The Impact of Geopolitical Tensions on Indian Equity Markets

Understanding Market Volatility, Investor Sentiment, and Economic Risks Amid Global Uncertainties

Table of Contents

Executive Summary

This analysis assesses the profound impact of escalating geopolitical tensions on Indian equity markets, focusing on the interplay between regional conflicts, rising crude oil prices, and investor sentiment. Key findings reveal that geopolitical conflicts—particularly in West Asia and along India's borders—have heightened market volatility and risk aversion, triggering notable index corrections and fluctuations in sectoral performances.

Rising crude oil prices amid geopolitical disturbances have disproportionately affected India’s inflation outlook and economic growth expectations, reinforcing market uncertainty. Nonetheless, these disruptions have also created selective investment opportunities by inducing temporary undervaluations, enabling risk-aware investors to capitalize on market corrections within fundamentally strong sectors.

Introduction

Geopolitical tensions have increasingly shaped the dynamics of global financial markets, with emerging economies like India being particularly vulnerable due to their strategic location and economic dependencies. This analysis investigates the multifaceted relationship between ongoing geopolitical conflicts—especially those in West Asia and regional security challenges—and their ramifications on Indian equity markets.

Infographic Image: Impact of Geopolitical Tensions on Indian Markets: Key Insights 2024-2026

The scope of this study encompasses a detailed exploration of major recent geopolitical events, including the US-Iran standoff, India-Pakistan border tensions, and the Israel-Palestine conflict. It examines how these events influence crude oil prices, investor behavior, and market volatility, thereby affecting key indices and sector-wide performances across the Indian equity landscape.

Methodologically, the analysis combines qualitative assessments of geopolitical developments with quantitative market data, focusing on index movements, volatility metrics, and sector-specific impacts. This evidence-based approach aims to provide a comprehensive understanding of how uncertainty emanating from geopolitical risk translates into measurable market outcomes and informs investor decision-making.

1. Overview of Geopolitical Tensions Affecting Indian Markets

In an increasingly interconnected global environment, geopolitical tensions have become a pivotal force shaping the economic and financial landscape of emerging economies such as India. For Indian markets, situated at the confluence of South Asia and the energy-rich West Asian region, geopolitical disturbances reverberate beyond diplomatic corridors and military engagements—they directly influence market sentiment, trade flows, and economic stability. This section sets the foundational geopolitical context necessary for comprehending how external conflicts and regional rivalries act as catalysts for uncertainty that percolates through Indian equity markets. The examination of recent geopolitical flare-ups, India’s inherent vulnerabilities rooted in its energy dependence and border disputes, and the chronology of recent escalations collectively elucidate the multidimensional risks exerting pressure on India’s marketplace.

Indian markets remain acutely sensitive to geopolitical developments, given both the strategic importance of the region and the nature of India’s economic dependencies. While market reactions may appear as volatility and price corrections at a surface level, deeper causes often lie in the persistent and evolving external risks—such as tensions in West Asia involving the US and Iran, and protracted security challenges along India’s northern borders. These core geopolitical dynamics establish the external shockwaves that later manifest in market behaviors analyzed in subsequent sections. Recognizing these triggers is essential to unpacking the complex risk environment within which Indian investors operate today.

Key Recent Geopolitical Events

The period from late 2025 into early 2026 has been marked by a series of significant geopolitical events that profoundly impact India’s external environment. The ongoing US-Iran conflict looms large, punctuated by escalating rhetoric and threats of imminent military action. Notably, a declaration by then-U.S. President Donald Trump in April 2026 underscored a forthcoming severe strike on Iran, intensifying fears of disruptive conflict in the global oil corridors. This geopolitical fracas pushed Brent crude oil prices above $105 per barrel, directly stoking inflationary concerns within India due to its heavy reliance on imported petroleum products. Such escalation highlights the heightened sensitivity of Indian markets to fluctuations originating from West Asia’s geopolitical landscape. Parallelly, persistent security tensions between India and Pakistan continue to flare, with recent terrorist attacks in Kashmir contributing to geopolitical unease. The deadly attack in Kashmir in April 2025, which claimed 26 lives, triggered a diplomatic fallout, including India's suspension of the Indus Waters Treaty—an unprecedented move affecting bilateral relations and regional stability. These developments amplify investor anxiety, as historically, such security breaches along the border have precipitated short-term market jitters and longer-term concerns about regional peace and economic continuity.

Additionally, the Israel-Palestine conflict, particularly the Israel-Hamas hostilities, although geographically distant, have indirect bearings on India’s trade and diplomatic engagements. India’s bilateral services trade with Israel, amounting to approximately USD 1.3 billion, could face logistical and insurance-related constraints if maritime and air traffic premiums surge due to regional conflict escalation. Furthermore, ongoing trade disputes and tariff adjustments internationally feed into this geopolitical matrix, creating layers of complexity for India’s export-oriented sectors sensitive to global supply chain disruptions.

India’s Vulnerabilities to Geopolitical Risks

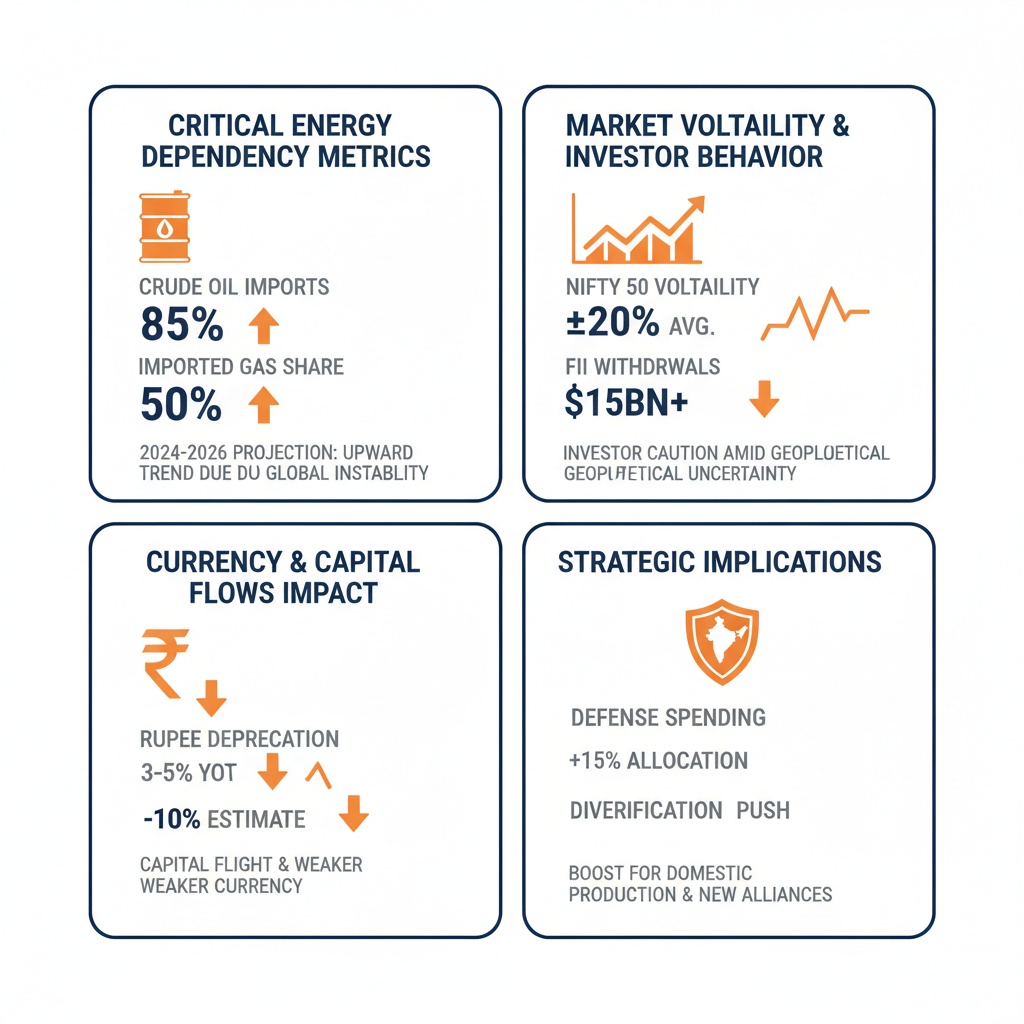

India’s economic and strategic susceptibilities stem primarily from two interlinked vulnerabilities: its dependence on imported energy resources and the protracted nature of border tensions that occasionally flare into conflict. Currently, India imports approximately 85% of its crude oil requirements, primarily from West Asia, a region historically prone to geopolitical shocks. Any disruption in supply chains or a surge in oil prices triggers inflationary pressures domestically, constraining growth outlooks and investor confidence. Given the 2026 spike to Brent crude prices above $105 per barrel, stemming from tensions in the Persian Gulf, India’s inflation trajectory tightened significantly, prompting concerns about cost-push factors affecting industrial output and consumer spending patterns.

Alongside energy reliance, India’s northern and northeastern borders remain sensitive flashpoints. The contestations along the Line of Actual Control (LAC) with China and ongoing hostilities with Pakistan in Jammu and Kashmir create a fragile security environment. These border tensions not only pose direct military and diplomatic challenges but also indirectly disrupt investor sentiment due to the impending risks of escalation. India’s security expenditures and resource diversion toward defense allocate fiscal space away from other developmental priorities, adding economic strain during geopolitical crises. Furthermore, these tensions often precipitate temporary restrictions and disruptions in trade routes, impacting cross-border commerce and supply chains vital to border states and manufacturing hubs.

Compounding these vulnerabilities is India’s exposure to capital flow volatilities triggered by geopolitical uncertainties. Foreign Institutional Investors (FIIs) have historically shown risk aversion during periods of escalated external conflicts, leading to sizable outflows and stock market sell-offs. For example, as observed in April 2026 during the US-Iran tensions, FIIs offloaded equities worth approximately ₹8,331.15 crore in just a single day. Such capital flight exacerbates currency depreciation pressures and market instability.

Timeline of Recent Escalations and Their Correlation with Market Volatility

The escalation timeline throughout the last 18 months underscores how geopolitical tensions have increasingly encroached upon India’s economic and financial stability. Key milestones include October 2024, which saw a brief rally in crude oil prices associated with the Israel-Hamas conflict, and May 2025, when the Kashmir terrorist attack triggered immediate security crackdowns and diplomatic responses. The subsequent reduction in bilateral cooperation with Pakistan, including the suspension of the Indus Waters Treaty in April 2025, represented a significant deterioration in regional relations and added to market uncertainties.

The crescendo occurred in April 2026 with renewed hostilities between the US and Iran. The announcement of intensified military action precipitated a spike in global crude prices by about 5%, impacting not just inflationary expectations but investor risk sentiment within India. Concurrently, foreign institutional investors responded with heavy equity sell-offs, while domestic institutional investors partially absorbed the shock with buying interventions. This dynamic interplay revealed the bifurcated investor response contingent on geopolitical news flow. Complementing these direct geopolitical events, ongoing disputes such as US-China trade tensions and tariff adjustments layered additional risk into the market environment, sustaining elevated volatility levels.

These sequential escalations collectively build a narrative of heightened geopolitical risk that creates an unstable backdrop for Indian markets. The timeline reveals how external conflicts and regional security dilemmas unfold into sustained investor anxiety and reactive market movements—key considerations to appreciate before analyzing subsequent empirical market data.

2. Market Response to Geopolitical Tensions - Volatility, Indices, and Sectoral Impact

The Indian equity markets have increasingly mirrored the turbulence emanating from geopolitical flashpoints, particularly conflicts in West Asia and regional security escalations. Building on the geopolitical event context of the prior analysis, this section examines how emerging risks have tangibly translated into measurable market disruptions. As geopolitical uncertainty intensifies, Indian benchmark indices have demonstrated heightened volatility and pronounced sectoral sensitivity, reflecting both external shocks and the domestic economic structure's vulnerabilities. The nexus between geopolitical tensions and market movements is crucial for understanding shifts in investor confidence and sector-specific performances, especially in a market deeply intertwined with global energy dynamics and capital flows.

Market fluctuations in India cannot be fully understood without recognizing crude oil's pivotal role. India's dependency on imported oil—particularly from regions vulnerable to geopolitical instability—renders its inflation outlook, currency valuation, and corporate profitability susceptible to external shocks. Each spike in crude prices reverberates through the markets, amplifying risk aversion and triggering discernible sell-offs in sectors bearing the brunt of cost pressures. This interplay amongst global geopolitical developments, commodity pricing, and domestic market performance underscores the complex, immediate impacts that geopolitical risk presents to Indian equities.

Index Performance Surrounding Key Geopolitical Events

A data-driven perspective reveals notable impacts on India’s primary equity indices, the BSE Sensex and NSE Nifty, in response to recent geopolitical escalations. For instance, on April 2, 2026, following heightened U.S.-Iran tensions and President Trump’s declaration of impending military action, the Sensex declined by approximately 1,434 points, or 1.96%, settling at around 71,700, while the Nifty plunged nearly 2%, losing 446 points to close near 22,234. This marked a sharp reversal from gains of over 1.6% recorded in the prior day, illustrating the market's sensitive reaction to geopolitical developments. The contrast between intra-week gains and sudden drops highlights the episodic nature of volatility induced by exogenous geopolitical shocks. Additionally, analysis of the India VIX, a barometer of short-term market fear, showed a 7.63% increase, closing at 12.73, signifying market participants’ expectations of increased price swings and uncertainty.

Historical data further emphasizes that Indian markets, while resilient over longer horizons, routinely experience knee-jerk declines during intensified geopolitical strains. Similar episodes in 2025 during escalating India-Pakistan tensions and separatist incidents in Kashmir led to sharp index corrections with BSE Sensex shedding over 600 points in a single session, accompanied by corresponding Nifty downturns below psychological thresholds like 24,000. These episodes underline the direct correlation between geopolitical flashpoints and investor risk aversion. Divergence between Foreign Institutional Investor (FII) outflows and Domestic Institutional Investor (DII) inflows also underscores differing investor behaviors. FIIs have been net sellers during turbulence—offloading equities worth billions of rupees—intensifying downward pressure on indices, whereas DIIs have played a partial stabilizing role, absorbing sell pressure amid volatile trading. The observed Sensex declines of 1,434 points in April 2026 and over 600 points during 2025 geopolitical events further quantify these impacts [Chart: Index Performance around Key Geopolitical Events].

In synthesis, the Indian equity indices depict a pattern wherein geopolitical shocks trigger immediate, sharp declines followed by periods of oscillating recovery, marking discernible market phases characterized by increased risk premiums and investor caution. The indexes’ susceptibility to sudden drops also reflects the broader global risk environment, where Indian markets react more acutely due to their economic openness and strategic vulnerabilities.

Crude Oil Price Trends and Their Market Implications

Crude oil price dynamics stand at the heart of the Indian market’s sensitivity to geopolitical tensions. The Strait of Hormuz—a critical chokepoint for 20% of global seaborne oil—has repeatedly been the flashpoint pushing Brent crude prices upward during regional conflicts. In recent months, Brent crude surged by upwards of 5-6% to reach and briefly exceed $105 per barrel amid rising West Asian tensions, notably involving the US and Iran. Such abrupt price movements exert inflationary pressures domestically, as India imports approximately 85% of its crude oil demand. The pass-through of surging oil prices into fuel and transportation costs cascades into broader consumer price indices, prompting concerns among market participants regarding eroding corporate margins and upward inflation.

Empirical data demonstrates that spikes in crude oil prices correlate strongly with rising market volatility and bearish investor sentiment in India. For example, when crude prices jumped above the $100 mark following the escalation of US-Iran hostilities, the Sensex and Nifty reacted with sharp sell-offs, accompanied by currency depreciation—Indian Rupee weakening to historic lows above ₹91-92 per USD. Inflationary pressures driven by oil costs threaten to widen India’s trade deficits and may trigger monetary tightening or constrain fiscal spending, which investors view as headwinds for economic growth and corporate earnings. Moreover, brokerage reports from leading financial analysts predict a moderation of corporate earnings growth in Q4 FY26 to around 10%, down from 15-18% in preceding quarters, largely attributed to cost pressures from oil and gas inputs.

Looking beyond immediate price surges, the sustained elevation of crude oil introduces a structural risk premium on Indian markets, reflecting deeper concerns over balance of payments and inflation control. Traders and fund managers closely monitor oil futures and geopolitical developments around oil transit routes, aware that protracted disruptions translate to sustained market volatility and sectoral recalibrations. This feedback loop between geopolitical risk, commodity prices, and market sentiment remains a defining characteristic of India’s financial market responsiveness.

Sectoral Impact: Banking, Energy, and Currency Dynamics

The ripple effects of geopolitical tensions and associated crude price volatility manifest unevenly across various sectors of the Indian equity market. Banking and financial services, energy companies, and currency-sensitive firms have borne the brunt of market fluctuations, though each responds to distinct underlying drivers.

The banking sector experiences indirect pressures from geopolitical upheavals, largely through tightening liquidity conditions and fluctuating investor confidence. During episodes of heightened tension, liquidity risk premiums rise and Non-Performing Assets (NPAs) concerns can intensify in stressed segments. For example, in periods following the Kashmir terrorist attack and India-Pakistan diplomatic escalations in 2025, major banks like Axis Bank witnessed depreciations linked to asset quality fears. Furthermore, elevated crude oil prices strain inflation and economic growth prospects, weakening credit demand and increasing risk aversion among lenders. However, some banking entities report marginal advances growth and deposit accumulation, helping cushion systemic shocks. The divergent investor response to changes in banking fundamentals versus geopolitical risk highlights the sector’s complex role as both a macroeconomic barometer and risk absorber.

The energy sector exhibits a distinctly bifurcated response pattern. Upstream oil exploration and production firms such as Oil and Natural Gas Corporation (ONGC) and Oil India Ltd. tend to benefit from rising crude prices, as their revenue realizations increase correspondingly. Conversely, Oil Marketing Companies (OMCs) like Indian Oil Corporation and Bharat Petroleum face margin squeezes due to under-recovery from fuel price adjustments lagging crude price surges. This upstream-downstream dichotomy complicates sector performance; for instance, integrated majors like Reliance Industries Ltd. balance upstream gains against downstream cost pressures. Higher crude prices also directly increase input costs for aviation, chemicals, paints, and logistics sectors, leading to margin contractions and share price sensitivity to cost inflation. Aviation stocks repeatedly exemplify sector vulnerability—fuel accounts for a sizable component of operational expenditure, and jet fuel cost surges often produce rapid share price declines during geopolitical crises.

Currency dynamics further compound market responses. The Indian Rupee consistently faces depreciative pressure amid geopolitical risk spikes, exacerbated by foreign portfolio investor outflows. For example, during recent geopolitical flare-ups, the Rupee weakened beyond ₹91 per USD, driven by FII net sales totaling over ₹83 billion in constrained periods. Currency depreciation amplifies corporate input costs, particularly for firms dependent on imported raw materials and capital goods, and raises inflationary expectations. The Reserve Bank of India's interventions, including currency futures restrictions, have thus far struggled to fully stabilize the rupee amid external shocks. This currency-market feedback loop intensifies volatility in sectors highly exposed to exchange rate fluctuations.

In sum, sector-wise impacts during geopolitical tensions are multifaceted and influenced by both direct cost effects—via crude oil price changes and currency movements—and indirect effects from investor sentiment shifts and liquidity dynamics. The dualisms within the energy sector, the nuanced credit cycle influences on banking, and the currency-linked risks create a layered risk profile that investors and policymakers must daily navigate.

3. Managing Risks and Investment Opportunities amid Geopolitical Challenges

As geopolitical tensions persistently inject volatility into Indian equity markets, the imperative for investors to adopt robust risk management and tactical investment strategies grows ever more critical. The multifaceted nature of geopolitical risk demands a nuanced approach that balances cautious preservation of capital with the pursuit of value-driven opportunities. Navigating this challenging environment involves not only understanding the immediate market disruptions but also embedding theoretical insights into practical portfolio responses that safeguard assets and capitalize on dislocations. This section distills a forward-looking, strategy-oriented perspective, synthesizing prior analyses on geopolitical triggers and market impacts into actionable guidance tailored for India’s unique economic and geopolitical landscape.

The hallmark of an effective response to geopolitical risk lies in mastering both mitigation techniques that counterbalance uncertainty and identifying pockets of relative strength amid market sell-offs. Indian investors face a heightened challenge due to the country's substantial dependence on imported energy and global trade links but also enjoy advantages afforded by a diverse and increasingly resilient economy. For example, Brent crude prices have risen from $85 in April 2025 to $105 by April 2026 amid West Asia tensions, exacerbating inflationary pressures and market volatility in India. By applying theoretical frameworks linking geopolitical stress to investment behavior alongside empirical insights gleaned from recent volatility episodes, stakeholders can better position portfolios to weather shocks and exploit cyclical adjustments. Ultimately, this paradigm blends caution with opportunism, empowering investors to transform geopolitical adversity into strategic advantage [Chart: Crude Oil Prices Over Recent Geopolitical Events].

Risk Mitigation Techniques: Diversification and Hedging

Central to managing the precarious nature of geopolitical disruptions is the principle of diversification—spreading investments across uncorrelated assets, sectors, and geographies to reduce idiosyncratic risk. Given India’s susceptibility to external shocks, particularly through energy import channels and trade relations, investors are advised to ensure their equity portfolios encompass a balanced mix of domestic sectors with varying sensitivities to geopolitical stress. For instance, while the energy and banking sectors may experience short-term margin pressures or currency-driven headwinds during geopolitical crises, sectors such as information technology and pharmaceuticals often show relative defensive characteristics due to their export orientation and geographical diversification of revenue streams.

Hedging strategies further complement diversification by directly offsetting potential losses through financial instruments. The use of derivatives, such as futures and options on indices like Nifty and Sensex or sector-specific contracts, can effectively limit downside exposure triggered by sudden geopolitical shocks. Currency hedges are particularly pertinent in the Indian context, as rupee depreciation driven by crude oil price surges or foreign capital outflows exacerbates market volatility. Investors employ forward contracts or currency options to safeguard against sharp forex fluctuations that can erode returns, especially for foreign institutional investors. Additionally, commodities such as gold have historically served as natural hedges, appreciating during geopolitical crises as a traditional safe haven, thereby offering portfolio ballast.

Theoretical perspectives underpinning these mitigations draw from modern portfolio theory (MPT) and real options theory. MPT advocates constructing an efficient frontier that minimizes portfolio variance for a given expected return — a principle vital during periods of heightened geopolitical uncertainty. Real options theory highlights the embedded managerial flexibility in investment decisions, encouraging investors to view exposure reduction (via hedging) as valuable options to preserve capital until uncertainty resolves. Academically and practically, combining these frameworks equips investors to optimize risk-return trade-offs amid the pervasive but often unpredictable geopolitical risk landscape.

Identifying Potential Value Buys During Market Dips

Volatility spikes induced by geopolitical tensions frequently lead to indiscriminate sell-offs, where high-quality companies with sound fundamentals suffer undue price depreciation. For disciplined investors, these episodes present strategic entry points to accumulate positions at attractive valuations. Essential to this strategy is rigorous fundamental analysis to distinguish transient market-driven price declines from genuine deterioration in corporate health or growth prospects. Historical episodes, including the recent West Asia conflicts and their aftermath in early 2026, demonstrate that several sectors—particularly domestic consumption-driven businesses, IT services, and pharmaceutical companies—experienced sharp but temporary corrections driven more by sentiment than earnings erosion.

Investment frameworks rooted in behavioral finance emphasize exploiting such market inefficiencies. During panic-induced downturns, the gap between intrinsic value and market prices widens, enabling contrarian strategies that benefit from eventual market normalization. For Indian investors, sectors relatively insulated from oil price inflation and currency volatility, or those set to benefit from government reforms and domestic demand growth, form promising value buy candidates. Furthermore, identifying companies with strong balance sheets, consistent cash flows, and competitive advantages can mitigate longer-term risk even amid geopolitical uncertainty.

It is also vital to consider the cyclical nature of geopolitical risks and their temporal impact on markets. Event-driven sell-offs tend to be short term, as shown by historical recovery patterns following the Israel-Hamas conflict and prior West Asia tensions. Investors adopting a longer-term view, supported by fundamental and technical analysis, can harness these corrections to build positions at favorable prices that yield above-average returns when market stability resumes. As such, market dips during geopolitical crises should be approached methodically, informed by sector-specific and macroeconomic considerations rather than driven purely by volatility-induced fear.

Theoretical Frameworks Linking Geopolitical Risk to Investment Decisions

Understanding the interplay between geopolitical risk and investment behavior benefits from established theoretical models that elucidate investor response mechanisms under uncertainty. One foundational concept is the geopolitical risk premium—a notion positing that investors demand higher expected returns to compensate for the increased uncertainty surrounding political conflicts, trade disruptions, or military standoffs. This premium manifests as elevated volatility and risk aversion reflected in higher costs of capital and depressed asset prices during crises.

Building on this, the conditional volatility models, such as GARCH (Generalized Autoregressive Conditional Heteroskedasticity), capture how geopolitical events temporally affect market fluctuations, allowing investors to adjust portfolio exposure dynamically. These quantitative tools, combined with qualitative geopolitical analysis, empower investors to anticipate volatility regimes and calibrate risk thresholds accordingly.

Another pertinent framework is the behavioral approach to investment under uncertainty, which integrates psychological biases such as herd behavior, loss aversion, and overreaction to news. These tendencies often exacerbate price swings during geopolitical events and create opportunities for informed investors to capitalize on market mispricing. Integrating sentiment indicators and contrarian signals within a broader strategic approach enhances decision-making robustness amid geopolitical upheavals.

Lastly, real options theory advocates viewing investment opportunities with embedded managerial flexibility—such as delaying, scaling, or abandoning investments—as options whose value increases in times of uncertainty. Applied to equity investing, this perspective encourages strategic patience and disciplined allocation, balancing the need to remain invested for long-term gains against the prudence of risk mitigation in turbulent environments.

Together, these theoretical constructs provide a comprehensive framework for navigating the complexities of geopolitical risk, guiding investors toward evidence-based decisions that optimize returns while guarding against adverse shocks.

Conclusion

The evidence presented underscores that escalating geopolitical tensions significantly amplify volatility and risk aversion in Indian equity markets, with pronounced effects stemming from energy price shocks and capital flow fluctuations. These dynamics pose considerable challenges to market stability but simultaneously offer discerning investors tactical opportunities through transient price dislocations.

To navigate the intricate landscape shaped by geopolitical uncertainties, investors and policymakers must emphasize robust risk mitigation techniques, including diversification and hedging, and maintain vigilance for value investing possibilities emerging during market downturns. Strategic application of theoretical frameworks linking geopolitical risk to investment behavior can enhance portfolio resilience.

Looking ahead, continued monitoring of geopolitical developments and their evolving market correlations is imperative. Further analysis could delve deeper into real-time risk modeling and predictive indicators to better equip stakeholders in managing the implications of an increasingly unstable global geopolitical environment on Indian equity markets.

Glossary

- Geopolitical Tensions: Conflicts and political disputes between countries or regions that create instability and uncertainty in international relations and can influence economic and financial markets.

- Equity Markets: Financial markets where shares of publicly held companies are issued and traded through exchanges, reflecting the ownership of companies.

- Brent Crude Oil: A major trading classification of crude oil sourced from the North Sea, serving as a global benchmark price for oil.

- India VIX: The India Volatility Index that measures the market's expectation of volatility over the near term, often referred to as the market's 'fear gauge.'

- Foreign Institutional Investors (FIIs): Entities such as investment funds, insurance companies, and pension funds from foreign countries that invest in the financial markets of another country.

- Non-Performing Assets (NPAs): Loans or advances in a bank or financial institution that are in default or in arrears on scheduled payments for a specified period.

- Line of Actual Control (LAC): The demarcation that separates Indian-controlled territory from Chinese-controlled territory in the border areas between the two countries.

- Hedging: Investment strategies or financial instruments used to reduce or offset the risk of adverse price movements in an asset.

- Diversification: A risk management technique that mixes a wide variety of investments within a portfolio to reduce exposure to any single asset or risk.

- Geopolitical Risk Premium: The additional expected return investors require to compensate for uncertainty and potential losses arising from geopolitical events.

- Real Options Theory: A framework in investment decision-making that views opportunities as flexible options, allowing investors to adapt their strategies in response to changing uncertainties.

- Conditional Volatility Models (e.g., GARCH): Statistical models used to estimate and forecast time-varying volatility in financial markets, accounting for clustering effects influenced by external factors such as geopolitical events.

- Oil Marketing Companies (OMCs): Firms responsible for the refining, distribution, and sale of petroleum products to consumers, often subject to margin pressures during crude price volatility.

- Upstream Oil Exploration and Production: The sector involved in the exploration and extraction of crude oil and natural gas, generally benefiting from rising crude prices.

- Foreign Exchange (Forex) Risk: The potential for financial loss due to fluctuations in currency exchange rates, which can affect import costs, corporate earnings, and investor returns.

References

- US-Israel-Iran Conflict: Impact on Indian Stock Market, Crude Oil Prices, Rupee, and Investors - Share India

- How Global Tensions Influence the Performance of the Indian Stock Market

- How Geopolitical events impacts the Indian Stock Market – Suri and Co

- Indian Equities Face Pressure as Geopolitics and Oil Surge | Market News & Analysis

- Indian Markets May Open Lower Amid Oil Surge, Global Tensions -

- Indian Stock Markets Fall by 2% Amid Geopolitical Tensions

- India Markets Plunge Amid West Asia Tensions, Presenting Value Buys

- Indian Markets Collapse Amid Geopolitical Tensions And Global Uncertainty

- Geopolitical Risks and Indian Stock Returns | PDF | Risk | Price Of Oil

- Crude Oil Jumps Six Percent Strait of Hormuz Tensions | StockeZee Market Pulse