 3-3.5 million barrels daily, underscoring the temporal limitations of SPR interventions during protracted crises.

Price Stabilization and Volatility Moderation Outcomes Linked to SPR Deployments

Empirical data from early and mid-2026 indicate that SPR releases helped moderate short-term oil price spikes induced by supply uncertainty. Coordinated announcements by IEA countries appear to have significantly dampened speculative premiums embedded in crude futures, as evidenced by declines in option-implied volatility and tentative easing in spot market prices following release disclosures.

However, the temporary nature of these effects became apparent as prices rebounded in the ensuing weeks due to sustained geopolitical tensions and constrained spare production capacity. This cycle of rapid price suppression followed by a resurgence highlights the SPR’s role primarily as a psychological and tactical market tool rather than a fundamental supply fix.

Incomplete harmonization among countries in timing and magnitude of releases, as well as variable transparency regarding stock levels, also affected market confidence, limiting the overall price dampening potential. Coordinated release protocols outlined by the IEA emphasize these elements to maximize effectiveness, yet real-world operational constraints and differing national priorities created challenges during this episode.

Furthermore, the depletion of SPR stocks during extended use raises strategic dilemmas about balancing immediate market stabilization with preserving reserve capacity for future emergencies. Protracted reliance on SPR drawdowns risks undermining long-term energy security, necessitating integration of complementary measures.

International Coordination Frameworks and Contractual Mechanisms Underpinning SPR Use

The 2026 coordinated SPR release effort was guided by well-established multinational frameworks spearheaded by the IEA, which mandates member nations to hold the equivalent of 90 days of net oil imports in strategic stocks and provides procedures for synchronized drawdowns. These frameworks include multilateral agreements on volumes and timing, bilateral supply-sharing arrangements, and commercial incentives aimed at encouraging private sector stock releases.

Within the United States, SPR drawdowns are legally authorized by Presidential action under the Energy Policy and Conservation Act, with sales typically conducted through competitive bidding. Contractual terms ensure prompt execution and financial guarantee provisions to secure successful transactions. Parallel exchange mechanisms allow for temporary loans of crude with provisions for premium returns, enabling market participants to manage logistical complexities without immediate stock depletion.

These mechanisms also face operational challenges amid crisis context, including administrative coordination, contract dispute protocols, and logistics management across multiple sites with large storage caverns in Texas and Louisiana. Maintenance of infrastructure integrity and security against potential targeting remain core concerns during periods of geopolitical instability.

The 2026 Middle East crisis effectively tested these institutional capacities, confirming the strategic indispensability of well-coordinated, legally robust, and operationally resilient frameworks underpinning SPR releases.

Alternative Supply Buffers: Assessing Non-SPR Producer Capacity Amid the Crisis

Beyond SPR deployments, the capacity of alternative producers to increase output proved limited and characterized by structural constraints rooted in infrastructure maturity, environmental regulations, and long-term project timelines. Production gains from countries outside the Middle East—such as Brazil’s offshore deepwater fields and Canadian tar sands—are pre-scheduled and not responsive to short-term geopolitical shocks.

Brazil and Guyana together contributed incremental increases in the range of 100,000–200,000 barrels per day, constrained by engineering and environmental limitations. Canada projected a modest increase of approximately 200,000 barrels daily in 2026, following planned field developments. Norwegian North Sea capacity offered some flexibility, especially in mature fields with established flow infrastructures, yet seasonal weather and technical complexities impeded rapid expansion.

These incremental adjustments fell far short of plugging substantial Hormuz-related flow disruptions, reinforcing the criticality of SPRs as the immediate supply buffer despite their limitations.

This structural inflexibility underscores the importance of diversified energy sources and investments in strategic storage and infrastructure to bolster resilience against chokepoint vulnerabilities.

While the immediate deployment of Strategic Petroleum Reserves effectively provided a critical cushion against acute supply disruption and calmed initial market turmoil, its constraints highlight the need for complementary long-term institutional and policy measures. The subsequent section will delve into stabilization frameworks that support market confidence through fiscal discipline and monetary policy credibility, essential for sustaining resilience beyond emergency interventions.

Enhancing Economic Stability Through Fiscal Discipline and Monetary Prudence: Insights on Long-Term Institutional Frameworks

This subsection critically examines the long-term stabilizing role of fiscal rules and monetary policy frameworks in the context of heightened geopolitical risk, including the recent Middle East tensions. It situates these institutional tools as foundational mechanisms that governments employ to reduce policy uncertainty, anchor inflation expectations, and enhance macroeconomic resilience. By analyzing cross-country adherence to fiscal rules, monetary adjustments post-conflict, and the deployment of macroprudential safeguards, this discussion elucidates the ways disciplined policy frameworks mitigate volatility and reinforce investor confidence amid persistent external shocks.

Empirical Evidence on Fiscal Rule Compliance and Its Impact on Economic Volatility

Cross-country analyses indicate that fiscal rule adherence varies substantially, with emerging and developing economies demonstrating meaningful gains in economic resilience when such rules are credibly implemented. By 2025, institutional commitment to medium- to long-term fiscal targets has shown an inversion of conventional vulnerability patterns historically observed in these nations. Countries enforcing fiscal rules experience less pronounced declines in growth, consumption, and investment during geopolitical shocks, primarily by reducing policy uncertainty and reinforcing market confidence in fiscal sustainability.

Crucially, the stabilizing effect of fiscal rules disproportionately benefits economies marked by weaker political institutions and lower governance quality. In these contexts, fiscal discipline acts not merely as a budgetary constraint but as a commitment device that mitigates risks associated with unpredictable fiscal expansions or abrupt policy reversals. This effect underscores the role of fiscal rules in tempering the adverse economic consequences of external shocks, especially for countries in Central and Middle East Asia as well as parts of Sub-Saharan Africa, where political fragility heightens exposure to geopolitical disruptions.

Monetary Policy Adaptations in Response to Energy-Driven Geopolitical Inflation

Monetary authorities have confronted a complex policy environment post-2024 that demands balancing output stabilization against inflation control amid energy price shocks triggered by geopolitical conflicts. The empirical literature reveals that standard responses—such as tightening interest rates broadly—may be suboptimal in the face of supply-side disturbances that simultaneously compress output and elevate price levels.

Central banks have increasingly adopted conditional policy strategies recognizing the ambiguous optimal response to energy-related geopolitical shocks. For instance, instances of loosening interest rates to soften output declines coexist with periods of tightening aimed at preventing inflationary spirals, reflecting a nuanced approach calibrated to the structural composition of shocks. Post-conflict adjustments emphasize preserving inflation anchoring without exacerbating recessionary pressures, often necessitating flexible frameworks that depart from rigid inflation-targeting rules.

The evolving monetary frameworks also incorporate recognition of changing inflation dynamics, including conflict- and cost-push-induced pressures that challenge traditional Phillips curve relations. This has raised debates on the extent to which monetary policy can or should accommodate conflict-generated inflationary shocks without compromising credibility or long-term price stability.

Utilization and Effectiveness of Macroprudential Tools Amid Heightened Geopolitical Risk

The escalation of geopolitical tensions has underscored the importance of macroprudential instruments as complementary buffers to fiscal and monetary policies. The deployment of borrower-based measures, countercyclical capital requirements, and foreign exchange-related tightening has accelerated since the early 2020s, particularly in emerging markets with higher external vulnerability.

These tools serve to moderate systemic financial risks and restrain excessive risk-taking during periods of elevated uncertainty. Quantitative data highlight increased use of concentration limits, loan-to-value caps, and reserve requirements, illustrating a growing prudence in financial sector regulation. Importantly, political economy factors influence the pace and intensity of macroprudential adoption, reflecting institutional capacities and governance structures varying across jurisdictions.

By strengthening the resilience of banking systems and mitigating credit cycles, macroprudential policies contribute to the endurance of the broader economy in the face of external shocks. Their targeted application enhances monetary policy effectiveness, especially in economies where monetary space is constrained by pre-existing vulnerabilities or external debt exposures.

Building on the analysis of fiscal and monetary instruments, the subsequent section will explore the inherent limitations of striving for energy self-sufficiency and the ongoing dependence on regional and global economic linkages, with a focus on the paradoxical experience of major producers and resource-rich economies. This perspective reinforces the imperative for robust institutional buffers to complement structural adjustments.

5. Limits of Self-Sufficiency and Regional Dependencies

Energy Independence Paradox: Persistent Vulnerabilities in the U.S. Despite Record Domestic Production

This subsection critically examines the apparent contradiction between the United States’ record energy production levels and its continuing exposure to international energy price volatility. It underscores the limitations of domestic production in fully insulating U.S. markets and consumers from global supply shocks and price swings intensified by the Middle East conflict. By analyzing price transmission mechanisms, consumer impact, and sectoral cost pass-through, this analysis clarifies the persistent economic vulnerabilities faced by the U.S. despite its energy advantages.

Quantifying Consumer Price Volatility in the Aftermath of the 2026 Middle East Conflict

Following the escalation of conflict in the Middle East in early 2026, notably surrounding the Strait of Hormuz, gasoline prices in the U.S. experienced sharp upward momentum. Despite a robust domestic oil and natural gas production environment, crude oil prices tracked global benchmarks closely, with spot prices surpassing $100 per barrel during peak tensions. This surge translated into a 21.2% increase in gasoline prices over the prior twelve months as of March 2026, significantly contributing to headline inflation reaching 3.3%. The pass-through of these price increases was highly visible at consumer fuel stations, accentuated by regional infrastructure constraints in key markets such as California.

Inflationary effects extended beyond fuel, as rising energy costs factored into broader consumer price indices, with energy composing around 2% of average household expenditure but exerting an outsized influence on consumer sentiment and discretionary spending. The direct monetary impact of these price increases on consumers ranged extensively; households reported increases in annual fuel expenditures aligning with modeled scenarios projecting $50 to $150 billion in aggregate additional nominal spending tied to elevated energy costs. This broad-based price volatility highlighted that even with large-scale domestic supplies, consumer prices remain susceptible to international market disruptions.

In response to the crisis, the United States accounted for the largest share of strategic petroleum reserve releases, contributing 172 million barrels out of a coordinated 400 million barrels released globally. This substantial release effort underscores the limits of domestic production alone to address market tightness and price volatility, reaffirming the interconnectedness of the U.S. energy supply framework with international mechanisms and cooperation.

Breakdown of the total 400 million barrels released from Strategic Petroleum Reserves by contributing countries.

Energy Sector Cost Pass-Through and Transmission to Businesses and Consumers

The persistence of energy price volatility in U.S. markets is facilitated by complex transmission mechanisms linking upstream production costs and international crude benchmarks to downstream prices. Despite record domestic output, the United States remains integrated into global markets; thus, global disruptions impose direct cost pressures on refining and distribution networks. Analysis of Q1 2026 corporate earnings reveals compression in energy sector operating margins due to input cost increases not fully offset by immediate pricing adjustments, emphasizing lag and friction in pass-through processes.

Across affected sectors, energy cost pass-through rates vary significantly. Highly energy-intensive industries, such as chemicals, steel, and transportation, face strong input cost pressures, with estimates indicating approximately 80% of energy cost increases eventually reflecting in consumer prices over the medium term. Transportation, in particular, exhibits substantial sensitivity, as airlines, trucking, and maritime transport allocate 15–30% of operating costs to fuel, thereby amplifying the inflationary ripple effect. Retail and consumer-facing sectors report incomplete pass-through, constrained by pricing competition and demand elasticity, which results in margin pressures and muted short-term price adjustments, but sustained ultimate cost inflation for end consumers.

Consumer Behavioral Responses and Economic Impacts Amid Persistent Price Volatility

Consumer spending patterns post-shock reflect sensitivity not only to direct cost increases but also to broader economic and psychological effects. Elevated fuel prices act as a de facto tax on households, with lower-income groups disproportionately affected due to limited flexibility to absorb higher costs. Recent studies confirm that lower-income households responded to gasoline price surges primarily by reducing consumption volumes, whereas higher-income consumers increased nominal spending levels with minimal change to physical consumption.

The resulting divergence contributes to a K-shaped consumption dynamic, with discretionary spending on non-essential goods such as dining, travel, and apparel more vulnerable to contraction. Consumer confidence metrics show softening sentiment tied directly to energy cost inflation, constraining discretionary expenditure even in the context of stable employment and wage rises. Indirect economic effects also manifest through increased costs in transportation and logistics, exerting upward pressure on a wide basket of goods. Overall, sustained volatility in energy prices is likely to suppress real consumer spending growth, limiting broader economic momentum despite strong production fundamentals at the domestic energy sector level.

These findings demonstrate that high levels of domestic energy production, while beneficial, do not equate to complete insulation from global shocks. The United States continues to experience tangible economic repercussions from geopolitical disruptions, necessitating strategic considerations around diversification, demand management, and longer-term transition to more resilient energy frameworks—an analysis that segues naturally into assessment of regional dependencies and the limits of self-sufficiency globally.

Regional Interdependence Unveiled: GCC Economies' Vulnerability to External Demand Shifts and the Imperative for Diversification

This subsection critically evaluates the dependence of Gulf Cooperation Council (GCC) economies on external demand drivers, with a particular focus on hydrocarbon revenue reliance on China and the sensitivity of export earnings to global economic cycles. It further examines the status and progress of economic diversification beyond hydrocarbons, highlighting the limits of partial insulation afforded by resource wealth. This analysis complements the broader section by elucidating how external shocks propagate through regional interlinkages, underscoring structural vulnerabilities and resilience challenges within the GCC amid ongoing Middle East tensions.

Quantifying GCC Hydrocarbon Revenue Dependence on China (2024–2026)

The Gulf Cooperation Council’s hydrocarbon revenues remain significantly tied to Chinese demand, reflecting deepening trade and investment linkages formed over the past decade. From 2024 through 2026, China has consistently accounted for approximately 30 to 35 percent of total GCC oil and natural gas exports, driving a substantial share of fiscal receipts within the bloc. This relationship is exemplified by long-term supply contracts extending to the mid-2040s, notably the record LNG purchases agreements between Qatar and Chinese state enterprises commencing in 2026. These binding commitments anchor a large portion of GCC export earnings to China’s energy procurement policies and industrial growth trajectories.

Given China’s strategic adoption of hydrogen and clean energy technologies, GCC states are simultaneously positioning themselves as future exporters of clean fuels, thereby extending their energy dependency relationship beyond traditional hydrocarbons. Nonetheless, China’s energy consumption patterns remain largely tied to oil and gas imports, underpinning the continued fiscal impact of Chinese demand fluctuations on GCC countries. This concentrated exposure elevates the sensitivity of GCC economies to shifts in the Chinese economic cycle, trade policy adjustments, or geopolitical tensions affecting Sino-GCC trade corridors.

Export Earnings Volatility in GCC Linked to Global Economic Cycles

GCC export earnings exhibit pronounced volatility synchronized with global economic cycles, reflecting their commodity-dependent trade structure. Historical and recent data demonstrate that periods of global economic slowdown or increased trade tensions correspond with marked declines in GCC hydrocarbon revenues, exerting pressure on fiscal balances and external accounts. The recent geopolitical tensions and associated disruptions, although partially mitigated by elevated oil prices, have nonetheless intensified fluctuations in export volumes and values, constraining near-term economic growth prospects.

The dual forces of price swings and production constraints expose GCC economies to asymmetric shocks, where offsetting gains during commodity price upswings are often undermined by heightened vulnerability in downturns. This cyclical volatility challenges fiscal planning and necessitates greater reliance on sovereign wealth funds and fiscal buffers. Moreover, the heterogeneity within the GCC is notable, with countries like Kuwait and Oman experiencing sharper budgetary pressures due to slower revenue diversification and heavier hydrocarbon revenue dependence, while Saudi Arabia and the UAE benefit from relatively larger fiscal space and more diversified economies.

Evaluating Non-Hydrocarbon Sector Growth and Diversification Progress in GCC Economies

Economic diversification remains central to GCC strategies aiming to reduce vulnerability to external shocks. Over the 2024–2026 period, non-hydrocarbon sectors have expanded to constitute over 60 percent of GCC GDP, driven by investments in financial services, manufacturing, tourism, and emerging technologies. Sustained reforms in regulatory frameworks, infrastructure development, and capital spending underpin this growth, helping offset hydrocarbon sector constraints during periods of geopolitical uncertainty.

Despite these advances, sectoral growth rates vary significantly across member states. Qatar and the UAE display robust non-oil sector expansion, underpinned by sustained capital inflows and technology partnerships, whereas Oman and Kuwait lag in diversification efforts, reflected in higher fiscal deficits and slower uptake of new tax regimes. Initiatives centered on hydrogen production and fuel cell technologies, especially in Saudi Arabia and the UAE, indicate a strategic pivot towards future-oriented energy exports, yet the transition remains a medium- to long-term undertaking with substantial structural challenges.

The partial insulation afforded by diversification to date has mitigated—but not eliminated—the economic consequences of external shocks. The continued predominance of hydrocarbons in government revenue streams and export earnings signals the necessity for accelerated reforms and targeted investments to strengthen non-energy sectors. This includes expanding manufacturing bases, enhancing value chains, and leveraging digital transformation to build economic resilience against future external demand shifts.

While GCC economies have made notable strides in economic diversification, their heavy reliance on external demand—especially from China—continues to present a fundamental challenge. The intricate linkage between regional hydrocarbon revenues and global economic cycles underscores the limits of self-insulation and amplifies the importance of robust policy frameworks. This necessitates closer integration of immediate crisis management mechanisms with long-term structural reforms to bolster resilience against evolving geopolitical uncertainties and market volatilities.

6. Building Future Resilience: Strategic Imperatives

Accelerating Supply Chain Diversification and Renewable Energy Integration to Mitigate Chokepoint Risks

This subsection evaluates actionable strategies to reduce global energy market vulnerabilities arising from critical chokepoints such as the Strait of Hormuz. It integrates assessment of renewable energy deployment timelines, quantifiable targets for supply chain de-risking, regional infrastructure investment imperatives, and advanced portfolio management tactics to optimize risk exposure. The purpose is to inform strategic decision-making on mitigating systemic energy security risks through diversified sourcing and accelerated clean energy transitions over the 2026-2030 horizon.

Defining Renewable Energy Integration Timelines and Targets for 2026-2030

Governments across advanced and emerging markets have committed to markedly expanding renewable energy capacity as a central pillar for reducing dependence on vulnerable fossil fuel supply routes. Currently, consensus policy frameworks set ambitious targets to increase the renewable share of the global energy mix to between 30% and over 70% by 2030, necessitating a robust acceleration in deployment rates starting immediately. This translates into required annual capital expenditure increases on the order of 20-30% year-on-year for the remainder of the decade to meet these objectives.

Key instruments facilitating this expansion include large-scale solar and wind generation projects, grid modernization investments to enhance integration capabilities, and deployment of energy storage technologies critical for managing the intermittency inherent in variable renewables. National renewable acceleration programs—such as EU Renewables Acceleration Areas implemented starting in early 2026—are designed to streamline permitting processes, compress project development timelines, and provide technical and regulatory support to expedite commissioning.

Despite strong growth forecasts projecting renewable capacity globally to increase by approximately 2.6 times the 2022 installed base by 2030, bridging the gap toward pledges such as the COP28 tripling goal will require further policy enhancements. These include minimizing regulatory uncertainty, enhancing grid infrastructure investments, and de-risking private capital inflows via fiscal incentives like green bonds and government loan guarantees. Without these reinforced measures, renewable integration progress risks falling short of the scale necessary to materially mitigate chokepoint structural risks.

Quantifying Chokepoint Risk Reduction Through Supply Chain Diversification

Reliance on critical maritime chokepoints such as the Strait of Hormuz poses a structural vulnerability to energy-importing economies and global markets. To quantitatively assess the benefit of diversified supply chains, risk exposure models suggest that even incremental reductions of 20-30% in volume dependence on single transit routes can substantially decrease market volatility premiums associated with geopolitical tensions. Targeting a cumulative 40-50% reduction in chokepoint reliance through a combination of alternative sourcing, strategic stockpiles, and deployment of floating LNG terminals offers measurable mitigation potential over medium-term horizons.