The Strait of Hormuz Crisis: Unraveling Global Energy Security Risks and Economic Fallout in 2026

Table of Contents

Executive Summary

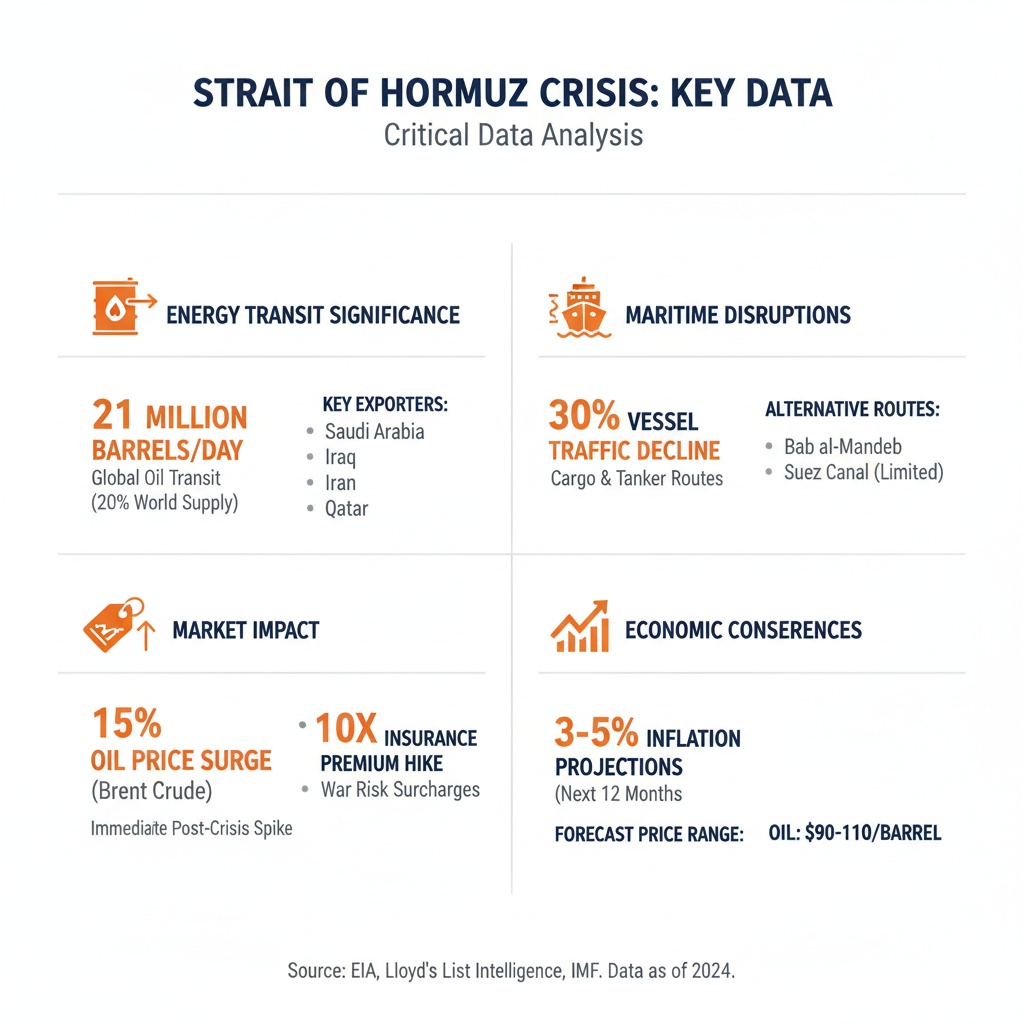

The Strait of Hormuz serves as a critical artery for global energy supplies, channeling approximately 20 million barrels of crude oil and refined products daily—accounting for 20 to 30 percent of globally seaborne oil trade and nearly one-fifth of total world oil consumption. Equally significant is its role in liquefied natural gas (LNG) transit, with around 20 percent of global LNG shipments passing through this narrow maritime corridor. Following escalating regional hostilities in early 2026, vessel traffic through the strait collapsed from an average of 130 daily transits to as few as five, precipitating a severe reduction in oil flow and inducing major supply shocks.

This disruption triggered immediate market reverberations: Brent crude prices surged above $110 per barrel, with West Texas Intermediate (WTI) at times exceeding $113, reflecting constrained physical supply and elevated war-risk premiums. War-risk insurance costs spiked over tenfold to as high as 3% of vessel value, adding several million dollars per voyage to shipping expenses. The compounded effects fueled a projected increase in headline inflation by up to 1.5 percentage points annually if the closure persists for multiple quarters, straining global economic stability. Despite efforts to augment alternative pipeline capacities, these remain incapable of fully compensating for the strait’s throughput, highlighting the imperative for coordinated diplomatic, military, and market interventions to restore the strait’s operational integrity.

Introduction

The Strait of Hormuz represents a linchpin in the architecture of global energy security. Spanning a mere 21 nautical miles between the Persian Gulf and the Gulf of Oman, this strategic maritime chokepoint facilitates the passage of nearly one-fifth of the world’s oil consumption and a significant share of liquefied natural gas exports. Its importance transcends regional boundaries, underpinning the energy demands of major Asian economies and industrialized nations alike. Any disruption in Hormuz reverberates swiftly across global markets, manifesting in price volatility and broader economic uncertainty.

In early 2026, escalating geopolitical tensions culminated in Iran’s effective closure of the Strait of Hormuz, a move unprecedented in recent decades. This dramatic escalation followed coordinated military strikes and intensified proxy conflicts, resulting in the near cessation of commercial vessel transits through the corridor. The ensuing crisis has directly impacted global oil supply chains, insurance premiums, and fiscal conditions, underscoring the inherent vulnerabilities embedded in reliance on a narrowly constricted transit route.

Infographic Image: Global Energy Risks and Economic Impact of Strait of Hormuz Tensions

This report aims to provide a comprehensive diagnostic analysis of the 2026 Strait of Hormuz crisis, elucidating the scale of disruption, its direct and indirect economic impacts, and the multifactorial causes underpinning the current impasse. Particular focus is placed on quantifying market volatility, inflationary pressures, and the effectiveness of alternative transport routes and mitigation strategies. Furthermore, the report evaluates ongoing diplomatic efforts and emerging coordination mechanisms designed to alleviate tensions and safeguard this vital global energy artery.

By synthesizing empirical data, geopolitical developments, and sectoral feedback loops, the report endeavors to inform stakeholders—from policymakers to industry leaders—of the pressing challenges and critical actions necessary to navigate this turbulent period and bolster long-term energy security resilience.

1. The Strait of Hormuz: Global Energy Artery at Risk

Unrivaled Strategic Value of the Strait of Hormuz in Global Energy Supply

This subsection establishes the foundational understanding of the Strait of Hormuz’s unparalleled significance as a critical global energy corridor. By quantifying the volume of oil and liquefied natural gas (LNG) traversing this narrow passage and contrasting it with alternatives, it frames why disruptions here have outsized effects on global energy security and market stability. Historical episodes of interruption highlight the consequences and vulnerabilities underpinning the current geopolitical sensitivity surrounding the strait.

Quantifying Daily Oil Transit Volumes Through the Strait of Hormuz

The Strait of Hormuz channels an estimated daily average of approximately 20 million barrels of crude oil and refined petroleum products, representing roughly 20 to 30 percent of globally seaborne oil trade and about one-fifth of total global oil consumption. This scale underscores its role as the world's most consequential maritime oil chokepoint, with several major Middle Eastern producers relying heavily on this corridor for export flows.

Prominently, Saudi Arabia exports around 5.5 million barrels daily through the strait, followed by Iraq, Iran, the United Arab Emirates, Kuwait, and Qatar, collectively accounting for the majority of Persian Gulf oil reaching international markets. The consumption profile is heavily skewed toward Asia, with key economies such as China, India, Japan, and South Korea absorbing nearly 85 percent of these shipments, emphasizing the strait’s crucial role in powering industrial and transportation sectors across the region.

These figures—5.5 million barrels for Saudi Arabia, 4.5 million for Iraq, 1.5 million for Iran, 3.0 million for the UAE, 2.0 million for Kuwait, and 1.0 million barrels for Qatar—further illustrate the significant reliance on the Strait for global oil supplies, reinforcing the narrow passage's strategic importance as a maritime chokepoint [Chart: Daily Oil Transit Volumes Through the Strait of Hormuz].

LNG Shipments and Broader Energy Trade Dependence on Hormuz

Beyond crude oil, approximately 20 percent of global liquefied natural gas trade passes through the Strait of Hormuz, primarily from Qatar and the UAE, the world's dominant LNG exporters. Qatar exports nearly 9.3 billion cubic feet per day, with over 90 percent of its LNG shipments reliant on this corridor. These volumes are similarly destined mainly for Asian markets, which are increasingly dependent on Gulf LNG to meet growing energy demand and transition needs.

The strait also serves as a vital conduit for petrochemicals and select manufactured goods, reinforcing its integral position within global energy and raw material supply chains. The convergence of oil, gas, and derivative flows through a constricted maritime pathway magnifies the economic risk associated with any disruption.

Limitations of Alternative Transport Routes and Their Capacity Constraints

Despite the critical reliance on the Strait of Hormuz, alternative export routes exist but are markedly constrained in both capacity and flexibility. Saudi Arabia’s East-West pipeline, connecting Eastern oil fields to the Red Sea port of Yanbu, can bypass the strait but is limited by terminal throughput, available tanker capacity, and logistical complexity. Its maximum operational throughput falls short of compensating for full strait closure scenarios.

Similarly, the UAE operates the Habshan-Fujairah pipeline providing a direct outlet to the Arabian Sea, reducing exposure to Hormuz-specific risks. However, recent incidents including drone attacks have exposed vulnerabilities along these pipeline routes themselves, reflecting broader regional security challenges. Collectively, these alternatives cannot fully replace the volume or ease of access provided by the strait, enforcing the latter’s irreplaceable status in global energy transit.

Historical Disruptions: Duration and Economic Impact as a Lens on Vulnerability

Historically, the Strait of Hormuz has faced multiple disruptions, notably during the Iran-Iraq War in the 1980s, when the “Tanker War” resulted in attacks on over 500 vessels and substantial interruptions to oil shipments. These events contributed to sharp spikes in oil prices and underscored the geopolitical volatility of the passage.

More recent escalations have similarly demonstrated how relatively small-scale or temporary disruptions cascade into widespread economic reverberations through elevated oil prices and heightened market uncertainty. The strait’s narrow physical geography combined with high traffic density ensures that even short-term interruptions can exert outsized effects on global energy security and economic stability.

Having established the Strait of Hormuz’s critical status as the linchpin of global oil and LNG trade, the next subsection will detail the dramatic drop in vessel traffic and illustrate how these physical constraints translate immediately into market price volatility, setting the stage for understanding the deeper economic ramifications of the conflict-driven supply shocks.

Dramatic Shipping Collapse and Oil Market Volatility Amid Hormuz Crisis

This subsection empirically documents the sharp collapse in vessel traffic through the Strait of Hormuz induced by escalating geopolitical tensions and analyzes the immediate consequences on global oil price dynamics and maritime insurance costs. Understanding these metrics clarifies how supply chain disruptions and risk re-pricing translate directly into financial market volatility and heightened economic uncertainty.

Precipitous Decline in Vessel Traffic: Quantifying the Disruption

Before the onset of conflict, daily vessel transits through the Strait of Hormuz averaged approximately 130, serving as the conduit for around 20 million barrels of oil daily, representing nearly one-fifth of global petroleum consumption. Following joint military actions and subsequent retaliations in late February 2026, traffic volumes plummeted drastically, with recorded daily transits falling to as few as five vessels at the crisis's peak. Even after a fragile ceasefire, throughput remained significantly suppressed, hovering around 10 ships daily—the equivalent of less than 10% of pre-conflict levels. This near standstill has forced the rerouting of hundreds of vessels, drastically elevating shipping time and costs as operators divert fleets via longer routes like the Cape of Good Hope to circumvent the conflict zone.

Selective passage policies enforced by Iranian authorities have further constrained maritime flow, only allowing a limited number of non-hostile or politically aligned vessels, often at informal fees, while tankers from sanctioned regimes face strict restrictions. This limited reopening has failed to restore meaningful transit volume, perpetuating global supply chain challenges and underscoring the strait's lack of substitutability in the short term.

Correlation Between Shipping Collapse and Oil Price Surges

The dramatic contraction in shipping through this critical chokepoint directly triggered a sharp supply deficit in global oil markets. Spot prices for benchmark grades responded immediately: Brent crude surged above $110 per barrel in early April, while West Texas Intermediate (WTI) similarly pushed past $113. These increases reflect not only realized supply constraints but also a significant war-risk premium incorporated by market participants, with price volatility amplified amid fears of prolonged disruption or wider regional escalation.

Additionally, the peculiar inversion where WTI prices occasionally exceeded Brent highlights market repricing of accessible versus physically constrained barrels. Whereas Brent prices traditionally lead owing to their seaborne delivery dependency, WTI’s premium during the crisis indicates that inland U.S. crude, unaffected by Strait disruptions, acquired higher valuation as it remained physically deliverable.

Price rallies were closely correlated with real-time declines in transit volumes—weeks marked by fewer than ten daily transits coincided with spikes of 6-9% or more within days. Attempts by producer states to offset these losses through increased pipeline throughput have proven insufficient to stabilize supply or cap prices, further reinforcing price sensitivity to Strait traffic data.

Marine Insurance Premium Hikes and Economic Amplification of Risk

The conflict has dramatically increased the cost and complexity of insuring vessels traversing the Strait. Historic war-risk insurance premiums, previously in the range of 0.2–0.3% of vessel value, have soared by more than tenfold, reaching up to 3% of vessel value in some cases. For VLCC tankers valued between $200 million and $300 million, this translates to an increase from several hundred thousand to millions of dollars per voyage in insurance costs alone.

Major underwriters, especially those in traditional insurance hubs, have either restricted or entirely withdrawn coverage for vessels operating within the high-risk zone, compelling shipowners either to seek prohibitively expensive alternative coverage or suspend operations altogether. This insurance cost shock acts as a force multiplier to the physical shipping constraints, further discouraging risky passage through the waters and contributing to supply tightness.

The escalation in maritime insurance premiums feeds through to freight rates and ultimately consumer fuel prices, compounding inflationary pressures across interconnected sectors, highlighting the multi-layered impact beyond simple physical supply disruption.

The documented collapse in maritime traffic and the consequential surge in oil prices, alongside sharply elevated insurance premiums, demonstrate the interconnectedness of physical supply constraints and market risk perceptions. This complex dynamic warrants further causal analysis into geopolitical escalation drivers and systemic feedback loops governing price behavior and economic vulnerabilities.

2. Diagnostic Analysis: Causes Driving the Oil Price Surge

Geopolitical Escalation Drivers: Unfolding Regional Contest and Strategic Posturing around Hormuz

This subsection dissects the pivotal geopolitical dynamics fueling the surge in oil prices by detailing the key actors’ strategies, military developments, and alliances shaping the evolving crisis in the Strait of Hormuz. By clarifying the timeline and nature of Iran's closure declaration, U.S. and Israeli military deployments, and the regional power alignments influencing escalation, it provides a robust foundation for understanding the underlying triggers intensifying market uncertainty and supply risks.

Iran’s 2026 Strait Closure: Timeline, Intentions, and Operational Control

In early March 2026, Iran’s Islamic Revolutionary Guard Corps announced a dramatic escalation by effectively closing the Strait of Hormuz to commercial shipping. This marked the most explicit maritime blockade since the conflict’s intensification, following coordinated airstrikes on Iranian territories by U.S. and Israeli forces in late February. Iran’s announcement on March 2 formalized the waterway closure, with threats of attack on vessels attempting passage, signaling a strategic leverage move to counter external military pressure and assert regional dominance.

Operationally, Iran enforced this closure through a combination of missile and drone strikes targeting merchant vessels, deployment of naval mines, and augmented presence of fast-attack boats patrolling the narrow 21-nautical-mile strait. Despite international legal ambiguity, Iran’s assertion has severely disrupted normal shipping flows, with insurance firms withdrawing coverage and commercial operators canceling transits. However, the blockade has not been uniformly applied; vessels from countries deemed friendly, such as India, Pakistan, and China, have reportedly been allowed passage, demonstrating Iran’s calibrated approach to maintain selective control while pressuring adversaries.

This near-total disruption has persisted through April 2026, fluctuating with diplomatic developments and intermittent ceasefire announcements. The political calculus behind Iran’s action reflects a desire to use the strait as a bargaining chip, leveraging its geographic chokepoint capability to signal resolve and inflict maximum economic cost on opposing coalitions.

U.S.-Israel Military Posture: Escalation, Force Projection, and Strategic Objectives

Countering Iran’s moves, the United States and Israel have significantly escalated their military posture around the Strait of Hormuz. The U.S. Navy surged deployment with at least 15 warships, including guided missile destroyers and amphibious assault ships carrying over 2,500 Marines, establishing a robust blockade and implementing mine-clearing operations to reopen safe passage. This buildup includes sea drone usage for mine detection and simultaneous readiness for potential naval and air strikes against Iranian maritime assets.

Israel’s military actions have complemented this posture by conducting sustained strikes on Hezbollah and other Iranian proxy targets in Lebanon and the broader region, targeting missile launch platforms and command centers. Intelligence cooperation between the U.S and Israel reportedly supports efforts to control the strait and degrade Iran’s ability to impose lasting closure, with preparations for a potential multi-week campaign intended to neutralize threats to navigation.

The combination of direct military action, naval presence, and diplomatic signaling underscores the coalition’s objective to prevent Iran from exploiting the chokepoint to destabilize global energy markets while maintaining plausible deniability regarding full-scale invasion plans. Washington’s deployment of additional Army paratroopers and Marines signals intent to sustain pressure and deter Iranian escalation despite vocal warnings from Tehran against interference.

Mapping Regional Power Alignments: Conflicting Axes and Their Role in Sustaining Tensions

The intensifying crisis at the Strait of Hormuz is deeply entrenched in a complex web of regional alliances and rivalries that collectively underpin the broader geopolitical standoff. Iran leads a cohesive ‘Axis of Resistance’ comprising allied state and non-state actors across Lebanon, Syria, Iraq, and Yemen, unified by shared strategic interests to counter U.S. and Israeli influence. This axis receives diplomatic and limited military support from Russia and China, adding an international dimension to the confrontation.

Opposing this coalition is a U.S.-backed bloc anchored by Saudi Arabia, the United Arab Emirates, and Israel, whose security cooperation and arms procurements reflect a shared goal of containing Iran’s regional ambitions. The Gulf powers, particularly the UAE and Saudi Arabia, have demonstrated strong backing for intensifying military pressure on Iran, advocating for measures ranging from enhanced naval operations to ground interventions to ensure the strait remains open.

Meanwhile, intermediary regional actors such as Oman and Qatar are pursuing diplomatic overtures, reflective of their historical roles as intermediaries despite the heightened hostilities. Turkey and Qatar’s alignment remains somewhat ambivalent, balancing economic ties with multiple sides while exerting regional influence independently. These overlapping power alignments, built on sectarian, ideological, and geopolitical foundations, perpetuate an environment prone to rapid escalation and complicate the prospects for swift conflict resolution.

Having established the geopolitical environment and militarized actions driving heightened risks amid the Hormuz crisis, the analysis will progress next to how these escalation dynamics feed into market sentiment and create self-reinforcing price and risk feedback loops that amplify economic vulnerabilities.

Market Feedback Loops: Insurance Spirals, Investor Flight, and Algorithmic Amplification

This subsection delves into the self-reinforcing mechanisms by which escalating geopolitical tensions around the Strait of Hormuz have intensified oil price volatility. By dissecting the surge in war-risk insurance premiums, shifts in investor asset allocations, and the growing influence of algorithmic trading, this analysis reveals how market dynamics propagate and magnify initial supply shocks into broader economic turbulence.

Quantifying the Surge in War-Risk Insurance Premiums Amid Hormuz Tensions

The military escalation involving the Strait of Hormuz has triggered an unprecedented spike in war-risk insurance premiums for vessels operating in the region. Prior to the intensification of the conflict, such premiums typically ranged from 0.2% to 0.3% of vessel value, reflecting relatively stable maritime security conditions. Since hostilities escalated, premiums have soared dramatically, in some cases exceeding 3% of the insured vessel value—amounting to a more than tenfold increase from baseline levels. For very large crude carriers valued around $200–300 million, this elevated premium translates into insurance costs nearing $7.5 million per voyage compared to hundreds of thousands previously, substantially inflating the cost of maritime oil transport. In certain cases, premiums have stretched as high as 7.5% of vessel value during acute conflict phases, effectively pricing risk at tens of millions of dollars per transit and rendering insurers either unwilling or financially incapable of providing coverage on conventional terms. This forced many shipowners to either seek prohibitively expensive alternative underwriting or suspend operations through the strait altogether, sharply reducing tanker transit volumes and pressuring physical oil supply chains.

Additional evidence from premium adjustments across major insurance markets underscores this trend. In Korea, for example, ship insurance contracts renewed during peak conflict periods reflected premium increases ranging from 200% to over 1,000%, with some companies reporting hikes of more than tenfold on war-risk riders. Globally, insurers like Lloyd’s and brokers in London have tightened underwriting rules, restricting coverage for vessels linked to U.S. or allied interests. Although some insurers have partially restored cover following brief ceasefire announcements, stability and verifiability remain prerequisites for premium reductions. The fluctuating insurance landscape thus represents a real-time barometer of conflict dynamics, amplifying uncertainty in maritime oil logistics and feeding directly into cost structures that underpin global commodity pricing.

Investor Behavior: Flight to Safe Havens and Its Role in Price Spikes

As geopolitical risks surrounding the Strait of Hormuz intensified, investor sentiment rapidly shifted towards risk aversion, precipitating marked reallocation of capital into traditional safe-haven assets. Treasury bonds of developed countries, gold, and certain fiat currencies perceived as low-risk garnered increased inflows, while exposure to oil-linked and regional equities diminished sharply. This broad movement dampened liquidity in riskier segments and concentrated capital in defensive instruments, indirectly reinforcing upward pressure on oil prices through anticipatory demand and speculative positioning.

The elevated uncertainty about the conflict’s duration and potential escalation heightened fears of sustained supply disruption. As a result, oil market participants—including institutional investors and commodity funds—expanded their purchasing of physical and paper barrels as a hedge against growing geopolitical premium risk. Price volatility itself attracted further speculative interest, generating a feedback loop where rising prices encouraged additional risk premiums and speculative buying, independent of immediate physical supply constraints. Currency markets mirrored this trend, with the U.S. dollar initially strengthening on safe-haven inflows, although broader structural economic concerns and weaker risk appetite limited sustained appreciation. Overall, the capital flight to secure assets contributed to amplifying the oil price spike beyond what direct supply-demand fundamentals would suggest, heightening the systemic risk embedded in financial markets connected to energy.

This dynamic is illustrated by the sharp rise in Brent crude prices from $70 per barrel pre-conflict to a peak of $110 per barrel during the height of the strait’s closure, coinciding with a pronounced decline in vessel traffic. As transit diminished due to geopolitical disruptions, market sensitivity amplified price spikes that exacerbated speculative and risk-premium-driven demand [Chart: Oil Price Changes Correlating with Vessel Traffic in the Strait of Hormuz].

Algorithmic Trading’s Role in Amplifying Market Volatility During the Crisis

High-frequency and algorithmic trading have played a pivotal role in magnifying oil price volatility amid the Strait of Hormuz tensions. Empirical data show a near eightfold surge in trading volumes on key energy futures contracts concurrent with peak crisis moments, driven largely by automated trading algorithms reacting to rapidly changing geopolitical information and price signals. These algorithms tend to respond instantaneously to risk-related news, heightening short-term price swings and reducing market depth when other liquidity providers withdraw due to uncertainty.

Algorithmic traders exhibit greater elasticity in market participation, providing liquidity during stable periods but withdrawing it sharply in volatile or crisis conditions. This behavior can exacerbate price dislocations as algorithmic systems cascade in reaction to common risk signals or stop-loss triggers. Regulatory reports indicate that the rise of automated trading strategies has increased the market’s sensitivity to geopolitical shocks, often amplifying the magnitude and speed of price adjustments beyond fundamental supply disruptions. Moreover, the increasing prevalence of algorithm-driven trading creates a feedback loop whereby geopolitical risk perceptions, as embedded in price movements, are rapidly priced and re-priced, generating episodic bursts of heightened volatility that challenge traditional risk management approaches in the oil market.

Building upon the understanding of how insurance costs, investor behavior, and automated trading amplify oil price volatility, the next subsection will synthesize these causal mechanisms within the broader systemic risk framework. This will elucidate how intricately interconnected global supply chains and financial markets translate localized geopolitical disruptions into pervasive economic vulnerabilities.

Systemic Vulnerabilities Unveiled: Inflation Surges, Sectoral Strains, and Monetary Responses Amid Hormuz Disruptions

This subsection delves into the broad economic repercussions triggered by escalating geopolitical tensions around the Strait of Hormuz. By quantifying inflationary pressures, mapping the differential impact on key economic sectors, and examining central banks' monetary policy adjustments, it illuminates the fragile interdependencies that amplify global economic risks beyond the immediate oil price shock. This analysis supports strategic understanding of how energy supply shocks propagate through complex economic systems, thereby informing policy and corporate risk management decisions.

Quantifying Inflationary Pressures from Hormuz Supply Disruptions

The disruption of oil flows through the Strait of Hormuz has exerted upward pressure on global inflation, with models projecting a substantive rise in headline inflation indices proportional to the duration of the strait’s closure. A closure extending to three consecutive quarters could elevate headline inflation measures by nearly 1.5 percentage points year-over-year, with core inflation also registering notable increases. These inflationary effects manifest prominently in consumer energy prices but gradually permeate broader price levels through second-round effects in wage-setting and production costs.

Emerging market economies are especially susceptible, with estimated inflation increments of up to one percentage point over a two-month disruption period, underscoring heightened vulnerability due to higher energy import dependencies and limited monetary policy space. Advanced economies similarly face inflation risks; however, the transmission mechanics and policy buffers present nuanced differences. Inflation expectations remain somewhat anchored in the medium term, evidencing a market belief in transitory price shocks conditional on resolution of supply constraints.

Sectoral Impact Profile: Identifying Economic Pressure Points

The surge in oil prices stemming from Strait of Hormuz tensions disproportionately impacts energy-reliant sectors, with aviation, transportation, and oil marketing companies among the hardest hit due to escalating fuel costs. The transport sector, encompassing air, road, and maritime modalities, experiences amplified operational expenses that ripple through supply chains, inflating costs for consumer goods beyond direct energy markets.

Industries such as chemicals, petrochemicals, ceramics, and construction also demonstrate heightened cost pressures, which may lead to margin compression and subdued growth prospects, particularly where pricing power is limited. Conversely, upstream oil and gas producers profit from elevated price realizations, benefiting from improved revenue streams amidst supply constraints. Additionally, accelerated interest in renewable energy and defense sectors reflects shifting demand patterns amid geopolitical uncertainty and energy transition imperatives.

In major emerging economies like India, the inflationary impact of high crude prices compounds existing macroeconomic vulnerabilities, driving up input costs and necessitating interest rate adjustments. Consumer-facing industries including paints, tyres, and synthetic textiles face moderate to high impact levels depending on energy intensity and exposure to global commodity price volatility.

Central Banks’ Monetary Policy Responses Amid Supply-Driven Inflation Shocks

Central banks confronting inflationary pressures from energy supply shocks face a constricted policy environment where traditional interest rate adjustments offer limited efficacy in addressing core supply disruptions. Many monetary authorities have implemented calibrated rate hikes to anchor inflation expectations while cautiously balancing potential growth slowdowns. This is particularly evident in emerging market central banks that adopted early and vigorous tightening to preserve currency stability and mitigate risk spreads.

Advanced economies have demonstrated a more measured tightening trajectory, influenced by initial accommodative stances during earlier pandemic phases and concerns regarding the persistence of inflation. Communication strategies emphasizing inflation targeting and forward guidance play a critical role in shaping market expectations and reducing volatility.

Supply-led inflation poses unique challenges, with central banks unable to directly augment physical oil supplies. Consequently, fiscal policies and strategic reserves coordination augment monetary actions. The combined macroprudential approach aims to temper inflationary spirals that could destabilize wage-price dynamics. Nonetheless, prolonged energy price shocks risk entrenching inflationary expectations, prompting preemptive monetary policy recalibrations across major economies.

Having established the multifaceted economic vulnerabilities exacerbated by the Strait of Hormuz tensions, the analysis is poised to transition into exploring pragmatic mitigation avenues. The next section will evaluate infrastructure resilience, diplomatic initiatives, and corporate risk management strategies aimed at alleviating these systemic fragilities and stabilizing global energy flows.

3. Mitigation Options and Strategic Imperatives

Bolstering Energy Supply Lines: Pipeline Capacities, Maritime Alternatives, and Cybersecurity Imperatives Amid Hormuz Disruptions

This subsection focuses on evaluating and enhancing physical and cyber infrastructure resilience to mitigate risks posed by geopolitical tensions in the Strait of Hormuz. By quantifying the capacities and vulnerabilities of existing pipeline alternatives, assessing the feasibility and costs of maritime route expansions, and scrutinizing cybersecurity investments necessary to safeguard energy transit systems, this analysis provides critical insights to inform strategic infrastructure hardening and risk management decisions under current crisis conditions.

Assessing the Capacity and Operational Constraints of East-West Pipeline Alternatives

The Saudi Arabian East-West pipeline stands as the foremost physical alternative to Hormuz transit, capable of redirecting a substantial volume of crude oil from producing fields in the Persian Gulf to the Red Sea port of Yanbu. Its theoretical maximum throughput reaches several millions of barrels per day, representing a critical relief valve when maritime traffic through the Strait is compromised. However, operational limitations significantly moderate this potential. The pipeline’s effective capacity is contingent upon downstream logistics capabilities including the availability of suitable tankers and port terminal throughput at Yanbu, which can become bottlenecks under sudden surge demands. As such, while the East-West pipeline can materially alleviate supply interruptions, it cannot fully compensate for a total Hormuz closure without coordinated logistical ramp-ups in shipping and terminal operations. These constraints were underscored in recent weeks as tanker availability and port congestion limited effective export volumes despite heightened redirection efforts.

Evaluating Alternative Pipelines and the Vulnerabilities of Land-Based Energy Transport

In addition to the East-West pipeline, the United Arab Emirates’ Habshan-Fujairah pipeline offers a direct ocean outlet bypassing the Strait via the Gulf of Oman, diversifying export routes and reducing reliance on maritime chokepoints. Yet, the security environment in the region directly impacts the operability and resilience of these alternatives; recent drone strikes and targeted attacks have vividly demonstrated their susceptibility to kinetic disruptions. Unlike naval passages, land-based infrastructure inherits unique vulnerabilities including fixed geographic exposure and relative immobility, complicating rapid repairs and protective measures. This fragility limits reliable throughput expansion during heightened conflict risk and necessitates bolstered defensive postures and contingency planning. Consequently, while these pipelines underpin short-term resilience, their strategic value remains circumscribed by security uncertainties that continue to inflate risk premiums and operational costs.

Feasibility and Costs of Expanding Maritime Alternative Routes Under Strained Conditions

Confronted with potential or actual closures of the Strait of Hormuz, global energy markets have contemplated extending reliance on longer maritime rerouting options such as navigating around Africa’s Cape of Good Hope or utilizing the emerging Northern Sea Route via the Arctic. These alternatives allow crude shipments to reach Asian and European markets without transiting the Gulf but introduce significant drawbacks. The Cape of Good Hope passage increases voyage distances by several thousand nautical miles, thereby escalating fuel consumption, crew costs, and exposure to volatile sea conditions. The Northern Sea Route, although seasonally viable due to warming trends, remains constrained by ice conditions, limited infrastructure, and geopolitical uncertainties involving Arctic governance. Scaling these routes implies substantial additional capital and operational expenditures, along with longer cargo transit times that reduce supply chain responsiveness. Current cost-benefit assessments suggest these routes serve as emergency contingencies rather than systemic replacements, emphasizing the premium on maintaining the Hormuz corridor's openness.

Additionally, maritime transport costs have risen sharply amid the crisis, driven largely by surging war-risk insurance premiums. These premiums have escalated from 0.25% to 3.0% of vessel value following conflict escalation, significantly inflating shipping expenses and complicating cost calculations for extended routes. Such an increase underscores the financial pressure on maritime alternatives and reinforces the emphasis on keeping the Strait of Hormuz operational whenever possible [Chart: Surge in War-Risk Insurance Premiums Amid Hormuz Tensions].

Current Cybersecurity Investment Trends Focused on Energy Transit Infrastructure Protection

Amid the intensifying geopolitical risks surrounding oil transit corridors, cybersecurity of physical and digital energy infrastructure has assumed heightened strategic priority. The Department of Defense and related U.S. federal agencies have significantly expanded budget allocations for cyber defense initiatives aimed at critical infrastructure protection in FY 2026, evidencing the rising urgency to counter cyber threats that could further disrupt oil and gas supply chains. Investment growth has targeted advanced cryptographic modernization, identity and access management, and the implementation of cybersecurity maturity certification programs designed to harden the defense industrial base. Concurrently, programs focusing on operational technology security and supply chain cyber risk management have received increased resourcing to address vulnerabilities specific to pipeline controls and terminal automation systems. However, these efforts face budgetary headwinds within civilian agencies and cybersecurity institutions, underscoring a need for sustained and integrated funding approaches. Strengthening digital defenses is imperative to prevent adversarial exploitation of energy transit system vulnerabilities in a context marked by kinetic threats and hybrid warfare.

Balancing Cybersecurity Funding Challenges with Critical Infrastructure Needs in 2026-2027

Despite the recognition of cybersecurity as a foundational element of energy supply resilience, recent budget proposals for key civilian agencies involved in infrastructure protection highlight a potential decline in available resources starting fiscal year 2027. Agencies like the Cybersecurity and Infrastructure Security Agency (CISA) face significant funding cuts and workforce reductions even as threat environments remain elevated. This contraction poses risks to the continuity and effectiveness of cyber risk identification, mitigation, and coordination activities vital to safeguarding pipelines, ports, and maritime logistics nodes linked to the Strait of Hormuz supply axis. The emerging funding gap necessitates strategic prioritization and increased efficiency in cyber defense operations to sustain momentum. Private sector collaboration and public-private partnership models will likely become more critical in compensating for federal budgetary constraints during this volatile period.

Understanding the physical and cyber dimensions of infrastructure resilience sets the stage for exploring how diplomatic initiatives and institutional responses can complement technological and operational defenses to secure the Strait of Hormuz corridor in the face of ongoing geopolitical volatility.

Navigating Diplomatic Currents: Multilateral Mediation, Legal Frameworks, and Emerging Coordination in Hormuz Crisis

This subsection critically examines the diplomatic and institutional responses shaping the evolving crisis in the Strait of Hormuz. By systematically mapping active multilateral mediation actors, analyzing the effectiveness of existing legal frameworks, and exploring innovative coordination proposals emerging in early 2026, this segment positions the diplomatic dimension as a pivotal avenue for risk mitigation amidst escalating tensions. It builds upon the previous diagnostic analysis by focusing on governance mechanisms that may stabilize maritime navigation and energy markets, offering insight essential for policymakers and industry leaders seeking sustainable resolutions.

Key Multilateral Mediation Actors Steering Conflict De-escalation in the Strait

Several multilateral actors have assumed central roles in efforts to mediate and contain tensions in the Strait of Hormuz. Pakistan has emerged as a primary intermediary, facilitating indirect dialogue between the United States and Iran, leveraging its geopolitical positioning to maintain communication channels despite strained bilateral relations. This mediation track involves coordination with regional stakeholders including Egypt, Turkey, and Saudi Arabia, forming a quadrilateral framework aimed at brokered ceasefires and preventing conflict escalation across the Gulf region.

Oman plays a distinctive role as a regional mediator, actively engaging both Iran and external powers through shuttle diplomacy. Omani officials have been pivotal in coordinating dialogues regarding maritime navigation safety and exploring mechanisms for partial reopening of the strait under internationally accepted norms. Moreover, China has become increasingly involved through a diplomatic initiative proposing a five-point peace plan with Pakistan, seeking to facilitate stability through both direct negotiations and broader multilateral engagement.

European Union representatives, notably the High Representative for Foreign Affairs, have vocally supported de-escalation efforts, emphasizing the importance of reinstating safe navigation through the strait for global economic stability. The EU’s diplomatic posture favors adherence to United Nations frameworks and international law, working alongside China and other stakeholders to maintain communication and humanitarian support.

Additional actors include the United Kingdom, which has convened virtual discussions focused on maritime security, and Bahrain, which has promoted resolutions within the United Nations Security Council to uphold freedom of navigation. Collectively, this constellation of actors reflects a multi-layered diplomatic environment, balancing regional interests with broader international concerns over energy security and rules-based maritime order.

Measuring Effectiveness: Success and Shortcomings of Existing Diplomatic and Legal Mechanisms

Despite sustained diplomatic activity, existing legal and institutional frameworks have exhibited limited success in resolving the crisis or fully reopening the Strait of Hormuz to commercial traffic. Historically, international law mandates freedom of navigation through strategic chokepoints, yet enforcement mechanisms lack the robustness to deter unilateral coercive actions or military escalations effectively. The current conflict represents a stark reminder of these limitations, as Iran’s effective closure of the strait has triggered sharp surges in global oil prices and widespread market disruption.

Past initiatives, including UN Security Council resolutions advocating safe passage, have struggled to produce concrete operational outcomes due to geopolitical polarization. The US, Israel, and Iran remain entrenched in maximalist positions, with Tehran linking strait access to comprehensive sanctions relief and regional security guarantees, while Washington insists on nuclear and military constraints. This impasse undermines confidence in purely legalistic approaches to conflict management, exposing a gap between normative frameworks and realpolitik enforcement.

Success rates of economic sanctions and diplomatic pressure, as observed in analogous cases, typically fall below one-third, particularly when core existential demands are involved. This low efficacy underscores the necessity for integrated approaches combining legal mandates with pragmatic diplomacy and confidence-building measures. Moreover, the persistence of skirmishes involving proxy actors and decentralized Iranian forces complicates the operationalization of legal protections, as enforcement requires multilayered military and political coordination.

Nevertheless, legal frameworks continue to provide essential reference points underpinning mediation efforts and international expectations. They establish the boundaries within which negotiated arrangements and ceasefire agreements may be crafted, lending legitimacy and continuity to evolving diplomatic initiatives despite their current limitations in crisis resolution.

Emerging Proposals: Innovations in Coordination and Governance for Strait Security

In response to the evident strains on traditional diplomacy and law, early 2026 has witnessed the surfacing of novel coordination mechanisms designed to enhance governance and stability in the Hormuz corridor. Multilateral initiatives are coalescing around increased transparency, regular communication protocols among naval forces, and joint monitoring mechanisms involving regional and international stakeholders.

Pakistan’s mediation framework has evolved to emphasize a quadrilateral dialogue model, integrating Egypt, Turkey, and Saudi Arabia, which seeks to bridge divergent security perceptions through incremental confidence-building and constructive engagement. Parallel to this, China’s five-point plan represents a strategic effort to reset the negotiation dynamics by coupling ceasefire calls with pragmatic steps toward economic reconstruction and maritime safety.

Furthermore, there have been proposals advocating enhanced institutional coordination platforms that blend diplomatic, military, and commercial actors to ensure rapid incident response and dispute resolution. These include calls for a dedicated Hormuz Strait Security Council—conceptually similar to maritime security forums in other chokepoints—that would institutionalize communication and preemptively manage tensions.

The international community is also exploring legal reforms aimed at strengthening enforcement of navigation freedoms under UN conventions. These reforms aim to modernize existing treaties to accommodate the complex realities of hybrid warfare, proxy engagements, and asymmetric threats characteristic of the current environment.

While these initiatives are nascent and face significant political hurdles, they collectively represent an adaptive shift toward multi-dimensional governance. They underscore a growing recognition that ensuring the Strait of Hormuz’s accessibility necessitates innovative diplomatic architectures beyond conventional bilateral or regional agreements.

Building on this analysis of diplomatic and institutional factors, the report now proceeds to evaluate practical mitigation options, focusing on infrastructure resilience and risk management strategies that complement and reinforce evolving governance efforts.

Corporate Risk Management: Hedging, Inventory, and Supply Chain Visibility Amid Hormuz Disruptions

This subsection delivers actionable strategies for corporate entities to mitigate escalating risks linked to Strait of Hormuz tensions. Positioned within the broader mitigation framework, it focuses on pragmatic tools—hedging, inventory optimization, and supply chain mapping—that enable firms to adapt swiftly to heightened volatility, cost inflation, and operational uncertainties. Drawing on recent market dynamics and empirical case evidence, it equips decision-makers with robust instruments to safeguard supply continuity and financial stability.

Advanced Hedging Strategies to Navigate Energy and Insurance Volatility

In response to intense price volatility triggered by geopolitical tensions around the Strait of Hormuz, corporate hedging strategies have become more sophisticated and multifaceted. Firms are increasingly leveraging a combination of futures, options, and swaps to stabilize cash flows subject to soaring oil price fluctuations and insurance premium increases. This layered approach mitigates exposure not only to commodity price swings but also to ancillary cost escalations such as war-risk insurance premiums that have surged by 25-50% amid the current crisis. Companies are incorporating scenario-based stress tests into hedging program designs to capture a broader range of geopolitical shock scenarios, ensuring portfolio resilience across abrupt market shifts.

Moreover, because traditional hedging alone may not fully capture risk related to supply disruption or policy changes, firms are coupling financial instruments with contractual risk-sharing provisions in supply agreements. This includes flexible take-or-pay schemes or indexed insurance premium pass-through clauses that can help absorb spikes in shipping and insurance costs. By adopting a dynamic framework for hedging that responds in near real-time to geopolitical signals, corporations can reduce earnings volatility and secure more predictable cost structures during protracted uncertainty.

Optimizing Inventory Levels for Crisis Resilience Without Excess Carrying Risks

Inventory management under heightened geopolitical risk demands a calculated balance between buffer stock increases and cost efficiency. In the wake of Strait of Hormuz disruptions, firms are revisiting optimal inventory models that favor slightly elevated safety stock levels calibrated to likely supply chain delays but avoid excessive capital lock-up. Data-driven inventory optimization systems now integrate real-time demand forecasting and supply variability analytics to adjust reorder points dynamically, minimizing both stockouts and overstock costs under volatile market conditions.

Best practices emerging from recent cases emphasize the integration of lean inventory principles with strategic reserve buffers specifically for critical raw materials and energy-intensive inputs. Firms employing automated inventory management software within an enterprise resource planning ecosystem achieve superior visibility and control, enabling prompt adjustments to procurement cycles and reorder quantities based on continuously updated risk assessments. Such calibrated inventory optimization strengthens operational continuity while containing heightened carrying and insurance costs, which have become particularly burdensome in the current environment.

Enhanced Supply Chain Mapping and Visibility as a Risk Anticipation Tool

In the face of acute disruptions in the Strait of Hormuz corridor, comprehensive supply chain mapping has emerged as a critical corporate risk management practice. Companies are rigorously analyzing the entire supply network to identify choke points, dependencies, and alternative routes beyond the immediate petroleum transit pathways. This granular visibility enables more informed decisions regarding supplier diversification, multi-modal transport alternatives, and contingency inventory positioning.

Practical implementations involve digital platforms equipped with real-time tracking and predictive analytics, which can simulate disruption scenarios and quantify potential lead-time impacts. Such insights facilitate proactive engagement with suppliers and logistics partners to develop joint risk mitigation protocols, enhance coordination, and ensure faster response times. Case studies demonstrate that firms with mature supply chain transparency are better positioned to negotiate contract adjustments, manage customer expectations, and maintain service levels despite escalating regional tensions and associated cost pressures.

Building on these risk management frameworks, the next section will explore scenario projections to anticipate how the evolving geopolitical landscape may shape near-term market trajectories and longer-term structural realignments, thereby informing adaptive strategies across governance and investment domains.

4. Scenario Projections and Contingency Planning

Navigating Turbulent Waters: Short-Term Price Volatility, Inflationary Pressure, and Currency Risks Amid Hormuz Disruptions

This subsection provides a focused, data-driven forecast of the immediate economic and financial impacts arising from ongoing tensions in the Strait of Hormuz. Positioned within scenario projections and contingency planning, it bridges the understanding of near-term price dynamics and inflationary outcomes with the critical challenge of currency volatility. It enables stakeholders to anticipate how acute disruptions could cascade through inflation metrics, oil price fluctuations, and exchange rate movements during the first half of 2026 under varying escalation scenarios.

Projected Inflationary Effects of Potential Strait of Hormuz Closure on 2026 Q1-Q2 Economic Stability

Recent scenario-based modeling anticipates that a temporary closure of the Strait of Hormuz would exert a substantial upward influence on both headline and core inflation throughout the first two quarters of 2026. Empirical estimates indicate that a full quarter closure could elevate headline inflation rates by approximately 1.3 percentage points annually compared to a baseline of no disruption. If the closure persists through two or three quarters, this inflationary impulse intensifies, potentially increasing headline inflation by up to 1.5 percentage points year-over-year by year-end.

More specifically, core inflation—which excludes volatile food and energy prices—would exhibit a delayed but meaningful rise, ranging from a moderate increase of 0.18 percentage points after one quarter of disruption to nearly 0.5 percentage points if the disruption extends to three quarters. While headline inflation tends to respond swiftly to oil price shocks transmitted through energy and transportation costs, the stickiness in core inflation reflects second-round effects feeding through wages, rents, and broader service-sector pricing. These inflation dynamics underscore the significant economic strain anticipated if supply chokepoints remain impaired in the near term.

These estimates are supported by recent quantitative projections that outline headline inflation increases ranging from 1.3% for a one-quarter closure to 1.5% for a three-quarter closure, clearly demonstrating the inflationary pressure escalation corresponding with prolonged disruption durations [Table: Impact of Strait of Hormuz Disruptions on Inflation Projections].

Forecasts of Near-Term Oil Price Volatility and Scenario-Dependent Price Trajectories in 2026

Oil price forecasts for 2026 increasingly reflect a high-volatility environment driven by geopolitical risk premiums associated with the Strait of Hormuz. Major analytical consensus suggests that Brent crude oil may trade between $90 and $110 per barrel in the near term, with occasional spikes towards or beyond $120 per barrel if tensions escalate. Notably, prices surged precipitously in early 2026, reaching near $110 per barrel during peak escalation moments, highlighting market sensitivity to perceived supply interruptions rather than actual measured shortfalls.

Institutional prognoses emphasize a front-loaded risk profile characterized by a sharp but potentially temporary spike in oil prices, typically moderating as partial restoration of maritime flows or strategic reserve releases occur. For example, under a scenario of constrained energy flows persisting into Q2, futures markets price in sustained premiums, although longer-term expectations point towards gradual normalization with prices returning below $80–$85 per barrel by later in 2026. This projected path combines market nervousness with balancing forces including potential OPEC+ production adjustments and emerging alternative supply routes. The uncertainty inherent in these forecasts calls for continuous monitoring given the rapid evolution of geopolitical developments.

Currency Exchange Rate Volatility Amid Escalating Energy Supply Risks in Early 2026

The acute energy supply uncertainties stemming from Strait of Hormuz tensions have rippled through currency markets, manifesting in heightened volatility particularly for oil-importing and emerging-market currencies. In Q1 and Q2 of 2026, currencies sensitive to oil price shocks—such as the Malaysian ringgit and certain Middle Eastern and Asian currencies—experienced downward pressure due to rising import costs and inflationary expectations. Concurrently, the U.S. dollar broadly strengthened as it remained the primary safe-haven currency amid global uncertainty and risk aversion.

This strengthens the feedback loop where inflationary pressures induced by energy price rises prompt tighter monetary policy or cautious stance by central banks, which in turn support the dollar's appreciation. Elevated exchange rate fluctuations complicate foreign exchange risk management for corporates and governments alike, amplifying the economic challenges of adapting to energy disruption. Traders and policymakers must account for these currency shocks in their contingency planning, recognizing that exchange rate volatility may further exacerbate inflation pass-through and impact trade balance dynamics during this heightened geopolitical risk period.

Building on the near-term outlook of price, inflation, and currency volatility, the following subsection will explore longer-term structural shifts arising from persistent geopolitical risks and evolving global energy transitions that could reshape commodity market fundamentals and trade routes beyond 2026.

Long-Term Structural Shifts: Energy Transition, Trade Route Evolution, and Middle East Economic Realignment

This subsection situates the near-term geopolitical-instability-driven oil price shocks within a broader long-term structural context. It evaluates how underlying shifts—particularly in renewable energy adoption, alternative trade route development, and regional economic diversification—intersect with and potentially mitigate risks posed by the Strait of Hormuz tensions. By assessing projected timelines for alternative infrastructure capacity, the accelerating energy transition, and evolving trade patterns, this analysis informs strategic planning beyond immediate crisis management toward sustainable resilience and geopolitical adaptation.

Projected Timelines and Constraints on Alternative Trade Route Capacity Expansion

While the Strait of Hormuz remains a critical chokepoint in the global oil supply chain, long-term resilience strategies increasingly emphasize development of pipeline and maritime alternatives. Currently, pipelines bypassing the Strait, such as those from Saudi Arabia and the UAE, collectively handle a limited share of total Strait traffic and face operational vulnerabilities including infrastructure susceptibility to drone attacks and geopolitical sabotage. Capacity expansion projects for alternative routes face significant lead times owing to complex engineering, financing hurdles, and regional insecurity. Accordingly, estimates indicate that meaningful capacity increases capable of offsetting full Hormuz disruptions are unlikely before the late 2020s, underscoring the ongoing strategic dependence on maritime transit through the Strait.

Moreover, maritime rerouting through longer passages such as around the Cape of Good Hope markedly increases shipping times and costs, limiting their practical utility as immediate substitutes. These physical and logistical constraints reinforce the immediacy of Hormuz-related risks in the medium term, even as strategic investments in bypass infrastructure continue.

Anticipated Renewable Energy Uptake and Its Interaction with Regional Hydrocarbon Dependency

Acceleration of renewable energy deployment, led by solar and wind technologies, is reshaping global energy demand profiles and holds potential to diminish long-run oil dependency. The Middle East has begun capitalizing on its substantial solar capacity and strategic geography to develop renewable energy infrastructure, integrating emerging low-carbon technologies such as green hydrogen production. However, this transition exhibits varying paces across states, constrained by infrastructure limitations, policy fragmentation, and economic reliance on oil revenues.

Importantly, renewable energy uptake is forecasted to reduce domestic hydrocarbon consumption gradually but will not fully supplant oil and gas export revenues in the near term. Current projections suggest that fossil fuels will remain economically significant to the region through the 2030s, extending the timeframe during which Strait of Hormuz stability remains critical. The coexistence of fossil fuels alongside renewables emphasizes the need for dual-track strategies balancing energy transition goals with immediate energy security imperatives.

Structural Impacts on Global Oil Consumption Patterns Driven by Sustained Instability and Energy Transition

Prolonged geopolitical instability around the Strait of Hormuz, combined with intensifying climate policies worldwide, is catalyzing structural shifts in global oil consumption. Major importers are pursuing diversified energy portfolios to mitigate risks associated with concentrated supply routes and exposure to price volatility. This evolving dynamic underpins a gradual decoupling of economic growth from oil consumption intensity through technological efficiency improvements, fuel substitution, and demand-side management.

Nonetheless, the multifaceted roles of petroleum—including its indispensable function as a feedstock for plastics, chemicals, and fertilizers—complicate rapid reductions in overall oil demand. Consequently, the sustained strategic importance of maintaining stable hydrocarbon exports persists, even amid transitions. Energy transition progress is thus modulating rather than eliminating the strategic risk premium that defines the global oil market's response to Strait of Hormuz tensions.

Climate Transition Effects on Middle East Energy Exports and Regional Economic Diversification

The imperative for climate-adaptive economic diversification in the Middle East is shaping long-term structural realignments. While hydrocarbon revenues remain central to fiscal budgets and social programs, governments increasingly invest in renewable energy projects and green infrastructure to hedge against the erosion of fossil fuel demand and price volatility.

Regional cooperation on energy transition policies, technological innovation adoption, and sustainable resource management is emerging as a critical enabler of resilience. The estimated expansion of low-carbon sectors, including hydrogen and solar exports, could reposition the Middle East as a future energy supplier beyond hydrocarbons. However, uneven progress among states and lingering dependence on oil exports pose persistent economic risks linked to global decarbonization timelines and policy environments.

These transitional dynamics will profoundly influence both the demand for Gulf oil exports through traditional corridors like the Strait of Hormuz and the regional geopolitical landscape, necessitating adaptive strategies that integrate climate and security considerations.

The long-term structural forces outlined here strongly condition the trajectory and effectiveness of mitigation strategies discussed subsequently. Understanding the evolving interplay between energy transition progress, trade route diversification, and regional economic transformation is essential for developing robust contingency plans and policy frameworks that address not only immediate risks but also sustain global energy security in a rapidly changing geopolitical and climatic environment.

5. Conclusion and Action Plan

Mapping the Economic Shockwaves: Quantifying Hormuz Disruption and Coordinated Global Responses

This subsection integrates the report’s analytical findings into a cohesive understanding of the economic vulnerabilities stemming from the Strait of Hormuz tensions and highlights the critical role of multilateral cooperation in formulating effective responses. By quantifying the economic impacts and detailing international coordination efforts, the section bridges diagnostic insights with actionable strategic priorities for stakeholders.

Quantifying the Economic Impact of Potential Strait of Hormuz Disruption

The Strait of Hormuz is a linchpin in the global energy supply chain, with approximately one-fifth of worldwide oil and liquefied natural gas exports transiting this narrow maritime corridor. Its disruption, whether partial or full, would cascade rapidly across multiple economic dimensions, manifesting first in global energy price volatility before spreading into inflationary pressures worldwide. Empirical modeling grounded in recent market behavior suggests that an extended closure could trigger oil price spikes surpassing 40% above baseline, amplifying transportation and manufacturing costs that directly feed into consumer price indices in major economies.

This inflationary shock would not be confined to energy-intensive sectors. The increased costs of fuel translate into elevated logistics and raw material expenses throughout global supply chains, especially in regions heavily reliant on Gulf energy exports. Central banks are already factoring these potential inflations into monetary tightening expectations, while energy-importing countries face balance-of-payment vulnerabilities. The resultant economic instability threatens to erode growth prospects, increase unemployment rates, and constrain fiscal space for public investments, underscoring the systemic nature of the risks posed by Hormuz tensions.

Coordinated International Action Plans: Frameworks for Stability and Security

In response to the strategic risks, a range of multilateral initiatives has been activated or proposed to stabilize the Strait of Hormuz and its surrounding geopolitical environment. These efforts include diplomatic backchannels among Gulf states and global powers aimed at de-escalating military postures and establishing maritime security protocols that guarantee uninterrupted transit. Furthermore, international organizations have called for enhanced surveillance mechanisms and cooperative frameworks emphasizing transparency and rapid conflict resolution to deter unilateral disruptions.

Institutional reforms emphasizing joint responsibility have been advanced to strengthen the resilience of global energy supply chains. These include collaborative investment in alternative infrastructure, crisis response coordination, and legal frameworks encouraging compliance with navigational rights. The collective recognition across involved states and bodies of the intertwined economic stakes reinforces the urgency for sustained dialogue and comprehensive approaches, integrating both short-term crisis management and long-term regional integration to safeguard stability. Such coordinated diplomacy represents the most viable pathway to mitigate the profound economic fallout from potential Hormuz bottlenecks.

Building on this synthesis of economic impacts and global coordination efforts, the report proceeds to define a clear implementation roadmap. This will detail phased actions and governance structures that operationalize these strategic priorities, enabling stakeholders to translate insights into effective mitigation and risk management.

Strategic Implementation Roadmap: Phased Actions, Stakeholder Roles, and Measurable Outcomes for Hormuz Security

This subsection delineates a concrete roadmap for implementing the strategic recommendations outlined in the report’s conclusion. It clarifies the sequencing of immediate and medium-term steps to stabilize the Strait of Hormuz, assigns clear responsibilities to key actors across the global governance landscape, and proposes quantifiable performance metrics. By bridging strategic insight with actionable frameworks, it equips decision-makers with pragmatic guidance essential for mitigating ongoing geopolitical and economic risks stemming from Hormuz tensions.

Phased Timeline for Immediate and Mid-Term Intervention Measures

The immediate priority is to stabilize maritime traffic and restore investor confidence through enhanced navigational security protocols and diplomatic de-escalation efforts. This includes rapid deployment of coordinated naval escorts and real-time maritime surveillance in the Strait, complemented by accelerated insurance risk assessments to moderate premium spikes. These urgent measures should be operational within the next 30 to 90 days to arrest further deterioration in trade flow and oil market volatility.

Concurrent with these near-term actions, the medium-term horizon—spanning 6 to 18 months—focuses on strengthening infrastructure resilience and institutional reforms. Upgrading alternative pipeline capacities and securing these critical supply routes against emerging threats such as drone attacks are integral to reducing chokepoint dependency. Simultaneously, concerted multilateral diplomatic initiatives must be institutionalized to foster conflict resolution and reinforce legal frameworks guaranteeing freedom of navigation under international law.

Defining Roles and Responsibilities Among Nation States, International Bodies, and the Private Sector

Nation states bordering the Gulf, notably Saudi Arabia and Iran, bear primary responsibility for regional security and the maintenance of navigational safety corridors. Their active cooperation and restraint are pivotal to preventing escalation and ensuring uninterrupted energy exports. The United States and allied defense coalitions have a strategic role in deterrence and rapid response capabilities, providing a security umbrella that underwrites stable maritime passage.

International organizations, including the United Nations, International Maritime Organization, and regional bodies such as the Gulf Cooperation Council, must steer diplomatic mediation, monitor compliance with international maritime law, and facilitate multilateral information-sharing mechanisms. These institutions also provide platforms for dialogue aimed at de-escalation and conflict prevention, reinforcing a rules-based order that underpins global energy security.

The private sector, particularly maritime insurers, shipping consortia, and energy companies, is tasked with implementing enhanced risk management protocols and investing in adaptive technologies. Collaborative public-private partnerships should be promoted to bolster cybersecurity, improve vessel tracking, and diversify supply chains to mitigate exposure to chokepoint disruptions.

Establishing Key Performance Indicators to Monitor and Evaluate Security and Economic Stability Outcomes

A robust performance measurement framework is essential for tracking the effectiveness of interventions aimed at stabilizing the Strait of Hormuz. Metrics should include maritime traffic volume normalization rates, reductions in insurance premium volatility, and frequency of security incidents such as vessel interdictions or attacks.

On the economic front, oil price stability indices and regional trade flow continuity indicators serve as proxies for the broader impact on global markets. Additionally, inflation trend analyses and central bank policy responsiveness offer insights into financial system resilience in the face of supply disruptions.

Institutional performance should be evaluated through diplomatic engagement frequency, progress in formal agreements safeguarding navigation rights, and adherence to international legal frameworks. Transparent public reporting of these KPIs will support accountability and facilitate informed policy recalibration.

With a clear roadmap integrating phased steps, accountable actors, and measurable outcomes, stakeholders can systematically address both immediate turmoil and build medium-term resilience. This framework paves the way for subsequent scenario modeling and contingency planning, enabling proactive adaptation to evolving geopolitical dynamics and economic conditions.

Conclusion

The 2026 developments in the Strait of Hormuz have starkly illuminated the strategic fragility inherent in global energy supply chains reliant on restricted maritime chokepoints. The precipitous decline in vessel traffic to less than 10% of pre-conflict levels has precipitated severe oil market volatility, substantial surges in transportation insurance costs, and significant inflationary ramifications extending well beyond the energy sector. Alternative pipelines, while valuable, fall short of fully offsetting the strait’s closure, reaffirming Hormuz’s irreplaceable role in sustaining global hydrocarbons flows.

The intricate geopolitical contest—rooted in regional power rivalries, strategic posturing, and proxy conflicts—continues to impede immediate resolution, even as multilateral initiatives and mediators progressively coalesce around innovative governance frameworks. Simultaneously, financial market dynamics, including investor flight to safe havens and algorithmic trading amplification, exacerbate price volatility, elevating systemic risk. These findings underscore the necessity of integrated approaches combining military de-escalation, diplomatic engagement, infrastructure resilience, and market risk management to stabilize both supply and economic systems.

Looking forward, near-term priorities must focus on reestablishing secure and predictable maritime operations through coordinated naval escorts, robust surveillance, and calibrated insurance mechanisms. Medium-term strategies should enhance pipeline capacities, strengthen cybersecurity defenses for energy infrastructures, and institutionalize multilateral maritime security protocols. Concurrently, sustained commitment to economic diversification and energy transition will moderate exposure over the longer term, reducing dependence on vulnerable chokepoints.

Ultimately, safeguarding the Strait of Hormuz demands a multidimensional response that aligns the interests of regional actors, global powers, international institutions, and private sector stakeholders. Transparent performance measurement and adaptive policy frameworks will be critical in tracking progress and fostering accountability. The lessons of the 2026 crisis serve as a clarion call to proactively bolster resilience against enduring risks that imperil global energy stability and economic prosperity.

References

- Saudi Arabia Monitors Hormuz Navigation Developments, Reaffirms Readiness to Protect Energy Supplies

- Geostrategic Analysis: April 2026 edition

- Strait of Hormuz Disruption 2026: Impact on Fuel Prices and Global Freight Costs

- The Global Costs of Instability in the Strait of Hormuz

- FM Cho urges safe navigation in Strait of Hormuz in phone talks with Iranian counterpart

- War in the Strait: How the Hormuz Crisis Is Shaking Global Energy Markets

- US-Israel Iran War Drives Oil Prices Above $100 Mark

- Strait of Hormuz and Global Oil and Gas Routes

- ‘Only country to have lost mariners’: India at Strait of Hormuz crisis meet

- China asks Iran to maintain safe navigation in the...

- Strait of Hormuz Closure: Global Impact and Inflation Risk

- Homeowners face higher mortgage rates as Donald Trump's Iran war hits FTSE 100 | The Standard

- Strait of Hormuz Crisis Disrupts Global Energy Markets

- Oil Prices Trigger Global Recession: $150 Barrel Risk

- Iran’s closure of the Strait of Hormuz is an international crisis | US-Israel war on Iran | Al Jazeera

- Alternative routes lack scale as Strait of Hormuz chokes

- Malaysia, a net oil importer, remains exposed to global price threats | KLSE Screener

- Strait of Hormuz Conflict Heightens Global Inflation and Recession Risks

- Strait of Hormuz Tensions Shake Markets, Impact Oil & Policy

- Strait of Hormuz Closure: Oil Prices Rise & Global Inflation Risks - World Today Journal

- New Iran-US tensions: Impact on Strait of Hormuz, oil

- The Economic Impact of U.S.–Iran Conflict on Middle East Markets

- Middle East geopolitical risk modestly affects inflation and inflation expectations

- Wang Yi: Ceasefire key to safe navigation in Strait of Hormuz - CGTN

- Hormuz Tensions: Impact on Maritime Insurance & Shipping Costs | Argus Media

- Q&A: Hormuz tensions put spotlight on marine insurance | Latest Market News

- Strait of Hormuz Tensions Raise Global Alarm Over Trade and Energy Supply

- PDF The Impact of the 2026 Iran War on U.S. Inflation: A Scenario Analysis

- With Hormuz choked, how does the world reroute — and what does that mean for Australia?

- The Multi-Layered Crisis in the Middle East

- A Strait, A Crisis, and $100 Oil: The Energy Shock Rippling Through Global Brands

- Why the Strait of Hormuz Matters to the Global Economy in 2026

- Strait of Hormuz Crisis Pressures Global Energy Trade

- Oil Price Forecast: WTI Near $120 as Strait of Hormuz Tensions Drive Breakout

- Hormuz Tensions Fuel Oil Price Rally

- The Strait of Hormuz: A Critical Chokepoint for Global Energy Security | Ambassador Dr. Ausaf Sayeed

- darpa

- PDF 1 Cybersecurity Investment Priorities - The White House

- UNDER SECRETARY OF DEFENSE

- PDF Analysis of the President's FY 2026 Budget Request

- The cyber winners and losers in Trump’s 2027 budget

- CISA’s vulnerability scans, field support on chopping block in Trump budget | Cybersecurity Dive

- Trump wants to take a battle axe to CISA again and slash $707M from budget

- FY 2026 EPA Budget in Brief

- DOE Sets 5-Year Plan to Harden US Grid Against Cyberattacks

- judiciary information technology fund

- PDF Climate Change Mitigation and Adaptation: The Legal Framework

- PDF The International Organization for Standardization

- Drug-Resistant Infections: A Threat to Our Economic Future

- PDF 100 Years of Drug Control.indb

- Forced Labour and Forced Marriage

- PDF 2023 G20 New Delhi Summit Final Compliance Report

- STRATEGIC PLAN 2021 - 2024

- Summary for Policymakers — Global Warming of 1.5 ºC

- IMO Financial Statements 2023.pdf

- Global Economy at a Crossroads: IMF Urges Action on Inflation, Debt, and Reforms | Other

- PDF Oil Markets in Focus Given Middle East Turmoil

- West Asia war: Impact of disruptions on global fuel supply, with potential for coal and n-power switch

- Iran closes Hormuz again over US blockade

- the strait of hormuz and its importance in middle east and ...

- Chokepoints under pressure: The fragile lifelines of global energy | Hellenic Shipping News Worldwide

- The Strait of Hormuz: Geography, Strategic Importance, and the Current Crisis