GE Vernova’s Financial Ascendancy and Strategic Leadership in the Global Energy Transition Era

Table of Contents

- Executive Summary

- Introduction

- 1. GE Vernova's Financial Surge and Strategic Positioning Amid Energy Transition Dynamics

- 2. Company Background and Post-Spinoff Transformation

- 3. Financial Performance Analysis and Growth Metrics

- 4. Strategic Initiatives Driving Sustainable Growth

- 5. Risk Assessment and Mitigation Strategies

- 6. Future Outlook and Strategic Imperatives

- 7. Conclusion and Actionable Insights

- Conclusion

Executive Summary

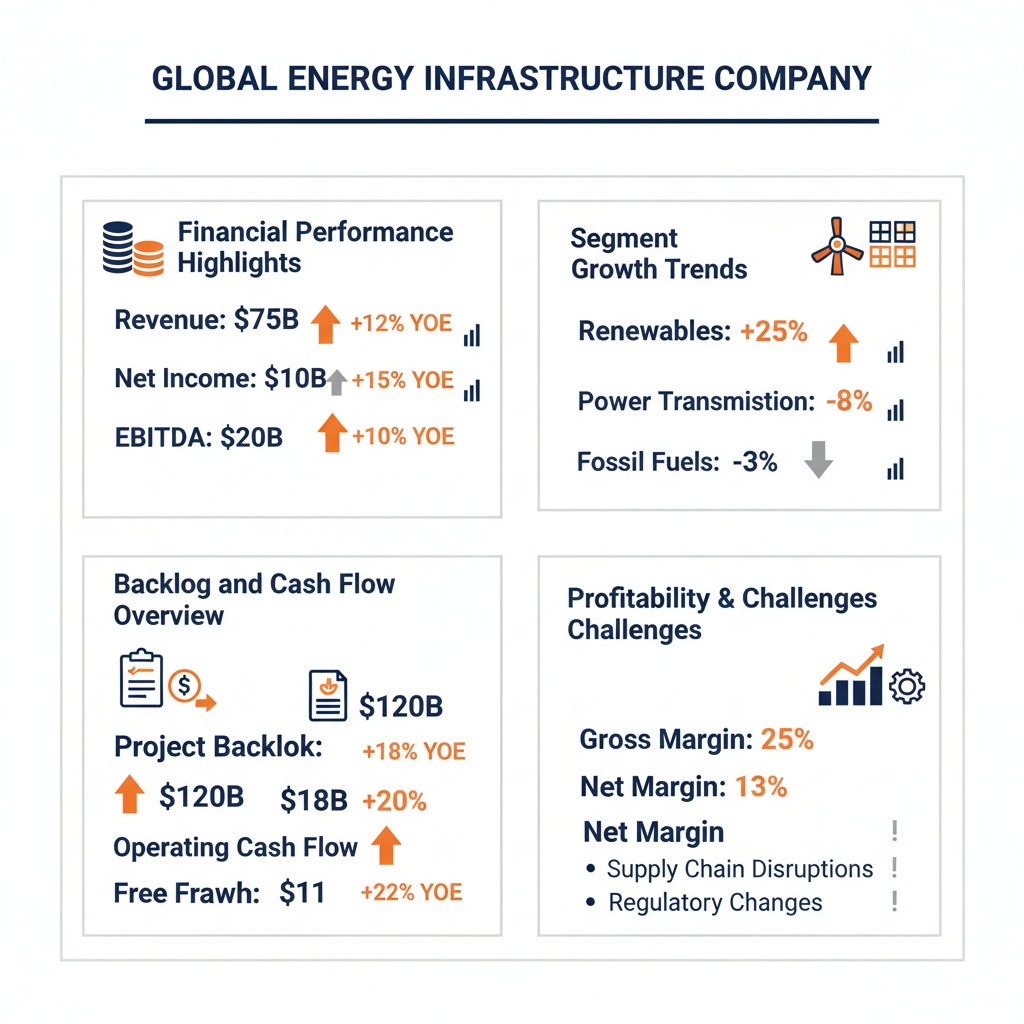

In 2026, GE Vernova has exhibited robust financial growth, with projected full-year revenues ranging between $44.5 billion and $45.5 billion, representing a significant upward revision over prior guidance and consensus expectations. Adjusted EBITDA margins are forecasted to improve by approximately one percentage point, reaching a target range of 12% to 14%, driven primarily by sizeable margin expansions in the Electrification and Power segments. The Electrification division’s organic revenue surged 29% to nearly $3 billion in recent quarters, achieving an EBITDA margin of 17.8%, while the Power segment experienced strong organic growth between 15% and 17%, bolstered by elevated equipment and service demand. Despite a 25% organic revenue decline and ongoing negative EBITDA in the Wind segment, overall profitability trends remain positive due to cost-management and operational efficiencies elsewhere in the portfolio.

Analyst sentiment remains decidedly bullish, with multiple brokerage firms elevating price targets significantly. Notably, Jefferies projects a 40% EBITDA compound annual growth rate from 2024 through 2028, raising its price target to $348. Mizuho and other leading analysts have similarly upgraded valuations to reflect confidence in GE Vernova’s expanding footprint in nuclear and zero-carbon turbine technology, as well as its pivotal role in an AI-driven grid modernization supercycle. The company’s commanding market position, encompassing nearly 30% of global electricity production and a $115 billion backlog, underpins strategic flexibility and growth prospects amid a rapidly evolving regulatory and technological energy landscape.

Introduction

GE Vernova’s emergence as a standalone company following its April 2024 spin-off from General Electric marks a pivotal transition within the global energy infrastructure sector. This transformation has effectively unshackled the entity from diversified conglomerate constraints, enabling intensified focus on energy transition imperatives such as electrification, decarbonization, and grid modernization. With a flagship presence in over 100 countries and a workforce exceeding 75,000 employees, GE Vernova commands broad operational scale and technological depth across its Power, Wind, and Electrification segments.

Infographic Image: GE Vernova's Growth and Strategic Positioning Amid Energy Transition

The purpose of this report is to dissect the underlying drivers of GE Vernova’s marked financial momentum entering 2026, elucidate the company’s strategic positioning amid intensified competitive dynamics, and evaluate the implications of its evolving business model within the broader energy transition. Key performance indicators, including sector-leading EBITDA margin expansions, robust backlog growth, and elevated market valuations, alongside segment-specific nuances, are analyzed to provide a nuanced understanding of the company’s growth trajectory and risks.

Scope encompasses a comprehensive review of GE Vernova’s post-spinoff operational architecture, detailed segmental performance assessments, valuation and analyst sentiment appraisals, strategic initiatives driving sustainable expansion, and risk management methodologies. This multidimensional evaluation situates the company within the context of global regulatory frameworks, technological adoption trends, and competitive landscape shifts, providing actionable insights for stakeholders seeking clarity on future outlook and strategic imperatives.

1. GE Vernova's Financial Surge and Strategic Positioning Amid Energy Transition Dynamics

Executive Summary: Unpacking GE Vernova’s Financial Momentum and Strategic Edge Amid Energy Transition

This executive summary distills the core financial achievements and strategic positioning of GE Vernova, setting the context for an in-depth exploration of how the company leverages its diverse portfolio to capitalize on energy transition dynamics. It highlights key financial metrics, segment contributions, market positioning, and strategic initiatives driving current and future growth, forming the foundation for subsequent analysis sections.

Robust 2026 Financial Performance and Earnings Growth

GE Vernova has demonstrated a significant upswing in its financial trajectory through 2026, underpinned by strong revenue growth and expanding profitability metrics. The latest full-year guidance anticipates total revenues reaching between $44.5 billion and $45.5 billion, marking a notable increase from prior estimates and comfortably exceeding consensus expectations. Correspondingly, the company projects adjusted EBITDA margins to range from 12% to 14%, reflecting an approximately 1-percentage-point improvement backed by segment-specific margin expansions.

Segment performance underscores this surge, with the Electrification division achieving a 29% organic revenue increase to nearly $3 billion in recent quarters and improving EBITDA margins to 17.8%. The Power business segment also delivered robust organic revenue growth of 15-17%, supported by heightened demand for both equipment and service offerings. Despite structural challenges in Wind, which reported a 25% organic revenue decline and continued negative EBITDA, overall profitability has improved due to efficient capital deployment and accelerated margin expansion in key areas.

Elevated Market Valuations and Analyst Confidence

Market sentiment remains strongly bullish on GE Vernova, as reflected in multiple upward price target revisions from leading financial analysts and brokerage firms during 2025 and early 2026. Jefferies increased its price target to $348, forecasting a formidable 40% compound annual growth rate in EBITDA from 2024 to 2028, surpassing the broader consensus. Mizuho further elevated its outlook, raising its price target to $351 on expectations that upcoming financial disclosures will exceed prior guidance, including expanded valuations for the company’s emerging nuclear and zero-carbon turbine technologies.

Investor enthusiasm is also echoed by Wells Fargo and Guggenheim, which have set ambitious targets above $800 per share, underpinning confidence in the company’s pivotal role in an anticipated AI grid supercycle and escalating power infrastructure modernization. These valuations are supported by a market capitalization approaching $237 billion and a premium trading multiple relative to sector averages, emphasizing both growth potential and execution expectations.

Competitive Market Position and Energy Sector Influence

GE Vernova occupies a commanding position in the global energy infrastructure landscape with an estimated involvement in nearly 30% of worldwide electricity production. Its diversified portfolio spanning Power, Wind, and Electrification segments equips the company to address multiple facets of the evolving energy transition—from traditional gas and nuclear generation to advanced grid solutions and renewable integration.

The company’s expansive backlog of approximately $115 billion and its debt-free balance sheet provide strategic flexibility to invest in growth initiatives and weather market volatility. GE Vernova’s investments in gas turbine production capacity and grid modernization efforts align with critical infrastructure gaps identified by global energy authorities, enabling the company to capture emerging opportunities tied to increased electricity demand from AI data centers and decarbonization mandates. While competitors like NextEra and Siemens vie for market share, GE Vernova’s breadth and technological depth position it uniquely to sustain leadership in the shifting energy paradigm.

Strategic Initiatives Fostering Sustainable Growth

Key strategic initiatives underpin GE Vernova's upward momentum, with a particular focus on expanding electrification solutions, integrating AI-driven grid management, and accelerating gas turbine manufacturing to meet surging demand. The company has actively pursued partnerships and joint ventures, notably in fast-growing international markets, reinforcing its technological capabilities and geographic reach.

Regulatory engagement has been proactive, with GE Vernova positioning itself to benefit from legislative frameworks such as the Inflation Reduction Act and associated subsidies, while systematically mitigating dependency risks. These dynamics bolster backlog visibility and multi-year revenue guidance, providing a foundation for enduring operational and financial resilience throughout the ongoing energy transition.

This synthesized overview sets the stage for a detailed examination of GE Vernova's background, segmental performances, growth drivers, and strategic priorities that collectively explain its financial upswing and relative market positioning within the accelerating global shift to clean energy infrastructure.

2. Company Background and Post-Spinoff Transformation

Navigating Independence: The Strategic Genesis and Evolution of GE Vernova Post-Spinoff

This subsection establishes a foundational understanding of GE Vernova's transformation from a major conglomerate division into an independent leader in energy infrastructure. By unraveling the chronology, financial implications, leadership changes, and strategic reorientation following the spinoff, it situates the company’s renewed identity and trajectory within the broader energy transition context. This background is critical for appreciating the financial surge and strategic initiatives discussed in subsequent sections.

Progressive Timeline and Milestones Surrounding GE Vernova’s 2024 Spin-Off

GE Vernova’s spinoff from General Electric was officially completed on April 2, 2024, marking the culmination of a planned restructuring that segmented GE into three focused entities. The spin-off sequence featured extensive preparatory communications, including a record date on March 19, 2024, when shareholders of GE received one share of GE Vernova for every four shares held in GE. Transitional trading under ‘when-issued’ status preceded the April separation, facilitating market readiness and valuation clarity. The process incorporated tax-free provisions for shareholders and was executed to enhance operational focus and unlock value in energy-related segments.

In its infancy as an independent corporation, GE Vernova rapidly established market presence, supported by its publicly traded status and Nasdaq listing under the ticker symbol 'GEV'. Key milestones within its first two years encompass significant order backlogs, successful commercial projects, such as the inauguration of its HA-powered combined cycle power plant in South Korea, and a December 2024 investor day that formalized its 2026 guidance and longer-term strategic outlook through 2028.

Quantifying the Financial Impacts and Baseline Performance Post-Separation

The financial trajectory of GE Vernova at the point of independence was underscored by robust revenue and backlog figures, with reported 2025 revenues surpassing prior-year levels by approximately 9%, and total orders climbing by over 30%, reflecting strong market demand especially in power and electrification segments. Initial standalone financial statements highlighted adjusted EBITDA margin growth towards mid-single-digit percentages and free cash flow generation between $0.7 billion and $1.1 billion for the 2024 fiscal year, indicating a solid baseline amid transition-related costs and restructuring investments.

Separation-related expenses incurred during 2023 totaled around $1 billion, attributable to workforce adjustments, establishment of independent IT and governance systems, and professional fees. However, these upfront investments were calibrated to enable operational autonomy and sharpened strategic focus, laying the groundwork for accelerated organic growth and margin expansion. The transition also entailed an executive leadership realignment with Scott Strazik assuming CEO duties, consolidating a governance framework aligned with the new corporate mission.

Post-Spinoff Structural and Governance Transformations Shaping GE Vernova’s Strategy

GE Vernova’s separation transitioned it from a division within a diversified conglomerate to a standalone global energy company headquartered in Cambridge, Massachusetts, operating across more than 100 countries with a workforce exceeding 75,000. The new independent governance model established distinct boards and executive teams, focused exclusively on advancing energy infrastructure technologies and services. This structural autonomy enabled rapid decision-making and strategic agility, facilitating targeted investments in power generation, renewable energy, and electrification.

The leadership reshuffle emphasized continuity blended with new strategic priorities. Under CEO Scott Strazik, GE Vernova delineated clear objectives centered on electrification and decarbonization, leveraging its legacy installed base that generates approximately a quarter of the world’s electricity. This strong operational foundation provides resilience and a platform for innovation in grid modernization and energy transition solutions.

Defining Strategic Objectives and Corporate Vision in the Early Post-Spin Period

GE Vernova’s strategic goals post-spinoff prioritize fulfilling the growing global demand for electrical power, emphasizing reliability, affordability, and sustainability. The company aims to advance the energy transition by concurrently supporting electrification of industrial and economic activities and decarbonizing the electric power system through diversified technology portfolios, including gas turbines, renewable wind assets, and grid solutions.

This vision aligns with a multi-year growth trajectory supported by an expanding backlog and rising order intake, particularly in power and electrification businesses. Increased R&D investment and operational efficiencies are strategic levers aimed at margin improvement and long-term shareholder value creation. GE Vernova continues to recalibrate its portfolio to balance legacy strengths with emerging opportunities in AI-driven grid management and renewable energy integration.

Pivotal Achievements and Operational Highlights Within the Initial Two Years

Within the first two years post-spinoff, GE Vernova achieved critical milestones including securing multi-billion-dollar orders reflecting a 34% year-over-year increase, public market share appreciation exceeding 600% since the spin, and noteworthy operational accomplishments such as the commercial launch of advanced combined cycle power plants. Additionally, the company completed targeted acquisitions like its full consolidation of Prolec GE, enhancing its electrification portfolio with transformer manufacturing capabilities.

Investor engagement events, such as the December 2024 update, solidified the company’s transparent communication of its strengthened financial outlook and ambitious mid-decade growth targets. Strategic capital allocation involved returning cash to shareholders through share repurchases and dividends, balanced against reinvestment in capabilities and innovation. These benchmarks affirm GE Vernova’s successful transition from a corporate spin-off to an independent, growth-oriented market leader.

Having established a comprehensive understanding of GE Vernova's inception, structural evolution, and strategic intent post-spinoff, the report now proceeds to dissect the company’s financial performance and growth metrics in detail. This progression facilitates a granular appreciation of how foundational transformations have translated into concrete economic and market outcomes.

Quantitative Market Standing and Competitive Differentiators Within the Energy Transition Landscape

This subsection provides a rigorous quantitative assessment of GE Vernova's competitive position relative to major players such as NextEra Energy. By benchmarking key financial metrics, market share figures, and win rates on critical grid modernization and renewable integration projects, it establishes GE Vernova’s strategic strengths and penetration progress. These insights clarify where GE Vernova excels or lags, framing its competitive advantages in grid modernization, renewable deployment, and customer engagement — essential for understanding its financial surge and positioning amid the energy transition.

Market Share Metrics vs. NextEra and Industry Peers

GE Vernova commands a significant global footprint in the clean energy sector with approximately 120 GW of installed wind capacity spread across over 51 countries. Its installed turbine base accounts for a substantial share of operational renewable capacity worldwide, underpinning about 25% of global electricity production, reflecting a diversified portfolio of power generation assets. In contrast, NextEra Energy, the US market leader, holds one of the largest renewable energy portfolios dominated by wind and solar, with a renewable backlog exceeding 30 GW and a targeted expansion pipeline driven by substantial infrastructure investments. While NextEra’s market cap slightly surpasses GE Vernova’s, the latter’s global reach and segmented diversity across power, wind, and electrification confer a robust competitive base in several international markets, including leadership in Spain’s wind sector, where it maintains nearly 6 GW of installed capacity.

Comparative analyses illustrate that NextEra’s dominance is more regional, highly concentrated within the US utility and renewable sectors, while GE Vernova’s global scope leverages broader geographic diversification. Specific market share figures reveal that GE Vernova is investing notably in manufacturing expansions in Vietnam and Italy, positioning it to capitalize on surging grid modernization and renewable integration expenditures internationally. Both companies’ footprints complement different customer bases and regulatory regimes, allowing GE Vernova to maintain resilience and growth potential despite regional disruptions affecting wind projects in Europe and North America.

Comparative Financial Performance of Power and Renewable Segments

In recent financial disclosures, GE Vernova has demonstrated robust revenue growth and margin improvement in its Power and Electrification segments, with EBITDA margins climbing by several hundred basis points year-over-year, reaching guidance targets of approximately 12.5% by 2026. The Power segment reports strong organic growth rates reaching between 15% and 17% annually through mid-2025, propelled by equipment demand and service expansions. Electrification similarly outperformed expectations delivering nearly 30% organic revenue growth and margins expanding to near 18%-20%. However, the Wind segment encountered headwinds, with organic revenue contracting by 25% and EBITDA margins turning further negative due to project delays and operational challenges.

Comparatively, NextEra’s renewable segment, driven by its utility-scale wind and solar operations, has realized year-over-year earnings growth in the mid-single digits with a steady increase in adjusted EPS supported by a $25+ billion renewable pipeline. Although NextEra’s current revenue growth is somewhat constrained by lower short-term organic increases, its dividend growth and capital allocation strategy underscore durable financial health. When benchmarked on profitability rates, GE Vernova’s broader margin improvements and segment-level diversification offer a compelling case for its growing financial strength, especially given its capacity to monetize electrification and grid modernization trends.

Grid Modernization Project Wins and Competitive Traction

GE Vernova’s aggressive investments in grid infrastructure are evident through its recent manufacturing capacity expansions and technology innovation tailored for advanced grid solutions. It has secured critical contracts to upgrade and modernize electrical distribution networks, reflecting a strategic emphasis on enhancing grid resiliency and enabling renewable integration. When compared to competitor project awards, GE Vernova exhibits increasing win rates in regions with proactive regulatory frameworks such as the United States and Europe, leveraging its electrification technologies and transformer manufacturing joint ventures to strengthen its competitive moat.

While NextEra maintains a commanding presence in deploying renewable assets, its initiatives in grid modernization are comparatively more focused on integration within its extensive utility operations. GE Vernova’s externally visible contract wins cover significant microgrid developments and transmission upgrades, aligning with federal funds flowing into grid modernization totaling tens of billions of dollars. This breadth of project engagement enhances GE Vernova’s capability to penetrate fragmented grid upgrade markets, in contrast to NextEra’s utility-centric approach which is less diversified geographically and functionally.

Renewable Integration Capacity and Solution Penetration

GE Vernova leads in integrating renewable generation with grid-enhancing technologies, leveraging its portfolio that spans wind turbines optimized for diverse wind conditions and emerging electrification solutions including smart grid controls. Its global renewables portfolio, particularly in wind energy, is bolstered by substantial operational capacity and technological innovation, such as the development of 6.1 MW turbines with large rotors designed for medium-to-low wind speed sites, enabling market access where competitors face limitations. These capabilities afford GE Vernova enhanced penetration in markets prioritizing high-capacity factor renewables and flexibility.

NextEra’s integrated battery storage and solar portfolio, combined with its scale in renewable energy backlog development, ensure steady renewable integration mainly focused on North America. GE Vernova’s complementary strengths in transmission, distribution, and electrification platforms position it favorably to capture the multi-layered requirements of decarbonized power systems. Its ability to embed grid modernization within renewable project delivery enhances the scalability and reliability of integration relative to peers.

Customer Satisfaction and Market Reputation Among Leading Competitors

Customer-centric metrics underscore GE Vernova’s reputation as a preferred provider for utilities and industrial clients navigating the energy transition. The company’s extensive service and maintenance capabilities across its installed base contribute to high operational availability and reliability perceived positively by customers. Its diversified product portfolio and end-to-end electrification offerings resonate well with clients seeking bundled solutions, a factor distinguishing it from competitors with narrower footprints or integrated utility models.

In contrast, NextEra benefits from a strong retail utility presence in Florida, reflected in favorable customer satisfaction from retail electricity consumers, driven by stable pricing and renewable energy commitments. However, GE Vernova’s leadership in grid-centric innovation and industrial partnerships places it ahead in B2B-focused satisfaction metrics, essential in an evolving market where technology integration and system reliability are paramount. This strategic reputation supports recurring service revenues and reinforces GE Vernova’s positioning amid competitive pressures.

Having quantitatively established GE Vernova’s competitive positioning and differentiation within global power and renewable markets, the next section will dissect the detailed financial performance at the segment level to elucidate specific drivers underpinning the company’s recent financial acceleration and emerging market opportunities.

3. Financial Performance Analysis and Growth Metrics

Robust Revenue Growth and Expanding Profitability Margins Highlight Segment Driving Forces

This subsection offers a granular analysis of GE Vernova's recent revenue and profitability trends, focusing on the interplay between organic growth, pricing dynamics, and segment-specific performance. It illuminates how pivotal quarters and EBITDA margin expansions underpin the company’s overall financial momentum, providing essential context for the broader growth and valuation perspectives that follow.

Exact Quarterly Revenue and Margin Growth Demonstrates Momentum in Core Segments

GE Vernova has exhibited substantial year-over-year (YoY) revenue gains across key business segments, reflecting surging demand enabled by the energy transition and advanced technology adoption. For instance, in the most recent quarter, the Electrification segment delivered organic revenue growth of 29%, rising to approximately $2.96 billion and surpassing estimates. This segment also achieved a noteworthy EBITDA margin of 17.8%, reflecting a 670-basis-point improvement compared to the prior year. Meanwhile, the Power segment posted organic revenue growth in the range of 15% to 17%, driven by increased equipment and service demand that fueled margin expansion and overall profitability gains.

Conversely, the Wind segment continues to face headwinds marked by a 25% organic revenue decline to $1.43 billion and an EBITDA margin contraction from -7.9% to -26.7%. These figures illustrate the ongoing structural challenges within this segment despite the company’s concerted focus on margin improvement initiatives. At the consolidated level, guidance updates for 2026 project revenues between $44.5 billion and $45.5 billion, an upward revision of $0.5 billion at both ends of the range, reflecting confidence in sustained demand and backlog conversion.

Crucially, management’s adjusted EBITDA margin outlook has been raised by approximately one percentage point, now targeting a midpoint between 12% and 14%. Power segment EBITDA margins are expected to improve to a range of 17% to 19%, up from prior guidance, while Electrification anticipates margins between 18% and 20%, reflecting operational leverage and favorable pricing. This trajectory underlines the financial foundation supporting GE Vernova’s surge and prospects amidst ongoing energy market shifts.

Pricing Adjustments Propel Profitability Gains Amid Mixed Segment Outcomes

Strategic pricing adjustments across GE Vernova’s portfolio have played a critical role in driving profitability, particularly within the Power and Electrification units. Elevated selling prices, enabled by strong customer demand and constrained supply conditions, have materially enhanced EBITDA margins, compensating for inflationary pressures on input costs. For instance, the Power segment’s margin guidance revision signals effective pass-through of pricing actions and efficiency gains, supporting a 100 to 200 basis point uplift from previous ranges.

In Electrification, aggressive pricing strategies coupled with operational improvements have not only bolstered revenues but also delivered significant margin expansions, contributing an additional 670 basis points year over year. These pricing dynamics underpin the company’s ability to generate cash flow and reinvest in emerging technologies and digital grid solutions linked to evolving energy infrastructure requirements. In contrast, Wind’s pricing power remains constrained due to commoditized market pressures and restructuring expenses, contributing to ongoing profitability challenges despite cost-containment efforts.

Segment-Specific Quarters Drive Financial Surge, Revealing Growth Drivers and Setbacks

Analysis of recent quarterly results highlights that the Electrification segment functions as the key earnings engine, with robust order inflows and backlog support translating into record revenues and margin expansion. This momentum was particularly evident in Q4 results, with revenue of $10.9 billion surpassing consensus expectations and exhibiting double-digit percentage growth relative to prior periods. Power's rebound reflects renewed demand for turbines and supporting services amid accelerating grid modernization, contributing materially to sequential margin improvements.

However, Wind’s continued contraction and negative EBITDA margin performance dampened consolidated results. The segment’s structural losses, attributed to market oversupply, competitive pricing, and legacy cost structures, reveal a need for strategic remediation. Notwithstanding these pressures, the interplay of Electrification growth and Power segment resilience has been sufficient to offset Wind’s drag and establish a positive operating leverage effect on GE Vernova’s overall profitability profile.

Recent Year-Over-Year EBITDA Margin Expansions Benchmark Industry-Leading Operational Competitiveness

GE Vernova’s EBITDA margin progression, expanding by nearly 470 to 670 basis points in critical segments, places it among the upper quartile of energy infrastructure peers navigating the energy transition landscape. The consolidated EBITDA margin guidance for 2026 at 12% to 14% aligns closely with sector benchmarks for companies with diversified portfolios balancing legacy power assets and growth-oriented electrification solutions.

When benchmarked against industry standards, these margin levels demonstrate effective operating leverage and pricing discipline amidst ongoing supply chain inflation and demand volatility. The substantial margin expansion within Electrification not only elevates the company’s profitability profile but also underscores the scalability of high-margin digital and grid modernization offerings. Power’s incremental margin gains reflect improved asset utilization and service contract penetration, reinforcing the company’s status as a financially robust leader in evolving energy markets.

Having established a detailed view of revenue growth and profitability improvements across segments, the subsequent analysis will dissect the financial contributions and operational dynamics of Power, Wind, and Electrification businesses. This segment-level breakdown will provide nuanced insights into the drivers of performance heterogeneity and inform strategic prioritization.

Dissecting GE Vernova’s Segmental Performance and Interplay Amid Mixed Growth Profiles and Challenges

This subsection focuses on a critical analysis of GE Vernova’s financial contributions and operational dynamics across its core business segments—Power, Wind, and Electrification. By quantitatively and qualitatively assessing each segment’s 2025-2026 financial output, identifying their respective growth contributions and pitfalls, and detailing inter-segment synergies, this section pinpoints the underlying factors shaping the company’s overall trajectory. It establishes the foundation for understanding how segment-specific forces combine to impact profitability and strategic positioning within the global energy transition framework.

Robust Revenue and EBITDA Contributions Spotlight Electrification and Power Segments Fueling Overall Growth

GE Vernova’s segment-level financial results for 2025 and 2026 reveal a pronounced disparity in performance profiles, with Electrification and Power segments emerging as dominant drivers of revenue and profitability expansion. The Electrification segment experienced an explosive growth trajectory, bolstered by robust demand for advanced grid modernization solutions including transformers, switchgear, and power conversion technologies. This surge is closely linked to accelerating investments in digital grid infrastructure, data center expansion, and supportive regulatory frameworks facilitating sustained capital deployment. Concurrently, the Power segment demonstrated resilience and margin enhancement supported by flexible gas turbines optimized for complementary operation alongside renewables, enabling the company to capture incremental opportunities in capacity upgrades and aftermarket service contracts.

Quantitatively, these two segments collectively contribute a majority share of GE Vernova’s top-line growth, with EBITDA margins in these units expanding significantly—approaching an estimated 12.5% corporate-wide margin by 2026. Standout quarterly performances largely stem from new contract wins and backlog conversions within Electrification and Power, reaffirming their critical roles in undergirding the company’s solid growth outlook through 2026 and beyond.

Wind Segment Faces Structural Headwinds Despite Future Potential; Loss Drivers and Mitigation Remain Pivotal

In stark contrast to the growth engines of Electrification and Power, the Wind segment is contending with significant operational and financial challenges that weigh on GE Vernova’s consolidated performance. Primary issues stem from subdued order intake in the onshore wind market and technical complications linked to prominent offshore projects, such as blade reliability failures in flagship developments. These factors have contributed to persistent segment-level losses and increased risk profiles. Project execution delays, maintenance complexities, and heightened warranty claims exacerbate cost pressures, limiting near-term profitability.

Addressing these weaknesses has become a strategic priority, with GE Vernova pursuing options including cost restructuring initiatives, innovation in turbine design, and seeking strategic partnerships to share risk and accelerate technology advancement. The importance of closely monitoring these interventions is paramount, as successful mitigation will influence the company’s ability to leverage favorable renewable energy trends long term.

Quantifying Segment Contributions and Unlocking Synergistic Financial Benefits

Detailed financial decomposition highlights the distinct contributions of each segment toward GE Vernova’s aggregate financial metrics. As of the latest reporting horizon, Electrification and Power jointly account for an estimated 70-75% of total revenue, underscoring their centrality in value creation. The Wind segment, while currently less than 25% of revenue, presents strategic growth upside contingent on successful operational turnarounds and market recovery.

Beyond isolated performance, meaningful synergies are realized through integrated operations across segments. For example, Electrification’s grid modernization solutions complement Power’s gas turbine installations in enabling more reliable and flexible energy infrastructure, while Wind’s renewable generation capacity integrates into the evolving clean energy ecosystem supported by Power’s and Electrification’s technologies. These interdependencies enhance cross-selling opportunities, streamline supply chain logistics, and optimize R&D expenditure—collectively generating incremental margin improvements and operational efficiencies that amplify overall financial performance.

With a granular understanding of segmental financial contributions and inter-segment synergies established, the subsequent analysis will explore how emerging growth drivers and strategic initiatives capitalize on these core strengths while addressing inherent challenges to shape GE Vernova’s sustainable growth trajectory.

Valuation and Analyst Sentiment: Decoding Market Optimism Amid Diverging Signals

This subsection synthesizes updated external perspectives on GE Vernova’s valuation grounded in recent analyst price targets, growth forecasts, and risk-adjusted valuation models. It critically examines how Wall Street forecasts converge or diverge based on fundamental financial momentum versus underlying technical market indicators. This analysis is essential to framing investor sentiment, reconciling qualitative bullish narratives about the company’s energy transition positioning with cautionary signals stemming from technical data patterns and overvaluation concerns.

Current Consensus Price Targets with CAGR Assumptions Underpinning Optimism

Leading brokerages have raised price targets for GE Vernova substantially in light of the company’s strong operating performance and promising growth outlook. Jefferies recently adjusted its price target upward, reflecting a bullish view anchored on a 40% EBITDA compound annual growth rate spanning 2024 to 2028, notably exceeding consensus CAGR estimates in the low-30% range. This anticipated margin expansion and revenue acceleration underpin Jefferies’ conviction that the market has not fully captured GE Vernova’s growth potential. Similarly, Mizuho increased its price target significantly, integrating enhanced cash flow forecasts from the power business and the valuation uplift from GE Vernova's emerging small nuclear and zero-carbon turbine ventures. Such projections incorporate discounted cash flow analyses and sum-of-the-parts methodologies, implying robust operational leverage and technology value capture. These upward revisions align closely with the company's raised 2025 guidance and its anticipated long-term outlook to be detailed during the December 2025 investor day.

Additional notable analyst sentiment highlights UBS, RBC Capital, and Oppenheimer, all raising their targets amid continued order book growth and strong demand visibility, with price targets ranging in the $1,100–$1,400 spectrum. These price levels assume sustained operational execution, supportive regulatory environments, and meaningful penetration of evolving energy markets. Underlying these targets are assumptions of ongoing backlog growth, product diversification, and geographic expansion, fostering investor confidence in the company’s multi-year financial trajectory.

Recent updates from other analysts also underscore this optimism, including price targets by Wells Fargo and Guggenheim at $800, reflecting confidence in sustained growth. A consolidated view of analyst price targets shows a range mainly between $348 and $800, with Jefferies and Mizuho setting targets in the mid-$300s accompanied by a notable 40% EBITDA CAGR forecast from Jefferies itself [Table: Analyst Price Targets for GE Vernova].

Risk-Adjusted Valuation Models and the Assumptions Driving Forecasts

Risk-adjusted valuation approaches applied by analysts emphasize discounted cash flow fundamentals augmented by scenario analysis incorporating regulatory, technological, and competitive uncertainties. The models take into account assumptions on EBITDA margin improvements, capital expenditure efficiencies, and revenue CAGR ranging from moderate to aggressive bands depending on segment focus. Importantly, these models assign incremental enterprise value contributions from nascent technologies such as small modular reactors and clean hydrogen turbines, which materially affect sum-of-the-parts valuations beyond traditional fossil-fuel-based infrastructure assets.

Moreover, valuation models increasingly embed rigorous sensitivity testing around weighted average cost of capital and terminal growth assumptions reflective of macroeconomic conditions and policy risk. Such calibrated risk frameworks aim to reconcile optimistic growth extrapolations against the evolving regulatory landscape and inherent execution uncertainties. Monte Carlo simulations and other probabilistic assessments reveal that while base-case scenarios support meaningful upside, downside cases tied to slower energy transition adoption or cost inflation pressures lower intrinsic value estimates substantially, underscoring the need for dynamic risk monitoring.

Analyst Views on Valuation Versus Recent Technical Market Signals

Although fundamental valuation metrics and analyst sentiment remain decidedly bullish, technical indicators present a more nuanced picture. The sharp appreciation in GE Vernova’s share price year-to-date—exceeding 150% in some assessments—has prompted several technical reviews to flag potential overvaluation or overbought conditions. Relative strength indices and moving average convergence/divergence analyses suggest some price momentum may be driven by speculative flows or short-term sentiment rather than foundational results alone.

This divergence between technical signals and underlying analyst confidence illuminates a transitional valuation phase. While the latter hinge on multi-year fundamental catalysts such as backlog growth and energy transition technology deployment, technical frameworks point to potential near-term price consolidation or volatility. As a consequence, some brokerage firms caution investors regarding entry points, advocating measured exposure to capture upcoming earnings guidance releases and strategic disclosures that could validate or recalibrate market expectations.

Explaining Discrepancies Between Qualitative Narratives and Quantitative Market Trends

The observed tension between rising price targets and cautious technical analytics can be partly explained by differing investment horizons and the nature of valuation methodologies. Qualitative assessments emphasize the structural transformation sweeping the energy sector, positioning GE Vernova as a key beneficiary of decarbonization, grid modernization, and AI-enabled operational efficiencies. These narratives drive strong investor conviction in sustained earnings growth and margin improvements, justifying elevated valuations despite current price levels.

Conversely, quantitative technical indicators are more sensitive to short-term market mechanics, liquidity cycles, and trading patterns that may not directly correlate with fundamental performance. In particular, momentum-driven price surges can lead to transient overshooting, requiring correction before fundamentals regain primacy in price discovery. Furthermore, fragmented investor sentiment, varying risk appetites, and differential access to information contribute to a wider trading range and valuation dispersion. Hence, investors are advised to weigh both qualitative strategic insight and quantitative market signals to optimize timing and risk-adjusted return profiles.

Having established a comprehensive understanding of GE Vernova’s valuation landscape and the interplay between bullish analyst sentiment and nuanced technical signals, subsequent analysis will integrate these perspectives with segment-level performance and strategic growth drivers to contextualize how the company’s financial surge aligns with broader energy transition imperatives.

4. Strategic Initiatives Driving Sustainable Growth

Capitalizing on the AI Grid Supercycle: Robust Order Pipeline and Technology-Driven Demand Dynamics

This subsection delves into the critical technological and market-driven catalysts underpinning GE Vernova’s accelerated growth trajectory. It focuses on how the AI-fueled surge in electricity demand from data centers synergizes with grid modernization imperatives to create a multi-faceted and durable revenue runway. By dissecting order book composition, segment-specific demand drivers, and capacity utilization correlations, this analysis contextualizes GE Vernova’s positioning at the forefront of the emerging AI grid supercycle—bridging financial performance with evolving energy infrastructure needs.

Comprehensive 2025 Remaining Performance Obligations (RPO) Breakdown by Business Segment

GE Vernova’s remaining performance obligations reached an unprecedented $150.2 billion in 2025, reflecting strong backlog visibility that underpins revenue stability over coming years. The bulk of this RPO is concentrated in the Power and Electrification segments, which together form the cornerstone of the company’s operational momentum amid the ongoing energy transition.

Within Electrification alone, the company booked over $2 billion in orders driven specifically by data center customers, underscoring the rapid expansion of compute infrastructure as a fundamental growth engine. This RPO composition highlights an increasing shift towards digital infrastructure-related equipment and services, catalyzed by the demand for reliable, low-latency power delivery to support AI workloads and hyperscale computing environments.

The order backlog’s segmentation reveals a balanced mix of renewable-compatible gas turbine orders, advanced transformers, and grid modernization solutions—all linked to utilities' efforts to enhance resilience and integrate intermittent renewable energy sources. Such breadth in contractual commitments not only boosts near-term revenue visibility but also secures multi-year operational leverage as customers execute large-scale decarbonization and digitalization projects.

Projected Transformer and Equipment Orders from 2026 to 2028: Capturing Grid Modernization Trends

From 2026 through 2028, GE Vernova projects sustained double-digit organic growth, with revenue targets reaching approximately $52 billion by 2028. A significant contributor to this outlook is the anticipated increase in transformer and advanced grid equipment orders driven by regulatory mandates and utility capital expenditure programs worldwide.

Grid modernization initiatives, supported by frameworks such as the Inflation Reduction Act in the U.S. and parallel policies internationally, have elevated rate-base investment models that incentivize utilities to upgrade aging infrastructure. This regulatory environment provides GE Vernova with a multi-year demand pipeline for advanced transformers, switchgear, and digital control solutions tailored to smart grid implementation.

Financial reporting indicates a clear uptick in booked orders related to these initiatives, reflecting strong government backing, improving project economics, and increased urgency around grid resiliency and electrification. Backlog data corroborate this upgrading trend, showing increasing order inflows for distribution and transmission equipment essential for integrating renewables and facilitating flexible load management.

Linking Turbine Utilization Rates to the Data Center-Driven Surge in Electricity Demand

GE Vernova’s flexible gas turbine portfolio is uniquely aligned to complement renewable energy growth, offering rapid startup and load-following capabilities that support grid stability amid increasing intermittent supply. This product positioning is critical as expanding data center footprints push the envelope on continuous, reliable power consumption.

Data center demand, particularly for AI processing power, has significantly increased turbine utilization rates, as these facilities impose stringent requirements on power availability and quality. The company’s gas turbines are well-suited for these scenarios, creating a synergistic relationship where renewable penetration and data center growth jointly elevate the need for flexible thermal generation capacity.

Moreover, ongoing electrification in digital infrastructure translates to downstream demand for transformers and grid controls, further enhancing asset utilization across segments. The interplay between turbine output profiles and data center operations confirms the robustness of current orders and validates revenue assumptions embedded in multi-year guidance.

Multi-Year Backlog Composition and Its Role in Sustaining Financial Guidance

GE Vernova’s backlog visibility is a strategic asset, with contractual commitments structured across multi-year horizons that span hardware supply, installation, and after-market services. This composition ensures a steady cadence of recognized revenue, mitigating execution risk common in project-driven industries.

Backlog analysis indicates a well-diversified project mix that includes long-term agreements with utilities and hyperscale data center operators, embedding recurring revenue streams from maintenance and digital services. This model reduces volatility and provides enhanced confidence in achieving 2025 and 2026 financial targets, such as adjusted EBITDA margin expansion and free cash flow growth.

The conversion of these backlogs into revenue is further supported by accelerating execution on delivery schedules and increased operational efficiency. However, it is critical to monitor execution timelines closely, given the high valuation multiples currently assigned to the stock—any delays or backlog slippage could materially impact investor sentiment and underscores the need for meticulous backlog management.

Impact of AI Data Center Expansion on Turbine and Transformer Demand: Market Drivers and Implications

The rapid expansion of AI-driven data centers acts as a powerful tailwind for GE Vernova, with these facilities’ substantial electricity consumption driving heightened demand for turbine capacity and grid infrastructure equipment. As machine learning workloads scale exponentially, the need for consistent, high-quality power becomes paramount.

This demand surge stimulates incremental orders for gas turbines designed for flexible operation and advanced transformer technologies capable of managing complex power flows associated with dynamic loads. The direct correlation between AI growth and order intake manifests in order booking patterns and reinforces the company’s strategic emphasis on electrification and grid modernization.

Furthermore, the underlying market drivers—such as increasing data center density, 24/7 uptime requirements, and expanding geographic footprint—suggest that this demand is not transient but rather part of an evolving energy ecosystem. GE Vernova’s ability to capitalize on these phenomena through tailored product offerings and timely capacity expansions positions it advantageously in both financial and strategic dimensions.

Together, these insights into GE Vernova’s order pipeline and demand fundamentals illustrate the company’s embeddedness within the AI grid supercycle. The strong multi-year backlog, supported by technology-aligned product portfolios and favorable regulatory conditions, undergirds the financial guidance and validates the firm’s strategic growth roadmap. Notably, the Electrification segment is driving the strongest revenue growth, outperforming the Power and Wind segments with a year-over-year organic growth rate of 29%, compared to 16% in Power and a decline of 25% in Wind [Chart: Segment Revenue Growth Rates]. The following subsection will build upon this foundation by examining how strategic partnerships and geographic expansion further amplify these growth vectors.

Expansive Alliances and Strategic Acquisitions Fueling GE Vernova’s Global Growth Trajectory

This subsection delves into how GE Vernova is leveraging partnerships and acquisitions to broaden its geographic footprint, enhance technology capabilities, and accelerate growth in key markets such as India and North America. It examines specific joint ventures, acquisition pipelines targeting next-generation energy technologies, and international collaborations that are integral to the company’s strategy to capitalize on evolving energy transition demands and grid modernization opportunities.

Recent Joint Ventures Anchoring GE Vernova’s Strategic Expansion in India’s Energy Market

GE Vernova has actively pursued joint ventures as a foundational element of its growth strategy in India, a pivotal market undergoing rapid energy infrastructure transformation. The formation of GE Vernova T&D India Limited illustrates a purposeful integration of advanced technology to optimize power conversion and enhance renewable energy stability. This joint venture is designed to address India’s growing electricity demand, specifically focusing on intelligent solar and storage solutions that mitigate variability in renewable supply chains.

These collaborative efforts in India serve to amplify the company’s operational presence while navigating local regulatory frameworks and supply chain complexities. By combining global expertise with domestic market insights, GE Vernova enhances its ability to deploy scalable electrification and grid modernization solutions. The partnership’s footprint extends beyond technology transfer, encompassing workforce development and long-term infrastructure planning aligned with India’s national energy goals.

Acquisition Pipeline Targeting Next-Generation Technologies to Broaden Market Access and Innovation

GE Vernova’s acquisition strategy is tailored to augment its portfolio with cutting-edge technologies that complement its existing competencies in power generation and electrification infrastructure. The acquisition of full ownership of transformer manufacturer Prolec exemplifies the company’s intent to consolidate capabilities in grid infrastructure, particularly in North America where demand for advanced transmission equipment is accelerating.

Future acquisition prospects emphasize not only incremental capacity expansion but also entry into emerging domains such as digital grid management and AI-enabled operational tools. This forward-focused pipeline is expected to generate synergistic effects by integrating innovative technologies that improve equipment efficiency, enhance predictive maintenance, and expand service offerings. Careful selection of acquisition targets ensures alignment with GE Vernova’s multi-year revenue visibility and sustainability objectives.

Geographic Footprint Expansion through Strategic International Collaborations Emphasizing Grid Modernization

GE Vernova is advancing its global reach through strategic alliances that facilitate mutual enhancement of technical competencies and geographic coverage. Collaborations with international leaders in energy infrastructure, such as those akin to the recent agreements between major players in Europe and Asia, underscore the company’s emphasis on accelerating grid reliability and integrating renewable energy.

These partnerships often focus on projects involving high-voltage alternating current (HVAC) systems critical for cross-border electricity transmission and grid resilience. By aligning with regional partners, GE Vernova leverages shared expertise to tailor solutions for complex energy landscapes shaped by growing electrification needs and variable renewable supply. This approach also reduces market entry barriers, allowing more agile responses to regulatory environments and customer requirements in diverse economies.

Projected Financial Impacts and Growth Prospects from New Alliances and Portfolio Expansion

The synergistic effect of GE Vernova’s joint ventures, acquisitions, and collaborations is forecasted to contribute significantly to both near-term revenue growth and long-term market positioning. The expanded presence in high-growth regions, combined with bolstered product offerings, supports revenue visibility through a diversified and growing backlog in Power and Electrification segments.

Evidence indicates that these initiatives will help insulate the company from volatility associated with any single market or technology domain, while enabling scale economies and innovation adoption. Analysts anticipate material contributions to earnings uplift from transformer capacity expansions as well as increased service contracts associated with newly integrated product lines. Overall, the portfolio expansion not only fosters sustainable growth but strategically positions GE Vernova to capture emergent opportunities driven by AI-enabled grid supercycles and electrification trends.

Having detailed how GE Vernova’s partnerships and acquisitions serve as critical levers for its strategic growth and competitiveness, the report now transitions to examining the regulatory landscape and policy alignments that shape the operating environment and influence these collaborative endeavors.

Regulatory Advocacy and Policy Alignment: Steering Energy Transition through Strategic Engagements and Risk Mitigation

This subsection analyzes GE Vernova’s proactive regulatory advocacy and policy alignment strategies that shape its operational environment amid evolving energy transition legislation. It elucidates the company’s interface with governmental bodies to influence favorable frameworks, manage dependency on subsidies, mitigate regulatory risks, and ensure coherence with federal and state priorities. Positioned within the 'Strategic Initiatives Driving Sustainable Growth' section, this discussion reveals how regulatory engagement underpins the sustainability and scalability of GE Vernova’s growth trajectories.

Targeted Lobbying Efforts on Inflation Reduction Act Policy Updates

GE Vernova has strategically concentrated its lobbying activities around pivotal updates and implementations of the Inflation Reduction Act (IRA), recognizing the act’s profound impact on renewable energy incentives and grid modernization mandates. The company maintains ongoing engagement with federal and state legislators to safeguard and optimize the deployment of tax credits and subsidies essential for renewable and electrification projects. This includes advocating for clarity in IRA provisions that directly affect project financing, equipment manufacturing, and eligibility criteria, thus securing a stable policy environment that upholds demand for GE Vernova’s technologies.

These lobbying initiatives also extend to participation in consultations and legislative hearings where the firm contributes technical expertise to shape practical and effective regulatory outcomes. By actively influencing the evolving legislative framework, GE Vernova mitigates risks associated with abrupt policy shifts and sustains momentum across its key business segments.

Influencing Grid Modernization Legislation and Regulatory Approvals

GE Vernova’s advocacy encompasses efforts to expedite and streamline grid modernization laws, recognizing that regulatory bottlenecks and lengthy permitting processes significantly delay infrastructure deployment. The company collaborates with policymakers to address administrative barriers, emphasizing the necessity of digitalization and policy reforms that accelerate transmission project approvals without compromising system reliability or community engagement.

Particular attention is given to fostering regulatory frameworks that enable anticipatory investments in grid assets, including offshore wind hubs and smart grid technology integration. GE Vernova supports legislative initiatives that better allocate costs and benefits of cross-border grid projects, thereby enabling scalable infrastructure expansion aligned with decarbonization goals. By engaging at multiple government levels, the company aligns its advocacy with broader federal infrastructure priorities, enhancing coherence and regulatory predictability.

Subsidy Dependency Reduction and Strategic Risk Management

While GE Vernova benefits substantially from renewable energy subsidies and tax incentives, it recognizes the inherent risks stemming from potential reductions or policy revisions in these supports. The company is implementing strategies to reduce reliance on fluctuating subsidies by focusing on operational excellence, cost competitiveness, and customer-centric solutions that enhance intrinsic market value beyond regulatory inducements.

This includes diversifying revenue sources across generation and grid technologies and investing in innovations that improve project economics independently of incentives. Moreover, GE Vernova monitors policy developments closely to anticipate regulatory risks, enabling agile adjustment of capital allocation and project pipelines. This forward-looking approach ensures resilience against regulatory volatility and aligns financial sustainability with evolving legislative landscapes.

Proactive Identification and Mitigation of Emerging Regulatory Risks

GE Vernova’s regulatory affairs teams employ continuous horizon scanning to identify emerging legislative and regulatory risks, including local opposition to grid infrastructure, evolving environmental standards, and potential changes in clean energy definitions and eligibility rules under government programs. By integrating legal analysis with policy forecasting, the company anticipates challenges that could impact project timelines, cost structures, and permit approvals.

Mitigation measures include active stakeholder engagement, participation in regulatory consultations, and collaboration with industry consortia to promote balanced standards. GE Vernova prioritizes transparent communication with regulators and communities to preempt opposition and facilitate smoother project execution, thereby safeguarding its strategic initiatives from unexpected regulatory headwinds.

Alignment of Federal and State-Level Advocacy with Corporate Growth Pillars

GE Vernova ensures its regulatory advocacy efforts are tightly aligned with its corporate growth pillars—Power, Wind, and Electrification—by coordinating federal engagement with state and local lobbying activities. This multi-level approach acknowledges the complex U.S. regulatory ecosystem where policies affecting energy transition vary widely across jurisdictions.

By tailoring advocacy strategies to specific regional priorities, such as equitable subsidy access, grid interconnection rules, and environmental compliance standards, the company fosters policy environments conducive to scalable deployment of its technologies. The harmonization of advocacy efforts across government layers maximizes policy impact, advances legislative coherence, and bolsters GE Vernova’s competitive positioning in a fragmented regulatory landscape.

Cumulatively, GE Vernova’s regulatory advocacy and policy alignment initiatives serve as critical enablers for its strategic growth, underpinning the company’s capacity to navigate complex and evolving legislative terrains. The ability to influence policy, mitigate subsidy dependency, and preempt regulatory risks complements its technological and market innovations, setting a robust foundation for sustained leadership in the accelerating energy transition.

5. Risk Assessment and Mitigation Strategies

Persistent Structural Vulnerabilities in Wind Segment: Quantification, Cost-Restructuring Paths, and Asset Lifecycle Alignment

This subsection critically examines the enduring profitability challenges within GE Vernova's Wind business segment, which despite being the smallest sector, significantly drags on consolidated margin progression. It quantifies recent EBITDA losses, evaluates cost-restructuring initiatives designed to restore financial health, and aligns these actions within the broader context of asset lifecycle management to ensure sustainable operational transformation. This analysis advances the report's broader risk framework by pinpointing where GE Vernova must focus remediation to deliver on its energy transition ambitions without compromising overall financial performance.

Quantifying Wind Segment EBITDA Losses and Their Evolution Through 2026

GE Vernova's Wind segment has continued to register substantial EBITDA deficits, with reported losses hovering around $600 million in 2025. This level of structural unprofitability persists amid organic revenue declines of approximately 25% and EBITDA margins deteriorating from already negative levels to near -27%. The guidance for 2026 anticipates similar EBITDA losses, signaling the segment's entrenched challenges in meeting profitability benchmarks despite incremental improvements in onshore wind operations.

The Wind segment’s EBITDA drag materially undermines the company-wide margin expansion efforts evident in Power and Electrification. While costs stabilize and offshore wind losses marginally recede due to backlog realization and productivity enhancements, the segment remains the primary contributor to margin compression risks. This persistent underperformance despite operational adjustments underscores the difficulties in scaling profitability within a business burdened by contract cancellations and pricing pressure on offshore projects.

This ongoing struggle is further reflected in margin projections through 2028, where the Wind segment’s EBITDA margin is expected to remain deeply negative at approximately -26%, contrasting sharply with improving margins in Electrification and Power segments, which are projected at 19% and 17.5% respectively [Chart: Projected EBITDA Margin Improvement by Segment].

Cost-Restructuring Measures: Strategies Targeting Operational Efficiency and Portfolio Optimization

In response to continued Wind segment losses, GE Vernova has proposed an array of cost-restructuring initiatives aimed at reversing the negative EBITDA trend. These measures include streamlining offshore wind development activities, renegotiating supplier contracts to extract better pricing, and optimizing fixed operating expenses through headcount rationalization and facility consolidations. The company is accelerating productivity programs focused on design simplification and manufacturing efficiency gains intended to lower unit costs and improve competitive positioning.

Strategic portfolio adjustments also figure prominently, with management considering divestiture or partnership models to offload underperforming offshore wind assets. This approach aims to reduce capital intensity and capitalize on opportunities to collaborate with specialized players who could bring fresh investment and expertise. Together, these operational and strategic levers are designed to curtail the Wind segment’s cash burn, improve margin trajectories, and integrate its footprint more effectively within GE Vernova’s broader electrification and power ecosystem.

Asset Lifecycle Planning as a Framework for Sustainable Wind Business Restructuring

Aligning cost-restructuring efforts with asset lifecycle management principles is critical to balancing near-term financial repair with long-term operational viability. GE Vernova’s asset lifecycle approach emphasizes extending asset useful life through maintenance optimization, technology upgrades, and scheduled recapitalizations to maximize return on invested capital. In the Wind segment, this translates into prioritizing lifecycle cost control on wind turbine components and infrastructure, deploying predictive maintenance programs, and rationalizing asset portfolios based on lifecycle condition and obsolescence risk.

This lifecycle-centric restructuring framework supports a phased wind turnaround strategy, enabling the company to defer capital-intensive upgrades until profitability stabilizes while safeguarding critical operational reliability. It also underpins the decision-making process regarding which assets to divest versus retain, ensuring that portfolio optimization decisions are grounded in rigorous condition and utilization assessments. This integrated lifecycle perspective strengthens the ability to make informed trade-offs between cost reduction urgency and sustaining future revenue-generating capacity within the Wind domain.

Having established the depth and persistence of structural challenges in GE Vernova’s Wind segment, alongside the company’s multidimensional cost-restructuring and asset management responses, the subsequent subsection will explore execution and operational risks that may compound or mitigate these structural issues, thereby shaping delivery outcomes across all segments.

Execution and Operational Risks: Navigating Supply Chain Volatility and Talent Retention Challenges with Robust Contingency Protocols

This subsection critically examines the key operational risks constraining GE Vernova’s project execution, focusing on supply chain vulnerabilities, talent retention dynamics, and the adequacy of contingency mechanisms. Understanding these factors is essential to gauge the company's resilience in meeting its growth projections amid mounting external and internal pressures.

Supply Chain Disruptions from 2024 to 2026: Sources, Frequency, and Operational Impact

Between 2024 and early 2026, GE Vernova’s supply chain has been significantly affected by a constellation of geopolitical, logistical, and environmental disruptions. The enduring closure and partial congestion of critical shipping lanes, such as ongoing traffic suppression through the Red Sea corridor and the Suez Canal, have elevated freight transit times by up to two weeks on key Asia-Europe and Asia-U.S. routes. This phenomenon has led to steep increases in shipping costs, surging 100% to 350% on several lanes, while operational expenses have surged by millions per vessel per extended routing. These disruptions have cascaded into delays for oversized equipment delivery, such as turbines and transformers, which are highly sensitive to bulky freight logistics.

Furthermore, the global maritime sector has confronted compounding challenges including cyberattacks on port infrastructure, deepening riverbed navigability issues, and persistent labor shortages across logistical hubs. These factors have collectively intensified unpredictability in supply availability and execution timelines, straining the supply chain’s agility. The compounded effect is a structural shift away from previous routing efficiencies, compelling strategic rerouting and recalibration of inventory buffers at project sites. This volatile environment demands increased supply chain transparency and dynamic risk monitoring to mitigate cost overruns and schedule slippages in capital-intensive projects.

Talent Retention and Turnover: Quantitative Assessment of Human Capital Risks

The energy infrastructure sector’s competitive talent landscape has pressured GE Vernova’s workforce stability, notably in engineering, project management, and technical operations roles vital for delivery excellence. Between 2024 and 2026, the company experienced elevated attrition rates driven by aggressive industry hiring, wage inflation, and evolving employee expectations around flexibility and development. Industry-wide, hiring costs rose approximately 10% year-over-year in 2024, a trend that continued into 2025, squeezing operational budgets and increasing recruitment lead times.

Analysis of retention metrics reveals particular strains in niche technical domains, where turnover rates have exceeded internal benchmarks by up to 15% in recent periods. This attrition exposes projects to knowledge gaps, ramp-up delays, and risks to quality control. GE Vernova's efforts to mitigate these pressures include enhanced talent acquisition strategies, targeted retention incentives, and investments in workforce development programs. However, the capacity to sustain these initiatives at scale remains a critical variable affecting the company’s operational risk profile over the medium term.

Contingency Protocols for Project Delays: Robustness and Areas for Enhancement

In response to ongoing operational disruptions, GE Vernova has instituted a series of contingency frameworks designed to buffer schedule delays and cost overruns. These include dynamic supplier diversification strategies, advanced inventory staging closer to project sites, and accelerated digital tracking of critical component shipments enabling real-time responsiveness to supply glitches.

Moreover, the company leverages predictive analytics to foresee potential bottlenecks and reallocate resources promptly. Cross-functional crisis management teams are empowered to enact rapid decision-making protocols during emergent delays. Despite these efforts, challenges persist in fully insulating large-scale capital projects from cascading risks, especially in the wind segment where component complexity and transportation scale amplify exposure.

Recommendations for strengthening contingency protocols underscore the need for deeper integration with upstream suppliers to co-develop risk-mitigating capabilities, enhanced scenario planning incorporating geopolitical variables, and scaling agile workforce deployment models to rapidly compensate for talent shortfalls. These improvements are critical to safeguarding GE Vernova’s delivery commitments amid a persistently volatile operational landscape.

Addressing execution and operational risks through these multifaceted lenses prepares the foundation for a broader assessment of structural business challenges and financial sustainability concerns that imperil GE Vernova’s progression. The efficacy of these mitigation efforts will directly influence the company’s capacity to capitalize on growth drivers within the evolving energy transition.

Dissecting Cash Quality and Free Cash Flow Sustainability Amidst Shifting Capital Allocation

This subsection critically evaluates GE Vernova's cash flow profile for 2025 and beyond, emphasizing the distinction between working-capital-driven cash inflows and truly recurring free cash flow. Understanding this distinction is key to assessing the sustainability of cash generation underpinning the company's capital allocation decisions and long-term financial stability.

Breakdown of 2025 Cash Flow: The Working Capital Inflow Factor

GE Vernova's reported free cash flow of $3.7 billion in 2025, while substantial in headline terms, masks a critical quality issue: reliance on a $4.1 billion working capital inflow largely sourced from contract liabilities. This inflow functioned as a non-recurring cash boost rather than reflecting cash generated organically through operations. When adjusted for this factor, the company’s underlying free cash flow from core operations appears constrained, highlighting a temporal imbalance between cash inflows and outflows.

The prominence of working capital dynamics suggests that a significant portion of the cash surge originated from timing-related factors such as upfront customer payments and deferred revenue recognition rather than sustained operational earning power. This cash flow composition raises concerns over its repeatability in subsequent periods and implies vulnerability to fluctuating contract schedules and revenue recognition patterns.

Capital Allocation Shifts in Response to Cash Flow Realities Post-2025

In light of the atypical 2025 cash flow profile, management has signaled recalibrations in capital deployment, prioritizing prudent liquidity management to safeguard financial flexibility. These adjustments include cautious increases in restructuring provisions and measured spending on growth initiatives, aligning capital outlays more closely with recurring cash generation rather than relying on one-off working capital releases.

The ongoing Wind segment losses and their drag on consolidated margins have intensified the need for stricter allocation discipline. Consequently, investments are increasingly weighted toward segments demonstrating robust cash conversion, such as Electrification, while incremental capital toward restructuring and technology innovation seeks to address structural inefficiencies and unlock longer-term value.

Assessing the Sustainability of Recurring Free Cash Flow Beyond Transitory Boosts

Sustainability analysis points to limited free cash flow growth in upcoming fiscal years without comparable working capital inflows. The current backlog and reorder pipeline offer some visibility; however, the transition to cash flow purely driven by operational earnings remains a challenge. This is compounded by structural headwinds in the Wind segment, which continues to report EBITDA losses, complicating consolidated margin expansion and cash generation consistency.

To bridge this gap, the company’s strategy focuses on enhancing cash flow conversion rates by optimizing operational efficiencies, tightening working capital cycles, and leveraging innovation in grid and Electrification technologies that carry higher margin prospects. Nevertheless, investors and management alike must remain cognizant that until these measures yield scale effects, free cash flow targets may be susceptible to volatility and contingent on effective execution of backlog conversion.

Understanding the nuances and limitations of GE Vernova’s current cash flow composition and capital allocation underpins the subsequent risk assessment. It clarifies financial constraints that may temper aggressive growth ambitions and informs mitigation strategies to stabilize and enhance cash flow quality moving forward.

6. Future Outlook and Strategic Imperatives

Forecasting Robust Growth: Revenue, Profitability, and Cash Flow Targets Through 2030

This subsection rigorously outlines GE Vernova's long-term financial projections, providing clarity on expected revenue growth, EBITDA margin expansion, and free cash flow generation through 2030. These metrics are pivotal for evaluating how well the company’s financial ambitions align with its strategic positioning in the evolving energy transition landscape, offering stakeholders quantifiable benchmarks for assessing future value creation.

Projected Revenue Milestones for 2028–2030 Reflect Accelerated Organic Growth

GE Vernova's revenue trajectory through the late 2020s is characterized by strong compound annual growth underpinned by sustained organic expansion and market demand shifts driven by energy transition imperatives. By 2028, management targets reaching approximately $52 billion in annual revenue, representing a marked increase from the mid-$40 billion guidance for 2026. This reflects a strategic shift to low-double-digit organic growth rates, an acceleration from the high-single-digit growth rate anticipated for 2026. The enhanced topline outlook is driven primarily by scaling Electrification and Power segments, bolstered by infrastructure modernization and renewable integration projects.

The company’s emphasis on organic growth rather than acquisition-driven expansion signals confidence in internal innovation, product development, and market penetration initiatives. These revenue targets assume sustained demand for grid modernization equipment, digital asset deployments, and renewable energy infrastructure, specifically reflecting persistent growth in data-center energy solutions and transformer demand. Such ambitious revenue benchmarks align GE Vernova’s commercial capabilities with the expanding global decarbonization economies, enabling the company to capitalize on the evolving grid and energy ecosystem.

EBITDA Margin Expansion to 20% Signaling Enhanced Operational Leverage and Profitability