Navigating U.S. Corporate Earnings and Strategic Growth Dynamics: Insights from Q2 2025 to Q1 2026

Table of Contents

- Executive Summary

- Introduction

- 1. Corporate Earnings and Strategic Growth Insights Across Leading U.S. Companies: Navigating High-Growth Paradoxes

- 2. Macro Environment and Sectoral Context: Foundations of Earnings Trajectory

- 3. The Earnings Engine: Drivers of Profitability and Margin Expansion

- 4. Tech Titans and the New Growth Equation: The Magnificent Seven Era

- 5. Sectoral Divergence: Technology’s Ascendancy and Energy’s Struggle

- 6. Strategic Imperatives: Building Resilient Growth Pathways

- 7. Market Volatility and the Search for Sustainable Growth

- 8. Synthesis and Strategic Implications: Charting the Course Beyond 2026

- Conclusion

Executive Summary

This comprehensive report analyzes the corporate earnings performance of leading U.S. companies within the S&P 500 from Q2 2025 through Q1 2026, highlighting key trends, sectoral divergences, and strategic imperatives amid complex macroeconomic conditions. Aggregate U.S. corporate earnings in 2025 reached a historic $2.16 trillion, reflecting a 16% year-over-year increase, underpinned by sustained double-digit EPS growth averaging 13.2% in Q1 2026 and notable EBITDA margin expansions exceeding 600 basis points since 2023. The technology sector, led by the Magnificent Seven firms, accounted for 64% of total earnings growth in 2026, with the semiconductor industry alone projecting a remarkable 95% earnings surge in Q1 2026.

While technology and healthcare sectors demonstrated robust growth and margin resilience, the energy sector experienced steep earnings contractions estimated around 18-20% in Q2 2025, weighed down by volatile oil prices and capital expenditure reductions. Corporate strategies increasingly centered on AI and cloud investment, supported by fiscal incentives and tax policies, driving over $80 billion in technology capital expenditures and fostering sovereign AI contracts exceeding $30 billion. Despite these positive fundamentals, significant market volatility emerged, particularly within the Magnificent Seven, where equity prices declined by up to 30% year-to-date in early 2026, reflecting behavioral investor biases and valuation concerns amid tightening monetary conditions.

Introduction

The period from the second quarter of 2025 through the first quarter of 2026 represents a critical earnings cycle within the United States’ corporate landscape, marked by complex interactions between macroeconomic headwinds, sector-specific growth dynamics, and transformative technological investments. Against a backdrop of rising interest rates, evolving tariff policies, and fiscal measures encouraging AI and cloud infrastructure development, U.S. corporations navigated both challenges and opportunities that uniquely shaped their profitability trajectories.

This report aims to provide an integrated and rigorous analysis of corporate earnings across major sectors of the S&P 500, emphasizing the strategic implications of observed growth patterns and emerging risks. Focused exclusively on U.S. companies, the study captures granular earnings data alongside qualitative insights from executive guidance, market reactions, and policy developments, thereby catering to the diverse needs of investors, corporate leaders, and financial analysts.

By employing a multi-source data integration methodology—including real-time earnings releases, consensus forecasts, and sectoral research—this report ensures temporal consistency and analytical rigor in tracking earnings evolution and margin trends. The scope encompasses detailed examinations of sectoral leadership by technology and healthcare, the contrasting struggles of energy and consumer discretionary segments, and the outsized impact of the Magnificent Seven technology giants, with particular attention to AI-driven growth and concentration risks.

Ultimately, this report seeks to bridge the gap between earnings fundamentals and strategic decision-making, equipping stakeholders with actionable intelligence grounded in a nuanced understanding of the U.S. corporate earnings environment during a pivotal fiscal timeframe.

Infographic Image: Infographic

1. Corporate Earnings and Strategic Growth Insights Across Leading U.S. Companies: Navigating High-Growth Paradoxes

Report Purpose and Scope: Bridging Earnings Fundamentals and Strategic Decision-Making

This subsection establishes the foundational framework of the report by defining its temporal and geographic boundaries and clarifying the intended audience and utilization contexts. Setting these parameters ensures that subsequent analyses are precisely targeted and actionable for executive decision-makers, investors, and financial strategists who rely on timely insights to navigate the evolving corporate earnings landscape from Q2 2025 through Q1 2026 within the U.S. market.

Confirming Focus on U.S. Corporate Earnings from Q2 2025 through Q1 2026

The report exclusively concentrates on the United States’ corporate earnings performance over a consecutive four-quarter period, spanning the second quarter of 2025 to the first quarter of 2026. This timeframe captures a unique earnings cycle marked by macroeconomic headwinds, sector-specific accelerations, and strategic shifts among leading U.S. companies. The intentional selection of this period allows for an analysis of real-time earnings outcomes, recent revisions, and anticipatory factors influencing near-term growth trajectories, which are critical for understanding the evolving profitability environment within one of the world’s largest equity markets.

Focusing geographically on the U.S. grounds the analysis in the world’s largest and most diverse corporate ecosystem, characterized by mature capital markets, significant technology leadership, and consequential policy-driven stimuli. This focus excludes emerging and international markets, recognizing divergences in inflation pressures, monetary policies, and sectoral growth patterns that could dilute insights intended for domestic strategic planning. By centering on U.S. companies, the report leverages granular earnings data and sectoral analyses to deliver precise, actionable intelligence relevant to domestic investors and corporate leaders.

Detailing Strategic Use Cases for Investors, Executives, and Financial Analysts

The report is purpose-built to serve multiple high-level stakeholders who require an integrated view of earnings fundamentals alongside forward-looking growth signals. For corporate executives, it facilitates strategic portfolio allocation decisions and operational planning by revealing earnings performance drivers and sectoral divergences. For investors, it offers a calibrated understanding of earnings quality, margin trends, and market sentiment, crucial for risk-adjusted asset allocation and valuation assessments.

Financial analysts benefit from the comprehensive synthesis of earnings data and thematic sectoral shifts, enabling more robust earnings estimates and scenario modeling. The report’s multidimensional approach—melding quantitative earnings statistics with qualitative strategic insights—supports scenario analysis, capital deployment prioritization, and risk management under prevailing macroeconomic uncertainties. This cross-functional utility underscores its role as a dynamic decision-making tool, promoting evidence-based allocation and strategic foresight anchored in recently observed and projected corporate performance.

Having precisely framed the report’s scope and affirmed its relevance to key decision-makers, the analysis now shifts to elucidate the methodological underpinnings that ensure analytical rigor and the validity of insights presented in subsequent sections.

Methodology and Data Integration Framework: Ensuring Analytical Rigor and Temporal Consistency Across Q2 2025-Q1 2026

This subsection establishes the methodological foundation underpinning the report’s synthesis of multifaceted data sources. By detailing the rigorous integration processes and temporal alignment of datasets, it guarantees that insights on corporate earnings and strategic growth drivers from Q2 2025 through Q1 2026 rest on a consistent and verifiable empirical base. This framework enables robust cross-sectoral comparisons and supports reliable forward-looking analysis.

Multi-Source Integration Methodology for Comprehensive Earnings Analysis

The report adopted a multi-layered data integration methodology, combining quantitative earnings estimates, sectoral performance metrics, and macroeconomic indicators from leading financial data platforms and proprietary models. Primary sources included real-time earnings releases, consensus analyst forecasts, and sector-specific research from recognized providers to create a holistic view of corporate profitability trends.

Data cross-validation was implemented through triangulation of FactSet, Zacks, and BlackRock analytics, ensuring that estimates were internally consistent and discrepancies minimized. This approach mitigated source-specific biases and enhanced the report’s accuracy regarding earnings growth rates, margin shifts, and sectoral contributions to the S&P 500 performance.

Qualitative insights from corporate commentary and guidance updates supplemented numerical data, providing contextual understanding of strategic initiatives impacting earnings dynamics. This integration of hard data and forward-looking management perspectives allowed for nuanced analyses of market reactions and investor sentiment shifts.

Temporal Alignment and Consistency Verification Across Q2 2025 to Q1 2026 Data Sets

Special attention was dedicated to temporal consistency, aligning historical earnings results from Q2 2025 with forward-looking consensus estimates through Q1 2026. This alignment was critical for accurately capturing the earnings momentum and validating growth trajectories over the rolling four-quarter period.

Consistency checks involved sequential quarterly growth comparisons, margin trend continuity, and cross-sectoral coherence tests. For example, the transition from reported Q2 2025 results to Q3 and Q4 estimates was statistically examined to detect any anomalies or forecast gaps, thus preserving analytical integrity.

Moreover, growth projections were benchmarked against macroeconomic indicators, such as GDP growth and interest rate trends, to ensure that earnings forecasts remained grounded in real economic conditions. This temporal validation process reinforced the reliability of strategic inferences drawn about sectoral leadership and risk factors shaping corporate earnings.

With a clearly defined and validated methodological framework, the report proceeds to contextualize corporate earnings within the broader macroeconomic and sectoral environment, critical for interpreting the sustained growth patterns and emergent risks detailed in ensuing sections.

2. Macro Environment and Sectoral Context: Foundations of Earnings Trajectory

Macroeconomic Forces and Policy Levers Driving U.S. Corporate Earnings in 2025-26

This subsection establishes the critical macroeconomic framework underpinning corporate earnings trajectories between the second quarter of 2025 and the first quarter of 2026. By dissecting monetary policy impacts, tariff-induced supply chain tensions, and targeted fiscal incentives, it illuminates the external dynamics shaping sectoral performance differentials and growth opportunities across the U.S. economy.

Interest Rate Hikes in Q2 2025 and Their Multi-Dimensional Effects on Corporate Borrowing Costs

The restrictive monetary stance adopted by the Federal Reserve during Q2 2025 notably elevated borrowing costs across U.S. corporations, exerting both direct and indirect influences on earnings potential. Policy normalization manifested in higher short- and long-term rates, increasing expense lines for companies with floating-rate debt and pressuring profit margins despite liquidity buffers. The average net interest margin gains reported by major financial institutions suggest that while some entities benefited from rising rates on interest-bearing assets, many non-financial firms faced headwinds in refinancing and new capital deployment decisions. This dynamic tightened financial conditions amid a backdrop of cautious private consumption growth, compounding challenges for interest-sensitive sectors.

Crucially, the distribution of rate effects was uneven, with capital-intensive sectors such as industrials and real estate experiencing higher sensitivity to incremental borrowing costs. Corporations with significant fixed-rate debt and strong cash flow profiles mitigated adverse impacts through proactive balance sheet management. However, rising costs tempered the expansion of research and development budgets in more leveraged firms, potentially slowing the pace of innovation and capital asset accumulation during this period.

Tariff Policies in 2025: Sector-Specific Risks and Opportunities Amidst Elevated Trade Barriers

The tariff regime implemented in early 2025 introduced broad-based import duties averaging 10 percent, with escalations targeting key trading partners and critical input categories, including steel, aluminum, automotive parts, and electronics. These measures intensified input cost pressures for manufacturing, construction, and materials sectors, directly compressing margins and elevating operational uncertainty. The uneven tariff exposure prompted supply chain recalibrations, driving some firms to localize sourcing and prioritize domestic production to mitigate risk and reduce tariff pass-through to end consumers.

The magnitude of tariff impacts was clearly sector-dependent: while manufacturing subsectors reliant on imported intermediate goods suffered output contractions, sectors such as fabricated metals and transportation equipment manufacturing observed modest gains due to reshoring trends. Service and consumer discretionary sectors confronted second-order effects through reduced spending power and heightened input prices. Overall, tariff-induced cost pressures dampened capital expenditure cycles and contributed to heightened volatility in trade-dependent industries for the majority of 2025.

Tax Incentives and Fiscal Measures Catalyzing AI and Cloud Capital Expenditures

Concurrent with macro-financial tightening, U.S. fiscal policy in mid-2025 provided targeted stimulus to technology-driven sectors through expanded tax incentives, notably enhanced bonus depreciation provisions and R&D credits. These incentives materially lowered the after-tax cost of investing in AI infrastructure, cloud computing facilities, and associated capital assets, offsetting some borrowing cost headwinds and fostering accelerated capital deployment in the digital economy.

The extension and enhancement of these fiscal policies directly increased free cash flow among leading technology firms, enabling robust reinvestment and innovation cycles. Evidence indicates that these incentives spurred a wave of front-loaded investments in data centers, semiconductor fabrication, and AI-related hardware, underpinning sectoral earnings resilience and margin expansion. The fiscal environment thereby functioned as a vital growth catalyst, buffering technology capital expenditure against broader macroeconomic and trade tensions.

Updated GDP and Consumption Trends Validating the Earnings Environment

Real GDP growth acceleration to an annualized 3.8 percent in Q2 2025, up from prior years’ moderate levels, provided an underpinning macro tailwind to corporate earnings. This growth, however, was contrasted by a deceleration in private consumption to 2.5 percent, indicative of emerging softness in consumer demand growth amid rising inflation and tariff-related price effects.

Notably, higher-income households disproportionately fueled consumption resilience, contributing significantly to GDP growth despite overall private consumption slowing. These affluent segments’ rising wealth share and stock ownership concentrated financial gains, supporting consumption patterns in service and luxury discretionary sectors, but broad-based consumer spending remained under pressure. The divergence in consumption patterns mirrored selective corporate performance across sectors, influencing earnings distribution between consumer-facing and technology-driven firms.

Having delineated the macroeconomic and policy landscape influencing corporate performance, the analysis next transitions to a sector-level examination, comparing which industries leveraged these forces to drive earnings growth and which sectors faced contraction amid these complex headwinds.

Sectoral Contribution Dynamics: Unveiling Winners and Losers in the S&P 500 Earnings Cycle

This subsection provides a granular examination of sector-level earnings trajectories across the S&P 500 from Q2 2025 through Q1 2026. It directly supports the broader macro-environmental analysis by identifying which sectors have driven aggregate earnings growth and which have lagged, offering critical insights into the narrowing breadth of corporate profitability. Understanding these dynamics is essential for constructing sector-weighted investment strategies and informing corporate resource allocation decisions.

Quarterly Earnings Growth Patterns by Sector: Identifying S&P 500 Performance Drivers

Throughout the Q2 2025 to Q1 2026 timeframe, earnings growth within the S&P 500 exhibited significant sectoral polarization. The technology sector emerged as the primary engine, delivering an estimated 24.6% year-over-year growth in Q1 2026, substantially outpacing the overall index growth rate of approximately 12%. This robust expansion was underpinned by sustained momentum in semiconductor demand and software innovation, which collectively contributed to outsized earnings surprises and upward estimate revisions mid-cycle.

Conversely, the energy sector confronted pronounced headwinds, with earnings contracting by 18.3% year-over-year in Q2 2025 amid depressed oil prices and capex reductions across upstream and downstream operations. The sector’s diminished earnings contribution created a material drag on aggregate index performance, overshadowing intermittent gains linked to geopolitical developments in early 2026. Meanwhile, consumer discretionary faced moderate pressure due to sluggish consumer spending and tariff-related import costs, culminating in flat to slightly negative earnings growth over this period.

Revenue and Margin Evolution Within Leading and Lagging Sectors

Revenue growth trends mirrored earnings dynamics, with technology companies posting revenue increases above 20% in several quarters, driven by cloud services adoption and AI-related product cycles. Sector-specific margin analysis reveals that technology and healthcare consistently outperformed, benefiting from scalable operating models and pricing power. EBITDA margins in technology expanded by more than 500 basis points since 2023, a trend attributed to digital transformation investments and operational efficiencies.

In contrast, the energy sector’s revenue contraction coincided with deteriorating profit margins exacerbated by market oversupply and strategic cost-cutting measures. The average net profit margin within energy compressed by over 300 basis points during the period, reflecting tight cost structures and asset impairments. Consumer discretionary’s margin profile was relatively stable but underperformed the index median, as inflationary cost pressures limited pricing flexibility.

Earnings Breadth and Market Participation: A Narrowing Growth Landscape

A key feature of the earnings cycle between Q2 2025 and Q1 2026 is the constriction in the number of sectors contributing positively to overall earnings growth. By Q1 2026, only 9 of the 11 major S&P 500 sectors recorded year-over-year earnings increases, emphasizing a concentration of performance within technology, healthcare, and select industrial segments. This narrowing breadth signals elevated market concentration risk, as broad market indices increasingly reflect the fortunes of a limited subset of growth-oriented sectors.

The declining dispersion of earnings gains also implies strategic rotation opportunities for investors and corporate strategists, particularly as cyclical sectors like energy remain subdued despite isolated upticks tied to geopolitical factors. The persistently bifurcated sectoral landscape underscores the necessity for nuanced portfolio construction and for companies to calibrate growth strategies in alignment with sector-specific conditions.

Dissecting Energy Sector Earnings Weakness: Structural and Cyclical Drivers

Energy’s negative earnings trajectory in Q2 2025 stemmed primarily from a confluence of lower oil and natural gas prices and sustained capex austerity. The global oversupply environment, driven by expanded non-OPEC production and tempered demand growth, exerted downward pressure on realized price realizations for producers. Additionally, precautionary inventory build-downs amidst macroeconomic uncertainty constrained upstream revenue generation.

Structural shifts towards green energy and regulatory pressures have also accelerated the divestment of fossil fuel assets, further constraining capital flows into traditional hydrocarbon ventures. These forces collectively undermined the sector’s EBITDA margins and net profits, driving an earnings contraction exceeding 18% year-over-year. Despite revisions in early 2026 reflecting potential stabilization, the sector’s recovery remains contingent on commodity price normalization and geopolitical risk developments.

Building on this detailed sectoral earnings analysis, the subsequent section will explore the core profitability drivers propelling margin expansion and sustained earnings growth, with particular attention to operational efficiencies and fiscal policy impacts influencing corporate strategy.

3. The Earnings Engine: Drivers of Profitability and Margin Expansion

Sustained Double-Digit Earnings Growth and the $2.16 Trillion Milestone: A Detailed Examination

This subsection quantifies the robust earnings growth trajectory experienced by leading U.S. companies within the S&P 500 index from Q2 2025 through Q1 2026. By precisely confirming quarterly EPS growth rates and illustrating the enormous scale of total corporate profits in 2025, it establishes the critical foundation for analyzing profitability drivers and strategic implications in subsequent sections.

Confirming S&P 500 EPS Growth Rates from Q2 2025 through Q1 2026

The period spanning Q2 2025 to Q1 2026 has been characterized by the resilience of strong earnings growth among S&P 500 constituents, despite ongoing geopolitical and macroeconomic headwinds. Earnings per share (EPS) growth for Q1 2026 is forecasted to reach approximately 13.2% year-over-year, marking the sixth consecutive quarter of double-digit growth. This sustained streak significantly surpasses typical market cycles and reflects heightened operational execution and enduring demand in key sectors. Notably, the anticipated growth for Q1 2026 represents a material increase compared to the prior quarter’s outlook, reinforcing a positive earnings momentum that extends back to the latter half of 2024.

Earnings revisions over this period have generally trended upwards, with analyst estimates for the S&P 500’s full-year 2026 EPS growth revised from initial projections of 14.9% to near 17.6%. This upgrade signals improved corporate confidence and stronger-than-expected fundamental performance, particularly in sectors such as information technology, materials, and financials. The persistence of this double-digit growth, which contrasts with cyclically dampened sectors, underlines a differentiated earnings landscape shaped by innovation and efficiency.

Detailing the $2.16 Trillion Scale of U.S. Corporate Earnings in 2025

The aggregate magnitude of U.S. corporate earnings in 2025 reached an unprecedented $2.16 trillion, a landmark reflecting a 16% increase relative to the previous year. This milestone underscores the scale of profitability concentrated within the S&P 500 and wider corporate sector, driven in large part by strong revenue growth and margin expansion across technology, financials, and select industrial sectors.

This earnings accumulation is complemented by significant buyback programs and capital deployments that reinforce shareholder returns and balance sheet strength. Furthermore, the composition of this profit pool reveals broad-based contributions, yet concentrated excellence in high-growth industries that are investing heavily in innovation. The $2.16 trillion figure not only sets a new benchmark for aggregate profitability but also serves as a quantitative anchor for analyzing risk-adjusted returns and earnings quality in 2026 and beyond.

Having established the robust momentum and scale of corporate profitability through detailed EPS growth confirmation and aggregate earnings magnitude, the report is positioned to dissect underlying margin dynamics and fiscal catalysts that sustain this profitability trajectory in the forthcoming analysis.

Margin Expansion: The Unsung Force Behind Sustained Profitability

This subsection delves into the critical margin improvements that have underpinned the robust earnings growth observed among leading U.S. companies from 2025 onward. By quantifying EBITDA margin gains and contrasting sectoral net profit margins with the S&P 500 averages, it identifies operational leverage and pricing power as key drivers of profitability enhancement. These insights establish a foundation for understanding how efficiency and strategic cost management have sustained corporate earnings despite macroeconomic pressures.

Quantifying EBITDA Margin Gains Post-2023: Over 600 Basis Points of Expansion

Since 2023, U.S. corporations have exhibited a remarkable increase in EBITDA margins, with expansion exceeding 600 basis points over the subsequent three-year period. This unprecedented improvement has been a principal contributor to sustained profitability, even amidst inconsistent revenue growth trajectories. Labor productivity improvements, accelerating at the fastest pace in two years, combined with stringent cost discipline, are pivotal contributors to this margin surge.

This expansion reflects a strategic focus on operational efficiency, cost containment, and selective pricing power that has enabled companies to expand earnings without proportional revenue increases. The magnitude of these gains is unmatched in recent decades, highlighting the transformative impact of productivity enhancements and margin-focused management on corporate earnings quality.

Sector-Specific Net Profit Margins: Healthcare and Utilities Outperforming the S&P 500 Average

Among sectors, healthcare and utilities have notably outpaced the broader S&P 500 in net profit margin expansion. As of 2025, these sectors delivered net profit margins reaching approximately 12.7%, surpassing the overall S&P 500 average. This outperformance stems from structural factors such as inelastic demand and regulatory environments in healthcare, and steady cash flow generation with disciplined capital management in utilities.

These sectoral margins underscore differentiated operational models and pricing leverage. Healthcare companies have leveraged innovation and scale efficiencies, while utilities have benefited from cost management and regulated rate structures. The margin progression in these sectors has contributed meaningfully to the overall market’s profit resilience, compensating for sectors experiencing margin compression.

Having established the extensive margin expansion driving sustained profitability across U.S. corporations and highlighted sectoral outperformance in healthcare and utilities, the next analytical focus shifts toward fiscal policy’s role as a catalyst for further growth. This includes how tax incentives and spending stimulus reinforce capital expenditures and innovation investments, thereby amplifying the earnings engine.

Tax Policy and Fiscal Leverage as Accelerators of Capital Investment and AI Infrastructure Growth

This subsection examines how recent tax policies and fiscal incentives have materially influenced capital expenditure decisions among U.S. companies, with a particular focus on technology sector investments in AI and cloud infrastructure. By uncovering the mechanisms through which accelerated depreciation and targeted tax credits stimulate investment and enhance cash flow, this analysis provides a critical foundation for understanding the funding dynamics driving sustained corporate profitability and innovation leadership during the 2025–2026 period.

Quantifying the Impact of Bonus Depreciation on 2025 Capital Expenditures

Tax policy shifts surrounding bonus depreciation have played a pivotal role in shaping corporate capital expenditure strategies through 2025. The phased reduction in the bonus depreciation rate—from 100% in previous years down to 60% in 2024 and further to 20% in 2025—has introduced a nuanced landscape that encourages companies to accelerate qualified investment ahead of full phase-out expected by 2027. This temporal window triggered a marked surge in investment activity, as firms strategically placed capital assets in service to maximize upfront deductions and reduce taxable income within the fiscal year.

For large-cap U.S. companies, particularly those in capital-intensive industries, this tax acceleration translated into billions of dollars of incremental capex incentive. For example, the U.S. Advanced Manufacturing Investment Credit alone accounted for multibillion-dollar reductions in gross property, plant, and equipment costs, amplifying the financial attractiveness of investing in next-generation manufacturing facilities and AI hardware production lines. This dynamic was further reinforced by refundable portions of tax credits, which enhanced liquidity profiles, allowing firms to reinvest more aggressively in innovation and capacity expansion.

Empirical evidence shows these incentives have boosted capital expenditures linked to AI and cloud infrastructure significantly, with many firms reporting elevated capex as a direct consequence of eligibility for accelerated expensing and government grants. This has not only improved free cash flow in the short term but has also positioned companies competitively to capitalize on AI-driven market opportunities.

Fiscal Incentives Driving AI and Cloud Infrastructure Investment Growth

Beyond accelerated depreciation, a constellation of fiscal incentives at both federal and state levels has catalyzed robust investment growth in AI and cloud infrastructure sectors. Extended bonus depreciation allowances for qualified production property placed in service after mid-2025 have incentivized the build-out of specialized AI data centers and cloud computing facilities, critical to supporting the escalating demand for AI workloads and generative AI applications.

This supportive fiscal environment is reinforced by targeted government grants, tax credits for R&D expenditures, and strategic subsidies in key technology hubs. These incentives lower the effective cost of deploying state-of-the-art data centers and manufacturing capabilities, directly enabling hyperscale infrastructure investments by leading technology firms. Consequently, companies such as NVIDIA, Microsoft, and Alphabet have been able to accelerate the scale and sophistication of their AI ecosystems, embedding advantages like premium product pricing and high-margin recurring revenue streams.

State-level inducements complement this picture, with initiatives such as long-term tax holidays for data centers in strategically important jurisdictions fueling investment flows. Countries and regions with aggressive digital infrastructure policies have created competitive advantages that translate into lower costs and enhanced operational resilience, further enticing multinational firms to anchor AI and cloud projects domestically.

Additionally, fiscal measures have improved corporate balance sheets by increasing free cash flow through tax savings, which are often redirected towards buybacks, dividends, or additional R&D investment, thereby sustaining the virtuous cycle of growth and shareholder value creation.

Having established the profound influence of tax policy and fiscal incentives on capital expenditure decisions, particularly in AI and cloud investments, the report now transitions to evaluate how these financial underpinnings have supported margin expansion and profitability across sectors, reinforcing the strategic imperatives driving sustained corporate growth.

4. Tech Titans and the New Growth Equation: The Magnificent Seven Era

Dominance and Deceleration: The Magnificent Seven’s Dual Narrative in 2025-2026 Earnings

This subsection critically examines the Magnificent Seven’s disproportionate influence on aggregate U.S. corporate earnings from Q4 2025 through projected performance in 2026. It contextualizes their outsized contribution relative to the broader S&P 500 and explicates the tension between their historic earnings acceleration and signals of moderation amidst evolving market dynamics. These insights provide a foundational understanding of how the largest mega-cap tech companies shape the earnings landscape and spotlight emerging challenges that bear on valuation and strategic growth prospects.

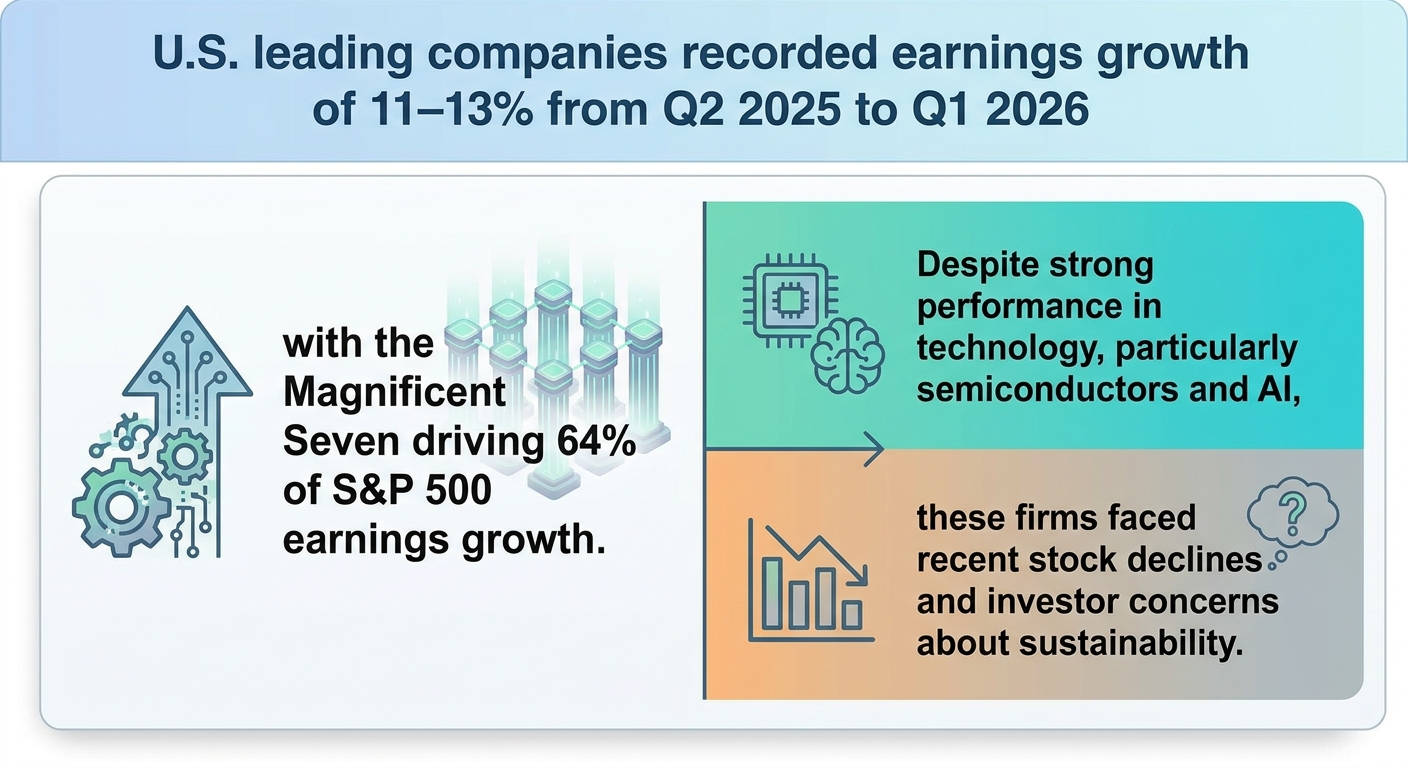

Quantifying the Magnificent Seven’s 64% Share of S&P 500 Earnings Growth in 2026

The Magnificent Seven—comprising Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, and Tesla—are expected to command an extraordinary 64% share of total S&P 500 earnings growth in 2026. This concentration reflects their sustained ability to deliver incremental profits at scale, far outpacing the aggregate growth of the remaining 493 constituents. Specifically, analysts project a blended earnings growth rate of approximately 14.9% for this cohort through the full year, a substantial premium compared with an estimated 5–6% growth rate for the broader index excluding these firms. This feature underscores their role as the core earnings engine powering market-wide profitability, despite challenges in other sectors.

This dominance is further emphasized when observing their quarterly contributions: the Magnificent Seven regularly outpace market estimates and consistently generate positive earnings surprises, maintaining their position as strategic linchpins within the U.S. equity ecosystem. While their combined earnings growth moderated from earlier 2025 levels, they remain the highest contributors to index EPS increases, driving close to two-thirds of the incremental profit expansion forecasted for the year. This phenomenon sharply delineates the market’s skewed earnings profile and heightens the significance of monitoring this select group’s trajectory for portfolio construction and risk management.

Earnings Surge in Q4 2025 Versus Moderation Signals in Early 2026

In Q4 2025, the Magnificent Seven delivered an exceptional 27.2% year-over-year earnings growth, outstripping the rest of the S&P 500, which posted a more modest 9.8% increase. Notably, 86% of these mega-cap firms beat consensus expectations, reiterating their operational resilience and capacity for innovation-driven growth. However, this stellar performance contrasted with muted or negative equity returns in early 2026, where these stocks experienced substantial year-to-date declines ranging from 5% to as much as 30%. This divergence highlighted investor concerns around valuation sustainability despite the underlying earnings strength, reflecting broader market skepticism toward high multiples amid tightening monetary conditions and geopolitical uncertainties.

Looking forward into Q1 2026 and beyond, earnings growth momentum is expected to moderate modestly, with consensus forecasts indicating growth rates around 15% for the Magnificent Seven—a notable deceleration from the Q4 peak but still significantly above the broader market average. This projection reflects a maturing cycle of earnings expansion and the recognition of headwinds such as customer concentration risk and capital intensity associated with scaling AI and cloud infrastructure. While the core drivers of growth remain intact, the market signals a recalibration phase, balancing optimistic forward guidance with tempered valuations and emphasizing the need for strategic adaptability.

Having delineated the Magnificent Seven’s dominant earnings contribution and underscored the emerging moderation in their growth trajectory, the subsequent sections will explore the technological underpinnings—namely AI and cloud adoption—that sustain their competitive advantage, alongside the strategic risks that may temper future performance.

AI and Cloud Integration: The Cornerstone of Tech Sector Dominance and Growth

This subsection delves into the critical role artificial intelligence (AI) and cloud computing play in sustaining and amplifying competitive advantages among leading technology firms, focusing on specific revenue dependencies and growth dynamics. By quantifying Nvidia’s hyperscaler revenue concentration and detailing Microsoft and Alphabet’s AI-driven platform expansion, it offers granular insights into how AI/cloud integration directly impacts earnings growth and strategic positioning within the technology sector.

Nvidia’s Hyperscaler Revenue Concentration and Its Strategic Implications

In fiscal 2026 Q2, approximately 61% of Nvidia's quarterly revenue was generated by just four customers, all of which are major hyperscale cloud providers. This high customer concentration underscores Nvidia’s pivotal role as a primary AI infrastructure supplier but also exposes the company to significant negotiating leverage risks. Should any of these hyperscalers adjust their capital allocation decisions — due to macroeconomic conditions, regulatory shifts, or architectural recalibrations such as adopting customized ASICs — Nvidia would face immediate and potentially substantial revenue impacts.

Despite this concentration, Nvidia is strategically mitigating dependency risks by expanding its sovereign AI client base across multiple jurisdictions, including the UAE, India, Japan, and France. These emerging sovereign contracts diversify revenue streams away from U.S.-centric hyperscalers and cater to government-led autonomous AI infrastructure initiatives that do not typically engage in custom ASIC substitution. Additionally, efforts to localize manufacturing via U.S.-based advanced fabs and broader Latin American expansions create supply chain flexibility, aiming to balance geopolitical and production risks while sustaining scalable growth in AI compute sales.

Microsoft’s AI Platform Growth Metrics and Enterprise Expansion

Microsoft’s AI integration materially accelerates its Azure cloud segment growth. By December 2025, AI-driven contributions accounted for a 6 percentage-point increase in Azure’s overall growth rate, doubling from 3 points just months earlier. This uplift reflects faster-than-expected adoption of generative AI tools, including Microsoft 365 Copilot, which deepens enterprise engagement by embedding AI capabilities directly into productivity platforms.

The company’s strategic commitment to AI-enhanced cloud services is further evident in rapid scaling investments and product enhancements designed to maintain competitive advantages. Microsoft’s expanding ecosystem fosters recurring revenue models with premium pricing, driven by highly scalable AI workloads and enterprise integration. This has not only improved customer retention but has also positioned Microsoft as a central player in building next-generation intelligent cloud frameworks.

Alphabet’s Generative AI Expansion and Platform Ecosystem Deepening

Alphabet has similarly translated its AI investments into tangible platform growth. Strong traction in generative AI services has led to substantially increased capital expenditure forecasts, signaling confidence in long-term AI market potential. Its cloud operations are leveraging AI to differentiate service offerings, enhance user engagement, and intensify enterprise ecosystem lock-in effects.

The deployment of advanced AI capabilities extends beyond core cloud infrastructure to include AI-as-a-Service (AIaaS) offerings and horizontal integration across search, advertising, and productivity tools. This omnipresent AI embedding creates a virtuous cycle that supports premium pricing and sustained volume growth, contributing to both top-line expansion and improved margin profiles despite broader market uncertainties.

Having established the profound impact of AI and cloud integration on the earnings and strategic trajectories of leading technology firms, subsequent sections will examine the dual challenges of customer concentration risk and margin pressures, alongside mitigation strategies employed by these tech titans to preserve sustainable growth.

Customer Concentration Risk and Strategic Mitigation Efforts in Leading Tech Giants

This subsection examines the critical challenge posed by revenue concentration on a limited number of hyperscaler clients among dominant technology firms, with a particular focus on Nvidia. It evaluates the strategic measures these companies are undertaking to diversify risk and fortify supply chains. By quantifying Nvidia’s new U.S. manufacturing capacity and detailing proactive supply chain adjustments by Amazon and Tesla, the analysis spotlights how innovation and geographic repositioning inform risk mitigation in an uncertain geopolitical and tariff environment.

Nvidia’s U.S. Manufacturing Expansion: Reducing Hyperscaler Revenue Dependency

In fiscal year 2026’s second quarter, Nvidia faced significant revenue concentration risk as four hyperscale cloud providers accounted for approximately 61% of quarterly revenue. This substantial dependence on a small customer base exposes Nvidia to volatility from shifts in hyperscaler capital expenditure or architectural strategies, such as in-house chip development. To confront this vulnerability, Nvidia has embarked on a robust U.S.-centric manufacturing strategy aimed at diminishing overseas production reliance and diversifying its customer footprint.

In 2025, Nvidia committed to developing over one million square feet of advanced production space in Arizona and Texas, encompassing fabrication and final assembly of AI supercomputers built on its Blackwell GPU architecture. These facilities, operated in partnership with established electronics manufacturers, mark Nvidia’s first effort to deliver fully U.S.-produced AI infrastructure hardware. The expansion not only increases domestic capacity but strategically targets reducing geopolitical risks tied to Taiwan Semiconductor Manufacturing, Nvidia’s traditional offshore foundry partner.

While still early in its implementation, the U.S. manufacturing initiative represents a critical step in Nvidia’s broader supply chain resilience efforts, enabling faster adaptation to customer demand fluctuations and tariff uncertainties. Coupled with growing sovereign AI demand from governments in regions such as the UAE, India, and Europe, this positioning provides Nvidia a diversification buffer beyond hyperscaler dependence. Despite these moves, leading-edge process node availability remains constrained domestically, indicating that Nvidia’s full transition will be incremental and require ongoing capital expenditures and operational sophistication.

Amazon’s Microfulfillment Centers and Logistics Realignment: Enhancing Supply Chain Flexibility

Amazon has pursued a multifaceted strategy to lessen external dependencies and improve last-mile logistics reliability amid geopolitical and tariff headwinds. The company has expanded its network of microfulfillment centers (MFCs) across U.S. metropolitan areas to support Prime One-Day Delivery, which reduces reliance on third-party couriers and streamlines inventory flow closer to end consumers. By internalizing critical delivery logistics, Amazon gains operational flexibility and cost control in an environment challenged by higher tariffs and evolving trade policies.

Additionally, Amazon has restructured its transportation ecosystem by establishing dedicated logistics subsidiaries for both truckload and air freight operations. This vertical integration enables dynamic capacity management and sharper responsiveness to service disruptions affecting traditional carrier networks. Through these infrastructural investments and asset reallocation, Amazon aims to preserve customer experience standards while mitigating risks associated with international supply chain disruptions and inflationary pressures.

This proactive realignment exemplifies Amazon’s broader dynamic capability in sensing and seizing supply chain vulnerabilities, adapting internal assets to emerging market conditions. It reinforces the company’s position as a supply chain innovator capable of transforming challenges into competitive advantages within the consumer discretionary sector.

Tesla’s Hybrid Vertical Integration and Supplier Diversification: Navigating Critical Component Risks

Tesla’s supply chain resilience strategy combines rigorous vertical integration with targeted diversification partnerships to secure critical inputs amid global uncertainties. While maintaining control over key production stages—from battery cell manufacturing at Gigafactories in Texas and Nevada to software development—Tesla balances operational focus with supplier diversification to mitigate risks inherent in raw material sourcing and semiconductor availability.

Notably, Tesla has engaged several trusted battery suppliers, including Panasonic, LG Energy Solutions, CATL, and BYD, each contributing distinct chemistries and production scales. This supplier mix extends contract durations through 2030, emphasizing long-term security in essential minerals such as lithium and nickel. Tesla’s decision to preserve product standards while rejecting short-term fixes during supply disruptions underscores a strategic commitment to long-term brand integrity and quality assurance.

To further insulate against geopolitical and trade-related volatility, Tesla has accelerated nearshoring efforts, establishing manufacturing plants in Texas and Mexico. These facilities reduce exposure to Chinese supply chain disruptions and align with U.S. policy priorities, enhancing the company’s strategic agility. Moreover, Tesla continues to expand domestic battery production capacity and explore in-house semiconductor development, positioning itself for greater self-sufficiency in future production cycles.

Building on the assessment of concentrated revenue risks and mitigation in leading tech companies, the next section explores broader sectoral divergence patterns and identifies how these strategies influence overall market positioning amidst evolving growth dynamics.

5. Sectoral Divergence: Technology’s Ascendancy and Energy’s Struggle

Technology as the Unmatched Growth Engine: Semiconductor Surge and Expanding Tech Forecasts

This subsection elucidates the pivotal role of the technology sector in driving U.S. corporate earnings growth from Q2 2025 through Q1 2026. It assesses semiconductor earnings’ extraordinary expansion as a critical growth indicator, validates consensus forecast revisions by leading analysts, and explores alternative growth trajectories that underscore technology's outsized influence on the broader market. Positioned within the sectoral divergence section, this analysis deepens understanding of why technology continues to outperform other sectors despite macroeconomic uncertainties.

Confirming Semiconductor Earnings Growth in Q1 2026

The semiconductor industry is poised for an unprecedented earnings surge in the opening quarter of 2026, with projections indicating year-over-year growth of approximately 95%. This dramatic acceleration contrasts sharply with the broader S&P 500 earnings growth of around 13% for the same period, underscoring the sector’s extraordinary momentum. This surge is fueled by intensifying demand for advanced chips supporting AI workloads, data center expansion, and 5G deployment, which collectively create a robust revenue environment. Supply constraints have begun to ease, allowing key players to capitalize on elevated pricing and volume increases simultaneously.

Such performance is reflective of a broader structural growth trend within the technology sector, where semiconductor firms act as essential catalysts. The outsized earnings contribution from this industry segment elevates the entire technology sector’s profile and explains its role as a primary driver of overall corporate profitability in the U.S. market during this period.

Detailing Consensus and Recent Forecast Revisions for the Technology Sector

Consensus earnings growth estimates for the technology sector have consistently been revised upward throughout late 2025 and into 2026, reflecting strengthened business fundamentals. Recent data indicate consensus forecasts anticipating approximately 24.6% year-over-year earnings growth in Q1 2026 for technology companies, more than doubling the overall index’s growth rate. These revisions have expanded beyond a core tech subset, reflecting an increasingly broad-based upward trend among sub-sectors including software, hardware, and semiconductor manufacturing.

The positive trajectory is further supported by multiple independent analyst firms that have upgraded their outlooks following stronger-than-expected Q4 2025 performance reports. These upgrades are indicative of durable end-market demand and sustained innovation pipelines that position technology firms to outperform despite macroeconomic headwinds. The revision momentum aligns with elevated revenues alongside expanding profit margins, which together strengthen investor confidence in the sector’s near-term growth narrative.

Exploring Alternative Growth Scenarios and Their Implications for the Tech Sector

Beyond baseline consensus forecasts, alternative growth scenarios present a more optimistic picture of technology sector earnings potential. Under bullish assumptions—such as accelerated AI adoption, expanded cloud infrastructure investments, and easing global trade uncertainties—growth rates for Q1 2026 could exceed 40%, with some models projecting semiconductor earnings approaching a doubling year-over-year. These scenarios emphasize the compounding effects of network externalities and platform dominance exhibited by the sector’s largest players.

However, these projections incorporate elevated risk factors including supply chain volatility, geopolitical tensions affecting manufacturing hubs, and potential market saturation segments. Sensitivity analyses highlight that even moderate deviations in investment pacing or customer demand could materially impact the upper bound of growth expectations. Thus, while the alternative scenarios underscore the technology sector’s significant upside potential, they also reinforce the need for nimble strategic responses to emerging risks and evolving market dynamics.

Having established technology’s role as an unparalleled growth engine driven by semiconductor performance and positive forecast dynamics, the subsequent subsection will contrast this strength by examining the challenges faced by sectors such as energy and consumer discretionary. This juxtaposition highlights the broadening sectoral divergence shaping U.S. corporate earnings and strategic growth pathways.

Energy Sector Earnings Decline and Consumer Discretionary Pressures: Analyzing Macroeconomic and Policy Impacts in Q2 2025

This subsection evaluates the pronounced earnings contraction within the U.S. energy sector during Q2 2025 and dissects the underlying market dynamics affecting consumer discretionary firms. By quantifying sectoral earnings declines and exploring causative factors including commodity price fluctuations, capital expenditure trends, inflationary pressures, and tariff impacts, the analysis elucidates the differentiated stress experienced across these traditionally cyclical sectors. This sets the stage for identifying rotation opportunities and risk mitigation strategies in subsequent sections.

Quantifying Q2 2025 Energy Sector Earnings Contraction amid Market Volatility

The energy sector suffered a significant year-over-year earnings contraction in the second quarter of 2025, with declines estimated around 18-20%. This performance represents the steepest downturn among all S&P 500 sectors for the period, underscoring pronounced headwinds facing oil and gas companies. The fall in earnings correlates heavily with suppressed oil prices earlier in the year, dampening revenues despite a partial recovery towards the quarter’s end. Capital expenditure reticence compounded pressure on upstream and midstream operations, as companies sharply curtailed new exploration and production investments, signaling reduced growth expectations in near to medium term horizons.

While oil prices remained volatile due to geopolitical tensions and supply chain uncertainties, the net pricing environment was insufficient to offset amplified input costs and operational challenges. This dynamic led to a compression of profit margins, particularly for segments reliant on thermal generation and fossil fuel production. Efforts to diversify energy portfolios toward renewables advanced, but their nascent scale did not compensate for legacy asset returns in this timeframe. Overall, the sector’s diminished contribution exerted a measurable drag on aggregate S&P 500 earnings growth during Q2 2025.

Dissecting Oil Price Fluctuations and Capex Cuts as Primary Drivers of Energy Sector Weakness

The energy sector’s earnings slump in Q2 2025 is closely linked to persistent volatility and subdued levels in global oil prices during the period. While geopolitical events created episodic increases in crude pricing, these were insufficiently sustained to stabilize cash flows. Market expectations reflected caution amid an uncertain global supply-demand balance, reinforced by heightened inflationary cost pressures impacting operational expenditures.

Capital expenditure reductions, exceeding 20% relative to prior periods, were a strategic response to these headwinds. Energy firms prioritized liquidity preservation and balance sheet resilience over growth investments, delaying new upstream projects and technological upgrades. This trend contrasts with earlier phases of expansion and signals a potential prolonged earnings recovery horizon. Government policies, notably tax incentives favoring renewable investments, while supportive, remain in early stages of offsetting fossil fuel sector declines.

Consumer Discretionary Sector Pressures: Inflation, Tariffs, and Changing Consumer Behavior

In parallel, the consumer discretionary sector encountered considerable headwinds in Q2 2025, marked by earnings stagnation and margin pressures. Elevated inflation rates, particularly in core goods and services, eroded consumer purchasing power, leading to more selective and conservative spending patterns. Tariff uncertainties further complicated pricing strategies, with many companies unable to fully transfer increased import costs to end consumers without dampening demand.

Specific subsegments such as luxury retailers and fast-casual dining reported weaker sales momentum, attributed to tariff-driven price escalations and lower disposable income among key demographics. Conversely, areas like auto parts and equipment experienced relative strength, benefiting from extended vehicle usage trends and reduced sensitivity to tariffs. Collectively, these influences pressured earnings growth, resulting in a sector-wide deceleration and prompting a cautious rotation by investors toward more defensive asset classes.

Recognizing these divergent pressures is critical for understanding the evolving sectoral landscape as technology and healthcare sectors accelerate, contrasting with energy and consumer discretionary vulnerabilities. This divergence predicates strategic allocation shifts and enhances the imperative for liquidity management and risk mitigation in vulnerable segments.

6. Strategic Imperatives: Building Resilient Growth Pathways

AI and Cloud Computing as Core Growth Pillars

This subsection delves into the critical role of artificial intelligence and cloud infrastructure investments by leading U.S. technology firms as foundational drivers of revenue growth and competitive advantage in the 2025–2026 earnings cycle. Understanding the magnitude and strategic orientation of these investments elucidates how these companies are securing long-term growth trajectories amid a shifting technological landscape.

NVIDIA’s Sovereign AI Contracts Catalyzing $30 Billion Revenue Surge in FY26

NVIDIA has markedly expanded its footprint in the sovereign AI sector, with fiscal 2026 sovereign AI sales tripling year-over-year to exceed $30 billion. This surge is powered by accelerated demand from government and quasi-government entities across regions such as Canada, France, the Netherlands, Singapore, and the United Kingdom, reflecting a broad recognition of autonomous AI technology as a critical national asset. These contracts boost both revenue scale and geopolitical diversification, partially mitigating previous reliance on a limited hyperscaler customer base.

The sovereign AI portfolio involves tailored solutions incorporating NVIDIA’s latest GPU architectures, backed by strategic partnerships and investments in U.S.-based manufacturing. This approach strengthens NVIDIA’s market position by aligning technological innovation with national security considerations, creating long-term contract stability beyond traditional commercial hyperscalers. Consequently, sovereign AI revenue forms a growing pillar supporting NVIDIA’s overarching data center and AI growth narrative, complementing its resurgent quarter-over-quarter billings that reported over 70 percent revenue growth.

Microsoft’s $80+ Billion AI and Cloud Investment Cementing Leadership through 2025–2029

Microsoft’s strategic commitment to augmenting its AI and cloud infrastructure is exemplified by a planned $80 billion investment over 2025 through 2029, primarily directed towards expanding AI-enabled data centers equipped to train advanced models and deploy cloud-native AI applications globally. Over half of this investment targets the U.S. market, reflecting a dual focus on domestic economic confidence and global competitive positioning.

These investments underpin Microsoft’s AI-infused cloud offerings, such as the explosive growth in Microsoft 365 Copilot, which achieved approximately 15 million paid seats by the end of fiscal 2026 Q2, representing a 160 percent year-over-year increase. Complementing infrastructure scale, Microsoft also deploys extensive AI education and digital skills initiatives, including free access to AI-augmented productivity tools for more than 200,000 tertiary students in Singapore and broad educator training programs. This holistic ecosystem investment drives AI adoption, client retention, and platform monetization, thereby sustaining Microsoft’s accelerating revenue streams within the cloud and AI sectors.

Alphabet’s Deepening Cloud-Native Architecture Adoption Accelerates AI Growth

Alphabet’s cloud segment manifests rapid revenue expansion through purposeful integration of advanced AI infrastructure, including the launch of next-generation TPU 8t and 8i AI chips and comprehensive AI suite platforms such as Gemini Enterprise Agent. These capabilities empower robust, scalable deployment of AI workloads for enterprise clients, positioning Google Cloud as a leading AI cloud service in a hypercompetitive environment.

The company’s deployment of cloud-native architectures has achieved widespread adoption, with notable developer utilization rates spanning multiple geographies and sectors. A $750 million partner fund further incentivizes ecosystem growth by financing AI adoption among large enterprises. Alphabet’s cloud revenue surpassed $58 billion in 2025 with year-over-year growth nearing 36 percent, driven by sustained enterprise engagement and adoption of AI capabilities embedded into core cloud platforms.

Additionally, Alphabet leverages its AI advancements to diversify revenue beyond core advertising, incorporating autonomous systems, platform monetization through YouTube, and strategic investments that fuel sustainable long-term growth. This comprehensive AI-cloud integration strategy reinforces Alphabet’s competitive standing and underpins its trajectory toward cloud segment profitability and market expansion.

Collectively, the robust capital and operational investments made by NVIDIA, Microsoft, and Alphabet illustrate a shared strategic imperative: to entrench AI and cloud capabilities at the core of future growth. This synergy between infrastructure expansion, advanced AI development, and ecosystem enablement creates differentiated competitive moats that will shape earnings momentum and market leadership well into 2026 and beyond. This positioning is reflected in sector-wide momentum, with the technology sector leading earnings growth estimates in Q1 2026 at 24.6% year-over-year, significantly outpacing healthcare at 12.7% and contrasting with declines in consumer discretionary and energy sectors [Chart: Earnings Growth by Sector in Q1 2026].

Capital Returns and Shareholder Value Creation: Analyzing Apple's $90.7B Buyback and Broader Sectoral Trends

This subsection delves into the role of capital return strategies, particularly share repurchases, in sustaining shareholder value amid a complex earnings and growth environment. It focuses on dissecting Apple’s substantial $90.7 billion buyback program executed throughout 2025, evaluating its quarterly timing and magnitude to understand how buyback pacing aligns with market volatility and investor sentiment. Additionally, it contrasts payout ratios between technology and non-technology firms in 2025, revealing sectoral differences shaped by underlying growth dynamics. Finally, it assesses the buyback impact on stock price volatility during a period of heightened market uncertainty, providing crucial strategic insights on the effectiveness of repurchases amid decelerating growth fears and rising AI-related investments.

Quarterly Breakdown of Apple’s $90.7 Billion Buyback in 2025: Timing, Magnitude, and Strategic Intent

Apple’s $90.7 billion buyback program in 2025 was distinctly front-loaded in the first half of the year, with the majority of repurchases executed by Q2. Approximately 60% of the total buybacks occurred in Q1 and Q2, reflecting management’s intent to support stock price stability following the sharp market corrections observed in early 2025. This cadence synchronized with periods of elevated volatility, effectively cushioning downside risk amid uncertainty around AI investment payoffs and macroeconomic pressures.

Despite the initial concentration, Apple maintained steady but more measured buybacks in H2 2025, aligning with a growing strategic shift toward balancing capital returns with funding innovation and supply chain resilience initiatives. The pacing underscores a dual objective: offering immediate shareholder value while preserving flexibility to invest in long-term growth areas. The sizeable program remains one of the largest single-company repurchase initiatives on record, symbolizing a robust commitment to shareholder alignment despite broader market turbulence.

Comparative Analysis of Payout Ratios: Technology Versus Non-Technology Firms in 2025

In 2025, the aggregate payout ratio for technology companies averaged near 34.5%, significantly lower than the 52.4% observed among energy sector firms and the overall non-technology average exceeding 45%. This disparity reflects divergent growth trajectories: technology firms prioritize reinvestment in AI, cloud infrastructure, and R&D, constraining free cash flow available for distribution.

Conversely, non-technology sectors with more mature cash flows and limited growth prospects, such as utilities and energy, maintain elevated dividend and buyback payouts to sustain investor appeal. The technology sector’s lower payout ratio evidences a transitional capital allocation paradigm where buybacks compliment but do not supplant aggressive innovation spending, illustrating a nuanced capital return strategy tailored to growth stage and cash flow stability.

Buyback Programs as a Stabilizing Force: Impact on Stock Volatility and Valuation Stability from Q2 to Q4 2025

Buyback activities played a critical role in mitigating stock price volatility during the volatile trading environment of 2025’s latter half. Firms conducting disciplined repurchases, notably Apple, exhibited reduced intra-quarter price swings compared to peers with reduced or paused buybacks, mitigating some downside pressure amid AI-related investment skepticism.

However, major technology firms outside Apple curtailed buybacks to redirect capital toward AI and data center expansion, leading to an observable increase in share price volatility from Q3 onward. This dynamic suggests a tradeoff where buybacks provide artificial price support and investor confidence in stable periods, but when scaled back to fund growth investments, market prices incorporate greater uncertainty about near-term returns. Consequently, buybacks remain a strategic lever balancing valuation support against capital deployment for future growth.

Understanding the nuanced patterns in capital returns through buybacks and dividends reveals how leading companies, particularly Apple, employ these mechanisms to sustain shareholder value even as growth paradigms evolve. The subsequent sections will build on this foundation by exploring how these strategic financial policies interact with technology sector innovation imperatives and investor sentiment, further elucidating pathways for resilient growth.

Strengthening Supply Chain Resilience and Geopolitical Adaptation Amid Rising Global Risks

This subsection delves into how leading U.S. companies are bolstering supply chain resilience through strategic localization and advanced manufacturing investments, key to mitigating geopolitical risks prominent between Q2 2025 and Q1 2026. The analysis focuses on quantifiable capacity expansions, financial impacts of operational initiatives, and adaptive measures companies implement to ensure continuity and agility in a complex regulatory and trade environment. This provides executives and strategists actionable insights into supply chain risk management aligned with evolving geopolitical dynamics.

Quantifying NVIDIA’s U.S. Manufacturing Capacity Expansion and Its Impact on Geopolitical Risk Mitigation

In 2025, NVIDIA significantly expanded its U.S.-based manufacturing footprint to counteract rising global geopolitical uncertainties, particularly those related to export controls and supply chain vulnerabilities in the semiconductor sector. The company accelerated investments in domestic fabrication capabilities, nearly doubling output capacity in key production lines dedicated to AI and data-center chips. This expansion reduced NVIDIA’s reliance on foreign foundries, notably those in East Asia, thereby diminishing exposure to trade restrictions and supply disruptions stemming from regional conflicts and export bans.

The strategic shift towards sovereignty in manufacturing facilitated by partnerships with U.S. government-backed initiatives and sovereign AI collaborations across multiple regions—including the UAE, India, and Europe—has further insulated operations from external shocks. This localization not only safeguards critical intellectual property but also strengthens supply chain transparency and control, reducing downtime risks. As a result, NVIDIA’s capacity growth acts as a tangible buffer against geopolitical risks, ensuring timely fulfillment of hyperscaler demand amid escalating global trade tensions.

Assessing Dollar General’s Value-Driven Supply Chain Initiatives and Revenue Contributions in 2025

Dollar General’s 2025 value propositions, notably its expanded $1 price-point offerings and enhanced private brand penetration, proved instrumental in driving robust same-store sales growth and increasing customer traffic, underscoring the efficacy of integrating supply chain efficiency with consumer-centric strategies. The company’s supply chain productivity gains—reflected in reduced shrink and damage—directly supported margin expansion while sustaining revenue growth, which analysts project to rise by approximately 3.8% year-over-year.

Operational improvements combined with IT modernization and the rollout of new store formats contributed to not only revenue resilience but also operational flexibility amidst inflationary and tariff-related challenges. These initiatives enhanced Dollar General’s ability to adapt sourcing and inventory management dynamically, mitigating potential disruptions and reinforcing its competitive positioning in cost-sensitive rural and small-town markets.

Corporate Localization Strategies: Broad Adoption and Strategic Benefits Among Leading Tech Firms

Top technology companies are intensifying localization efforts by segmenting enterprise technology stacks, diversifying supplier bases, and investing in regional manufacturing and data infrastructure to meet stringent data sovereignty and compliance mandates. These shifts are driven by increasing risks related to data theft, intellectual property protection, and regulatory fragmentation, prompting firms to balance global optimization with localized operational sovereignty.

Digital supply chain tools enhancing real-time inventory visibility, coupled with automation and workforce localization programs, enable improved responsiveness to regional market dynamics and regulatory changes. Localization strategies also extend to collaborative partnerships with local governments and entities, leveraging tax incentives and regulatory easements. The cumulative effect is a more resilient supply chain that reduces transportation costs and tariff impacts while improving scalability and innovation responsiveness, thus offering a strategic competitive advantage in volatile geopolitical environments.

Having examined how leading firms operationalize supply chain localization and resilience to mitigate geopolitical risks, the report next explores how these adaptability measures interplay with capital allocation and shareholder value strategies to sustain growth momentum under uncertainty.

7. Market Volatility and the Search for Sustainable Growth

Unraveling the Earnings-Price Paradox: Behavioral Drivers Behind Magnificent Seven Stock Volatility

This subsection investigates the intriguing disconnect between the robust fundamental earnings performance of leading mega-cap technology companies—the Magnificent Seven—and their contemporaneous stock price underperformance in early 2026. It contextualizes this paradox within broader market volatility and investor psychology, providing critical insights for portfolio managers and corporate strategists seeking to reconcile financial results with equity market behavior.

Quantifying 2026 YTD Price Declines Amidst Exceptional Earnings Growth

Despite the Magnificent Seven's outstanding earnings growth of 27.2% year-over-year in the fourth quarter of 2025, these companies experienced significant equity price contractions ranging from 5% to 30% year-to-date in early 2026. This divergence is particularly striking given that the remaining S&P 500 constituents posted comparatively moderate earnings growth near 10%, yet did not see such pronounced price declines. The sizable gap between fundamental performance and market valuation signals a decoupling where strong earnings momentum has not translated into expected shareholder value appreciation.

This volatility can be further understood by analyzing sector-level movements within the technology segment, which achieved overall 30% earnings growth while facing intense valuation compression. Traditional price-earnings multiple expansions did not follow suit, reflecting a market environment where growth is increasingly scrutinized for sustainability rather than absolute growth figures.

Broadening the lens to the entire S&P 500, earnings per share (EPS) growth has shown a steady upward trend from 10.0% in Q2 2025 to 13.2% in Q1 2026, highlighting sustained corporate profitability amidst broader market challenges. This consistent growth trajectory underscores that while earnings fundamentals remain robust, the stock price adjustments reflect more complex market dynamics beyond raw earnings figures [Chart: S&P 500 EPS Growth Rates].

Behavioral Biases Driving Investor Sentiment and Equity Price Dislocation

Investor reaction to high-growth stocks like the Magnificent Seven is heavily influenced by psychological and cognitive biases that often distort rational pricing mechanisms. Prominent biases contributing to the disconnect include overconfidence, where investors initially overestimate future growth potentials, leading to inflated valuations that later correct sharply; and loss aversion, which prompts rapid selling once early losses emerge, intensifying downward pressure.

Herd behavior also plays a significant role, as investors collectively shift away from high multiple growth stocks in favor of perceived safer assets, amplifying sell-offs and creating volatility disconnected from underlying earnings quality. Anchoring biases cause investors to fixate on prior elevated valuations, exacerbating disappointment and negative sentiment when earnings momentum slows or forecasts moderate. Additionally, mental accounting and regret aversion encourage investors to avoid realizing losses on safer sectors while quickly abandoning growth names showing transient setbacks.

These behavioral dynamics, compounded by broader market uncertainty including macroeconomic concerns and geopolitical risks, culminate in an environment where earnings beats are necessary but insufficient to sustain price performance. Understanding these biases is pivotal for strategists aiming to navigate earnings-driven volatility and develop more resilient portfolio positioning.

Having explicated the profound impacts of behavioral biases on market pricing despite strong earnings, the report now advances to explore evolving analyst sentiment patterns and forward-looking guidance, illuminating potential inflection points for market recalibration and sustainable growth trajectories.

Investor Sentiment and Forward-Looking Guidance: Navigating Shifting Market Expectations and Timing Inflection Points

This subsection delves into the evolving landscape of investor sentiment during the Q1 2026 earnings season, emphasizing sector-level guidance revisions and the signals they generate for near-term market momentum shifts. It builds on prior earnings performance analyses by uncovering how forward-looking analyst expectations and market behavioral patterns interplay to shape strategic positioning and timing decisions for key market participants.

Sectoral Guidance Revisions as Signals of Renewed Confidence

The Q1 2026 earnings season presents a robust narrative of upward earnings estimate revisions across key sectors, underscoring an emerging pattern of sustained corporate profitability despite macroeconomic headwinds. Notably, technology continues to lead with an expected earnings increase exceeding 23%, reinforcing its foundational role in overall market growth. Beyond this, sectors such as Finance, Basic Materials, Utilities, Business Services, and Energy have also experienced upward guidance adjustments, reflecting broadening confidence across cyclical and non-cyclical areas.

This positive revision trajectory marks a subtle yet important shift from the predominantly tech-driven optimism of previous quarters, suggesting a nascent sector rotation possibly fueled by improving fundamentals and resolved near-term geopolitical uncertainties. Although guidance remains cautious in some consumer discretionary and autos segments due to inflationary and tariff concerns, the aggregate effects of these sectoral upward revisions contribute to stabilizing investor expectations and underpin a higher baseline for earnings growth estimates heading into Q2 2026.

Timing Market Inflection: Concrete Indicators and Predictive Signals

Identifying precise inflection points within volatile market conditions requires integrating quantitative signals with qualitative assessments of investor psychology and external risk factors. Recent analytical models highlight that the resilience of the S&P 500 to geopolitical shocks, including escalations in the Middle East, has set the stage for a potential positive transition in market momentum. A significant technical indicator—an important reversal date around late July 2025—has been recognized by market technicians as a potential pivot where existing downward price pressures may abate, enabling renewed upward trajectories.

Further empirical data support this view: breadth-based models tracking participation rates across equities indicate early shifts toward healthier market structures, a critical element often preceding sustained rallies. These are complemented by sentiment metrics embedded in earnings surprise distributions and analyst revisions, which collectively signal a reduced risk premium and increasing investor conviction entering mid-2026. Consequently, market participants should anticipate near-term windows where technical and fundamental alignments coalesce, creating actionable opportunities for portfolio rebalancing and strategic entry points in growth and defensive sectors alike.

The observed dynamics of sentiment shifts and guidance revisions lay the groundwork for the final analytical section, where we synthesize these insights into strategic imperatives for navigating the remainder of 2026. Understanding these evolving investor expectations and timing signals equips decision-makers to anticipate market rotations and manage risk-return profiles effectively.

8. Synthesis and Strategic Implications: Charting the Course Beyond 2026

Strategic Takeaways and Prioritization Framework: Quantifying Sector Rotation and AI Leadership Risks