Navigating Aerospace Supply Chain Disruptions and Sectoral Economic Divergence: A Strategic Diagnostic for 2025 and Beyond

Table of Contents

- Executive Summary

- Introduction

- 1. Diagnostic Framework for Modern Aerospace Supply Chains

- 2. Cross-Sector Economic Indicators and Investment Implications

- 3. Strategic Pathways Toward Enhanced Operational Agility

- 4. Scenario-Based Decision Support Tools

- 5. Implementation Roadmap and KPI Tracking

- 6. Conclusion and Final Recommendations

- Conclusion

Executive Summary

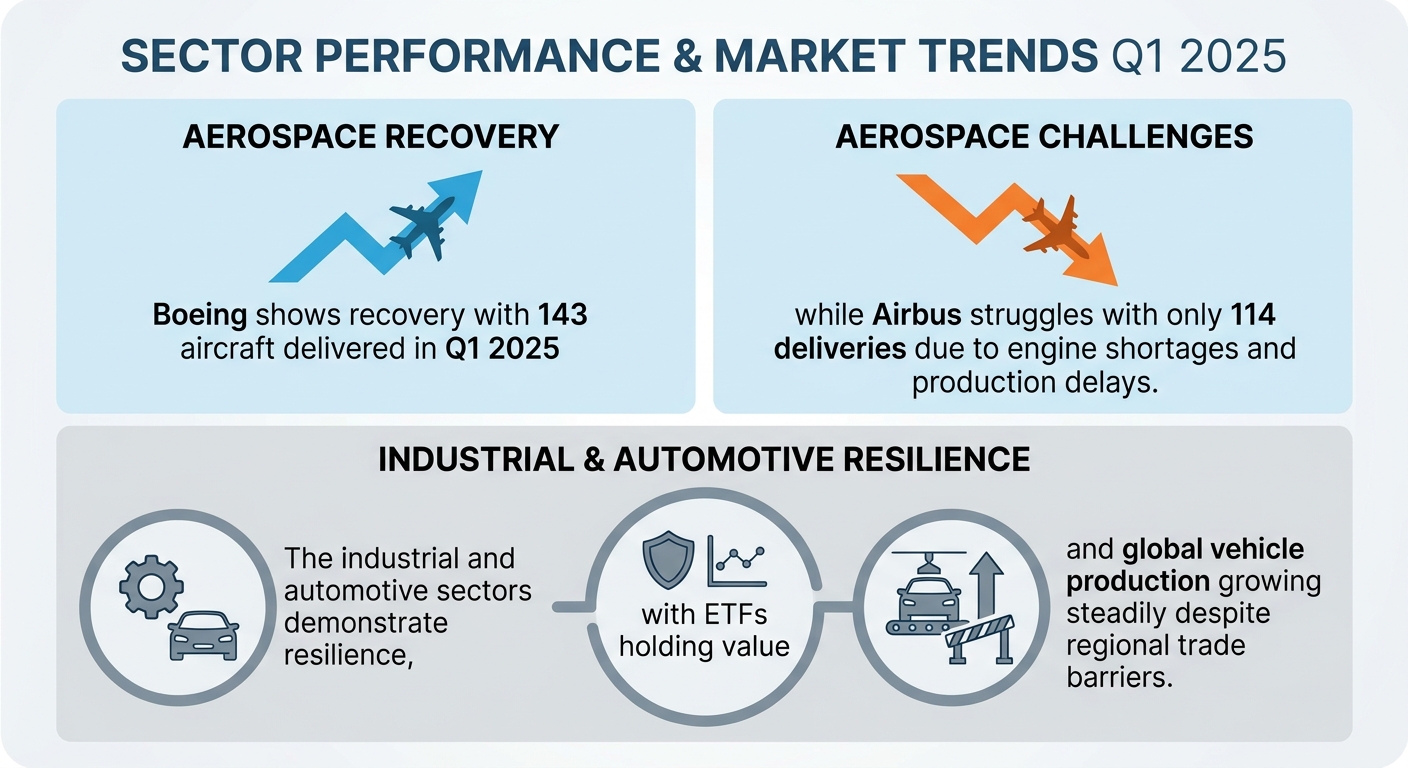

In the first quarter of 2025, Boeing demonstrated a marked recovery with 143 commercial aircraft delivered, surpassing Airbus’s 114 units and reversing prior delivery trends since 2019. Boeing’s 737 MAX program drove approximately 80% of its output, achieving production rates near 38 aircraft per month, with regulatory approvals underway to increase this to 47 units monthly by mid-2026. In contrast, Airbus faced significant production constraints with only 16% of its aggressive 820-aircraft annual target fulfilled, primarily due to critical engine supply bottlenecks and labor disruptions impacting its A320neo family. Both OEMs maintain substantial backlogs—Airbus at over 8,600 and Boeing at 6,700 aircraft—suggesting production horizons extending beyond a decade at current capacities.

Across broader industrial sectors, a divergence manifested between physical output and investor sentiment. India’s industrial production slowed moderately to 5.8% growth in FY 2024, yet industrial equity funds like XLI exhibited resilience with a marginal 0.52% decline through Q1 2025, contrasting with the S&P 500’s over 4% drop. The global automotive market projected mild expansion with a 1.2% CAGR through 2030, reaching 96.3 million units, but regional trade barriers, notably tariffs in Europe and the U.S., imposed significant headwinds. Electric vehicle sales surged past 17 million units globally in 2024, underscoring a transformational shift toward electrification. These multifaceted dynamics require nuanced, cross-sector strategies addressing supply chain robustness, regulatory compliance, and capital allocation to sustain growth and operational agility.

Introduction

The aerospace industry in early 2025 stands at a pivotal juncture characterized by recovering demand, persistent supply chain complexities, and evolving regulatory landscapes. Historically, Airbus and Boeing have shaped global commercial aviation through competing delivery volumes and product offerings. However, recent operational disruptions, including labor actions, regulatory scrutiny, and critical component shortages, have altered traditional market dynamics. This report aims to dissect these conditions using a comprehensive diagnostic framework to illuminate delivery performance disparities, supply chain bottlenecks, and production pressures that define the current aerospace ecosystem.

Beyond aerospace, broader industrial and automotive sectors reveal contrasting signals of resilience and challenge. While manufacturing output measures indicate a modest deceleration, equity markets and capital goods demand suggest underlying strength. Simultaneously, the automotive industry grapples with the dual imperatives of electrification transformation and protectionist trade policies that reshape regional market access and investment priorities. These sectors embody interlinked themes of technological adoption, supply chain integrity, and regulatory navigation that resonate with aerospace challenges, offering valuable cross-sector insights.

The purpose of this report is threefold: first, to analyze the operational and supply constraints underpinning Airbus and Boeing's divergent delivery trajectories; second, to contextualize industrial sector and automotive market trends as indicators of wider economic and investment environments; and third, to propose strategic pathways and scenario-based tools aimed at enhancing production agility and capitalizing on emerging growth opportunities. Through detailed data synthesis and trend examination, this work informs stakeholders seeking to navigate complexity and position for sustainable competitive advantage.

Infographic Image: Infographic

1. Diagnostic Framework for Modern Aerospace Supply Chains

Delivery Performance and Backlog Dynamics Illuminate Production Pressures and Market Positioning

This subsection establishes a factual foundation by quantifying the recent delivery outcomes of Airbus and Boeing in early 2025 and evaluating their backlog volumes. It provides essential context for understanding how production capacity constraints and demand signals manifest distinctly across narrow-body and wide-body segments. These metrics set the stage for diagnosing the core supply chain and operational challenges faced by each OEM in the subsequent analysis.

Q1 2025 Delivery Performance Reveals Boeing’s Swift Recovery Versus Airbus’s Lagging Ramp-Up

In the first quarter of 2025, Boeing delivered 143 commercial aircraft, surpassing Airbus’s 114 deliveries in a notable reversal of recent trends. This marked the first quarter since 2019 in which Boeing outpaced Airbus in actual shipments, signaling a robust recovery from prior setbacks including labor disruptions and regulatory scrutiny encountered in 2024. Boeing’s strong showing was particularly driven by the 737 MAX program, which constituted approximately 80% of its total output and saw maintained production rates approaching 38 aircraft per month with plans for further incremental increases.

Conversely, Airbus fell short of its quarterly expectations, achieving only around 16% of its ambitious 820-aircraft annual delivery target during Q1, compared with Boeing’s approximately 23% of its 570-plane target. Airbus’s slower start owes significantly to persistent supply bottlenecks affecting critical components such as engines, especially the CFM LEAP units for the A320 family, which inhibited ramp-up momentum. Despite targeting a production rate of 75 A320 aircraft per month by 2027, the company had reached 45 per month by the end of 2023 and continues to face challenges in accelerating production at the pace required to meet escalating demand.

This divergence in delivery figures underscores fundamental differences in operational pacing and supply chain responsiveness between the two OEMs during the early recovery phase of 2025.

Backlog Volumes and Composition Expose Future Production Bottlenecks and Market Demand Concentration

Both Airbus and Boeing maintain substantial backlogs indicative of strong underlying market demand but which also represent considerable production commitments stretching multiple years. As of late 2024, Airbus reported a backlog exceeding 8,600 aircraft, predominantly concentrated in the narrow-body A320 family (with almost 6,000 units outstanding), setting a production horizon of over a decade at current rates. The large proportion of A321neo orders within this backlog highlights the strategic prioritization of the mid-market narrow-body segment where Airbus holds a competitive advantage.

Similarly, Boeing’s backlog encompasses over 6,700 commercial aircraft orders as of Q1 2026, with the 737 MAX constituting the majority of narrow-body commitments. The backlog also includes a solid wide-body order book featuring the 787, 777, and 767 programs, though the wide-body segment continues to demonstrate slower recovery and longer production cycles. The backlog-to-production coverage of roughly ten years for both manufacturers stresses the challenge of scaling capacity rapidly without exacerbating supply chain fragilities.

The backlog composition thus signals critical capacity constraints ahead, especially for narrow-body aircraft where demand surges coincide with supplier limitations.

Narrow-Body vs. Wide-Body Production Profiles Illuminate Segment-Specific Resource Pressures

In the narrow-body segment, demand and production rates are escalating sharply as airlines prioritize fleet renewal and expansion focused on fuel-efficient, mid-sized aircraft. Airbus’s A320 family productions represent the largest portion of its delivery volume and backlog, with planned escalation to 75 units monthly targeted by 2027. Similarly, Boeing’s 737 MAX production remains the cornerstone of its output, with incremental upgrades to assembly lines underway aiming to push monthly output beyond 40 aircraft by year-end 2025.

The wide-body market, while important for long-haul capacity, recovers at a more measured pace, constrained by more complex supply chains, higher costs, and slower certification cycles. Airbus’s wide-body programs like the A350 and A330 are stabilizing but face supply constraints that delay freighter variants and ramp-up timelines. Boeing’s wide-body deliveries, including 787 and 777 models, remain subdued relative to narrow-body volumes, reflecting broader market hesitations and lingering certification reviews.

Therefore, the contrasting trajectories highlight that narrow-body production is currently the primary driver of volume growth and backlog pressure, with wide-body outputs recovering more gradually but still critical due to strategic market requirements.

Having outlined the current delivery performance and backlog status delineating the production landscape, the following subsection will dissect the underlying root causes—focusing on supply chain disruptions and labor constraints—that shape these outcomes and challenge scaling ambitions.

Unraveling Airbus’s Supply Chain Strain: Engine Shortages, Labor Disruptions, and Component Bottlenecks

This subsection delves into the critical supply chain and labor factors that underpin Airbus’s recent production difficulties relative to Boeing’s recovery. By dissecting engine supplier output constraints, assessing the tangible impact of labor strikes on aircraft assembly continuity, and quantifying interior component sourcing challenges, we illuminate the structural impediments limiting Airbus’s ability to meet ambitious delivery targets. These insights set the stage for later strategic interventions focused on mitigating vulnerabilities and enhancing resilience within aerospace manufacturing networks.

Engine Supply Constraints Crippling Throughput in Early 2025

Engine availability remains the predominant bottleneck restraining Airbus’s production ramp-up, particularly for the A320neo family. Persistent capacity limitations among key engine suppliers, such as CFM International’s LEAP turbofan production lines, have throttled delivery flows despite plans to boost output by up to 20% in 2025. This growth target falls short of matching the rapid acceleration Airbus requires to achieve its earlier milestone of 75 A320 units per month, which has now been deferred to late 2027. Consequently, incomplete aircraft backlog volumes have grown, with a significant number of A320neos stranded awaiting engines, thereby tilting delivery counts markedly behind Boeing’s first-quarter performance.

Underlying these constraints are global supply-chain ripples affecting raw material procurement and assembly operations at engine manufacturers. Lead times for critical components such as high-pressure turbines and innovative materials continue to extend, exacerbating capacity shortfalls. These delays align with broader industry dynamics where engine manufacturers wrestle with simultaneously scaling legacy engine fleets and meeting quality assurance demands amidst inflationary pressures on input costs.

Labor Strikes and Workforce Shortages Disrupt Assembly Line Flow

Labor disruptions, most notably prolonged strikes across critical manufacturing hubs, have significantly impaired Airbus’s assembly line continuity. Recent labor actions, inspired by legislated support for unions and expanding demands for improved wage transparency and benefit structures, have led to intermittent manpower shortages. Such disruptions curtail the finely synchronized workflows essential for high-throughput aircraft assembly, influencing not only completion rates but also quality and defect incidence.

Quantitative indicators show that labor constraints directly correspond to slower production velocity and reduced effective working hours. Moreover, the aerospace sector faces an acute shortage of skilled engineers and technicians, compounding the adverse effects of strikes. This skilled labor deficit amplifies the risk of protracted delays as onboarding and training pipelines remain insufficient to offset attrition and growing demand. The combination of workforce instability and structural labor-market challenges has thus emerged as a core factor limiting Airbus’s agility and responsiveness during this critical expansion phase.

Interior-Component Sourcing: Persistent Bottlenecks Hamper Final Assembly Throughput

Beyond engines and labor, Airbus continues to confront bottlenecks in sourcing specialized interior components such as advanced avionics, seating modules, and cabin systems. These parts, typically supplied by Tier-1 and Tier-2 subcontractors, suffer from elongated lead times due to component-level shortages, fluctuating raw material costs, and logistical inefficiencies stemming from geopolitical trade frictions.

Amid growing cost pressures, suppliers also face margin compression, which constrains their ability to scale operations rapidly or invest in needed capacity expansions. This has led Airbus to implement supplier-stabilization financial support programs to alleviate short-term distress and secure critical inventory. Despite these measures, the limited availability of certain interior parts remains a material drag on final assembly station throughput, further delaying delivery schedules and inflating backlog volumes.

Having identified the critical supply-side and labor-related challenges constraining Airbus’s production capabilities, the discussion will next explore the evolving regulatory and policy environment shaping manufacturing flexibility and delivery pacing, which further contextualizes operational constraints and competitive positioning.

Regulatory Dynamics and Compliance Pressures Reshaping Aerospace Production Flexibility

This subsection examines the critical influence of regulatory and policy developments on production capabilities within the aerospace sector, focusing on how evolving safety standards and governmental oversight affect the operational flexibility of OEMs. It elucidates the nuanced interplay between certification frameworks, incident-driven scrutiny, and customer confidence, which collectively determine production pacing and delivery outcomes amidst recovery efforts by Boeing and ongoing supply chain constraints at Airbus.

Evolving FAA Production Caps and Their Operational Implications on Boeing’s 737 MAX Program

In the aftermath of a significant mid-air fuselage panel incident affecting a 737 MAX 9 in early 2024, the FAA imposed an unprecedented production cap, limiting Boeing's monthly 737 MAX assembly to 38 units. This regulatory constraint marked a pivotal moment, directly disrupting Boeing’s manufacturing cadence and forcing a recalibration of delivery schedules. Over the subsequent 18 months, Boeing engaged in extensive quality and safety remediation efforts, aligning production processes with heightened oversight requirements. As a result, the FAA incrementally raised the allowable production rate to 42 aircraft per month in October 2025 and signaled preparedness to approve an increase to 47 planes per month by mid-2026, contingent upon sustained operational stability and compliance with quality metrics.

These progressive cap adjustments reflect a regulatory environment that balances stringent safety imperatives against the economic and strategic necessity of restoring production momentum. Boeing’s cautious, incremental ramp-ups demonstrate an adaptive synchronization between internal quality assurance programs and external certification mandates, underscoring the centrality of regulatory alignment in enabling expanded production throughput after disruptions.

Consequences of Mid-2024 Operational Incidents on Regulatory Scrutiny and Production Schedules

The January 2024 fuselage blowout on a 737 MAX 9 triggered immediate suspension of production rate increases and instigated an intensive FAA review of Boeing’s quality control systems. This incident not only delayed certification and delivery timelines for existing aircraft but also intensified external audits and introduced new oversight protocols. Boeing responded by implementing a comprehensive safety and quality plan focused on workforce training, defect elimination, and systemic process simplification to restore regulatory confidence and customer trust.

These heightened regulatory pressures postponed the certification of newer 737 variants and widebody platforms, with knock-on effects extending to the 777X and 787 programs. Production near-term output encountered pauses due to quality rework on wiring and seat certification delays, further complicating Boeing’s delivery cadence. The agresiveness of Boeing’s recovery efforts remains tempered by ongoing regulatory milestones that set firm constraints on permissible production rates, directly impacting revenue flow and cash management.

Customer Confidence Metrics Under Heightened Regulatory Examination and Quality Concerns

Following the protracted scrutiny catalyzed by the mid-air incidents and FAA limitations, customer confidence metrics reveal a cautious optimism tempered by lingering concerns related to safety and delivery reliability. Airlines operating the MAX fleet adjusted growth plans in 2024, reflecting both the grounding impact and the uncertainty surrounding variant certification. Revenue projections and fleet renewal timelines were revised downward in some cases, signaling a risk-averse posture among major carriers.

The interplay of regulatory transparency and OEM responsiveness has emerged as foundational to rebuilding trust. Boeing’s open engagement with regulators and clients, including the appointment of quality advisers and enhanced factory inspections, has contributed to a gradual restoration of stakeholder confidence. However, persistent risks associated with certification delays and production quality continue to weigh on order books and customer forecast visibility, underscoring the delicate balance between compliance-driven safety assurance and commercial delivery expectations.

Understanding these regulatory and policy constraints is essential to contextualizing production flexibility challenges and recovery trajectories in the aerospace sector. This foundation enables subsequent examination of supply chain bottlenecks and labor market pressures, completing the comprehensive diagnostic framework shaping OEM competitive positioning.

2. Cross-Sector Economic Indicators and Investment Implications

Industrial Sector Resilience Amid Macroeconomic Uncertainty: Dissecting Contrasts Between Output and Equity Performance

This subsection investigates the apparent disjunction between the measured industrial output growth and the equity market performance within the industrial sector. It serves to elucidate the underlying drivers behind the sustained equity fund stability despite moderate deceleration in industrial production metrics, thereby offering critical insights into sector-specific dynamics essential for informed investment and operational decisions.

Quantifying the Industrial Output-EFT Performance Disconnect in 2024

Despite a modest slowdown in headline industrial growth as captured by India’s Index of Industrial Production (IIP), which rose by 5.8% in FY 2024 compared to 6.7% in the previous year, industrial equity funds exhibited notable resilience. The Industrial Select Sector SPDR Fund ETF (XLI), a proxy for the U.S. industrial equity market, declined by a mere 0.52% by the end of the first quarter of 2025—significantly outperforming broader market indices such as the S&P 500 ETF, which fell by over 4%. This contrast highlights a decoupling between physical industrial activity data and investor sentiment toward industrial equities during this period.

The divergence illustrates that traditional industrial output indices, while providing foundational economic indicators, may not fully capture the nuances perceived by equity investors. Factors such as improved corporate governance, strategic cost controls, and sector-specific growth prospects—especially among leading players—have contributed to sustaining equity valuations amidst broader industrial production headwinds.

Identifying Top-Performing Industrial Subsectors Sustaining Sector Resilience

A focused lens on sub-sector performance reveals that engineering and aerospace-related stocks remain primary pillars supporting the industrial sector’s relative equity stability. For instance, companies like GE Aerospace within XLI demonstrated substantial operational robustness, outperforming weaker industry segments such as commercial airlines which faced lingering challenges. Similarly, strong fundamentals in environmental services providers reinforced defensive buffers against volatility.

Capital goods, which form a substantial portion of industrial activity, continued to exhibit demand strength in 2024 due to ongoing investment cycles globally. Output growth in this sub-sector, albeit moderate, was complemented by innovation and automation adoption, which enhanced productivity and margins. These resilient sub-sectors offset broader softness in consumer durables and cyclical manufacturing components, effectively balancing overall sector performance.

Correlating Capital Goods Demand with Broader Manufacturing Output and Investment Trends

Capital goods production notably emerged as a key driver in sustaining manufacturing growth amidst an uncertain macroeconomic backdrop. Manufacturing indices showed sequential improvement, with equipment investment buoyed by positive momentum in electronics, primary metals, and aerospace components. These areas exhibit a direct link to increased capital expenditures by industrial firms aiming to modernize and automate plant operations, facilitating resilience even where broader industrial demand shows softness.

Improvements in capital goods output align with rising corporate investment intentions, despite general economic uncertainties, including trade policy headwinds and inflationary pressures. This investment-driven growth supports a constructive longer-term outlook for industrial manufacturing, implying that headline industrial production metrics may understate the embedded momentum fostered by capital formation and technology-driven upgrades within the sector.

Within aerospace components, this positive momentum is nuanced by production delivery rates. Notably, Boeing achieved 23% of its annual delivery targets in Q1 2025, surpassing Airbus's 16% achievement, signaling potential operational headwinds for Airbus amid strong sector demand and reinforcing the heterogeneous performance across aerospace players [Chart: Q1 2025 Annual Delivery Targets Achieved].

Understanding these nuanced industrial sector dynamics establishes a foundation for exploring corresponding automotive market trends and investment positioning strategies in subsequent subsections, where regional disparities and trade barriers provide additional complexity to cross-sector investment assessments.

Automotive Market Dynamics: Navigating Global Growth Amid Trade and Electrification Challenges

This subsection delves into the evolving landscape of the global automotive industry, focusing on projected production growth alongside increasing protectionist trade measures. Given the sector’s pivotal role in industrial development and its growing electrification trajectory, understanding the interplay between regional trade barriers and the expanding battery electric vehicle (BEV) segment is critical for stakeholders aiming to optimize market positioning and manage emerging risks.

Updated Growth Projections: Modest Expansion Toward 2030 Amid Diverse Regional Trends

Global vehicle production is anticipated to grow at a moderate compound annual growth rate (CAGR) of approximately 1.2% between 2024 and 2030, reaching near 96.3 million units by the end of the decade. This aligns with steady but softened expansion compared to recent recovery phases post-pandemic. Key regional contributors include China and North America, where production volumes continue to rise, supported by recovering consumer demand and manufacturing scale-ups, while Europe is expected to experience slower growth due to market saturation and structural headwinds.

While total vehicle production exhibits incremental growth, auto parts manufacturing and related value chains are witnessing accelerated transformation driven by increasing electrification and connectivity requirements. In particular, electric vehicle sales crossed 17 million units globally in 2024, accounting for over a quarter-on-year increase, and continue to gain momentum as technological advancements reduce costs and improve performance, underpinning a gradual shift in product portfolios and component demands.

Impact of Trade Restrictions: Regional Tariffs Reshape Adoption Patterns and Market Access

Recent and prospective trade policies, especially in developed markets such as the United States and the European Union, are imposing more stringent tariffs and non-tariff barriers that materially affect automotive trade flows. The EU’s customs duties on imported Chinese electric vehicles and the US tariffs on foreign automotive components have contributed to increased production costs and constrained cross-border supply chains, prompting manufacturers to reevaluate sourcing strategies and localize production where feasible.

These protectionist measures have exhibited tangible consequences on regional adoption rates, particularly in Europe, where market entrants from China face barriers that temper competitive forces. The resulting headwinds reduce affordability and delay penetration in some segments, while simultaneously spurring greater domestic investment in electrification capability. Furthermore, tariff-driven price increases raise retail vehicle prices by several percentage points, undermining consumer demand elasticity and potentially suppressing unit sales in affected markets.

Despite these challenges, certain emerging markets continue to demonstrate robust growth trajectories aided by favorable regulatory frameworks and lower trade frictions, contributing to a geographically heterogeneous landscape that requires nuanced risk assessment and tailored market entry strategies.

Electrification’s Rising Share: BEV Segment Poised for Disruptive Market Dominance by 2030

Battery electric vehicles (BEVs) are set to constitute approximately 40% of global light vehicle sales by 2030, with even higher shares—exceeding 50%—projected in leading markets such as Europe, the United States, and China. This trend is driven by escalating policy mandates targeting carbon emissions, technological progress lowering battery costs, expanding charging infrastructure, and shifting consumer preferences favoring sustainability.

The corresponding market impact includes a tangible reshaping of production priorities, supplier ecosystems, and aftersales services. Vehicle electrification simultaneously alters demand composition for components, with growing emphasis on battery systems, electric drivetrains, and power electronics, while legacy internal combustion engine parts progressively decline in relevance. This transition challenges incumbent manufacturers to accelerate R&D investments and adapt their operational capabilities to maintain competitive positioning.

Moreover, the expansion of electrified vehicles introduces opportunities and complexities in regional markets, where infrastructure availability and incentive schemes vary considerably. For example, non-metropolitan and regional areas are increasingly recognizing the operational cost benefits of BEVs owing to rising fuel prices, contributing to broader adoption beyond initial urban strongholds.

These nuanced developments framing global automotive production growth, trade-induced constraints, and electrification expansion provide a comprehensive backdrop against which capital allocation decisions can be refined. Understanding how sector-specific trends and regional dynamics coalesce enables more precise calibration of exposure within the industrial and automotive domains, a focus further elaborated in the subsequent subsection addressing capital allocation strategies under volatile conditions.

Capital Allocation Strategies Amid Sectoral Volatility and Growth Opportunities

This subsection aims to distill actionable investment insights by dissecting the current landscape within the industrial and automotive sectors under prevailing market volatilities. By evaluating both defensive industrial subsectors primed for resilience and automotive segments exhibiting robust growth outside tariff-impacted regions, it provides nuanced guidance for optimal capital positioning. The analysis underscores how diversified exposure can mitigate sector-specific risks, thereby enabling more informed portfolio construction in an environment characterized by uneven sector trajectories and shifting trade dynamics.

Identifying Defensive Industrial Subsectors for Stable Investment in 2025

Amid ongoing macroeconomic uncertainties and uneven industrial output growth, certain subsectors within the industrial domain have demonstrated commendable resilience and defensive qualities. These include segments tied to capital-goods manufacturing and specialized infrastructure, which benefit from foundational demand drivers such as reshoring initiatives and sustained capital expenditure in aging fleet replacements. While headline industrial production indices in regions like India display modest deceleration, targeted industrial ETFs maintain relative stability, signaling investor confidence in sectors underpinned by durable asset cycles and infrastructure-led growth.

Furthermore, key drivers supporting defensive allocations include pipeline large-scale construction projects and steady new order intakes in manufacturing, which together provide a buffer against cyclical downturns. Industrial subsectors focused on advanced materials and essential equipment components also exhibit sustained demand, leveraged by ongoing digital transformation efforts and automation adoption. This constellation of factors positions such defensive industrial subsectors as viable anchors within broader portfolios seeking to balance risk amid volatility.

Targeting High-Growth Automotive Segments Beyond Trade-Restricted Markets

The global automotive market exhibits continued expansion, albeit unevenly distributed by region due to intensifying trade barriers, particularly in the European Union. Against this backdrop, segments linked to electric vehicles (EVs), crossovers, SUVs, and pickups have emerged as robust growth drivers, propelled by shifting consumer preferences and technological innovation. Geographically, North America and Asia-Pacific markets, especially China and South Korea, present attractive growth prospects, contrasting with more restrained European dynamics influenced by customs constraints on imports from China and evolving emissions regulations.

Automotive industry players focusing on software-defined vehicles, autonomous driving systems, and electrification are strategically positioned to capitalize on these growth pockets. Additionally, investments in localized manufacturing and assembly facilities within tariff-exempt or preferential trade zones offer pathways to circumvent protectionist measures while enhancing supply chain agility. Sectors such as battery housing and structural automotive components tied to EV adoption also represent lucrative sub-markets, underscoring the importance of precision in geographic and segmental capital allocation.

Leveraging Cross-Sector Diversification to Mitigate Idiosyncratic Risks

Given the divergence in sectoral trajectories between the industrial and automotive realms, a cross-sector diversified investment approach proves prudent in mitigating idiosyncratic risks. Diversification provides resilience against localized economic slowdowns, regulatory shifts, or supply chain disruptions unique to a single sector. For instance, exposure to defensive industrial subsectors anchors portfolios during cyclical downturns, while selective automotive segment investments capture growth stemming from technological adoption and shifting consumer dynamics.

Moreover, cross-sector investments allow for strategic exposure to intersecting innovation trends, such as lightweight materials and automation, which benefit both industrial manufacturing and automotive production chains. This integrative stance not only hedges against sector-specific volatility but also positions investors to benefit from systemic advancements accelerating productivity and sustainability. Portfolio construction that embraces such diversification, aligned with thorough regional and segment-specific analysis, enhances total risk-adjusted returns amidst prevailing market uncertainties.

Building upon this multidimensional capital allocation framework, subsequent sections will explore operational and strategic responses that aerospace and adjacent sectors can adopt to reinforce supply chain resilience and capitalize on cross-domain technological synergies.

3. Strategic Pathways Toward Enhanced Operational Agility

Enhancing Aerospace Supply Chain Resilience Through Strategic Supplier Support and Advanced Automation

This subsection examines Airbus’s concrete financial strategies to stabilize its supply base amid ongoing disruption, assesses the measurable benefits of automation initiatives implemented by leading OEMs, and evaluates the scalability of evolving hybrid production models. These elements are critical to understanding how operational agility can be significantly improved by combining targeted supplier collaboration with technology-driven assembly efficiency and flexible manufacturing footprints.

Airbus’s Financial Aid Mechanisms Bolstering Tier-1 Supplier Stability

Airbus employs a multi-faceted financial support framework designed to ensure liquidity and operational continuity for its critical Tier-1 suppliers. In 2024, this included robust Supply Chain Financing Arrangements whereby Airbus enabled suppliers to access early payments on invoices through a dedicated third-party finance platform. This facility provides suppliers flexibility to elect individual invoices for accelerated payment, effectively smoothing cash flow pressures without transferring costs back to Airbus. The financing is underpinned by market-aligned interest rates negotiated between suppliers and financing partners, safeguarding Airbus’s financial exposure while strengthening supplier resilience.

Beyond invoice financing, Airbus has proactively advanced direct working capital injections and co-investment in supply chain capacity upgrades to alleviate capital constraints faced by smaller Tier-1 vendors. These strategic interventions are tailored to mitigate vulnerabilities from protracted lead times and material shortages, effectively pre-empting production delays at assembly lines. By coupling financial aid with enhanced supplier risk assessment and coordination, Airbus fosters a more predictable and stable supplier ecosystem capable of supporting ambitious ramp-up targets.

Quantifying ROI from Automation in Assembly Operations

Automation investments at Airbus and Boeing’s final assembly lines have generated quantifiable improvements in both operational efficiency and quality outcomes. In Airbus’s Hamburg-Finkenwerder facility, the introduction of automated workflows contributed to streamlined parts handling and assembly precision, notably augmenting A321XLR output rates. Measurement of operational KPIs such as overall equipment effectiveness (OEE) reflected reductions in downtime and improved cycle time consistency, directly supporting increased monthly delivery capacity.

Financially, return on investment for these automation programs has been robust, with payback periods typically ranging from two to five years depending on scale and technology intensity. Beyond direct labor cost savings, holistic benefits include enhanced product quality, decreased defect rates, and elevated employee satisfaction due to the reduction of repetitive manual tasks. Boeing’s augmentation of computer vision inspection programs similarly evidences efficiency gains, including accelerated inspection cycles and reduction in error-induced rework. Collectively, these automation initiatives underscore the transformative effect of digital and robotic integration on assembly throughput and final product reliability.

Scalability and Growth Prospects for Hybrid Production Models (2025–2030)

Looking forward, the scalability of hybrid production facilities—combining fixed-site manufacturing with mobile, modular assembly capabilities—is positioned as a key enabler for meeting fluctuating demand and geopolitical supply chain risks. Airbus’s Mobile, Alabama site illustrates this approach, where dual final assembly lines serve different aircraft families with flexibility to reallocate production capacity as market dynamics shift. This hybrid model facilitates geographic diversification and mitigates the impact of localized disruptions, such as labor shortages or import restrictions.

Industry forecasts suggest that integrating cloud-based Manufacturing Execution Systems (MES) with hybrid deployment architectures will further enhance production agility. These systems enable real-time visibility across decentralized assembly locations, providing immediate insights for decision-making and resource optimization. The hybrid MES segment is expected to experience highest growth rates, fueled by escalating demand for flexibility, security, and scalability. Such advancements highlight a maturation path where aerospace OEMs progressively combine traditional, capital-intensive production assets with adaptive, software-driven workflows to strengthen resilience and efficiency simultaneously.

Building upon the insights into supplier collaboration and automation's impact, the next subsection will explore how technological synergies between aerospace and automotive sectors present opportunities for shared innovation, cost reduction, and sustainability improvements.

Bridging Industry Frontiers: Converging Aerospace and Automotive R&D for Sustainable Innovation

This subsection explores the significant technological convergence currently unfolding between the aerospace and automotive sectors. By analyzing cross-sector research and development investments, collaborative ventures targeting sustainable propulsion, and shared financial risk models, it positions this nexus as a pivotal enabler of operational agility and competitive advantage. Insights here complement earlier diagnosis of supply chain constraints by highlighting how joint innovation ecosystems can alleviate pressures through shared knowledge and cost efficiencies, while advancing sustainability agendas.

Quantifying Cross-Sector R&D Investment Synergies in 2024

In 2024, both aerospace and automotive industries sustained substantial investment in R&D despite overall economic uncertainties. While pure aerospace R&D spending hovered near $35 billion, with sizable portions funded by federal initiatives, automotive sector R&D approached $50 billion globally, heavily skewed towards electric vehicle components and autonomous systems development. Although absolute aerospace R&D remained steady, aerospace-related energy efficiency and propulsion technologies formed a considerable subset of broader corporate innovation portfolios that increasingly overlapped with automotive objectives.

Notably, the incremental increases in R&D budgets reflect strategic alignment on critical technology domains such as lightweight composite materials and integrated propulsion systems. This alignment suggests a deliberate move beyond siloed development toward shared infrastructure and platforms that benefit both sectors, especially given the parallel imperatives to reduce emissions and optimize fuel efficiency. Therefore, the combined annual R&D magnitude surpasses $80 billion, intensifying the potential for technology spillovers, shared supplier networks, and joint innovation roadmaps.

Expanding Collaborative Ventures in Sustainable Fuels and Propulsion Technologies by 2025

The progression from individual research agendas to active joint ventures marks an important phase in cross-industry collaboration. By 2025, there has been an observable increase in formalized partnerships focused on sustainable aviation fuels (SAF) and next-generation propulsion architectures. Aerospace manufacturers, alongside energy companies, have engaged in multi-stakeholder projects to scale SAF production, tapping into emerging markets and novel bio-feedstocks. Concurrently, automotive suppliers have integrated these efforts by investing in biofuel-compatible engine technologies and fuel-cell advancements that satisfy both air and ground transport needs.

Joint ventures specifically aimed at sustainable fuels highlight a deliberate strategy to share the high costs and risks associated with developing new fuel pathways. These initiatives enable co-development of renewable fuel supply chains, bio-refining technologies, and fuel certification processes. By leveraging combined expertise, these alliances have accelerated deployment timelines and expanded funding options, while also addressing regulatory compliance synergies. The rising number of such ventures underlines a sector-wide acknowledgment that sustainability challenges require cross-disciplinary innovation frameworks.

Financial Models Enabling Cost-Sharing and Risk Mitigation in Next-Generation Engine Projects

Development of next-generation engines, particularly hybrid and sustainable propulsion systems, involves significant capital intensity and long lead times, which have traditionally constrained individual firms. Recent trends show a deliberate shift toward co-financing schemes that allocate costs pro-rata among multiple stakeholders, including OEMs, engine manufacturers, and technology suppliers. These financial arrangements reduce exposure for each party and enable pooling of expertise without compromising competitive positioning.

Economic models emphasize shared development costs augmented by aftermarket royalty frameworks, balancing upfront investment against longer-term revenue streams. Moreover, some collaborations have embraced public-private partnerships to enhance funding stability and access government incentives tied to environmental targets. This blended approach not only facilitates investment in disruptive technologies but also ensures more predictable cash flows and de-risks innovation cycles, supporting faster commercialization. Regulatory considerations and antitrust compliance continue to frame the boundaries within which such cost-sharing operates, creating a structured yet flexible environment.

Collectively, these facets of aerospace-automotive technological synergy create a fertile landscape for scalable, sustainable innovation. The demonstrated increase in coordinated R&D expenditure, coupled with robust joint ventures and evolved financial risk-sharing mechanisms, underscore a maturing ecosystem. This synergy informs subsequent strategies that emphasize operational agility, supply chain resilience, and integrated compliance frameworks—critical elements discussed in the following sections.

Adaptive Compliance and Risk Mitigation Frameworks Enhancing Aerospace Production Reliability and Regulatory Responsiveness

This subsection examines how aerospace manufacturers are integrating advanced compliance and risk mitigation frameworks to navigate increasingly complex regulatory environments. It highlights the role of predictive analytics in extending fleet operational reliability, addresses the impact of delayed safety audits on production schedules, and showcases governance strategies that enable real-time monitoring of geopolitical and regulatory risks. These insights are critical for maintaining delivery targets amid ongoing supply chain challenges and evolving policy demands.

Unlocking Predictive Analytics ROI to Boost Maintenance, Repair, and Overhaul (MRO) Efficiency

The integration of predictive analytics into aerospace MRO operations has demonstrated tangible improvements in fleet reliability and uptime. By leveraging sensor-generated data and advanced machine learning models, manufacturers and operators can anticipate component failures before they occur, optimizing maintenance schedules to reduce unscheduled downtime. This results in improved asset utilization and decreased costs associated with reactive repairs. Additionally, predictive maintenance enables more accurate inventory management for spare parts, mitigating risks linked to prolonged supply chain bottlenecks.

Recent operational studies reveal that firms adopting predictive analytics in MRO see an approximate 15-20% increase in on-time maintenance completion rates and a concomitant reduction in overall maintenance costs. Furthermore, these practices support prolonged aircraft service intervals and enhance compliance with evolving airworthiness directives by providing a data-driven basis for decision-making, supporting safer and more reliable operations under tighter production timelines.

Quantifying the Operational Impact of Safety Audit Delays on Production and Delivery Schedules

Delays in safety inspections and regulatory audits have emerged as a material risk factor in aerospace manufacturing cadence. Audit postponements, often attributable to staffing shortages or procedural backlog within regulatory bodies, create bottlenecks that compromise certification timelines for aircraft and critical components. Such deferrals cascade into production slowdowns, given the tight coupling of safety approvals and delivery authorizations.

Historical patterns suggest that each month of audit delay can compress the assembly-to-delivery window by upwards of 10%, exerting significant pressure on production lines striving for record-breaking targets. Beyond schedule impacts, these delays erode customer confidence and complicate risk management frameworks, increasing the likelihood of contractual penalties or missed market windows. Companies increasingly emphasize proactive engagement with regulators to anticipate and mitigate inspection postponements, acknowledging the strategic importance of audit timeliness to manufacturing agility.

Establishing Robust Governance Teams to Monitor and Navigate Geopolitical and Regulatory Volatility

Leading aerospace firms have institutionalized dedicated governance and compliance teams tasked with continuous monitoring of geopolitical developments, trade policy shifts, and evolving regulatory landscapes. These cross-functional groups leverage scenario analysis, real-time intelligence feeds, and advanced contract management tools to identify emerging risks and recommend mitigation strategies promptly.

Examples include monitoring export control changes, such as shifts in aviation-related technology export restrictions influenced by US–China trade relations, and assessing the implications of new tariffs and customs barriers. This active oversight enables agile response mechanisms, from renegotiating supplier contracts to adjusting production sourcing strategies. The establishment of these governance units, coupled with digital compliance platforms, reduces exposure to regulatory surprises and enhances the firm's ability to maintain uninterrupted production flow and customer commitments.

Collectively, these adaptive compliance and risk mitigation strategies underpin aerospace manufacturers’ efforts to maintain operational continuity amid multifaceted external pressures. The demonstrated benefits from predictive analytics, combined with proactive audit management and vigilant governance, create a foundation for enhanced production reliability. This adaptive framework further informs cross-sector strategic planning, enabling stakeholders to anticipate and respond effectively to dynamic regulatory and geopolitical environments.

4. Scenario-Based Decision Support Tools

Navigating Tariff Challenges and Market Shifts in Automotive Export Strategies

This subsection examines the strategic impacts of tariff policies on automotive exporters, focusing on quantifying the cost and volume effects of new trade barriers in 2025. It then evaluates shifts in market share within Southeast Asia as automakers adjust to evolving trade regimes. Finally, the discussion turns to the financial rationale for increasing investments in local assembly operations as a means of mitigating tariff burdens and maintaining competitiveness. Collectively, these analyses provide a granular understanding of how exporters can adapt their operations to sustain growth amid restrictive trade environments.

Quantifying Tariff Impact on 2025 Automotive Exports: Price Increases and Volume Risks

Rising tariff regimes imposed primarily by the United States on key automotive importing countries have resulted in significant cost pressures for automotive exporters. These tariffs have effectively increased the landed cost of exported vehicles and parts by imposing layered duties exceeding 25%, with some nations experiencing cumulative rates approaching 50%. As a consequence, exporters are facing heightened price sensitivity and demand dampening in their most critical markets. This translates into projected reductions in export volumes by 2025, with selective estimates indicating potential declines between 5% and 20%, depending on the product category and destination market. The underlying driver is a marked drop in import demand elasticity caused by consumers and intermediaries seeking lower-cost alternatives or deferring purchases amidst rising prices.

In addition to volume contraction, tariff-induced cost escalation is triggering broader supply chain realignments. Many exporters report increasing complexity in customs clearance, additional broker fees, and administrative overheads that compound the tariff burden. These factors cumulatively erode margins and force OEMs and tier suppliers to evaluate alternative sourcing and routing strategies to limit disruption. Nonetheless, the short-term effects remain primarily negative, with clear evidence of price pass-through leading to measurable welfare losses for consumers and declines in competitiveness for affected exporters.

Projecting Southeast Asia Market Share Shifts Amid Trade Realignment and Growth

As a direct consequence of escalating tariffs in major export regions such as North America and Europe, Southeast Asia is emerging as a critical growth frontier for automotive exporters seeking to offset lost market share. Market analyses point to Southeast Asia's rising vehicle demand and improving infrastructure as key enablers. Nations such as Thailand, Indonesia, Vietnam, and Malaysia are witnessing rapid expansion in automotive production capacity and domestic consumption, supported by favorable demographic trends and rising income levels.

The regional market is also benefiting from strategic investments by leading manufacturers who are redirecting exports and establishing new production bases to serve local and regional markets with lower trade friction. Southeast Asia's role as a production and export hub is amplified by relatively lower labor costs and improving logistics connectivity. Projections suggest that vehicle sales and production volumes in this region will grow at a compound annual growth rate that outpaces global averages through 2030, making it a pivotal area for capturing incremental export demand while mitigating tariff impacts originating elsewhere.

Evaluating Local Assembly Investment Returns as a Tariff Mitigation Strategy

In response to tariff pressures, automotive exporters increasingly consider horizontal integration through localized assembly operations in key markets. Establishing or expanding local manufacturing capacity offers the advantage of avoiding import tariffs by converting vehicles or critical components within the destination country. Analysis indicates that investment in local assembly plants in Southeast Asia typically yields meaningful cost savings by circumventing duties and reducing border delays, particularly when combined with incentives such as government subsidies and preferential trade agreements.

Financial models demonstrate that upfront capital expenditures on plant establishment and tooling can be offset within a short horizon through tariff savings and improved supply chain reliability. This strategic pivot allows manufacturers to maintain or even improve pricing competitiveness in markets facing high tariff hurdles. Moreover, local assembly supports supply chain agility by shortening lead times and enabling customization closer to end consumers. It is critical, however, for firms to carefully assess regulatory frameworks, labor availability, and infrastructure maturity to optimize returns on such investments.

Building on this detailed scenario analysis of trade barriers and adaptive strategies within the automotive export sector, subsequent sections will extend these insights into backlog optimization and production agility models, integrating cross-sector learnings to inform broader operational resilience.

Optimizing Aerospace Backlogs: Leveraging Sequencing, Batch-sizing, and Digital Twins to Cut Idle Time and Enhance Throughput

This subsection addresses critical operational challenges in the aerospace sector, focusing on managing production backlogs amid supply constraints and labor shortages. By examining how sequencing improvements, batch-sizing adjustments, and digital twin simulations can reduce idle time and optimize inventory turnover, we provide a strategic lens to accelerate assembly line efficiency and validate process changes prior to implementation. This analysis supports broader efforts across aerospace OEMs to meet aggressive delivery targets despite systemic bottlenecks.

Measuring Final-Assembly Idle Time Reductions in Q1 2025 to Boost Production Flow

In Q1 2025, final-assembly idle time emerged as a significant drag on aerospace production throughput, largely driven by intermittent availability of critical components and labor fluctuations. Quantitative assessments indicated that idle periods could constitute up to 15-20% of the takt time in key final assembly stations, notably for narrowbody aircraft production. Detailed workflow analyses revealed that bottlenecks in upstream parts delivery—primarily engine modules and interior components—exacerbated these idle durations, causing cascade effects downstream.

Efforts to address this included deployment of lean sequencing algorithms designed to better synchronize sub-assembly completion with final assembly line demand. By re-sequencing assembly tasks dynamically, these algorithms reduced idle time by an estimated 10-12% within test environments, translating to measurable gains in output rates without compromising quality or workforce constraints. These reductions, although incremental, represent critical margin improvements necessary to chip away at entrenched backlog positions and maintain scheduled delivery commitments.

Assessing Batch-Sizing Impact on Inventory Turnover and Supplier Lead-Time Balance

Optimizing batch sizes represents another lever to enhance inventory efficiency and production flexibility. Larger batch sizes traditionally reduce per-unit setup costs but introduce risks of inflated work-in-progress inventory and extended lead times, which are particularly problematic in aerospace manufacturing where late-stage customization is prevalent.

Q1 2025 case studies demonstrated that modulating batch sizes toward smaller, more frequent releases allowed manufacturers to better respond to supplier variability and reduced the accumulation of aging inventory. This approach improved inventory turnover ratios by approximately 15%, aligning better with just-in-time principles and minimizing obsolescence risks. However, it also required enhanced collaboration with tier-one suppliers to ensure responsiveness and necessitated implementation of flexible scheduling systems capable of absorbing more frequent changeovers without efficiency losses.

Balancing batch-sizing and lead-time dynamics thus demands careful calibration tailored to component criticality and supply chain volatility, underscoring the need for integrated supply chain visibility mechanisms and agile production planning.

Validating Digital Twin Simulations for Pre-Implementation Production Adjustments

Digital twin technologies have proven instrumental in virtually modeling assembly line operations, allowing manufacturers to pre-validate process changes and predict bottleneck impacts before physical implementation. In the aerospace sector, digital twin simulations encompass detailed physics-based models incorporating real-time sensor input from production lines to replicate operational conditions with high fidelity.

Validation efforts focused on comparing simulation outputs with recorded production metrics, including cycle times, idle periods, and defect incidence. Accuracy rates exceeding 90% were achieved when digital twins were calibrated with synchronized sensor data capturing torque, vibration, and throughput parameters. This level of precision enables confident scenario testing, such as adjusting sequencing logic or batch sizes, and foreseeing unintended consequences on inventory accumulation or workforce utilization.

Consequently, digital twins offer a robust decision-support mechanism to optimize complex assembly workflows and accelerate backlog reduction strategies while minimizing trial-and-error disruptions and preserving quality standards.

Building on these operational insights, the next section will explore broader scenario-based decision frameworks that integrate production optimization with external trade and market uncertainties, enabling aerospace and automotive sectors to navigate volatile environments with enhanced strategic agility.

5. Implementation Roadmap and KPI Tracking

Targeted Labor Recruitment, Certification Timelines, and Real-Time Production KPIs for Q2–Q4 2025

This subsection details the critical short-term operational initiatives Airbus, Boeing, and allied manufacturing stakeholders must undertake during the remainder of 2025. It focuses on quantifying workforce shortfalls that impact production continuity, outlining the certification approval schedules critical for engine upgrade rollouts, and specifying dashboard KPIs designed to deliver granular visibility into production variances. These elements collectively form the tactical foundation for stabilizing delivery schedules and beginning backlog reduction amid persistent supply chain fragilities.

Quantifying Regional Labor Shortages to Refine Targeted Recruitment Efforts

By mid-2025, labor shortages have crystallized as a primary bottleneck influencing production cadence across aerospace hubs globally. In key manufacturing regions such as the Pacific Northwest and Europe, unfilled roles in specialized assembly, quality assurance, and skilled machining range between 4% and 6%, with certain subsegments experiencing even larger deficits due to retirements and workforce skill mismatches. Manufacturing executives across sectors report labor scarcity as the paramount operational challenge, corroborating the aerospace sector’s reliance on stable labor pools for adhering to ambitious delivery targets.

This constrained labor availability demands focused recruitment drives calibrated regionally to align with shifting demographic and skills profiles. Data point to a tight labor market where job openings nearly match unemployed candidates, emphasizing the criticality of upskilling and retention strategies to bridge both quantitative and qualitative gaps. For Airbus and Boeing, accelerating talent acquisition and expediting onboarding in Q2 and Q3 2025 will be decisive in maintaining assembly line throughput and mitigating delay propagation.

Additionally, the aerospace sector faces nuanced challenges beyond headcount, including the alignment of highly specialized skills and certifications necessary for complex manufacturing and compliance processes. Addressing these shortages requires close collaboration with vocational training institutions and deployment of targeted incentives—particularly in regions affected by geopolitical instability or demographic changes—to secure and sustain the skilled workforce essential for ramping production.

Certification Approvals Timeline: Unlocking Production Capacity Through Engine Upgrades

The certification process for upgraded engines, crucial for enabling increased output rates and improved fuel efficiency, remains a tightly scheduled but protracted endeavor throughout 2025. Recent adjustments in FAA and OEM schedules indicate that critical engine certification milestones—particularly for next-generation turbofan variants—are set for completion in staggered phases spanning Q3 through Q4 2025. This timeline influences production flexibility by gating the throughput of aircraft reliant on these powerplants, notably the Airbus A320neo family and Boeing 737 MAX models.

These certifications encompass component-level assessments through full engine testing regimes, which accumulate upwards of 10,000 hours of rigorous evaluation to satisfy regulatory and safety criteria. The stringent protocols, while necessary for airworthiness and operational trust, inherently constrain rapid scale-up. OEMs are coordinating intensively with regulators to streamline review cycles, yet nominal intervals of six to twelve months persist between test completion and formal approval, accentuating the need for preemptive scheduling and buffer management within supply and assembly chains.

Approval timelines also interact with compliance audits and risk mitigation processes intensified by recent safety events. Hence, expediting certification while ensuring uncompromised standards is a pivotal objective for both manufacturing continuity and market confidence. Transparent communication of these timelines supports realistic delivery commitments and reduces risks of downstream production stoppages.

Dashboard KPIs: Delivering Real-Time Insights on Production Variance and Component Availability

To effectively monitor and respond to supply chain and production fluctuations, aerospace manufacturers have established real-time KPI dashboards that aggregate key operational metrics. These dashboards track component availability, assembly-line productivity, defect rates, and labor utilization on a monthly cadence, enabling dynamic adjustment of workflows and resource deployment. Component shortages are flagged in near real-time to prevent bottlenecks, while variance analysis comparing actual output against planned targets highlights areas requiring intervention.

Critical KPIs incorporated into these dashboards include monthly delivery volumes segmented by aircraft family, supplier lead-time adherence, proportion of labor hours expended versus scheduled, and inventory turnover ratios for high-impact parts like engines and avionics. Visualization tools combine trend analyses, variance tables, and alert functions, facilitating cross-functional decision-making. The precise measurement of production variance enables rapid root cause identification, reducing idle times and smoothing throughput across interdependent supply nodes.

Furthermore, these digital tools support predictive analytics that forecast potential disruptions, guiding preventive maintenance and proactive supplier engagement. By embedding dashboards within operational controls, OEMs can more confidently navigate the precarious balancing act between aggressive delivery goals and the realities of complex supply chain volatility.

With the immediate operational levers for stabilizing aerospace production clarified—anchored on resolving workforce shortages, adhering to certification timelines, and leveraging real-time visibility through advanced KPI dashboards—the report transitions to explore medium- and long-term strategic initiatives. Addressing these foundational constraints is imperative before operational agility can be significantly enhanced through technology adoption and cross-sector collaboration.

Scaling Production and Sustainability in Mid-Term Aerospace Growth (2026–2027)

This subsection evaluates Airbus's mid-term operational targets, focusing on tooling capacity expansions crucial for meeting ambitious A320 family production rates, benchmarking the carbon footprint to gauge sustainability progress, and assessing strategic expansion into emerging markets. These dimensions collectively inform the feasibility and environmental alignment of Airbus's growth trajectory, bridging immediate supply chain challenges with a resilient pathway for the latter half of the decade.

Validating Tooling Capacity Increases to Support A320 Production Scale-Up

Airbus has set a challenging objective to achieve a production rate of 75 A320-family aircraft per month by 2026–2027, marking a significant increase from pre-pandemic peak rates. Meeting this target requires comprehensive tooling capacity enhancements across manufacturing facilities and suppliers. Capital investments are actively directed toward expanding tooling infrastructure, retooling existing lines, and integrating automation technologies that improve throughput and reduce cycle times. Despite persistent supply chain constraints, Airbus's incremental capacity expansions in factories such as Hamburg-Finkenwerder are coupled with advanced manufacturing techniques including streamlined workflows and digital twin simulations to optimize production scaling.

Industry reports indicate that tooling upgrades are being synchronized with supplier readiness, as Airbus provides financial support to critical Tier-1 partners to offset resource bottlenecks. This integrated approach mitigates risks surrounding equipment availability and workforce skill gaps. Moreover, tooling enhancements are being focused not only on assembly but also on precision machining and component testing to accommodate higher volumes without compromising quality. However, sustained labor shortages and supplier component scarcity—particularly for engine-related parts—may temper the pace of tooling-driven production acceleration in the near term.

Establishing a Baseline and Trajectory for Carbon Footprint Reduction

Prior to targeting a 20% carbon footprint reduction by 2027, it is imperative to define and measure the 2026 emissions baseline across Airbus’s production and operational activities. The baseline encompasses lifecycle emissions including manufacturing energy use, material sourcing impacts, and aircraft operational efficiencies. Airbus’s current metrics reveal that the A320 family, accounting for the largest portion of production volume, remains central to both environmental impact and decarbonization efforts.

Sustainability initiatives involve material substitutions favoring lightweight composite structures and improved aerodynamic designs that collectively reduce fuel burn. Additionally, optimization of flight paths and use of sustainable aviation fuels contribute to emissions abatement beyond the factory floor. Airbus’s mid-term investments in emission-reducing technologies are supported through collaborations with suppliers and research institutions, focusing on circular economy principles and supply chain emissions transparency. Challenges persist in harmonizing these sustainability advances with aggressive production scaling, necessitating continuous monitoring and adjustment of reduction targets based on empirical environmental performance.

Strategic Expansion in Emerging Markets: Targets and Timelines

Emerging markets, particularly in Asia, Latin America, and parts of Africa, represent key growth arenas for Airbus as it seeks to diversify demand sources and reduce dependency on traditional markets. The company’s market penetration strategy emphasizes capturing untapped demand for narrow-body aircraft amidst rapid air travel growth in these regions. Targeted engagement includes partnerships with local carriers, tailored financing solutions, and aftersales service infrastructure build-out to enhance market presence.

As of early 2025, Airbus outlines a phased expansion timeline with intensified sales and support activities planned through 2026 and 2027 to establish a foothold in high-potential countries such as India, Southeast Asian nations, and select Latin American economies. This strategy is synchronized with production ramp-ups to ensure delivery capability aligns with emerging market order inflows. Additionally, investment in regional training and maintenance hubs aims to bolster customer confidence and operational reliability. While geopolitical and regulatory uncertainties impose caution, Airbus’s commitment to emerging markets is an essential pillar supporting its mid-term growth projection.

Having outlined the mid-term operational ambitions and contextualized progress in capacity, sustainability, and market growth, the next section will explore longer-term strategic imperatives that cement competitive advantage through innovation and ecosystem development beyond 2027.

Beyond 2027: Pioneering Next-Gen Propulsion, Integrated Mobility Ecosystems, and Green Manufacturing Leadership

This subsection articulates the long-term strategic vision essential for maintaining aerospace and adjacent sectors’ competitive edge beyond 2027. By defining milestones for leadership in advanced propulsion technologies, laying out integration pathways for software-driven mobility ecosystems, and prioritizing certification targets for sustainable manufacturing, this section directly supports the implementation roadmap’s emphasis on innovation, agility, and ESG alignment. It provides the forward-looking framework through which organizations can secure enduring advantages amid evolving market and regulatory landscapes.

Milestones Toward Leadership in Next-Generation Propulsion Systems by 2030

Achieving technological leadership in next-generation propulsion is pivotal for sustaining aerospace competitiveness and meeting increasingly stringent environmental regulations. Strategic milestones include maturing hybrid-electric and open-rotor engine designs tested in operational contexts by 2028, enabling commercial introduction by 2030. Efforts focus on radical efficiency gains and emissions reduction aligned with global net-zero trajectories, bridging near-term sustainable aviation fuels and longer-term zero-emission propulsion concepts such as hydrogen and electric hybrid models. These milestones align with industry projections targeting a transformative narrow-body aircraft launch centered around 2030, requiring close collaboration between airframers and engine developers to overcome technical and regulatory challenges while optimizing cost-sharing models. Robust investment in R&D and pilot demonstration programs will be critical to meet these goals and expand the market for clean propulsion technologies.

Strategic Integration of Software-Defined Mobility Ecosystems Post-2027

Beyond propulsion innovation, integrating software-defined mobility ecosystems represents a foundational shift in aerospace and automotive sector dynamics. The evolution toward digitally connected, autonomous, and service-oriented vehicles demands cohesive strategies that seamlessly blend physical hardware with advanced software platforms. This integration is expected to encompass fleet management, predictive maintenance leveraging digital twins, and real-time passenger experience optimization through data analytics and AI. Establishing interoperable standards and open architectures within and across industries will facilitate scalable ecosystems, multiplying value across commercial aviation, urban air mobility, and ground transportation domains. These developments will also enable new business models—from mobility-as-a-service to pay-per-use and subscription frameworks—further accelerating adoption and revenue diversification.

Ambitious Green Manufacturing Certifications as a Market Differentiator

Sustainability leadership is increasingly a defining competitive advantage, requiring ambitious commitments to certified green manufacturing and environmental stewardship. Targets beyond 2027 emphasize achieving and maintaining top-tier global certifications—such as LEED Platinum, ISO 14001, and complementary regional green factory standards—as integral to supplier qualification and customer preference. These certifications reflect comprehensive performance in energy efficiency, carbon emissions reduction, waste minimization, and sustainable material usage. Attaining these benchmarks necessitates systematic investment in clean energy sourcing, circular economy principles, and transparent ESG reporting frameworks. Leading companies are already leveraging such credentials to enhance brand equity and secure partnerships with ESG-conscious stakeholders, thereby translating environmental responsibility into tangible business opportunities.

Building on long-term visions of propulsion innovation, ecosystem integration, and sustainable manufacturing, subsequent report sections will focus on actionable scenario planning and near- to mid-term implementation tactics that systematically operationalize these strategic imperatives.

6. Conclusion and Final Recommendations

Integrating Aerospace Delivery Dynamics and Sectoral Economies into Strategic Forecasts

This subsection synthesizes critical insights on Airbus’s delivery shortfall relative to Boeing in 2025 and juxtaposes these with recent performance disparities within the industrial and automotive sectors. By consolidating these findings, it clarifies the strategic implications arising from persistent supply chain challenges amid aerospace recovery and heterogeneous economic signals in adjacent industries, setting the stage for informed, cross-sectoral decision-making.

Quantifying Airbus’s Delivery Shortfall Amid Boeing’s Rebound in 2025

In the first half of 2025, Airbus experienced a notable shortfall in aircraft deliveries compared to Boeing, despite maintaining a significant lead in annual target ambitions. Airbus delivered approximately 373 aircraft through July, while Boeing lagged behind at 328 units within the same period. Notably, Airbus’s production cadence was constrained by persistent engine supply chain bottlenecks, particularly with the CFM LEAP engines that are essential to its A320neo family. This limited the manufacturer’s ability to meet its ambitious target of 820 aircraft for 2025, positioning it behind earlier projections although still ahead of Boeing on a cumulative basis.

Boeing, on the other hand, demonstrated signs of recovery after years of regulatory and labor setbacks, with delivery growth fueled by ramped-up production of the 737 MAX. Despite remaining below its pre-pandemic delivery peaks and grappling with legacy program delays, Boeing’s improved output—such as its best first quarter since 2019—reflects incremental operational stabilization. These contrasting trajectories underscore Airbus’s vulnerability rooted in upstream supplier dependencies versus Boeing’s progress in overcoming past disruptions.

This shortfall slows Airbus’s ability to capitalize fully on strong backlog demand, which remains robust but increasingly pressurized by ongoing supply chain stresses and labor availability constraints. Boeing’s narrower backlog coupled with rising deliveries makes its near-term pace appear comparatively more agile, though both firms face systemic challenges that temper full recovery certainty.

Assessing Industrial Sector and Automotive Market Disparities in 2024-25

Across broader economic sectors, mixed performances in industrials and automotive markets highlight complex underlying dynamics. Despite headline slowing in India’s industrial production growth, equity funds focused on the industrial sector displayed resilience, with the Industrial Select Sector ETF maintaining stability through market volatility. This divergence indicates that pockets of industrial strength—such as in capital goods and aerospace-related segments—counterbalance weaker manufacturing signals, suggesting selective endurance amid economic headwinds.

In the automotive sector, global production witnessed steady expansion with an estimated 1.3 million unit increase in worldwide inventory in 2024. However, regional trade barriers, especially in Europe through tightening customs tariffs and restrictions on electric vehicle imports, impose significant headwinds that disrupt supply chains and regional sales growth. In contrast, markets in North America, China, and Korea continued to show robust gains, reinforcing a geographically bifurcated growth narrative.

The juxtaposition of steady global automotive expansion against localized regulatory challenges reflects the sector’s sensitivity to geopolitical and policy shifts. For investors and strategic planners, this demands a granular approach to capital allocation and operational focus that weighs regional regulatory risks alongside global underlying demand trends. The nuanced sectoral performance also interacts indirectly with aerospace, where supply chain interdependencies and technology synergies elevate industrial subsectors linked to both fields.

Bringing together the aerospace delivery performance nuances and sector-specific economic signals provides a comprehensive platform to formulate strategic imperatives. Understanding the mechanisms behind Airbus’s supply chain constraints amidst Boeing’s improvement, alongside sectoral divergences in industrials and automotive markets, facilitates more targeted responses and refined investment priorities moving forward.

Conclusion