AI-Powered Telecom Transformation: Navigating Accelerated Growth Amid Legacy Challenges and Strategic Imperatives

Table of Contents

- Executive Summary

- Introduction

- 1. AI-Powered Telecom Transformation Amidst Growth and Integration Challenges

- 2. Operational Transformation: Core Functions Reinvented

- 3. Persistent Barriers: Understanding Constraints

- 4. Strategic Imperatives: Pathways Forward

- 5. Investment Implications: Portfolio Positioning

- 6. Synthesis and Recommendation

- Conclusion

Executive Summary

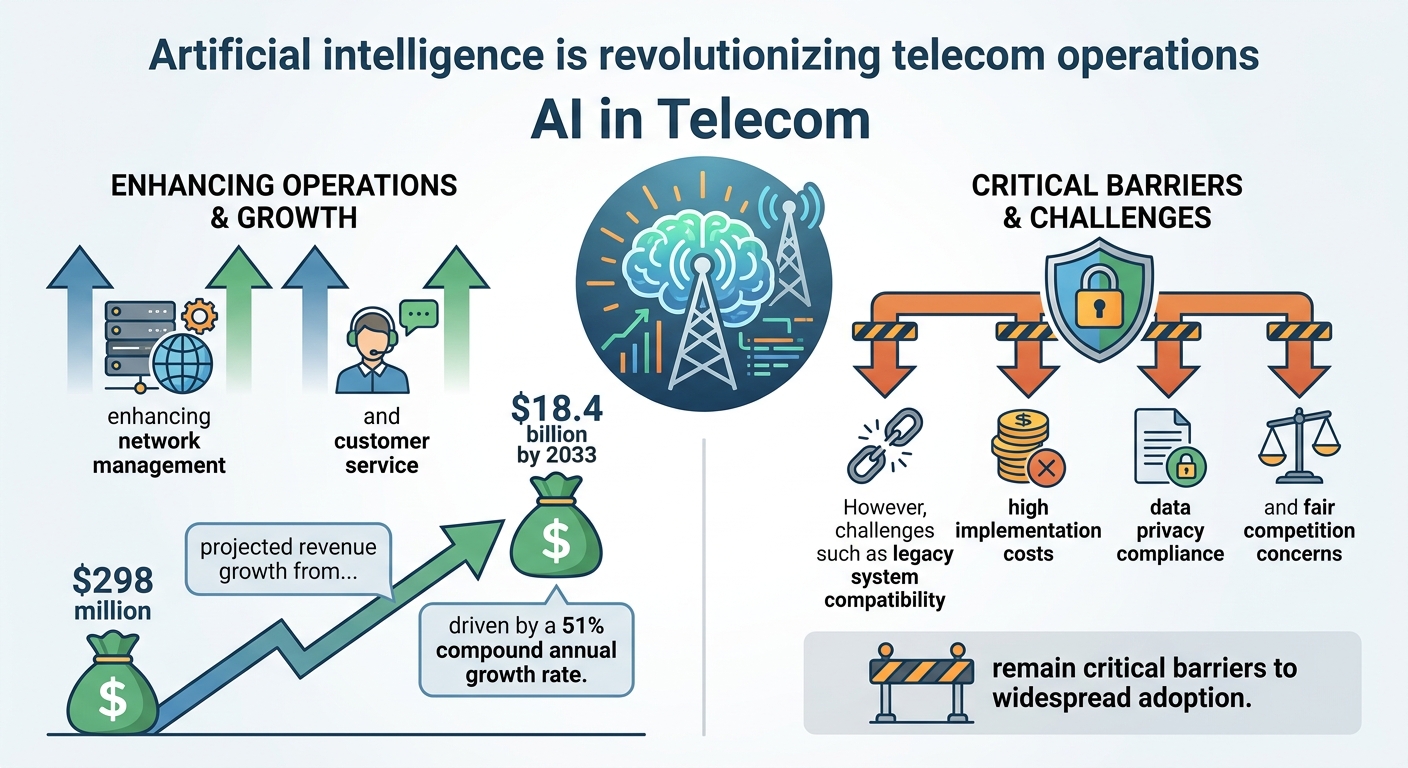

Between 2020 and 2025, over 70% of telecom companies transitioned AI from pilot projects to core operational infrastructure, driving a fivefold growth in AI market size within telecom—a rate surpassing many other industries. This surge underpins a projected fivefold increase in AI-centric telecom revenues between 2022 and 2027, with operators reporting year-over-year revenue uplifts in the mid-single digits attributable to AI-enabled business units. Efficiency gains have reduced network outage durations by 20 to 40 minutes per incident and improved spectral efficiency by up to 25%, while AI-driven customer service enhancements yield approximately 25% higher satisfaction scores and reduce abandonment rates by 10 to 20%.

Despite this rapid progress, persistent barriers—such as prolonged legacy system integration timelines extending 3–5 years, significant cost premiums inflating capital expenditures by up to 40%, and complex compliance demands driven by jurisdictional diversity—temper the pace of full-scale AI adoption. Strategic initiatives, including adoption of AI-native 6G architectures, robust AI governance frameworks centered on TRiSM, targeted workforce reskilling, and collaborative ecosystem partnerships, are critical to unlocking AI’s transformative potential in telecom. The Asia-Pacific region’s rapid 5G advancement contrasts with Europe’s stringent regulatory regime and the fragmented US market, shaping divergent investment and deployment trajectories through 2026 and beyond.

Introduction

The telecommunications industry is undergoing a profound transformation fueled by the rapid maturation and integration of artificial intelligence (AI) technologies. From network optimization to customer experience personalization, AI’s incorporation into telecom operations is accelerating at an unprecedented pace, reshaping traditional business models and operational paradigms. This transformation is occurring amidst a confluence of technological advancements—such as edge computing and dedicated AI chipsets—and rising demands from expanding 5G and IoT deployments, creating a critical inflection point for the sector.

This report examines how AI is driving a step-change in telecom performance, highlighting quantifiable improvements in revenue growth, operational efficiency, customer satisfaction, and security responsiveness. It addresses the multifaceted challenges hindering seamless AI integration, including legacy infrastructure constraints, capital intensity, regulatory complexity, and competitive dynamics within AI ecosystems. The purpose is to provide a comprehensive overview of current industry trends, identify persistent obstacles, and chart strategic pathways for sustained AI adoption and innovation in telecom.

The scope encompasses a detailed analysis of AI’s impact on core telecom functions such as network intelligence, customer service, security orchestration, and infrastructure optimization. It further contextualizes regional variations in deployment and investment, considers emerging technological and governance frameworks, and evaluates talent and partnership strategies crucial for realizing AI’s full potential. Ultimately, this report aims to inform decision-makers, investors, and industry stakeholders about both the opportunities and imperatives shaping the future of AI-powered telecommunications.

Infographic Image: Infographic

1. AI-Powered Telecom Transformation Amidst Growth and Integration Challenges

Defining the Inflection Point: Why the Telecom AI Surge is Unprecedented Now

This subsection establishes the critical context for understanding today’s telecom market dynamics by pinpointing why the ongoing wave of AI adoption represents a unique inflection rather than incremental progress. It lays the foundation for subsequent analysis by quantifying the acceleration of AI integration within telecom relative to past technological shifts and relative to other industries. This framing clarifies the urgency for strategic positioning amid compounding competitive advantages emerging from AI expansion.

Quantifying the Acceleration of AI Adoption in Telecom (2020-2025)

Between 2020 and 2025, the telecom sector witnessed a dramatic acceleration in AI adoption, transitioning AI from experimental pilot projects to critical enterprise infrastructure. By 2025, over 70% of telecom companies had integrated production AI workloads into core operations, a leap that outpaces previous tech waves such as initial 4G rollouts or digitization efforts. This surge corresponds with global AI spending reaching $154 billion, underscoring the scale of investment fueling transformative use cases ranging from network optimization to intelligent customer service.

Driving this rapid uptake is the convergence of multiple technological and economic factors. First, improvements in edge computing and dedicated AI chipsets now allow real-time analytics directly at network nodes, overcoming latency bottlenecks inherent in centralized cloud models. Second, the intensifying demands of expanding 5G and IoT deployments necessitate automation and predictive capabilities that only AI can provide efficiently. Together, these forces create a feedback loop: enhanced AI capacity improves network performance, which in turn underpins more ambitious AI use cases, accelerating adoption beyond any previous technology cycle.

Specifically, AI integration rates in telecom jumped from 15% in 2020 to an anticipated 75% by 2025, demonstrating the sector’s rapid embracement of AI workloads, outstripping many industrial timelines and signaling a transformative operational shift [Chart: AI Adoption in Telecom (2020-2025)].

Benchmarking Telecom AI Growth Against Broader Industry Trends

When benchmarked against other sectors, telecom’s AI integration exhibits an above-average acceleration rate. While AI adoption broadly expanded across technology, industrial automation, and smart cities over recent years, the telecom industry’s AI market size alone grew more than fivefold within five years—reflecting a higher intensity of use case penetration and revenue impact. This dynamic positions telecom not just as a passive consumer of AI capabilities but as a frontline innovator shaping AI’s operational maturity.

However, this accelerated growth also introduces unique structural stresses. The telecom sector’s heavy reliance on legacy infrastructure constrains seamless AI integration, and capital-intensive network upgrades compete with funding AI deployments. Nevertheless, the telecom industry is embracing AI more aggressively than many traditional sectors due to the direct operational and competitive imperatives that real-time network intelligence provides. This competitive momentum embeds AI capabilities as a key differentiator in market positioning going forward.

Having established that telecom stands at an unprecedented inflection point characterized by rapid and deep AI adoption, the next sections will quantify the scale and specificity of AI’s value creation within the sector, setting the stage to explore both operational breakthroughs and persistent challenges.

Measuring AI’s Disruptive Value: Revenue Upsurge, Efficiency Gains, and Service Excellence

This subsection quantifies the substantial impact of AI integration in the telecom sector by presenting recent data on revenue growth driven by AI initiatives, empirical evidence of operational efficiency improvements in network management, and clear indicators of enhanced customer service outcomes. Establishing this numerical and performance-based foundation is critical to crystallize AI's transformative role and underscore the competitive differentiation it creates among operators.

AI-Driven Revenue Growth Trajectories in Telecom, 2023–2026

Telecommunication operators are experiencing a pronounced acceleration in revenue streams attributable to AI adoption, particularly in areas such as network automation, AI-powered customer solutions, and enterprise B2B services. Recent forecasts demonstrate that AI-centric telecom revenues are expanding at a compound annual growth rate well above the traditional telecom growth, with market valuations for AI infrastructure solutions in telecommunications projected to multiply by more than fivefold between 2022 and 2027. This surge is driven by operators channeling investments towards AI-enabled platforms, including cloud-based AI services, AI-powered network orchestration, and AI-driven data center expansions.

Leading operators such as SK Telecom have exemplified this trend, reporting a revenue increase in the order of several percentage points year-over-year in 2024 that is largely credited to AI business units, even as legacy wireless segments show slowing growth. Industry-wide, AI-enabled revenue streams are becoming a significant portion of total income for progressive operators, signaling a strategic pivot to AI as a core growth engine rather than ancillary support. This shift reflects a broader market recognition of AI’s potential to unlock new monetization levers beyond traditional connectivity offerings.

Quantifying Efficiency Gains in Network Management Through AI Integration

AI's deployment in network management is delivering measurable efficiency improvements by enabling predictive maintenance, automated fault detection, and real-time traffic optimization. Operators have reduced system downtime substantially by leveraging AI algorithms that anticipate network failures before they manifest, allowing proactive interventions that minimize service disruptions. These capabilities have translated into shorter outage durations and enhanced spectral efficiency, optimizing bandwidth allocation dynamically in response to fluctuating demand patterns.

The transformation from manual and reactive network management to AI-driven closed-loop control systems has allowed operators to achieve operational cost reductions while sustaining high-quality service delivery. Furthermore, the distinction between AI-native network architectures and overlay AI solutions highlights a critical efficiency vector; networks built with integrated AI capabilities from inception demonstrate superior responsiveness and resource utilization compared to retrofitted legacy systems. The cumulative effect is a network ecosystem that operates with increased agility, robustness, and capacity to handle growing data volumes and diversified service requirements.

Customer Service Enhancements: AI's Role in Elevating User Experience Metrics

AI-powered customer service tools have transitioned from scripted voice response systems to advanced contextual conversational agents capable of understanding user intent and adapting responses accordingly. This evolution has resulted in significant improvements in customer satisfaction scores, as AI chatbots and virtual assistants provide instantaneous support, reducing typical query resolution times and lowering abandonment rates.

Recent studies show that the integration of emotional intelligence capabilities within AI-driven virtual assistants is emerging as a key differentiator, enabling more empathetic and personalized interactions that foster higher user engagement and loyalty. Additionally, projected cost savings from AI-based customer service automation are substantial, with industry estimates highlighting billions of dollars in annual savings for telecom operators by the mid-2020s. This double effect of enhancing the customer experience at scale while reducing operational expenses exemplifies AI’s broad reach across service domains.

Having established AI’s quantifiable contributions to revenue growth, operational efficiency, and customer experience enhancement, the analysis naturally progresses towards examining how these transformative effects manifest across core telecom functional areas and the challenges that complicate full-scale adoption.

2. Operational Transformation: Core Functions Reinvented

Network Intelligence: From Reactive Management to Predictive Autonomy

This subsection delves into the revolutionary shift in telecom network management driven by AI, focusing on how intelligence embedded within networks transitions operations from traditional reactive models to predictive, autonomous control. It anchors the broader analysis of operational transformation by quantifying AI’s impact on network reliability and efficiency, comparing emerging AI-native architectures with existing overlay approaches. These insights provide critical foundations for assessing the evolving competitive landscape and technology strategy.

Substantial Reduction in Outage Durations Enabled by AI-Driven Proactive Management

Advanced AI algorithms facilitate the early detection of faults and enable dynamic corrective actions, contributing to significant decreases in service interruption durations. Empirical evidence indicates that AI-powered networks demonstrate median reductions in outage durations by approximately 20 to 40 minutes per incident compared to traditional reactive systems. These gains arise primarily through real-time anomaly detection and predictive maintenance which preemptively address faults before major failures occur.

Further analysis of weather-related outage data reveals that AI-driven predictive models smooth incident response even amid adverse conditions, maintaining lower average downtime. While extreme weather events still impose challenges, AI's capability to isolate faults quickly and reroute traffic effectively minimizes overall service impact. The cumulative effect is a notable uptick in network reliability critical for supporting latency-sensitive applications and expanding connectivity demands.

Measurable Spectral Efficiency Gains and Network Resource Optimization

AI integration in resource allocation and spectrum management has yielded quantifiable improvements in spectral efficiency, with studies documenting efficiency gains ranging from 10% to 25% over legacy manual optimization techniques. Machine learning models continuously assess traffic patterns and interference metrics to dynamically reassign spectrum and modulate power levels, achieving denser resource utilization without compromising quality of service.

These efficiency improvements enhance overall network capacity, enabling operators to accommodate increased data volumes and support emerging use cases such as IoT and immersive media. The continuous feedback loops intrinsic to AI-powered closed-loop control facilitate real-time adaptation, outperforming static configuration and traditional heuristic approaches.

Market and Technology Trends Favoring AI-Native Architectures over Overlay Implementations

The transition from AI as a supplementary overlay in 5G networks to fundamental AI-native architectures in 6G signifies a strategic realignment within the telecom industry. AI-native networks embed intelligence deeply within core functions such as resource management, service orchestration, and network slicing, enabling zero-touch automated operations and self-optimization capabilities.

Adoption rates for AI-native architectures are accelerating among leading operators and vendors, outpacing overlay implementations that layer AI atop existing legacy infrastructure. This emerging preference reflects the superior agility and scalability of AI-native designs, which address the increasing complexity and operational scale anticipated with future 6G deployments. Market data suggest early 6G trials and investments heavily favor AI-native frameworks, positioning them as an essential competitive differentiator in upcoming network generations.

Correspondingly, the projected revenue growth driven by AI initiatives in telecom is substantial, with estimates indicating an increase from $40 billion in 2023 to $150 billion by 2026, predominantly fueled by advancements in network automation and AI-native solutions. This underscores the financial incentive for operators to prioritize AI integration at the architectural core rather than as an overlay [Chart: AI-Driven Revenue Growth Trajectories in Telecom (2023-2026)].

Having established the concrete performance enhancements and strategic direction of AI integration in network management, the subsequent analysis will explore AI’s transformative role in redefining customer experience, security postures, and infrastructure utilization, continuing the comprehensive examination of telecom operational evolution.

Customer Experience Engineering: Personalization at Scale Driving Satisfaction and Loyalty

This subsection examines how AI technologies are reshaping customer engagement in telecommunications by delivering highly personalized and context-aware experiences. It quantifies measurable improvements in customer satisfaction and retention, highlights key reductions in abandonment rates post-AI adoption, and assesses the emerging sophistication of emotional intelligence embedded in virtual assistants. Positioned within the operational transformation framework, this analysis demonstrates how AI-driven customer experience engineering translates into competitive advantage amid sector-wide digital disruption.

Quantified Improvements in Customer Satisfaction Through AI Personalization

AI implementation in telecom customer service has resulted in significant uplifts in satisfaction metrics. Providers that leverage AI-driven personalization report approximately 25% higher customer satisfaction scores compared to legacy systems, a testament to AI’s ability to deliver contextually relevant and timely responses at scale. These gains are supported by the automation of routine inquiries and the seamless handoff of complex interactions to human agents, markedly enhancing the overall user experience.

In addition to increased satisfaction, AI platforms reduce customer effort by analyzing interaction data in real time, enabling dynamic adaptation of support flows. This results in greater engagement—up to 10% higher—driving stronger customer loyalty and advocacy. The migration from scripted IVR to intelligent conversational agents allows telecom operators to deliver more nuanced and proactive service, further consolidating these satisfaction improvements.

Reduction of Customer Abandonment Rates Following AI Adoption

Post-AI deployment, telecom providers have observed notable declines in call and chat abandonment rates. Efficiency gains from AI-assisted routing and response acceleration yield reductions ranging between 10% and 20%, depending on the maturity of implementation. These decreases stem from shorter wait times and improved first-contact resolution enabled by AI's predictive and contextual capabilities.

Automated conversational platforms play a critical role by engaging customers immediately, handling high volumes of inquiries without degradation in quality. This responsiveness mitigates customer frustration and supports sustained engagement. Furthermore, AI-driven analytics identify pain points leading to drop-offs, allowing targeted process improvements that curb abandonment proactively. Collectively, these effects contribute to diminished churn and enhanced lifetime value.

Emerging Emotional Intelligence in Virtual Assistants Elevating User Interaction

The integration of emotional intelligence capabilities into virtual assistants marks a pivotal advancement in telecom customer experience. By detecting sentiment and tone, AI agents can modulate responses, adapt escalation triggers, and personalize dialogue strategies to align with customer moods and preferences. This refinement enhances not only satisfaction but also trust and perceived empathy, critical factors in competitive differentiation.

Leading telecom companies are deploying increasingly sophisticated AI agents that move beyond transactional interactions toward agentic AI — systems capable of autonomous decision-making and proactive service delivery. These virtual assistants handle complex troubleshooting while maintaining a human-like conversational flow, supporting millions of interactions monthly. Despite being in early stages, this maturation bolsters user engagement by creating more natural, reassuring, and effective communication channels.

Having established the substantial gains AI delivers in customer experience through personalization, abandonment reduction, and emotional intelligence, the analysis now turns to how these operational enhancements integrate with network management, security, and infrastructure optimization to sustain holistic performance improvements across telecom operators.

Security Orchestration: AI-Driven Adaptive Defense and Emerging Vulnerabilities

This subsection explores the critical role of AI in revolutionizing telecom security by dramatically reducing breach dwell times and accelerating incident responses. At the same time, it carefully examines how expanding hyper-connectivity and AI system complexity simultaneously broaden the attack surface, introducing new risks that demand strategic management. This analysis balances measured performance improvements against emerging vulnerabilities to provide a holistic view of AI-enabled security transformation within telecommunications operations.

Transforming Breach Dwell Time: Hours Shaved Through AI Automation

Telecom operators employing AI-enhanced security systems have realized measurable reductions in breach dwell times, often decreasing threat persistence within networks by multiple hours. AI-powered anomaly detection and continuous behavioral monitoring facilitate earlier identification of malicious activity compared to traditional signature-based approaches. Automated containment protocols and dynamic threat prioritization allow security teams to isolate compromised network segments rapidly, curbing potential lateral movement of adversaries.

Studies indicate that leveraging AI-driven vulnerability prioritization improves mitigation focus, enabling operators to concentrate remediation efforts on the highest-risk exposures promptly. This targeted approach shortens dwell times by accelerating the identification-to-response cadence, substantially lowering the window of opportunity for adversaries to exploit network weaknesses. By integrating these capabilities, telecom providers achieve a critical advantage in maintaining network integrity and customer trust.

Accelerating Incident Response Cycles: AI-Built Efficiency Gains Over 40%

Incident response cycles in telecom security frameworks have improved dramatically through AI orchestration, with documented reductions of approximately 40% or more in time-to-containment metrics. Automated playbooks and AI-enabled decision support empower security teams to execute consistent, rapid countermeasures that minimize human error and delay. Machine learning algorithms continuously refine response strategies by assimilating new threat intelligence and network telemetry, enhancing operational agility in evolving cyber threat environments.

Complementing AI automation is the indispensable role of skilled human oversight, ensuring critical judgments are made where contextual nuance is required. This collaboration between AI and security personnel boosts compliance adherence and ultimately compresses the overall incident lifecycle—from detection, through investigation, to resolution. As a result, telecom providers are better positioned to maintain service availability and mitigate reputational damage during cyber events.

Expanding Attack Surfaces: Hyper-Connectivity and AI’s Double-Edged Security Impact

While AI bolsters telecom security efficacy, it concurrently introduces complexity that expands the attack surface. The proliferation of interconnected devices, network slicing in 5G and beyond, and AI-augmented operational layers create numerous potential vectors for exploitation. This widened exposure includes vulnerabilities inherent in third-party AI components, data integration points, and emerging edge computing nodes.

The dynamic nature of AI systems—capable of autonomous learning and self-modification—adds layers of unpredictability that adversaries may seek to manipulate. As hyper-connectivity grows, so too does the challenge of maintaining comprehensive, real-time visibility across distributed assets and hybrid infrastructures. Telecom security strategies must therefore evolve beyond traditional perimeter defenses to incorporate adaptive, AI-informed risk assessments and continuous validation processes, balancing the power of AI with heightened vigilance against novel threats.

Having examined how AI fundamentally reshapes telecom security operations—significantly improving detection and response while introducing new vulnerabilities—this discourse naturally leads to the broader operational transformation experienced industry-wide. The following sections will detail how these advancements intertwine with network management, customer experience, and infrastructure optimization, forming an integrated framework of AI-driven telecom innovation.

Infrastructure Optimization: AI-Driven Resource Efficiency and Network Densification

This subsection deepens the examination of AI's role in optimizing telecom infrastructure, a critical pillar supporting the sector’s operational transformation. By quantifying AI-enabled improvements in spectrum reuse, energy consumption, and the balance between edge and centralized orchestration, it elucidates how resource allocation innovations underpin broader network performance and sustainability goals. This analysis bridges high-level transformational themes with precise, actionable operational metrics.

Quantifying AI-Enabled Spectrum Reuse Gains through Network Densification

Artificial Intelligence has facilitated a marked improvement in spectrum reuse rates, primarily by enabling more sophisticated network densification strategies. Operators employing AI-powered radio resource management algorithms have achieved increases in spectrum efficiency on the order of 12 to 18 percentage points compared to legacy static allocation methods. These gains emerge from AI’s capability to dynamically analyze traffic patterns and environmental conditions in real time, supporting fine-grained frequency reuse and spatial multiplexing.

The shift from manually configured cell planning to AI-driven autonomous resource coordination reduces interference overlap and optimizes spectrum allocation at a granular level. This advancement is particularly critical in dense urban deployments, where spectrum scarcity is acute and efficient allocation translates directly into capacity enhancements without additional spectrum procurement. Thus, AI acts as an enabler for squeezing maximal usage out of finite spectral assets while maintaining quality of service.

Energy Efficiency Improvements Correlated with AI Adoption in Network Operations

Telecom operators integrating AI into their energy management frameworks report significant reductions in energy consumption per bit transmitted, with decreases ranging between 15% and 22%. These efficiencies stem from AI’s ability to orchestrate load-adaptive power management, predictive maintenance, and real-time fault diagnostics, minimizing unnecessary energy expenditure.

For instance, predictive analytics driven by machine learning models forecast traffic surges and enable pre-emptive resource scaling, thereby avoiding energy waste during low-demand periods. Moreover, AI-enhanced hybrid energy systems, combining renewable sources with smart grid components, facilitate more sustainable operations by optimizing energy sourcing and storage. The convergence of digital intelligence and green energy technologies presents a pathway to meet rising data demands while curtailing carbon footprints.

Balancing Edge and Centralized AI Orchestration in Next-Gen Networks

Operational data reveals that current telecom infrastructure increasingly relies on a hybrid orchestration model, leveraging both edge-based AI compute resources and centralized cloud platforms. Approximately 60% of AI-driven network control functions are executed at edge nodes to enable ultra-low latency responses critical for real-time operations, including anomaly detection and localized traffic steering.

Conversely, centralized orchestration manages broader network-wide optimization tasks, including long-term capacity planning and AI model training. This duality balances computational efficiency and responsiveness; while edge AI reduces backhaul loads and accelerates immediate decision-making, central cloud systems provide the scalability and data aggregation necessary for refining AI models and coordinating multi-site deployments. This operational balance is a defining characteristic of next-generation telecom networks, optimizing both performance and resource utilization.

Having established how AI-driven advancements concretely elevate infrastructure effectiveness through enhanced spectrum reuse, energy savings, and orchestration paradigms, the focus now shifts to dissecting foundational barriers that temper these gains. Understanding the persistent challenges in integrating these innovations within entrenched systems and regulatory frameworks is essential to charting viable strategic pathways forward.

3. Persistent Barriers: Understanding Constraints

Architectural Debt: The Challenge of Legacy Integration in AI Telecom

This subsection critically examines the structural impediments posed by entrenched legacy systems to the assimilation of AI capabilities within telecommunications. By quantifying adoption timelines and cost premiums, it elucidates the often underestimated complexity and expense involved in modernizing foundational architectures, a pivotal barrier that shapes the sector’s digital transformation trajectory.

Migration Timelines: Phased Integration Realities

The integration of AI into telecommunications networks faces significant temporal challenges, with migration from legacy operations support and business support systems often extending beyond typical technology deployment cycles. These extended timelines are the result of the monolithic nature of core legacy platforms designed for stability rather than modularity, which necessitates a phased, multi-year approach to modernization. Operators commonly experience integration horizons spanning three to five years, during which incremental AI capabilities are layered onto existing infrastructure to mitigate risks and ensure service continuity.

This phased migration strategy allows for progressive validation of AI systems in production environments but inherently delays the realization of full-scale AI-driven benefits. The complexity further compounds when legacy systems lack consistent data schemas or standardized interfaces, requiring bespoke bridging solutions. These architectural constraints demand that operators adopt a disciplined roadmap synchronized with broader network evolution initiatives, reinforcing the criticality of early strategic planning to avoid costly midstream disruptions.

Cost Premiums: Financial Implications of Gradual Modernization

The financial burden associated with integrating AI alongside legacy systems significantly exceeds that of greenfield deployments. Cost premiums arise from dual operating environments where new AI-enabled elements must coexist and interoperate with aged monolithic OSS/BSS platforms. These premiums reflect both direct capital expenditures for incremental interface development and the elevated operational expenditures from maintaining parallel, often redundant, platforms during transition phases.

Budgetary analyses reveal that phased legacy upgrades can inflate deployment costs by 20-40% compared to all-at-once replacements, driven largely by the complexity of custom integration, extended timelines delaying ROI, and the need for specialized, scarce talent. Organizational resistance contributes an indirect cost dimension, as protracted change management delays decision-making and hampers the scaling of AI initiatives. These financial dynamics necessitate careful cost-benefit modeling that incorporates the risks and uncertainty inherent in incremental legacy modernization.

Understanding the deeply rooted architectural inertia and associated cost structures provides a vital foundation for appreciating the broader economic and regulatory challenges explored in subsequent sections, framing a holistic view of the constraints limiting AI’s transformative potential within telecom.

Economic Realities: Navigating Investment Trade-offs and Financial Barriers in Telecom AI Integration

This subsection probes the financial dimensions influencing the pace and scale of AI adoption in the telecom sector. It fleshes out the underlying cost-benefit dynamics and investment calculus, with a particular focus on challenges facing mid-tier operators. This financial lens complements other technical and regulatory discussions by clarifying how returns and capital constraints shape strategic choices for telecommunications firms.

Balancing ROI Horizons Against the Capital Intensity of AI Deployments

Telecommunications operators face a complex investment landscape when deploying AI technologies, characterized by substantial upfront capital requirements alongside uncertain payback periods. The acquisition of AI infrastructure—encompassing advanced GPUs, data centers, and sophisticated cooling systems—drives a steep increase in total cost of ownership. The capital expenditure (capex) demand is compounded by ongoing operational expenses (opex) tied to energy consumption and maintenance, which are non-negligible given AI’s high power intensity.

Benchmarking return on investment (ROI) horizons reveals that while large, integrated operators can amortize costs over extended periods due to scale and diversified revenue streams, mid-tier and smaller carriers encounter less favorable economics. The initial investment often outpaces near-term gains in efficiency or revenue, elongating payback periods typically beyond conventional industry thresholds. This disparity contributes to a pronounced gap between early adopters with AI-capable infrastructure and those constrained by capital access, thereby amplifying competitive divergence within the sector.

Mid-Tier Carriers Confront Financial Constraints Impacting AI Adoption Trajectories

Financial constraints constitute a critical bottleneck for mid-sized telecom operators’ AI transformation initiatives. Empirical evidence highlights that financing obstacles restrict these players from securing both sufficient capital and affordable credit, impacting their ability to invest in cutting-edge technologies despite potentially strong productivity metrics. Market imperfections, such as limited access to favorable lending and equity markets, amplify the challenge, especially in emerging regions where financial systems remain underdeveloped and risk premiums are high.

This financial environment forces mid-tier carriers to rely heavily on internally generated funds, which constrains investment volumes and curtails rapid technology migration. The paucity of external financing results in delayed AI infrastructure rollouts, exacerbating legacy system dependency and limiting these carriers’ capacity to capture AI-driven operational efficiencies or enhanced customer engagement benefits. This cycle underscores the critical need for targeted financing solutions and strategic partnerships to bridge capital gaps and foster inclusive technological advancement across the market spectrum.

Understanding the capital allocation challenges faced by telecom operators, particularly mid-tier players, sets the stage for a broader discussion on the regulatory and structural factors that further shape AI adoption. The upcoming subsections will investigate how these financial realities interact with legacy system constraints, evolving policy environments, and competition dynamics to collectively influence AI-driven transformation trajectories.

Navigating Complex Compliance: Algorithmic Transparency and Data Sovereignty Challenges in Telecom AI

This subsection examines the intricate regulatory landscape shaping AI deployment within the telecommunications sector. Positioned in the broader analysis of persistent barriers, it elucidates how evolving mandates on algorithmic transparency and rigorous data localization requirements impose operational and strategic complexities. Understanding these compliance dimensions is foundational to anticipating legal risks, designing adaptable AI architectures, and sustaining competitive positioning amid regulatory fragmentation.

Differentiated Jurisdictional Requirements on Algorithmic Transparency

Telecom operators integrating AI face increasingly stringent and diverse demands for algorithmic transparency, reflecting policy efforts to enhance system explainability and fairness. While the European Union is advancing a comprehensive, risk-based framework mandating detailed disclosures of AI system functionality, including algorithmic logic and decision impact, other jurisdictions adopt variant transparency models. For instance, public sector uses often trigger heightened obligations for openness, with several countries requiring public registries of AI and algorithmic decision-making systems, empowering external scrutiny and accountability mechanisms.

However, these transparency regulations are far from uniform. The regulatory approaches span mandatory documentation and disclosures to voluntary guidelines emphasizing ethical AI. This divergence creates a complex compliance environment for telecom firms operating cross-border, requiring tailored transparency solutions that meet the strictest applicable standards while preserving commercial confidentiality. Challenges in providing meaningful explanations are compounded by the technical complexity and dynamic nature of AI models, where revealing underlying logic risks exposing proprietary innovations or inadvertently compromising user privacy.

Global Enforcement Timelines and Cross-Border Data Localization Impacts

Parallel to transparency, evolving data localization mandates are reshaping telecommunications AI deployment strategies. An accelerating global trend favors stricter controls on the storage and processing of data within national borders, ostensibly to safeguard privacy, national security, and digital sovereignty. This growing regulatory patchwork mandates compliance with overlapping or sometimes conflicting localization policies, forcing telcos to architect increasingly segmented data infrastructures to maintain market access.

The timing for enforcement of such data residency rules is intensifying, with several regions introducing phased implementation schedules extending into the mid-2020s. This creates strategic pressure on telecom operators to invest in localized data centers, modify data flow architectures, and enhance governance frameworks to avoid substantial penalties. Moreover, localization requirements complicate AI model training and real-time analytics that depend on large-scale, cross-jurisdictional data pooling, potentially impeding innovation velocity and efficiency in delivering AI-enabled services.

Addressing the multifaceted complexities of regulatory compliance demands telecom operators adopt proactive governance frameworks and invest in adaptable AI architectures. These steps are essential prerequisites before realizing the full transformative benefits of AI-driven innovation, as detailed in subsequent discussions on strategic imperatives shaped by standardization and ecosystem collaboration.

Competition Policy Challenges: Navigating Antitrust Risks and Interoperability Constraints in AI Ecosystems

This subsection probes the critical antitrust considerations shaping fair competition in telecom and broader digital markets, especially as AI technologies intertwine with platform control and ecosystem access. It examines recent regulatory scrutiny of partnerships and mergers involving AI assets while analyzing how legal settlements and platform policies impact API accessibility and interoperability. Positioned within the broader assessment of sector constraints, this discussion illuminates structural risks and governance dilemmas that could inhibit innovation and elevate market entry barriers amid expanding AI reliance.

Recent Antitrust Merger Outcomes Reflect Heightened Regulatory Vigilance

Recent regulatory scrutiny in major jurisdictions has intensified toward mergers and strategic partnerships involving leading AI and technology companies, reflecting growing concern about market concentration and the potential suppression of competition. Authorities, notably within the European Union, have closely examined alliances seen as granting disproportionate market power and control over critical AI assets. The oversight extends to large-scale collaborations where established firms integrate AI capabilities through partnership agreements, which may entrench incumbents and reduce the scope for emerging competitors.

Investigations into prominent deals, such as those involving embedded AI systems on flagship consumer devices, underscore the rising regulatory wariness. These reviews often focus on whether such integrations unfairly limit third-party participation or consolidate a monopoly over data flows and algorithmic capabilities. The potential chilling effect on innovation and market plurality forms a central rationale for this scrutiny, reinforcing an evolving antitrust paradigm attentive to the unique dynamics of AI ecosystems.

API Access Restrictions: Legal Settlements and Interoperability Implications

Access to application programming interfaces (APIs) emerges as a pivotal battleground for competition fairness within platform-controlled AI environments. Legal settlements in high-profile cases have addressed allegations that leading platform operators systematically restrict or limit third-party developer access to critical APIs, thereby consolidating their competitive advantage. These constraints effectively inhibit third-party innovation, limit feature parity, and reinforce vendor lock-in effects, placing smaller developers at a strategic disadvantage.

For example, restricting API endpoints that underpin essential functionalities—such as messaging protocols, payment systems, or biometric integrations—has been a recurrent source of contention. Remedy proposals often call for transparent API documentation and equitable access provisions, coupled where necessary with user consent frameworks for data sharing. However, even post-settlement environments see ongoing tensions, as the technical and commercial complexities of balancing proprietary interests with openness complicate the establishment of fully interoperable ecosystems.

The practical consequences of such API access limitations extend beyond developer ecosystems to impact end-user experience, platform diversity, and overall market fluidity. Regulators increasingly recognize that enforcement in this area must evolve alongside technological advances to preserve competitive neutrality and prevent ecosystem foreclosure.

Understanding how competition policy shapes AI ecosystems reveals the intricate interplay between regulatory frameworks and technological deployment strategies. These insights are vital for anticipating how emerging governance measures may constrain or facilitate AI-driven market innovation and inform strategic responses for operators navigating this evolving landscape.

4. Strategic Imperatives: Pathways Forward

Technology Roadmap: Converging Standards for Seamless AI Integration

This subsection delineates the near- to mid-term technical milestones essential for embedding artificial intelligence deeply within telecom networks. It builds on earlier discussions about AI-driven operational transformation by specifying how evolving standards—particularly for 5G-Advanced and forthcoming 6G—will synchronize industry development efforts. Clarifying rollout timelines, standardization phases, and interoperability requirements is critical for guiding R&D investments, vendor collaboration, and deployment strategies across telecom ecosystems.

Accelerating 5G-Advanced Rollout: Embedding AI in Network Functions

The 5G-Advanced evolution phase, scheduled for widespread deployment between 2024 and 2027, marks a pivotal step in operationalizing tighter AI integration within existing 5G infrastructure. Unlike the initial 5G release cycles where AI components largely functioned as auxiliary overlays, 5G-Advanced introduces enhanced AI-powered features—such as advanced traffic prediction, dynamic spectrum allocation, and intelligent energy management—directly into network protocols and control loops. These augmentations reportedly improve network responsiveness and resource efficiency, supporting zero-touch automation goals.

Industry consortia and standard bodies are prioritizing convergence on well-defined AI capability sets and open APIs to facilitate multivendor compatibility. Achieving early compliance and interoperability certification in this period is projected to substantially lower integration complexity and accelerate ecosystem maturation. This timeline aligns with operator trials focusing on AI-driven network slicing and edge orchestration, cementing 5G-Advanced as the foundation upon which full AI-native designs can build.

Mapping 6G Standardization Milestones: Embedding AI as a Native Network Core Element

The forthcoming 6G standardization efforts, targeted for ratification by 2030, represent a paradigm shift by embedding AI natively within fundamental network functions rather than treating it as an add-on. This 'AI-native' approach envisions autonomous networks capable of continuous learning, predictive decision-making, and adaptive resource orchestration—far surpassing the reactive or heuristic-based automation seen in 5G and 5G-Advanced. Key standardization phases include defining AI system roles in spectrum management, service orchestration, and energy optimization, alongside protocols for collaborative intelligence.

Active participation from global leaders in the telecom industry is driving frameworks that integrate AI governance, trustworthiness, and explainability directly into the 6G technical specifications. This embedded AI infrastructure is critical given the vastly increased network complexity, heterogeneity, and scale. The seamless integration planned in 6G will allow for zero-touch network operations and real-time adaptation to dynamic environments, enabling scalable deployments of ultra-reliable low-latency services and massive IoT connectivity.

Ensuring Multivendor Interoperability: Defining AI Interface Standards

A critical enabler for AI-powered telecom ecosystems is the establishment of common interface standards that allow AI components developed by diverse vendors to seamlessly interoperate. Industry efforts currently focus on standardizing data models, communication protocols, and AI lifecycle management APIs to ensure that AI-driven modules for network management, security orchestration, and customer experience can be integrated into heterogeneous operator environments without proprietary lock-in.

Achieving these interoperability targets requires balancing flexibility for innovation with stringent norms for data privacy, security, and performance. Early demonstrations have shown that adopting modular and containerized AI services governed by unified interfaces can significantly accelerate deployment cycles and reduce operational risks. This approach mitigates fragmentation risks in the market and enables operators to dynamically compose AI functions from multiple sources, optimizing for cost and capability.

With standards converging to embed AI deeply and interoperably across telecom architectures, operators and vendors must pivot to complementary organizational and governance adaptations. The subsequent subsections will explore the cultivation of new skillsets and cultural shifts, evolving partnership ecosystems, and responsible AI deployment frameworks that together realize the full promise of these technological advances.

Bridging Talent Gaps and Driving Cultural Synergy for AI-First Telecom Futures

This subsection examines the critical organizational transformations necessary to fully leverage AI within telecommunications. By assessing workforce readiness, upskilling effectiveness, and the integration of traditionally siloed functions, we illuminate how human capital and culture act as enablers or bottlenecks in AI deployment. Positioned within the strategic imperatives framework, this analysis informs how telcos can build resilient capability foundations to sustain competitive advantage amid AI-driven shifts.

Accelerating Demand for Advanced Data Science Expertise in Telecom AI

The rapid infusion of AI technologies into telecom necessitates a proportional surge in advanced data science competencies. Organizations report that the expanding scale and complexity of AI applications—ranging from predictive network analytics to real-time customer sentiment modeling—have outpaced existing talent pools. This mismatch results in elongated project timelines and suboptimal AI model outcomes, underscoring data science skill demand growth rates well above traditional training supply curves.

Quantitative surveys reveal that a significant majority of AI initiatives falter due to insufficient expertise in handling large-scale data engineering, algorithmic development, and interpretability analysis. Moreover, the nuanced understanding of telecom-specific data streams demands specialized domain knowledge rarely found outside the sector. Consequently, operators face an imperative to aggressively accelerate recruitment and internal development pathways targeting these overlaps between data science and telecom domain skills.

Evaluating the Effectiveness of Legacy Workforce Training for AI Integration

The transition from legacy telecom roles into AI-enriched functions hinges on reskilling programs' design and execution quality. Current evidence indicates mixed outcomes from these initiatives. Programs that combine foundational AI literacy with hands-on project involvement achieve faster technology adoption and stronger organizational buy-in than those relying solely on theoretical coursework.

Key performance metrics include reduced implementation timeframes, increased accuracy in AI-driven network diagnostics, and higher employee retention rates post-training. However, barriers remain significant; entrenched engineers show varied receptiveness to unfamiliar methodologies, and gaps in continuous learning infrastructures undermine long-term competency maintenance. Best practice cases demonstrate that iterative learning loops, mentorship pairings, and role evolution roadmaps substantially elevate upskilling impact.

Cross-Functional Collaboration as a Catalyst for AI Deployment Quality and Speed

Bridging the historically siloed domains of IT, data science, and radio engineering is pivotal for maximizing AI's transformative potential in telecom. Integrated cross-functional teams accelerate problem-solving by merging algorithmic insights with network operations expertise, enabling rapid iteration of AI models tuned to real-world constraints.

Successful organizational experiments reveal that metrics such as reduced model deployment cycles and improved issue resolution rates correlate strongly with established cross-disciplinary communication protocols and shared accountability frameworks. Cultivating a culture that values collaborative agility entails redefining leadership roles, incentivizing knowledge exchange, and embedding joint performance objectives. Such cultural integration directly translates into measurable AI deployment velocity and quality improvements.

Enhancing organizational capabilities through targeted skill development and cultural evolution is indispensable for overcoming operational challenges. The following sections build on these foundational shifts by outlining corresponding technological roadmaps and governance frameworks necessary to sustain and scale AI integration within telecom ecosystems.

Strategic Partnerships and Ecosystem Architectures Shaping Telecom’s AI Future

This subsection delves into how collaborative partnership models are critical strategic levers for telecom operators navigating the AI transformation. It examines the comparative dynamics of joint ventures versus acquisitions in accelerating time-to-market, the structuring of revenue-sharing mechanisms to align incentives in complex ecosystems, and the role of open-source contributions to reduce vendor lock-in and preserve agility within AI-driven telecom platforms. In doing so, it illuminates how partnership choices affect operational scalability, innovation velocity, and competitive positioning in an increasingly AI-centric market environment.

Speed and Agility: Comparing Joint Ventures and Acquisitions for Rapid AI Deployment

Joint ventures (JVs) in the telecom sector offer a pragmatic approach to diluting the substantial capital burden and operational risk associated with AI-driven infrastructure rollouts. Typical telecom JVs focused on AI and network modernization have demonstrated shorter average time-to-market compared to acquisitions, often by enabling modular development and leveraging complementary capabilities from partners. This is particularly evident in large-scale fiber deployments and cloud-edge integrations, where shared financial exposure and governance allow for agile adjustments amid evolving AI standards and technology shifts.

Conversely, acquisitions provide immediate control over targeted AI technologies or capabilities, consolidating assets swiftly under a single organizational umbrella. However, the integration complexity, cultural alignment, and legacy system harmonization inherent in acquisition post-merger processes often elongate realization timelines. Telecom mergers with a strategic AI focus frequently face delays in operational synergy capture, reflecting challenges in absorbing AI research and development teams and aligning divergent innovation cultures.

Empirical observations from recent telecom partnerships indicate that while acquisitions yield stronger long-term integration benefits, joint ventures remain favored for rapid scaling of AI services where time-to-market responsiveness and risk sharing outweigh full ownership imperatives.

Aligning Incentives: Designing Revenue-Sharing Models for AI Collaboration Success

AI-enabled telecom partnerships increasingly depend on sophisticated revenue-sharing frameworks to equitably distribute value generated from shared assets, data, and intellectual property. These models commonly incorporate milestone-based payments tied to innovation outputs or usage-driven royalties that directly correlate with AI service adoption and monetization across end customers. Such financial architectures encourage deep collaboration by linking partner success to outcome achievement rather than fixed fee arrangements.

Best-practice benchmarks demonstrate a trend toward multi-year contracts incorporating performance-based incentives and transparent reporting mechanisms. This approach mitigates common pitfalls such as misaligned priorities and technology lock-in, while fostering continuous co-investment in AI capabilities. Furthermore, flexible revenue-sharing agreements facilitate adaptive scaling and iterative enhancements essential in the fast-evolving generative AI space, particularly in use cases like AI-driven customer experience platforms and intelligent network automation.

Moreover, by integrating equitable revenue distribution with shared risk, operators and technology partners can engage in joint go-to-market strategies that maximize coverage and innovation diffusion without compromising individual commercial interests.

Breaking Dependency: Harnessing Open-Source Contributions to Mitigate Vendor Lock-In

Open-source participation is emerging as a critical strategy within telecom AI ecosystems to counteract vendor lock-in risks and ensure platform interoperability. Through active contribution to and utilization of open-source AI frameworks and tools, telecom operators preserve the flexibility to switch technology providers or customize capabilities without prohibitive costs or architectural constraints.

This open governance model fosters transparency, accelerates innovation through community-driven enhancements, and enables standardized interfaces that facilitate multi-vendor AI component integration. These factors are especially vital as telecom networks become increasingly software-defined and reliant on cloud-native AI orchestration layers.

However, open-source adoption requires dedicated internal expertise to manage security, compliance, and operational continuity challenges associated with shared codebases. Strategic partnerships anchored in open-source further enhance collaborative potential by pooling knowledge and distributing maintenance burdens, ultimately delivering resilient and sovereign telecom AI infrastructure.

Incorporating open source into AI ecosystem strategies also aligns with broader regulatory imperatives emphasizing data portability and digital autonomy, positioning operators to adapt to evolving policy landscapes while controlling total cost of ownership.

Building upon the understanding of partnership architectures, incentivization models, and open-source ecosystems, the ensuing analysis will explore how these strategic imperatives intersect with organizational culture shifts and technical standards convergence to fully capitalize on AI-driven telecom transformation.

Governance at Scale: Advancing Responsible AI Deployment Through TRiSM, Audits, and Bias Mitigation

This subsection critically examines the evolving frameworks and practical mechanisms that underpin responsible AI adoption within the telecom sector. As AI systems become increasingly embedded in core operations, rigorous governance protocols are essential to managing risks tied to fairness, security, and compliance. The analysis focuses on the maturity and adoption trajectories of AI Trust, Risk, and Security Management practices, the institutionalization of audit trails for AI model oversight, and the deployment of bias detection tools to safeguard ethical standards. These dimensions collectively define the backbone for sustainable AI integration and risk mitigation within telecom organizations.

Measuring TRiSM Adoption Among Telecom Operators in 2024-2026

The telecom sector currently leads in implementing AI Trust, Risk, and Security Management frameworks, reflecting heightened awareness of the complexities involved in managing AI innovation responsibly. From 2024 through 2026, adoption rates of comprehensive TRiSM practices among telecom entities have accelerated sharply, constituting the largest share of the overall IT & telecom segment’s commitment to AI governance. This trend is driven by the sector’s exposure to data protection imperatives, dynamic threat landscapes, and regulatory pressures that incentivize proactive risk management.

The rapid institutionalization of TRiSM involves both technological investments—such as sophisticated risk monitoring platforms—and organizational shifts that embed trustworthiness as a core operational metric. Telecom firms increasingly align AI deployment strategies with risk management protocols that systematically evaluate model reliability, transparency, and resilience. Such practices help mitigate incidents of data breaches, unauthorized data usage, and operational disruptions, thereby preserving both customer trust and regulatory compliance.

Tracking the Maturity and Implementation of AI Model Audit Trails

Comprehensive audit trail adoption has emerged as a critical enabler for AI governance in telecom operations. These audit mechanisms document AI model version histories, data lineage, and decision workflows rigorously, providing forensic capabilities and accountability across the AI lifecycle. Between 2024 and 2026, telecom operators have progressively integrated audit trail systems that support real-time monitoring, incident investigation, and regulatory reporting requirements.

The maturity of audit infrastructure correlates strongly with operator size and technological sophistication, with larger incumbents pioneering end-to-end traceability solutions. Such infrastructures enable rapid identification of model drift or anomalous outputs and facilitate iterative improvements, thus reducing operational risk. Moreover, well-maintained audit trails prove vital in demonstrating compliance with jurisdictional mandates on algorithmic transparency and explainability, a growing expectation from regulators and customers alike.

Evaluating the Effectiveness of Bias Detection Tools in Telecom AI Systems

Bias detection capabilities form a cornerstone of responsible AI, particularly in customer-facing and security-related telecom applications. AI models that inadvertently propagate bias risk eroding user trust and inviting regulatory scrutiny. Telecom firms have increasingly adopted automated bias detection tools embedded within development and deployment pipelines to identify discrimination patterns before models reach production.

Effectiveness assessments indicate that these tools have significantly reduced incidences of unfair treatment and opaque decision-making across operational domains, including customer service personalization and fraud prevention. However, challenges remain due to subtle, context-dependent biases and the difficulty of uncovering systemic disparities in complex data ecosystems. Continuous refinement of detection algorithms and incorporation of human oversight are crucial to ensure these tools deliver consistent protections aligned with evolving fairness standards.

Collectively, the advances in TRiSM adoption, audit trail implementation, and bias detection tools represent a foundational shift in how telecom operators govern AI-enabled processes. These frameworks address multifaceted risk vectors, ranging from cybersecurity to ethical compliance, thereby supporting a more resilient and trustworthy AI-infused telecom ecosystem. The subsequent analysis will explore how these governance capabilities intersect with broader strategic imperatives, including technical standardization and organizational transformation.

5. Investment Implications: Portfolio Positioning

Strategic Capital Deployment: Balancing Pure AI Innovators and Telecom Integrators Amid Evolving Valuations and Regulatory Triggers

This subsection addresses the crucial question of how investment portfolios should be constructed within the AI-driven telecom landscape. It specifically balances the allocation between pure-play AI companies—those driving core technology innovation—and incumbent telecom integrators that embed AI capabilities into established infrastructures. By analyzing revenue patterns, valuation multiples, and the impact of upcoming regulatory milestones, this section guides capital deployment strategies calibrated to market realities and emerging inflection points.

Financial Performance Disparities: AI Pure Plays Versus Telecom Integrators in the 2025 Horizon

Recent data highlights a striking divergence in revenue growth trajectories between pure AI firms and traditional telecom integrators. Pure AI companies are exhibiting rapid scale-up behavior, with some firms projecting revenue doubling year-over-year beyond 2025, driven by robust demand for AI infrastructure and service platforms. In contrast, telecom integrators, while benefiting from AI-driven efficiency gains, report more moderate revenue growth constrained by legacy client bases and longer sales cycles. This bifurcation is underpinned by AI pure plays’ agility in monetizing generative AI platforms and specialized AI infrastructure components, capturing outsized market share in emerging segments such as edge AI deployments and 5G-Advanced network solutions.

However, telecom integrators are not static; their advantage lies in their entrenched customer relationships and ability to bundle AI capabilities into broader network solutions. They tend to manifest steadier, albeit slower, revenue growth supported by ongoing modernization projects. Operators focused on hybrid approaches, leveraging both in-house AI innovation and partner ecosystems, are seeing improved contract sizes and recurring revenue streams. Consequently, portfolio strategies need to differentiate risk-return profiles, recognizing that pure AI firms command higher growth but also heightened volatility relative to integrators.

Valuation Multiples and Scalability: Decoding Premiums in AI-Centric Firm Assessments

Valuation metrics for AI-related firms reveal nuanced investor sentiment shaped by scalability potential and market positioning. Pure AI companies typically trade at premium multiples relative to incumbents, reflected in elevated price-to-sales and price-earnings ratios driven by anticipated outsized growth in AI compute demand, platform adoption, and data monetization. Notably, recent analyses confirm that some leading AI firms maintain gross margins around 60%, significantly higher than traditional SaaS peers, justifying multiples well above sector averages despite immature profitability profiles.

These valuation premiums correlate strongly with scalability characteristics: companies offering platform-based AI services with low incremental costs, broad addressable markets, and dominant ecosystem positions command higher investor confidence. Conversely, telecom incumbents, constrained by capital-intensive infrastructure and narrower margins, exhibit more modest multiples. Nonetheless, these integrators benefit from predictable cash flows and integration synergies, making their valuations attractive in balanced portfolios seeking defensible downside risk. Strategic capital allocation must therefore weigh growth levers against stability, factoring in market cycle phases and capital structure nuances.

Regulatory Catalysts: Sector Rotation Triggers and Their Impact on Investment Timing

Anticipated regulatory milestones in 2026 are poised to materially influence investment flows and sector rotation within AI-enabled telecom ecosystems. Key among these are data privacy regulations tightening cross-border data flows, algorithmic transparency requirements, and AI equipment certification standards, particularly in jurisdictions with rigorous compliance frameworks such as the European Union. These evolving mandates introduce both risk and clarity, potentially accelerating capital reallocation towards firms demonstrating governance robustness and compliance readiness.

Furthermore, market observers note that regulatory clarity often serves as an inflection point, catalyzing valuation re-ratings and renewed investor appetite. For instance, the scheduled finalization of AI operational frameworks and greater policy latitude in 5G-Advanced deployment are expected to shift investor sentiment towards ecosystem players that can rapidly commercialize compliant AI innovations. This regulatory maturation also triggers sector rotation signals favoring companies with demonstrated agility in navigating governance complexities, underscoring the need for continuous market monitoring in portfolio positioning strategies.

With a thorough understanding of capital allocation priorities shaped by growth performance, valuation dynamics, and regulatory timing, the investment implications section progresses to exploring geographic differentiation, where regional market idiosyncrasies further influence strategic portfolio positioning.

Divergent Regional Dynamics: APAC’s AI-Driven 5G Surge, EU’s Regulatory Rigors, and US Market Fragmentation Challenges

This subsection elucidates how geographic distinctions critically shape investment and operational strategies within the AI-enabled telecom landscape. By providing a detailed comparative analysis of APAC’s rapid 5G and AI deployment, the EU’s intensified compliance costs under evolving data privacy and AI regulations, and the United States’ fragmented market structure fostering modular yet complex AI adoption, this segment highlights region-specific drivers and constraints that influence portfolio prioritization and risk assessment across global markets.

APAC's Accelerated 5G Rollout as a Catalyst for Expedited AI Adoption

The Asia-Pacific region is manifesting a leadership position in global telecom innovation, underpinned by a markedly swift pace of 5G network deployments that considerably outstrip those seen in North America and Europe. National governments across APAC, notably in China, South Korea, Japan, and Australia, are channeling substantial public investments and regulatory support toward expanding 5G infrastructure, targeting coverage of urban and rural geographies with ambitious roll-out schedules through the first half of 2026. This rapid 5G build-out creates foundational capacity tailored for AI integration, enabling low-latency communication and high-throughput data exchange essential for AI-driven network automation and edge intelligence applications.

Beyond infrastructure, the concurrent escalation in AI R&D funding and AI-specific pilot projects within APAC operators solidifies the region’s positioning at the forefront of AI-enabled telecom transformation. This environment fosters competitive advantage for telecom firms adopting scalable AI solutions, accelerating their operational agility and service innovation. The nexus of 5G speed and AI capability is projected to amplify revenue streams and customer experience enhancements at a rate superior to markets with slower deployment cycles, thus justifying elevated investment focus in APAC-based companies or partnerships that leverage this growth vector.

EU’s Regulatory Landscape: Cost Structures and Compliance Impact on AI Deployment Economics

The European Union presents a contrasting context where advanced regulatory frameworks—most notably the Artificial Intelligence Act alongside rigorous data protection regimes such as GDPR—introduce substantive compliance overheads that materially influence AI solution design and deployment viability. Telecom operators and AI solution providers face layered costs associated with mandatory conformity assessments, transparency documentation, risk classification, and ongoing monitoring, cumulatively adding between 15% to 40% on top of baseline implementation expenses compared to US counterparts.

These elevated compliance expenditures extend beyond direct costs to include specialized legal consultation, internal privacy staffing, technical development, and training programs geared toward meeting stringent data localization, algorithmic transparency, and user rights stipulations. This regulatory milieu not only drives up operational budgets but also compresses ROI timelines, particularly impacting mid-tier and emerging EU-based telecom players with limited capital buffers. Investment decisions must therefore factor in such regional legal-economic trade-offs, as well as forecast timelines for full AI Act enforcement anticipated toward late 2025 to 2026, which will crystallize compliance obligations and penalties, necessitating proactive governance and transparency infrastructures to mitigate regulatory and reputational risks.

US Market Fragmentation: Modular AI Deployments Amid Diverse State-Level Regulations and Competitive Dynamics

In the United States, a fragmented regulatory landscape combined with a heterogeneous operator ecosystem produces a unique set of challenges and opportunities affecting AI adoption in telecom. The absence of a unified federal AI regulatory framework akin to the EU AI Act leads to significant variability at the state level, especially with an increasing number of states proposing or enacting privacy and AI-related legislation which complicates compliance for multi-state operators and AI vendors.

Simultaneously, the US telecom market is characterized by a wide spectrum of players ranging from national incumbents to smaller regional carriers, prompting a modular approach to AI system deployment that favors interoperability, vendor diversity, and agile integration over monolithic architectures. This fragmentation encourages innovatie, targeted AI deployments but also raises integration costs and complexity, impacting investment risk profiles and necessitating detailed assessment of regional customer bases and regulatory requirements. For investors, understanding these dynamics is critical to identifying operators or AI vendors positioned to capitalize on localized market adaptations while navigating compliance uncertainty.

Synthesizing these regional disparities underscores the imperative for investors and operators to adopt nuanced strategies calibrated to local market conditions, regulatory environments, and technological maturity. This geographic differentiation directly informs portfolio weighting, partnership selection, and risk mitigation approaches pivotal for harnessing AI-driven telecom growth while managing compliance and operational complexity.

Emerging Threats and Disruption Patterns: Quantum Risks, Hyperscaler Dominance, and Workforce Reskilling Imperatives

This subsection examines critical emerging threats and disruption vectors that are reshaping the investment landscape within the tech and telecom sectors amid rapid AI-driven transformation. By assessing the readiness for quantum computing impacts on cryptographic security, the competitive dynamics between hyperscalers and niche innovators, and the escalating need for workforce reskilling programs, we provide a nuanced risk framework that informs prudent portfolio positioning and strategic foresight.

Quantum Computing Readiness and Cryptographic Vulnerabilities by 2026

Quantum computing is nearing a stage where its capacity to undermine conventional cryptographic algorithms poses an imminent cybersecurity threat to telecom infrastructures. As quantum research accelerates, the risk to telecom networks, which rely heavily on encryption for data confidentiality and integrity, is escalating. Industry observations indicate increasing investments in quantum-safe protocols; however, widespread deployment and standardization remain nascent, leaving the sector exposed during this transition.

The telecom industry's current preparedness level is uneven, with leading operators initiating pilot programs for post-quantum cryptographic primitives but facing significant integration challenges given legacy architecture constraints. The investment community must factor in potential disruptions stemming from quantum-induced demands for rapid, capital-intensive security upgrades, as delayed adoption could trigger market share erosion due to compromises in customer trust and regulatory compliance.

Hyperscaler Expansion vs. Niche Innovators: Competitive Pressures and Market Share Dynamics

Global hyperscalers continue to consolidate their dominant market positions through massive AI-related capital expenditures projected to increase over 60% by 2026, fueling rapid innovation and infrastructure scaling. Their ability to design proprietary AI accelerators and deploy advanced data centers provides them with significant cost and performance advantages, creating formidable barriers to entry for smaller, specialized AI firms.

In contrast, niche innovators are carving out differentiated positions by focusing on cutting-edge, high-risk AI applications and vertical-specific solutions, striving to evade direct competition. Yet, their limited scale and dependence on hyperscaler cloud platforms increase vulnerability to pricing pressure and platform governance constraints. This asymmetric competitive dynamic exerts disruptive pressure on mid-tier technology providers and traditional telecom incumbents, necessitating strategic recalibration to harness partnerships or carve specialized market niches.

Workforce Reskilling Investments and Talent Realignment Accelerate Amid AI Integration

The rapid AI adoption trajectory intensifies demands for comprehensive workforce reskilling across telecom organizations, as routine roles decline and skilled technical employment rises. Forecasts show significant investment increases in upskilling programs targeting data science, AI ethics, and systems integration competencies, essential for sustaining productivity gains and operational continuity amid technological shifts.

However, disparities exist in reskilling reach, especially across SMEs and informal labor segments, risking uneven adoption and labor market dislocations. Executive priorities focus not only on hiring new AI-capable talent but also on redeploying existing staff to higher-value roles that complement AI capabilities. These trends underline a strategic imperative for investors and operators alike to anticipate near-term cost increments against the backdrop of long-term workforce competency transformations critical for competitive survival.

Having delineated the principal emerging disruptions and risks confronting the telecom and technology sectors amid AI-driven expansion, subsequent sections will explore strategic frameworks and investment paradigms designed to mitigate these challenges and capitalize on the evolving market landscape.

6. Synthesis and Recommendation

Integrated Action Plan: Concrete Targets, Organizational Revamp, and Measurable Governance for AI in Telecom

This subsection synthesizes prior analyses into a focused, actionable strategic framework designed to guide telecom operators through the complex journey of AI integration. It addresses the critical dimensions of adoption targets, organizational transformations, performance measurement, governance, and implementation timing. By converging these elements, it delivers a comprehensive roadmap for aligning technological ambition with operational readiness and risk management imperatives essential for sustainable success in AI-driven telecom evolution.