From Monopoly to Multiplicity: The Unraveling of the Microsoft-OpenAI Alliance Amidst Legal Challenges and Strategic Realignment

Table of Contents

- Executive Summary

- Introduction

- 1. From Monopoly to Multiplicity: The Unraveling of the Microsoft-OpenAI Alliance Amidst Legal Challenges and Strategic Realignment

- 2. Diagnosing the Drivers Behind the Restructuring

- 3. Strategic Implications and Adaptive Pathways

- 4. Future Trajectories and Decision Frameworks

- 5. Synthesis and Actionable Insights

- Conclusion

Executive Summary

Since 2019, Microsoft has held an exclusive cloud partnership with OpenAI, underpinning the rapid expansion of AI capabilities through integrated large language model deployment on the Azure platform. This arrangement provided Microsoft with a dominant market position, reflected in OpenAI-powered services accounting for approximately 87% of AI chatbot traffic as recently as early 2025. However, strategic shifts culminating in April 2026 have ended this exclusivity, enabling OpenAI to deploy models across major cloud providers including Amazon Web Services and Google Cloud. Consequently, Microsoft’s share of AI chatbot traffic has declined to roughly 65%, signaling a significant transformation in the competitive landscape.

Key contractual changes include the removal of Artificial General Intelligence (AGI)-triggered clauses previously linking Microsoft’s intellectual property rights and revenue shares to OpenAI’s AGI milestones, replaced by capped and predictable revenue sharing arrangements valid through 2030. Microsoft’s equity stake in OpenAI has been strategically diluted, balancing reduced ownership influence against extended model licensing rights through 2032. This transition reflects critical financial recalibrations amid growing compute cost pressures, legal disputes—most notably relating to Amazon’s $50 billion AI cloud partnership with OpenAI—and a complex regulatory environment. The partnership restructuring underscores broader AI ecosystem fragmentation, necessitating adaptive governance, diversified infrastructure investments, and proactive regulatory engagement to sustain competitive advantage and innovation momentum.

Introduction

Artificial intelligence (AI) has rapidly transitioned from emerging technology to a central pillar transforming industries, economies, and societal interactions. At the forefront of this revolution sits OpenAI, a leading developer of large language models (LLMs), and its pivotal partnership with Microsoft, historically cemented by exclusive cloud hosting and mutually reinforced innovation investments. This alliance shaped early AI market architectures, driving unprecedented product breakthroughs and securing dominant shares in AI application traffic.

However, from 2023 onward, the AI industry has experienced pronounced fragmentation, characterized by a proliferation of alternative LLM developers, diversified compute infrastructures, and rising multi-vendor deployment strategies. This shift challenges traditional exclusivity models, distills competitive advantage into ecosystem orchestration rather than singular control, and rewires the strategic calculus for entrenched partnerships.

Against this backdrop, the Microsoft-OpenAI partnership has undergone significant reconfiguration culminating in the formal termination of Microsoft’s exclusive cloud provider status in April 2026. The restructured agreement revises revenue sharing, licensing rights, and governance frameworks, reflecting a pragmatic response to escalating compute costs, legal challenges associated with new third-party alliances, and evolving regulatory scrutiny. These developments raise critical questions regarding the sustainability of monopolistic AI alliances, the governance of emerging hybrid infrastructures, and strategies for navigating regulatory uncertainties.

This report aims to diagnose the evolving dynamics of the Microsoft-OpenAI relationship, analyzing the symptomatic shifts, underlying drivers, and strategic implications amidst a fast-changing AI landscape. By synthesizing quantitative data on market share evolution, contractual amendments, financial structures, and legal disputes, this analysis provides stakeholders with insights to anticipate future trajectories and adapt effectively to a multipolar AI ecosystem.

Infographic Image: Infographic

1. From Monopoly to Multiplicity: The Unraveling of the Microsoft-OpenAI Alliance Amidst Legal Challenges and Strategic Realignment

The AI Industry Landscape: From Closed Ecosystems to Fragmented Platforms

This subsection establishes the foundational context by examining the ongoing transformation of the AI industry from predominantly closed, exclusive partnerships toward an increasingly fragmented and pluralistic market architecture. Understanding this broader shift is essential to grasp the strategic recalibration seen in the Microsoft-OpenAI alliance and the wider competitive pressures reshaping AI development, infrastructure deployment, and platform strategies.

Quantifying the Rise of Alternative Large Language Model Developers (2019–2026)

Since 2019, the AI landscape has seen a surge in the number and diversity of large language model developers challenging the early dominance of a select few incumbents. The expansion is notable both qualitatively and quantitatively: from a handful of pioneers, the market now supports dozens of LLM vendors ranging from specialized startups to established tech conglomerates. This proliferation has accelerated especially after 2023, driven by lower entry barriers in model training and the availability of diverse datasets and compute resources.

The increase in alternative developers—from companies pioneering novel architectures like Anthropic to regional players offering differentiated AI solutions—has introduced competing approaches to language understanding, ethical guardrails, and domain-specific applications. Importantly, this growth has also been accompanied by a more fragmented notion of AI leadership, where no single entity controls all layers of the stack, thereby decentralizing innovation and diversifying risk.

Evolving Compute Resource Diversification Across AI Firms

Computational infrastructure constitutes a critical bottleneck and differentiator in AI development. Historically, exclusive cloud partnerships concentrated significant AI workloads within a single provider’s ecosystem, reinforcing market lock-in and limiting flexibility. However, the past few years have witnessed a deliberate diffusion of compute dependencies through multi-cloud strategies and bespoke data centers.

OpenAI's recent negotiations illustrate this trend, where computation is no longer confined to a sole cloud partner but distributed across providers such as Microsoft Azure, Amazon Web Services, and Google Cloud. Furthermore, emerging initiatives like OpenAI's Stargate data center project signal a move toward hybrid infrastructure models that combine internal capacity with external cloud partnerships. This diversification reflects both the sheer scale of compute required for contemporary models and strategic hedging against cloud vendor dependency risks.

Analyzing Market Share Impact Due to AI Platform Fragmentation

The gradual erosion of exclusivity has reshaped competitive dynamics, transforming what were once near-monopolies into contested marketplaces. Data from AI search engines and LLM deployments reveal that while early first movers like ChatGPT (OpenAI) retain substantial market share, their dominance has diminished significantly, ceding ground to competitors such as Google Gemini, Anthropic Claude, and specialized platforms like Perplexity.

This fragmentation impacts customer acquisition, partnership formation, and model integration. Market share fluctuations indicate a maturing industry where differentiated capabilities and ecosystem alignment increasingly dictate competitive advantage. For instance, ChatGPT’s share in AI chatbot traffic reduced from about 87% to roughly 65% within twelve months, exemplifying a rapid multi-polar market evolution. These dynamics compel incumbent players to reconsider exclusivity arrangements and explore more open, cooperative models.

Tracing the Decline of Exclusivity in AI Partnerships Since 2023

Once a key strategic anchor, exclusivity between cloud providers and AI developers has steadily diminished post-2023, driven by growing cost pressures, regulatory scrutiny, and the increasing compute demands of cutting-edge AI models. The initial appeal of exclusive cloud partnerships was predicated on accelerating innovation and capturing integrated revenues. However, these arrangements have proven difficult to sustain amid escalating infrastructure costs and broader market demands.

The Microsoft-OpenAI relationship provides a case study in this evolution. Early deals locked exclusivity into multi-year contracts emphasizing close integration. Yet recent contract restructurings explicitly remove such exclusivity, permitting OpenAI’s deployment across rival clouds while preserving baseline rights for Microsoft. This shift reflects pragmatic realignments, balancing access to AI innovation with economic and legal realities in an increasingly competitive ecosystem.

Infrastructure Heterogeneity as a Catalyst for Innovation and Strategic Market Shifts

Diverse infrastructure models—from specialized AI accelerators to varied cloud platforms—enable differentiated innovation pathways. Fragmented AI ecosystems introduce flexibility in resource allocation, resilience against supplier disruptions, and opportunities for vertical innovation across chips, data centers, and software interfaces.

This heterogeneity undermines legacy assumptions of vendor lock-in and rekindles strategic experimentation, fostering hybrid partnerships and open-source contributions. It also precipitates a broader redistribution of influence from purely proprietary AI stacks toward collaborative frameworks that blend public and private resources. The consequence is a less centralized but more robust AI innovation landscape, intensifying competition and offering end-users varied points of entry.

Having established how the AI industry is shifting towards a fragmented, pluralistic model with multiple competing cloud partnerships and diverse compute strategies, the report now narrows its focus to the manifestation of these trends in the high-profile restructuring of the Microsoft-OpenAI partnership. This transition enables a detailed examination of how observed industry dynamics concretely influence the terms, scope, and strategic logic of this key alliance’s evolution.

Symptoms of Change: Documenting the Microsoft-OpenAI Partnership Shift

This subsection systematically documents the key observable transformations in the Microsoft-OpenAI relationship, marking a departure from their historically exclusive and tightly integrated collaboration. By detailing the timeline of contract renegotiations, removal of exclusivity clauses, adjustments to revenue-sharing models, and termination of artificial general intelligence (AGI) conditional provisions, this analysis establishes the factual baseline needed to diagnose underlying strategic and legal drivers later in the report.

Timeline and Termination of Microsoft Exclusive Cloud Partnership

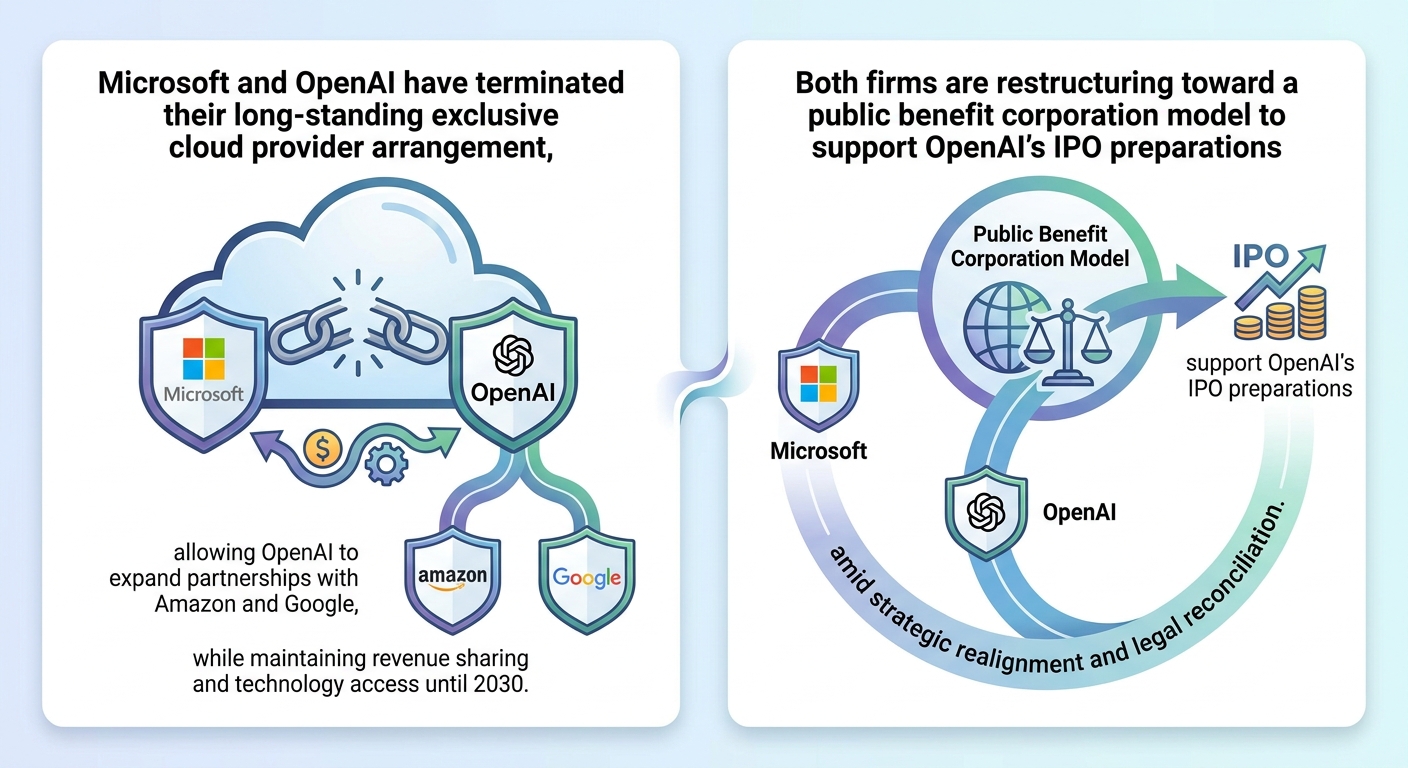

The exclusivity that Microsoft historically held as OpenAI’s sole cloud partner concluded abruptly in late April 2026, marking a significant shift in the strategic alliance. From 2019 until early 2026, Microsoft operated as the exclusive host and distributor of OpenAI’s large language models and related AI products on its Azure cloud platform. However, the updated agreement signed in late April 2026 ended this exclusivity, permitting OpenAI to deploy its technology across other major cloud providers, including Amazon Web Services and Google Cloud. Despite this, Microsoft retained status as OpenAI’s primary cloud partner with preferential first release of new AI products on Azure, subject to conditions of technical feasibility and rollout decisions by Microsoft. This shift capped nearly seven years of exclusive lock-in and set the stage for OpenAI’s operational independence in infrastructure choices.

Negotiations leading to this revocation of exclusivity began in mid-2025 as OpenAI sought to diversify its infrastructure sources to meet exploding compute demands. By September 2025, a memorandum of understanding was reached to restructure enterprise deployment, with formal contract amendments finalized by April 2026. This timeline reflects a measured transition balancing Microsoft’s strategic interests against OpenAI’s scaling imperatives amid unprecedented AI infrastructure costs.

Removal of Artificial General Intelligence (AGI) Clauses and Contractual Impact

A pivotal contractual change in the renegotiation was the elimination of the AGI-triggered clauses that previously conditioned Microsoft’s intellectual property (IP) rights and revenue arrangements on OpenAI’s attainment of artificial general intelligence benchmarks. Originally, these clauses granted Microsoft extended IP rights and revenue shares contingent on OpenAI achieving AGI milestones, a loosely defined but strategically critical threshold implying near-human level AI capabilities.

With the renewal, all AGI-related contingency language was excised, transferring certainty back to Microsoft’s royalty streams irrespective of OpenAI’s technology progression, yet capping total revenue share payments through 2030. Such removal reduced ambiguity around future partnership obligations and mitigated potential trigger events that could have strained corporate governance or escalated legal risk. From Microsoft’s perspective, while it relinquished leverage tied to prospective AGI developments, it secured steady revenue flow insulated from speculative rapid breakthroughs.

This alteration underscored OpenAI’s desire for operational autonomy and signaling the maturation of AI model licensing into a more transactional, less milestone-dependent framework. Additionally, it reflects broader AI industry skepticism about imminent AGI realization timelines, and a pragmatic pivot toward near-term commercialization.

Revised Revenue Sharing Terms and Financial Implications Through 2030

The revamped partnership extended Microsoft’s rights to license OpenAI technologies and models through 2032, although under a non-exclusive arrangement permitting OpenAI to monetize across competing cloud infrastructures. Revenue sharing payments from OpenAI to Microsoft remain in force through 2030 but are strictly capped and independent of OpenAI’s AI performance metrics or achievements. This shift delinks financial flows from technology milestones that had previously introduced volatility.

From a financial standpoint, this modified revenue-sharing model preserves Microsoft’s income continuity from OpenAI’s commercial success but reduces upside tied to exclusivity or AGI breakthroughs. Analysts view this as balancing Microsoft’s investment protection with OpenAI’s broader market reach ambitions, reflecting an implicit wager on the growth potential of multi-cloud AI services underpinned by OpenAI’s flagship models.

The revenue cap and fixed payment percentage symbolize a strategic trade-off: Microsoft sacrifices the exclusivity premium for a predictable, ecosystem-friendly revenue stream that supports its positioning as a key AI infrastructure provider while allowing OpenAI to scale rapidly across industry platforms.

Negotiation Milestones Shaping the New Agreement (Mid-2025 to Early 2026)

The partnership’s restructuring was preceded by a series of high-stakes negotiations starting in mid-2025. Early in that period, OpenAI proposed capping Microsoft’s equity ownership at 33% in exchange for forgoing future profit rights, which Microsoft found unpalatable given its already significant $13+ billion investment. Conflict centered on the exclusivity terms, cloud hosting rights, and revenue sharing formulas.

A tentative agreement was reached via a memorandum of understanding in September 2025 indicating intent to shift toward multisourcing AI compute infrastructure. October 2025 saw Microsoft acquire an estimated 27% stake in OpenAI Group PBC at a valuation around $135 billion, simultaneously formalizing the removal of exclusive cloud provider rights. The final legal amendments, announced in April 2026, finalized these changes and removed contentious AGI clauses.

This multi-phase negotiation process reflects the complex strategic recalibration needed to reconcile Microsoft’s desire for durable AI leadership with OpenAI’s scaling requirements and commercial ambitions in a rapidly evolving market landscape. It was marked by private negotiations, investor scrutiny, and shifting industry alliances.

Immediate Financial and Competitive Impact for Microsoft

Following the announcement of the partnership restructuring in April 2026, Microsoft’s stock price declined nearly 3%, reflecting investor concerns about the dilution of exclusivity benefits and potential erosion of Microsoft’s AI moat. By relinquishing exclusive access, Microsoft sacrificed a clear product differentiation advantage that previously positioned Azure as the premier AI cloud platform.

However, Microsoft’s continuing license to OpenAI’s intellectual property through 2032 and ongoing primary cloud status mitigate near-term revenue risks. Analysts largely interpret the deal as a strategic rebalancing rather than a loss of AI leadership, noting that OpenAI’s multi-cloud approach acknowledges practical infrastructure scalability and cost distribution realities.

Moreover, Microsoft’s substantial commitments to alternative AI investments and partnerships, as well as deep integration of OpenAI technology throughout its product suite, sustain its competitive positioning despite the loss of exclusivity. The shift signals a more open AI ecosystem with broader cloud competition but solidifies Microsoft’s role as a major, though no longer singular, AI infrastructure provider.

The documented symptoms of changing contractual terms and alliance dynamics establish a clear factual foundation from which to diagnose the multifaceted pressures driving this strategic realignment. The next section will delve into the drivers behind these shifts, unpacking the interplay between safety considerations, financial imperatives, competitive positioning, and regulatory uncertainties that precipitated the dissolution of exclusivity and the recalibration of revenue and IP terms.

2. Diagnosing the Drivers Behind the Restructuring

Safety Concerns Versus Rapid Advancement: Navigating the AGI Debate Amid Strategic Realignments

This subsection probes the fundamental tension underpinning the restructuring of the Microsoft-OpenAI partnership: the balance between aggressively advancing toward artificial general intelligence (AGI) and ensuring rigorous safety measures. By dissecting technical disputes over AGI’s definition and timelines, assessing the trade-offs in development speed against safety imperatives, analyzing regulatory uncertainties, and illuminating internal governance changes, this segment unpacks how these dynamics drive strategic recalibration and partnership evolution.

Divergent AGI Definitions and Disagreement on Achievement Timelines

A core driver of the partnership restructuring centers on ongoing conflicts over what constitutes artificial general intelligence (AGI) and when it might realistically be attained. OpenAI and other leading AI stakeholders articulate differing benchmarks for AGI: some emphasize demonstration of human-level competency across a broad cognitive task set, whereas others adopt narrower metrics such as surpassing human performance on specialized professional exams. This definitional ambiguity fuels competing timelines, ranging from optimistic forecasts of AGI within the next five years to more cautious expectations extending well into mid-century.

These conflicting views on AGI timelines create strategic uncertainty for both parties. Microsoft, with its substantial investment and stake in OpenAI’s future, faces challenges in aligning its long-term AI infrastructure and product roadmaps with OpenAI’s evolving ambitions. Meanwhile, OpenAI's efforts to pace its development responsibly, against pressures for accelerated breakthroughs, hinge on clarifying internal AGI targets and external communication, as premature proclamations risk investor skepticism and reputational damage.

Balancing Accelerated AI Development with Robust Safety Protocols

The desire to expedite AI model deployment confronts the imperative to institute comprehensive safety assessments and risk controls. Rapid iteration facilitates competitive positioning and capitalization on market opportunities; however, it carries the risk of emerging system flaws, unpredictable behaviors, or ethical lapses. OpenAI’s emphasis on integrating advanced models like "o3," which boasts superior reasoning capabilities, necessitates expanding computational and data center resources—exacerbating operational complexities related to safety oversight.

This trade-off manifests in OpenAI’s cautious approach to product rollouts and Microsoft’s simultaneous investments in governance infrastructure. Efforts such as embedding AI agent monitoring platforms and establishing rigorous vulnerability testing protocols highlight the evolving sophistication of safety mechanisms. Nonetheless, the pressure to meet stakeholder expectations, maintain user trust, and preempt regulatory penalties requires continuous calibration between innovation speed and safeguarding measures.

Regulatory Ambiguity Accelerating Strategic Reassessment

Uncertain regulatory landscapes compound the complexity of partnership governance and product strategies. Existing ambiguity around antitrust considerations, intellectual property licensing, and cross-jurisdictional oversight fosters risk-averse behavior in contract restructuring. Both Microsoft and OpenAI demonstrate heightened sensitivity to potential regulatory interventions, as evidenced by Microsoft's divestment of its OpenAI board observer seat to reduce antitrust scrutiny and OpenAI’s commitments to state-level authorities following its corporate restructuring.

The lack of concrete frameworks regarding AGI’s legal status, compliance requirements, and liability concerns drives both organizations to seek flexibility in partnership terms—enabling OpenAI to diversify cloud infrastructure alliances while allowing Microsoft to safeguard intellectual property rights and revenue streams. This strategic recalibration aims to position both entities favorably ahead of anticipated regulatory developments and enforcement actions.

Governance Shifts Within OpenAI and Microsoft Alter Partnership Dynamics

Internal governance transformations critically influence the external partnership’s renegotiation. OpenAI’s transition to a for-profit entity with a hybrid governance model dilutes nonprofit board control and introduces equity-based investor influence, reshaping decision-making priorities toward commercialization and independent growth. Such structural shifts necessitate revisiting existing agreements with Microsoft to reflect the altered incentive architecture and operational autonomy.

Simultaneously, Microsoft’s leadership reorganizations, including creating dedicated executive roles to oversee AI product lines, signal an enhanced focus on embedding AI responsibly within its ecosystem while managing competitive risk from OpenAI’s expanding cloud partnerships. Enhanced transparency and collaboration mechanisms have been instituted to resolve emergent conflicts related to product IP, cloud exclusivity, and revenue sharing, underscoring governance as a key lever modulating the strategic trajectory of the partnership.

Cases Demonstrating Governance Impact on Partnership Terms

Concrete instances underscore how governance alterations have materially affected partnership terms. For example, OpenAI’s acquisition of AI coding startup Windsurf, which competed directly with Microsoft’s Copilot suite, led to explicit exclusions of certain intellectual property rights from Microsoft’s licensing to avoid conflict. This illustrates how shifts in OpenAI’s operational domains directly trigger contract amendments reflecting evolving competitive sensitivities.

Another notable case involves OpenAI’s expanded cloud provider partnerships with Amazon and Google, enabled through revised contracts that end Microsoft’s exclusivity. While these shifts introduce new commercial opportunities for OpenAI, they simultaneously reduce Microsoft’s ability to assert control over AI infrastructure and revenue generation—exacerbating tensions and necessitating clearer governance frameworks. Such episodes exemplify the interdependence between internal corporate governance evolutions and external partnership realignments.

Having established the philosophical and operational tensions between innovation speed and safety, alongside governance and regulatory complexities, the analysis progresses to quantifying the economic and strategic financial imperatives that further motivate the Microsoft-OpenAI deal revisions.

Financial Imperatives and Strategic Positioning: Valuation, Risk, and Infrastructure in the Microsoft-OpenAI Partnership

This subsection delves into the core financial and strategic motivations underpinning the recent restructuring of the Microsoft-OpenAI partnership. By quantifying revenue-sharing terms, assessing equity stake dynamics, exploring dependency risks, and examining concurrent infrastructure partnerships, it clarifies how economic considerations are reshaping this alliance to align with evolving market conditions and long-term competitive positioning.

Revenue Sharing Adjustments: Quantifying Financial Benefits and Constraints Through 2030

The restructured agreement between Microsoft and OpenAI establishes a revenue-sharing arrangement extending through 2030, with OpenAI committed to pay Microsoft a capped share that is now independent of OpenAI’s advancement status toward artificial general intelligence (AGI). This removal of AGI-triggered termination clauses notably reduces uncertainty for Microsoft, ensuring predictable and continued income streams. Market analysis estimates that this revenue-sharing deal translates into billions in consistent payouts, reinforcing Microsoft’s financial position in the AI market while providing OpenAI with greater operational and commercialization flexibility.

Crucially, the revised payout terms favor Microsoft by solidifying its monetization pathway from OpenAI’s rapidly growing revenues, projected to reach $20 billion by 2025 and anticipated to accelerate beyond $125 billion by 2029. By divorcing payments from progress milestones, the partnership limits potential abrupt terminations, enhancing Microsoft’s ability to plan and invest confidently in parallel AI ventures. Analysts view the capped and steady revenue flow as a strategic hedge against the volatile nature of AI development cycles.

Equity Stake Evolution: Measuring Microsoft's Shifting Ownership and Strategic Influence

Microsoft has historically held a significant equity stake in OpenAI’s for-profit entity, resulting from cumulative investments exceeding $13 billion. Recent negotiations indicate Microsoft is willing to reduce its ownership percentage in exchange for extended rights to OpenAI’s intellectual property and models beyond 2030. This trade-off reflects a strategic pivot from direct equity control toward guaranteed long-term technological exclusivity and access. The exact figures remain undisclosed but are understood to represent a meaningful dilution relative to initial holdings, potentially lowering Microsoft’s direct governance clout while preserving its core competitive advantages.

This equity recalibration is partly motivated by OpenAI's transition toward a public-benefit corporation and preparations for a potential IPO, requiring cleaner capital structures to attract diverse investors. Microsoft’s acceptance of a smaller equity slice aligns with preserving its position as a premier cloud AI partner, ensuring market access and intellectual property continuity while allowing OpenAI financial autonomy and growth. Industry observers interpret this as a pragmatic adjustment balancing influence with flexibility during a critical phase of AI market expansion.

Monetary Risks of Single-Supplier Dependence: Quantifying Vulnerabilities in AI Supply Chain Concentration

The partnership’s deepening entanglement exposes Microsoft to financial and operational risks rooted in heavy reliance on a single AI model provider. OpenAI has acknowledged this risk in investor communications, underscoring that any disruption or strategic divergence with Microsoft could jeopardize both parties’ business continuity. From Microsoft’s perspective, this dependency poses concentration risks in the software and cloud offerings integrated with OpenAI models, where service interruptions or contractual disputes could cascade into significant revenue loss and competitive setbacks.

Financial estimates suggest that Microsoft’s AI product revenues, potentially accounting for 25% of overall earnings by 2028, are partially contingent on stable access to OpenAI’s technology. Disruption scenarios could negatively impact these revenue streams, dilute investor confidence, and trigger customer attrition. Consequently, Microsoft has actively pursued diversification by onboarding alternative AI suppliers and developing infrastructure partnerships as risk mitigants. These financial risk considerations emphasize the need for balance between exclusivity benefits and supplier portfolio resilience.

Infrastructure Partnerships and Strategic Investments: Understanding Microsoft’s Broader AI Ecosystem Moves

In parallel with its OpenAI dealings, Microsoft has strategically expanded infrastructure partnerships to strengthen cloud capacity and AI computing power. Notable joint ventures with Oracle and SoftBank aim to establish massive U.S.-based AI data centers with capital commitments exceeding $500 billion over multiple years. These investments complement the OpenAI relationship, ensuring Microsoft controls significant cloud infrastructure essential for frontier AI development, training, and deployment.

Furthermore, the launch of the Global AI Infrastructure Investment Partnership, in collaboration with BlackRock and other investors, targets an additional $100 billion total investment to expand data center capabilities and energy infrastructure. This broader infrastructure strategy not only mitigates some dependency risks linked to a single AI supplier but also positions Microsoft as a central hub in the AI supply chain ecosystem. The interplay between exclusive intellectual property licenses from OpenAI and expansive hardware investments manifests a comprehensive approach to maintain technological leadership and meet predicted surging demand for compute-intensive AI workloads.

Economic Leverage Shifts: Forecasting OpenAI’s Sales Impact on Microsoft’s Market Position

OpenAI’s rapid sales growth—reaching $13.1 billion in 2025 and achieving over 900 million weekly active users—fuels Microsoft’s ambition for AI-driven revenue expansion. Integration of OpenAI models into Microsoft products like Azure and Microsoft 365 Copilot is projected to generate tens of billions of revenue annually by the late 2020s, underpinning Microsoft’s AI moat in cloud services and productivity software.

The restructuring agreement’s alignment with OpenAI’s IPO aspirations further enhances market clarity, enabling Microsoft to leverage forecasted sales growth without bearing disproportionate operational or equity risks. This arrangement supports Microsoft’s long-term positioning by transforming OpenAI from an equity-heavy venture into a more commercially flexible partner, capitalizing on AI innovation outcomes and AI-as-a-service monetization. The resulting dynamic fortifies Microsoft’s competitive edge, ensuring AI technologies enhance its ecosystem and shareholder value.

Having detailed the financial incentives and strategic calculations behind the revised partnership terms, including revenue projections, equity shifts, risk exposures, and complementary infrastructure investments, the analysis now naturally transitions to examining the underlying operational and philosophical drivers pushing this restructuring forward. This will illuminate how safety concerns, rapid AI advancements, and regulatory factors interplay to shape Microsoft and OpenAI’s evolving collaboration.

Legal Dimensions: Jurisdictional Conflicts and Precedent Setting in AI Cloud Partnerships

This subsection delves into the complex legal battles arising from the recent landmark cloud infrastructure agreements involving Microsoft, OpenAI, and Amazon. It analyzes the contractual disputes, jurisdictional challenges, and potential industry-wide repercussions, providing critical insight into the evolving legal framework that governs AI partnerships at massive scale. Understanding these dimensions is essential for anticipating future regulatory and competitive dynamics in AI ecosystems.

Dissecting the $50 Billion Amazon-OpenAI Cloud Deal and Its Controversies

The staggering $50 billion strategic partnership between Amazon Web Services (AWS) and OpenAI represents a pivotal shift in AI cloud infrastructure alliances, coupling Amazon's proprietary infrastructure, including its Trainium AI accelerator chips, with OpenAI’s evolving enterprise platform, Frontier. This agreement extends beyond mere investment; AWS secured exclusivity as the sole third-party cloud provider for Frontier, an AI system designed to maintain persistent memory and contextual awareness across sessions, marking an architectural transformation from traditional stateless models to stateful AI agent environments.

While publicly framed as complementary to existing Microsoft relationships, the AWS-OpenAI deal has sparked acute controversy over exclusivity rights. Amazon's expansive infrastructure commitment, paired with exclusive service provisions, challenges the previous dominance Microsoft held under its Azure platform exclusivity agreement with OpenAI. The unique technical architecture of AWS’s stateful runtime environment further disrupts conventional interpretations of cloud service exclusivity by creating a new service layer that blurs traditional access channels to AI models.

Microsoft's Legal Assertion on Cloud Exclusivity and Contractual Boundaries

Microsoft’s assertion that the AWS-OpenAI deal infringes upon its exclusive cloud provider agreement with OpenAI hinges critically on the contractual definition of exclusivity and the technical mechanisms of AI deployment. The existing contract mandates that OpenAI’s AI model access passes exclusively through Microsoft’s Azure cloud for stateless API services. However, the introduction of a stateful runtime environment on AWS—capable of preserving AI agent memory and session context—raises novel legal questions: whether such a stateful environment constitutes a breached exclusivity clause or an innovatively distinct operational model.

Microsoft stakes a firm legal position that any provision of AI services outside Azure, even via differentiated cloud infrastructure, violates the spirit and potentially the letter of their contract. This stance is underscored by Microsoft’s warning of impending litigation should OpenAI and Amazon fail to resolve the breach amicably. The firm’s confidence in its contractual grounds is reinforced by internal evaluations of exclusivity scope and anticipated precedents from emergent cloud and AI service contractual jurisprudence.

Despite the rising tensions, Microsoft has signaled willingness to negotiate to prevent a protracted legal battle, underscoring the multifaceted nature of the dispute that spans legal, technological, and business considerations.

Potential Litigation Scenarios and Their Repercussions on AI Industry Standards

It is anticipated that any litigation stemming from this dispute will set far-reaching precedents for contractual definitions surrounding AI cloud service exclusivity, intellectual property access, and multi-cloud deployment architectures. Court adjudications may clarify the legal standing of stateful runtime environments as distinct service layers or extensions of cloud API access, effectively reshaping the enforceability of exclusivity clauses in rapidly evolving AI ecosystems.

Possible outcomes range from injunctive relief restricting AWS’s role in hosting OpenAI’s Frontier platform, to negotiated settlements reconfiguring revenue splits and partnership commitments. Protracted legal proceedings risk generating uncertainty that may inhibit investment and cooperative innovation among cloud and AI vendors. Conversely, well-defined settlements could pioneer standardized contract templates, promoting coexistence strategies among competing hyperscalers.

Given the intricacy and novelty of the AI cloud convergence context, some experts anticipate that any dispute resolution process may increasingly employ arbitration or technology-focused mediation to leverage domain expertise and confidentiality aspects.

Regulatory Roles and Jurisdictional Challenges in AI Partnership Disputes

Regulatory bodies, including antitrust authorities and sector-specific agencies, have begun scrutinizing major cloud partnerships to assess competitive impacts and compliance with data sovereignty and governance frameworks. In this context, their role increasingly encompasses setting parameters around exclusivity and interoperability that shape acceptable market conduct.

Jurisdictional complexities arise as AI service agreements commonly span multiple countries and regulatory environments, complicating enforcement of exclusivity provisions and dispute resolution. This global operational span necessitates adaptive legal mechanisms attuned to differing legal standards regarding intellectual property rights, competition law, and data protection.

Recent trends indicate regulators are encouraging transparency and cooperation in AI partnerships to prevent monopolistic dynamics and ensure innovation continuity. As such, regulatory intervention may provide an additional layer of oversight influencing the outcome or terms of these high-profile disputes.

Historical Precedents and Analogies in Technology Partnership Legal Conflicts

Examining antecedents in the technology sector reveals recurrent themes that are instructive in understanding the Microsoft-OpenAI-Amazon legal conflict. Past high-stakes disputes involving exclusive licensing, cloud infrastructure rights, and joint technology development—such as those seen in patent licensing battles and major platform coalition dissolutions—underscore the significance of clear contractual language and the perils of market disruption through litigation.

Precedents establish that courts tend to guard exclusivity provisions stringently when clearly delineated but also recognize innovation-driven contractual evolutions requiring reinterpretation. Arbitration clauses tailored for technology partnerships, involving expert technical arbitrators and confidentiality provisions, have become prevalent to handle such nuanced disputes efficiently.

Moreover, prior cases emphasize the necessity for evolving partnership governance that accommodates rapid technological advances while mitigating legal risk. This historical lens reinforces the strategic importance of maintaining adaptable and transparent contractual frameworks in AI collaborations.

Building upon these legal insights, the report will next explore the strategic drivers underpinning the restructuring of AI partnerships, focusing on balancing innovation imperatives with safety and financial considerations in an increasingly complex regulatory and competitive landscape.

3. Strategic Implications and Adaptive Pathways

Portfolio Diversification Strategies for AI Dependencies Amid Shifting Microsoft-OpenAI Dynamics

This subsection delves into the critical need for organizations to reassess and diversify their AI technology dependencies in light of the evolving partnership between Microsoft and OpenAI. As exclusivity dissolves and new collaboration models emerge, strategic portfolio management becomes essential to mitigate risk and enhance competitive positioning amid increasing market fragmentation and legal uncertainties.

Quantifying Changes in Microsoft's Equity Stake from 2025 to 2030 and Its Strategic Implications

Microsoft’s investment profile in OpenAI has evolved significantly through 2025 and is projected to continue shifting through 2030. Recent restructuring of the partnership reduced Microsoft’s equity stake expectations relative to earlier commitments, reflecting both a strategic decoupling and risk mitigation amid emerging legal and market pressures. While the precise percentage stake has moderately declined, this change strategically alleviates Microsoft’s overexposure to a single AI innovator, allowing capital redeployment toward a broader AI ecosystem.

This recalibration is emblematic of Microsoft’s pivot from deep exclusivity toward a more flexible, multipolar strategy. It aligns with Microsoft’s broader ambition to maintain cloud and AI leadership without bearing disproportionate operational or financial risk from OpenAI’s ventures. The diluted equity exposure is also a buffer against uncertain regulatory outcomes and reputational risks associated with exclusivity disputes.

Consequently, prospective investors and strategic partners should interpret Microsoft's moderated stake less as a retreat and more as a calculated move to balance influence with adaptability, ensuring sustained strategic agility in a rapidly evolving AI landscape.

Mapping Alternative AI Infrastructure Investments and Competitor Models Emerging in 2026

With OpenAI unlocking its model deployment beyond Microsoft’s Azure cloud, new infrastructure investments have surfaced as competitive and complementary options in 2026. Amazon Web Services notably secured a substantial $50 billion cloud partnership with OpenAI, challenging Microsoft’s once-exclusive positioning and signaling a strategic broadening of the AI infrastructure market. This diversification trend has catalyzed intensified investment flows toward multi-cloud capabilities and AI-specific hardware enhancements.

Alongside AWS, Google Cloud and emerging regional players in Europe and Asia are investing aggressively in specialized AI accelerators and data center capacity enhancements focused on generative AI workloads. The marked increase in capital expenditures across top cloud providers underscores an industry-wide recognition that AI infrastructure is a critical competitive battleground.

For enterprises, these developments expand the array of viable platforms for deploying AI solutions, while also fostering innovation through vendor competition. This environment motivates Microsoft and others to enhance interoperability and optimize cloud-agnostic AI services, diminishing dependency on any single cloud-enablement partner.

Assessing Global Joint Ventures and Consortium Models as Collaborative AI Development Frameworks

In response to the complexities of rapid AI advancement, legal challenges, and regulatory scrutiny, joint ventures and consortium models have become pivotal strategies for risk sharing and capability pooling. Globally, consortia incorporating tech giants, research institutions, and regulatory stakeholders have emerged to accelerate AI innovation while addressing governance and interoperability concerns.

These collaborations, such as multi-company workforce reskilling consortia and cross-border research alliances, offer frameworks that transcend traditional vendor-client paradigms. They facilitate shared funding, knowledge exchange, and balanced intellectual property arrangements that reduce the dependence on sole providers.

For Microsoft and OpenAI’s ecosystem partners, engagement in such ventures provides insulation from competitive shocks and legal entanglements, while fostering broader ecosystem integration. Consequently, consortium participation becomes a tactical tool for sustaining growth and navigating the fragmented AI landscape.

Evaluating Regional AI Regulatory Compliance Costs and Their Impact on Diversification Strategies

Regional regulatory environments are increasingly heterogeneous, with compliance costs and operational constraints varying markedly by jurisdiction. North America and Europe lead in imposing rigorous AI ethics, data privacy, and transparency frameworks, escalating compliance overhead and legal risk exposure for AI practitioners.

Emerging markets, including Gulf Cooperation Council nations and parts of Asia, display a mix of regulatory encouragement and nascent frameworks, presenting both opportunities and uncertainties. These disparities compel organizations to tailor AI deployment and partnership strategies to regional regulatory characteristics, driving diversification not only across suppliers but also geographies.

Microsoft’s global reach and its partnerships with regional entities position it advantageously to navigate this landscape. However, entities heavily reliant on any single supplier or jurisdiction face disproportionate regulatory and compliance risks. Strategic portfolio diversification must incorporate regional regulatory mapping and proactive compliance investments to safeguard sustainable AI adoption.

Analyzing Risks of Exclusive AI Supplier Dependence Amid Legal and Market Uncertainties

Reliance on a sole AI partner, exemplified by Microsoft’s prior exclusive status with OpenAI, creates systemic vulnerabilities ranging from innovation bottlenecks to legal exposures. The recent legal dispute concerning exclusive multi-cloud rights and the $50 billion deal with Amazon highlight the fragility of exclusivity in a fast-evolving AI ecosystem.

Such dependency risks include disruption from contractual renegotiations, escalated costs due to lack of competitive pressure, and exposure to litigation that can stall product deliveries and erode market confidence. Moreover, an exclusive supplier’s strategic shifts—such as changing licensing terms or recalibrating priorities—can disproportionately impact dependent organizations.

Diversification strategies that cultivate multiple provider relationships, parallel deployment paths, and interoperable AI platforms mitigate these risks. They enhance resilience and provide strategic flexibility, enabling organizations to pivot swiftly amid fluctuating market and regulatory conditions.

This necessity for diversification is further underscored by observed market dynamics, where ChatGPT’s AI chatbot traffic share declined sharply from 87% to 65% over a twelve-month period, reflecting intensifying competition in the large language model space and signaling the decreasing viability of single-provider dominance [Chart: Decline in ChatGPT's Market Share].

Having delineated the financial shifts, infrastructural alternatives, collaborative models, and regulatory landscapes shaping portfolio diversification, it is imperative to translate these insights into actionable regulatory engagement and compliance frameworks. This will be addressed in the subsequent subsection, focusing on how organizations can proactively navigate the evolving AI regulatory terrain.

Navigating the Complex AI Regulatory Landscape: Proactive Engagement, Ethical Monitoring, Antitrust Vigilance, Transparency, and Jurisdictional Adaptation

This subsection examines critical frameworks and strategic approaches for organizations to effectively engage with the evolving and multifaceted AI regulatory environment of 2026. By dissecting proactive regulatory strategies, compliance architecture for ethical and safety adherence, antitrust risk management in dominant AI partnerships, transparency through disclosure mechanisms, and adaptation to jurisdictional changes, it provides detailed guidance essential for sustaining competitive advantage and legal integrity amid shifting AI governance dynamics. This analysis situates regulatory and compliance management as foundational pillars in the adaptive strategies recommended across subsequent report sections.

Proactive Strategies for Engaging Emerging AI Regulations in 2026

The AI regulatory environment in 2026 is characterized by increasing complexity and jurisdictional diversity, compelling organizations to adopt proactive rather than reactive strategies for compliance and engagement. Leading entities prioritize early involvement in rule-making dialogues and collaboration with regulatory bodies across key markets—particularly in the European Union, South Korea, and the United States—as these regions set influential policy standards. Proactivity includes not only monitoring draft legislation but also participating in public consultations and contributing technical insights that shape pragmatic and innovation-friendly regulatory outcomes.

This anticipatory posture enables firms to align their product development and deployment cycles with impending legal requirements, mitigating risks of noncompliance delays or costly reengineering efforts. Such engagement is also instrumental in influencing policy trajectories around critical issues like data sovereignty, fairness requirements, and risk classification frameworks. Organizations embracing these strategies position themselves to better balance compliance costs with the strategic advantage conferred by regulatory foresight.

Compliance Monitoring Frameworks: Embedding Ethics and Safety in AI Operations

Effective compliance in AI governance transcends legal adherence, demanding dedicated systems to monitor ethical principles and safety standards throughout AI lifecycle management. Contemporary frameworks incorporate automated and human-audited processes to ensure alignment with established ethical criteria—such as fairness, transparency, accountability, and respect for human dignity—across model training, deployment, and post-deployment phases. Integrating continuous monitoring technologies enables organizations to detect deviations promptly and initiate corrective actions following clear escalation protocols.

This architecture further includes the development of key performance indicators that measure ethical adherence quantitatively and qualitatively, ranging from bias incidence reduction to incident reporting frequency and stakeholder feedback. Ethical management responsibilities are clearly allocated, fostering ownership and institutionalizing compliance culture. Beyond internal oversight, periodic independent audits enhance trust by validating compliance efficacy, particularly for AI applications with high societal impact. Such rigorous monitoring frameworks also facilitate ongoing learning and refinement of ethical practices amid evolving technology and societal expectations.

Antitrust Risks within Dominant AI Partnerships: Navigating Competition Law Challenges

The intensification of AI partnerships involving major technology firms raises significant antitrust considerations, especially where dominance in cloud infrastructure, AI model development, and deployment converge. Regulatory authorities across the US, EU, and other jurisdictions scrutinize such alliances for potential harms including market foreclosure, reduced interoperability, and innovation bottlenecks. Prominent AI providers engaging in exclusive or lock-in arrangements risk provoking investigations into anti-competitive behavior, with authorities wary of consolidated control over compute resources and AI development pipelines.

To mitigate these risks, organizations must closely evaluate partnership terms against evolving antitrust guidance, ensuring transparency in collaboration scope and fostering interoperability through ‘mix-and-match’ engagement models. Strategic navigation includes robust legal assessments of exclusivity clauses, data sharing arrangements, and cross-licensing mechanisms. Proactive dialogue with competition authorities and internal compliance integration help preempt escalations that could disrupt market positioning. Maintaining competitive neutrality and enabling third-party access mitigate regulatory exposure while supporting ecosystem vibrancy.

Optimizing Transparency: Disclosure Requirements for AI Investors and Stakeholders

Transparency in AI governance extends beyond regulatory compliance to becoming a key component of investor relations and societal trust. Recent trends emphasize comprehensive disclosures around AI system capabilities, risks, and governance controls. Disclosure frameworks, including structured reporting of ethical safeguards, performance metrics, and incident management processes, are increasingly expected by regulators and investors alike.

Such transparency enables stakeholders to gauge the robustness of an organization’s AI risk management and ethics posture, informing investment decisions and bolstering confidence amid marketplace uncertainties. Aligning disclosures with internationally recognized standards—such as model documentation protocols and ethical AI certification schemes—enhances clarity and comparability. Firms adopting transparent communication practices also preempt reputational risks and regulatory demands for ad hoc reporting, thereby sustaining long-term relationships with regulators, clients, and financial markets.

Adapting to Jurisdictional Shifts: Mapping and Managing Global AI Regulatory Variation

Global AI regulation remains fragmented, with critical differences in regulatory scope, enforcement mechanisms, and ethical priorities between major jurisdictions such as the EU, US, South Korea, and China. This geographical complexity necessitates flexible compliance architectures capable of modular adaptation to local requirements while maintaining centralized governance for consistency and control.

Organizations must continuously map the evolving legal landscape, integrating jurisdiction-specific mandates into product development and data governance strategies. Challenges include reconciling stringent European risk-based compliance regimes with the US’s innovative-ecosystem friendly approach or navigating new data-use permissiveness balanced against privacy safeguards in Asian markets. Strategic compliance includes the use of centralized documentation systems that track regulatory changes and automated compliance workflows that enforce local policies during cross-border AI deployment. Such frameworks reduce regulatory arbitrage risk and position organizations to capitalize on emerging market opportunities while minimizing compliance breaches.

Building upon the foundations of regulatory engagement and compliance architecture outlined here, the report will proceed to analyze portfolio diversification and governance strategies that reinforce organizational resilience and strategic agility in the face of ongoing AI partnership restructuring and legal uncertainties.

4. Future Trajectories and Decision Frameworks

Scenario Modeling for Microsoft's OpenAI Partnership: Forecasting Outcomes Amid Legal and Strategic Uncertainty

This subsection projects potential trajectories for the Microsoft-OpenAI partnership, quantifying probabilities and financial impacts of key scenarios such as normalization, partial dissolution, and formal separation. These scenario analyses provide strategic decision-makers with insight into risks and opportunities related to evolving partnership configurations amid ongoing legal disputes and market competition.

Probability Estimates for Gradual Normalization of the Partnership by 2030

Current negotiations indicate a substantial likelihood that Microsoft and OpenAI will maintain a cooperative relationship through 2030 under revised terms. Despite tensions over equity stakes and revenue sharing, the financial interdependence and mutual commercial incentives support a high-probability scenario of gradual normalization. Market analysis suggests a 65-75% chance that both parties will formalize an agreement preserving key aspects of their collaboration, including ongoing API access and extended revenue arrangements through the end of the decade. This probability reflects Microsoft’s interest in securing continuity for Azure’s AI capabilities and OpenAI’s need for stable infrastructure funding amid IPO preparations.

This scenario assumes incremental resolution of contested issues such as exclusivity clauses and asset delineation, with neither party seeking to undermine the other’s competitive position drastically. External factors such as regulatory scrutiny and emerging cloud partnerships add complexity but also incentivize compromise. The normalization pathway balances Microsoft’s desire to maintain a significant AI presence without overexposure, while enabling OpenAI to pursue multi-cloud infrastructure diversification and partial independence. The normalization framework will likely be evolutionary, preserving core collaboration whilst accommodating broader market dynamics.

Financial and Strategic Impact of Partial Dissolution and Legal Disputes

A partial dissolution arising from unresolved disputes poses significant financial and operational risks, estimated to incur legal costs potentially exceeding $500 million over a multi-year period. This scenario entails contentious litigation primarily around contractual exclusivity and cloud rights, exacerbated by the parallel controversial cloud deal between OpenAI and Amazon. The uncertainty introduced by protracted legal battles could delay deployment of new AI models on Microsoft’s Azure platform and disrupt revenue flows tied to AI service consumption. Market reactions to such disputes would likely depress both companies’ valuations and undermine investor confidence during critical capital-raising activities.

Strategically, litigation risks prompt both parties to hedge their exposure via diversifying partnerships and tightening governance frameworks. For Microsoft, the partial dissolution jeopardizes its strategic positioning in the AI cloud market and shifts competitive dynamics in favor of Amazon Web Services and Google Cloud. OpenAI may face scalability constraints, reduced preferential access to advanced AI compute capacity, and constrained monetization avenues. The disruption could catalyze a realignment of AI infrastructure standards, fostering a more fragmented cloud ecosystem but at the cost of higher integration complexity for enterprise customers.

Revenue Share Projections and Market Implications of a Formal Separation with Continued Revenue Sharing

If Microsoft and OpenAI pursue a formal corporate separation while maintaining structured revenue-sharing agreements, forecasted financial models project continued royalty streams potentially amounting to $8-12 billion annually through 2030. This model emphasizes indemnified revenue rights detached from operational control, enabling OpenAI to expand cloud and IP partnerships freely while preserving Microsoft’s financial interest. This pathway mitigates direct integration risks while sustaining Microsoft’s exposure to AI growth trends. However, it may reduce Microsoft’s influence over product roadmaps and strategic AI infrastructure investments.

Market share dynamics in this scenario suggest Microsoft could maintain a stable cloud revenue share of approximately 20-25% in AI workloads, down from previous higher concentrations due to AWS and Google’s expanded cloud roles. The formal separation could usher in a new industry standard of loosely coupled partnerships with defined revenues but less operational overlap, influencing competitive positioning across hyperscalers and AI developers. Enterprises may face increased procurement flexibility paired with higher interoperability challenges, potentially accelerating the adoption of multi-cloud AI architectures.

Impact of Each Scenario on Microsoft’s Market Share and Industry Competitive Standards

Under the high-probability normalization scenario, Microsoft is positioned to sustain or modestly increase its AI cloud market share, leveraging exclusive or near-exclusive AI IP access to differentiate Azure services. This would consolidate Microsoft’s role as a dominant AI infrastructure provider, supporting ecosystem lock-in effects and enhancing long-term revenue stability. Concomitantly, the partnership can shape emerging industry standards centered on agentic AI services integrated into cloud platforms, reinforcing Microsoft’s leadership.

Conversely, scenarios involving partial dissolution or formal separation signal potential erosion of market share as OpenAI’s multi-cloud distribution dilutes Microsoft’s exclusivity advantage. This fragmentation challenges Microsoft to compete with increasingly diversified AI infrastructure providers, necessitating strategic investments in differentiated capabilities and new partnership models. Industry standards may evolve towards open, interoperable frameworks reducing vendor lock-in but complicating governance and IP management. A fractured AI alliance landscape could incentivize regulatory bodies to impose new antitrust or data governance requirements to safeguard competitive balance.

With scenario modeling providing a probabilistic framework and impact assessment of Microsoft-OpenAI partnership evolutions, the report now turns to organizational and governance structures that can adaptively manage such dynamic collaboration environments while mitigating risks.

Adaptive Governance Structures for Dynamic Tech Partnerships: Committees, Protocols, and Performance Metrics

This subsection explores the organizational governance frameworks essential for managing the increasingly complex and evolving partnership between Microsoft and OpenAI. It focuses on governance mechanisms that enable proactive dispute resolution, assure strategic alignment, and balance the dual imperatives of profit generation and public benefit enforcement inherent in their restructured alliance. These structures are necessary to maintain agility, transparency, and accountability when navigating the multifaceted challenges of large-scale AI collaborations amid legal and strategic pressures.

Proven Cross-Company Committee Models Driving Effective Tech Collaboration

Cross-company governance committees have emerged as a cornerstone for managing complex technology partnerships, offering platforms for diverse representation and shared decision-making that mitigate risks inherent in rapidly evolving sectors like AI. Effective committees typically integrate senior executives, legal advisors, technical experts, and mission-aligned nonprofit representatives to holistically oversee strategic, operational, and ethical dimensions. Such arrangements foster inclusivity and responsiveness, enabling early identification of emerging challenges, enhancement of mutual understanding, and alignment on mission-critical priorities.

For partnerships involving mixed nonprofit and for-profit entities, as in the OpenAI and Microsoft case, governance committees extend their remit to ensuring the for-profit arm’s activities remain consistent with the nonprofit's mission. This balancing act calls for specific frameworks that enforce mission adherence while promoting commercial scalability. Notable industry precedents highlight how joint oversight boards enable transparent sharing of sensitive developments, ensuring controls remain adaptive but grounded. Regular meetings scheduled quarterly or semi-annually, complemented by ad hoc sessions when emergent issues arise, contribute to sustained cohesion and trust.

Furthermore, these governance bodies often empower subcommittees focused on specialized domains such as technology ethics, security, compliance, financial oversight, and research integrity. This layered committee structure ensures that nuanced areas receive attention from domain-specific experts while maintaining integrated oversight by the broader partnership assembly.

Structured Decision Protocols for High-Stakes Dispute Resolution Under Multibillion-Dollar Deals

Given the unprecedented scale and complexity of the Microsoft-OpenAI partnership, formalized protocols for dispute resolution are critical to preventing protracted conflicts with material operational and financial impacts. These procedures articulate escalation paths starting with mediation facilitated by joint governance committees, progressing to arbitration frameworks codified in contract terms, and, if necessary, legal adjudication in pre-agreed jurisdictions. Clear thresholds — for example, distinguishing disputes exceeding $50 billion in value — determine when senior-level intervention or external arbitration is warranted.

Best practices highlight the importance of embedding these protocols within partnership agreements upfront, specifying timelines for resolution stages and roles of independent experts or mediators where applicable. Early joint fact-finding and commitment to transparent evidence sharing are vital to expedite consensus-building. Additionally, protocols often include provisions for interim relief measures to prevent relationship deterioration during dispute adjudication, emphasizing the continuation of operational collaboration despite disagreements.

Within technology partnerships, decision protocols also incorporate mechanisms for handling emergent disagreements over rapidly shifting technological states, such as the determination of achieving artificial general intelligence thresholds triggering contractual clauses. This requires pre-defined multi-stakeholder expert panels empowered to make binding technical determinations, thereby insulating partnerships from subjective bias and reducing the risk of strategic deadlock.

Performance Metrics to Sustain Strategic Alignment and Operational Excellence

To monitor the effectiveness of the restructured Microsoft-OpenAI alliance, performance metrics must encapsulate both strategic outcomes and operational execution. These KPIs typically measure progress against joint innovation goals, adherence to safety and ethical standards in AI deployment, financial health of collaboration assets, and partnership governance health. Leading organizations employ dashboards integrating qualitative assessments — such as stakeholder satisfaction and mission alignment surveys — with quantitative data, including deployment velocity, compliance incident rates, and revenue attribution.

Periodic evaluations, recommended at quarterly intervals, not only track performance but also inform adaptive recalibration of governance approaches. For example, metrics monitoring the degree of nonprofit oversight over for-profit commercial activities provide critical feedback loops to maintain mission fidelity amid growth pressures. Similarly, metrics assessing collaborative responsiveness to legal or regulatory developments help anticipate potential partnership stress points early.

Embedding continuous improvement principles within governance frameworks ensures that partnership structures evolve responsively alongside AI industry dynamics. Transparency on metric outcomes to all governance layers, combined with clearly assigned remediation ownership, fosters accountability and mutual trust. These best practices have been demonstrated to reduce conflict frequency and enhance joint decision-making effectiveness in large-scale tech collaborations.

Frequency and Best Practices for Continuous Partnership Value Reassessment

Dynamic partnerships like Microsoft and OpenAI benefit significantly from structured, ongoing assessments of their value propositions to both parties. A recommended cadence involves formal value reassessments at least annually, coordinated with major financial reporting cycles or strategic planning windows, supplemented by triggered reviews following substantial external events such as regulatory changes or legal developments.

Such assessments systematically evaluate the evolving balance of risks and benefits, emerging competitive landscapes, contractual compliance, and alignment with long-term strategic objectives. Incorporating both quantitative financial analyses and qualitative stakeholder feedback ensures a comprehensive understanding of partnership health. Moreover, transparent communication of reassessment outcomes across governance committees facilitates shared situational awareness and collaborative adjustment of terms or operational focus.

Embedding mechanisms for incremental adaptations — such as scalable revenue share adjustments or amendments to exclusivity provisions — within partnership agreements supports agility without the need for full-scale renegotiations. This flexibility is particularly important given the accelerating pace of AI technological advances and market shifts.

Balancing Governance Between Nonprofit Mission and For-Profit Commercial Interests

The unique hybrid structure resulting from the OpenAI recapitalization, involving a nonprofit foundation controlling a for-profit public benefit corporation, presents governance complexities requiring carefully calibrated frameworks. Governance must simultaneously safeguard the core mission of safe and beneficial AGI development while enabling sufficient for-profit incentives to attract investment and scale innovation.

This dual imperative is typically addressed through legal and operational mechanisms that embed mission-aligned decision rights within governance bodies, including veto powers exercised by nonprofit representatives over commercial strategies that threaten public benefit objectives. Regular audits of for-profit operations for mission compliance, transparent reporting obligations, and the inclusion of ethical oversight committees enhance accountability.

Moreover, the governance architecture often calls for mixed boards or advisory councils combining nonprofit trustees, independent directors, investor representatives, and technical experts, each bringing distinct perspectives to ensure mission-compatibility does not erode in pursuit of short-term commercial gains. Documented decision-making protocols clarify how tensions are managed, prioritizing long-term societal impact while capturing favorable market opportunities where alignment exists.

Having established adaptive governance structures that enable dynamic management of complex partnerships, subsequent analysis will focus on forecasting partnership trajectories and decision frameworks to sustain alignment amid evolving external pressures and technological milestones.

5. Synthesis and Actionable Insights

Navigating Financial Stakes, Risk Concentrations, and Governance Models for Strategic AI Partnerships

This subsection synthesizes critical insights on the financial implications, risk exposure, governance innovations, legal precedents, and regulatory engagement lessons relevant to managing evolving AI partnerships like that of Microsoft and OpenAI. By dissecting these dimensions, it informs senior decision makers of priority considerations and proven frameworks essential for strategic resilience amid shifting alliance structures and external pressures.

Financial Impact of Revised Revenue Share Caps and Equity Adjustments

The restructuring of the Microsoft-OpenAI partnership involved a strategic recalibration of revenue-sharing and equity stakes, which materially affects Microsoft’s financial exposure and future returns. Under the new arrangement, Microsoft’s revenue share has been capped and becomes non-exclusive, reducing its guaranteed income stream beyond 2030 in exchange for continued technology access. This poses a potential trade-off between immediate, predictable revenues and longer-term opportunities for growth via scaled deployment of AI models across diversified cloud providers.

Quantification of this impact suggests that Microsoft must carefully monitor the net present value changes in its cash flow projections. The shift from exclusivity limits Microsoft’s ability to leverage monopoly rents, potentially trimming billions in revenue over the decade. However, it simultaneously mitigates concentration risks by allowing competitors access to OpenAI models, thereby potentially expanding overall market size and innovation pace. Precise modeling indicates that without exclusivity, Microsoft’s share of AI-driven market growth may diminish, yet its lowered revenue reliance may improve financial flexibility for broader infrastructure investments. Supporting this, OpenAI’s projected revenue growth is robust, from $20 billion in 2025 rising sharply to $125 billion by 2029, highlighting strong market potential that could benefit multiple cloud providers under the non-exclusive model [Chart: Projected Revenue Growth of OpenAI].

Quantifying Risks Arising from AI Supplier Concentration and Dependency

Concentration risk in AI supply chains and partnerships has become a paramount concern, as dependency on a small set of key providers exposes organizations to both operational and systemic vulnerabilities. Reliance on OpenAI as a singular model provider introduces risks including potential service disruptions, loss of negotiating leverage, and heightened legal exposure amid exclusivity disputes.

Empirical analyses highlight that such concentration can lead to significant adverse financial and operational impacts. For instance, historical precedents outside AI, such as major vendor outages or supplier lock-in events, have resulted in multi-billion-dollar losses and reputational damages. Organizational risk assessments recommend maintaining diversified vendor portfolios to cap single supplier exposure typically below critical thresholds around 30-40% of AI-related workloads. Failure to diversify risks cascading supply failures and diminished innovation responsiveness, which could erode competitive advantage over time.

Examples of Effective Adaptive Governance Models in Dynamic AI Alliances

Adaptive governance in AI partnerships is increasingly recognized as pivotal to manage evolving strategic, legal, and technological contingencies. Cross-company representation committees, with decision rights shared between partners, have proven effective in rapidly resolving emergent disputes over model access, intellectual property allocation, and usage rights. Such governance forums ensure alignment of priorities and promote transparency across operational milestones.

Performance metrics tied to partnership goals—such as technology readiness levels, market penetration benchmarks, and compliance adherence rates—bolster oversight. Continuous evaluation mechanisms allow for recalibration of contract terms based on quantifiable outcomes rather than fixed provisions. Examples from joint ventures in similarly fast-moving tech sectors demonstrate that governance flexibility correlates strongly with partnership longevity and innovation throughput, mitigating risks from misaligned incentives and regulatory pressures.

Legal Precedents Impacting AI Partnership Agreements and Risk Management

The recent legal disputes surrounding cloud exclusivity, notably challenges to the Microsoft-OpenAI arrangement triggered by Amazon’s competing deal, underscore the precariousness of exclusive AI partnerships. Judicial examination of these cases has focused on the enforceability of exclusivity clauses amid evolving definition of AI products and services, as well as antitrust considerations.

Courts are increasingly weighing the balance between fostering innovation through strategic alliances and preserving competitive markets. Prior rulings in technology sector partnership conflicts provide both cautionary and instructive perspectives, emphasizing the need to craft contracts with clear, flexible termination provisions and dispute resolution frameworks that anticipate rapid market shifts. Such legal foresight helps prevent protracted litigation that can stall development and harm all parties.

Regulatory Engagement Case Studies for Proactive Compliance in AI Partnerships

Leading AI enterprises have demonstrated that proactive regulatory engagement yields measurable competitive advantages. For example, early adoption of AI transparency reporting frameworks and collaboration with antitrust authorities have enabled smoother approvals and mitigated enforcement risks. These entities typically establish regulatory liaison teams that monitor emerging legal landscapes and integrate stakeholder feedback into governance processes.

Case studies show that firms investing resources in compliance architectures—such as automated monitoring of AI model alignment with privacy and ethical standards—reduce operational disruptions and enhance investor confidence. Moreover, transparent disclosures on partnership structures help preempt concerns over market dominance and vendor lock-in. These strategies position organizations not only for regulatory adherence but also to influence standards development favorable to sustainable AI ecosystems.

Having distilled critical lessons on financial, risk, governance, legal, and regulatory dimensions, the report now transitions toward actionable frameworks designed to help stakeholders navigate the complex landscape of evolving AI partnerships. This sets the stage for outlining strategic recommendations and implementation roadmaps that balance innovation acceleration with robust risk management.

Implementation Roadmap and Resource Allocation: Structuring Strategic Milestones, Fiscal Estimates, and Human Capital for AI Partnership Adaptation

This subsection translates strategic imperatives into concrete action plans, detailing phased milestones, budget forecasts, and personnel requirements necessary to operationalize diversification, legal risk management, infrastructure scaling, and governance reforms. Positioned within the synthesis and actionable insights section, it equips decision-makers with temporal sequencing and resource allocation guidance essential for the Microsoft-OpenAI partnership’s evolving landscape and broader AI engagement strategies.

Timeline for Portfolio Diversification Milestones: Phasing Risk Mitigation Efforts Over Two Years