Unraveling Extended Lead Times in Smartphone Production: Causes, Impacts, and Strategic Responses Amid Semiconductor Supply Challenges

Table of Contents

- Executive Summary

- Introduction

- 1. Understanding the Semiconductor Shortage and Its Origins

- 2. Component-Specific Delays and Manufacturing Bottlenecks

- 3. Structural Vulnerabilities in the Semiconductor Supply Chain

- 4. External Disruptions and Material Constraints

- 5. Cascading Effects on Production Costs and Market Dynamics

- 6. Regional Variations and Global Market Implications

- 7. Improvement Options and Mitigation Strategies

- Conclusion

Executive Summary

This report presents a comprehensive analysis of the prolonged lead times currently affecting smartphone production worldwide, driven primarily by systemic constraints in the semiconductor supply chain. Key findings reveal that semiconductor foundries, notably TSMC’s 3nm capacities, are fully booked through 2026 due to surging demand from AI-driven applications, limiting chip availability for smartphone manufacturers. Memory shortages persist with DRAM and NAND prices escalating by up to 95% quarter-over-quarter in early 2026, contributing to a projected 7-15% decline in global smartphone shipments through mid-2026. Labor disruptions, such as Samsung’s 18-day May 2026 strike, alongside geopolitical disruptions like Zimbabwe’s lithium export ban and Middle East helium shortages, further exacerbate production delays and cost inflation.

Regional disparities accentuate lead time variability, as China benefits from accelerated polysilicon plant construction while US and EU facilities face prolonged permitting delays extending timelines by up to 18 months. Strategic adaptations by major smartphone makers—Apple prioritizing premium models with compressed lead times and Samsung scaling back mid-range launches—restructure production schedules amid these constraints. Mitigation strategies centered on digital collaboration, supplier quality management, and diversified sourcing demonstrate potential lead time reductions of 10-30%, offering actionable pathways to enhance supply chain resilience under continuing global uncertainty.

Introduction

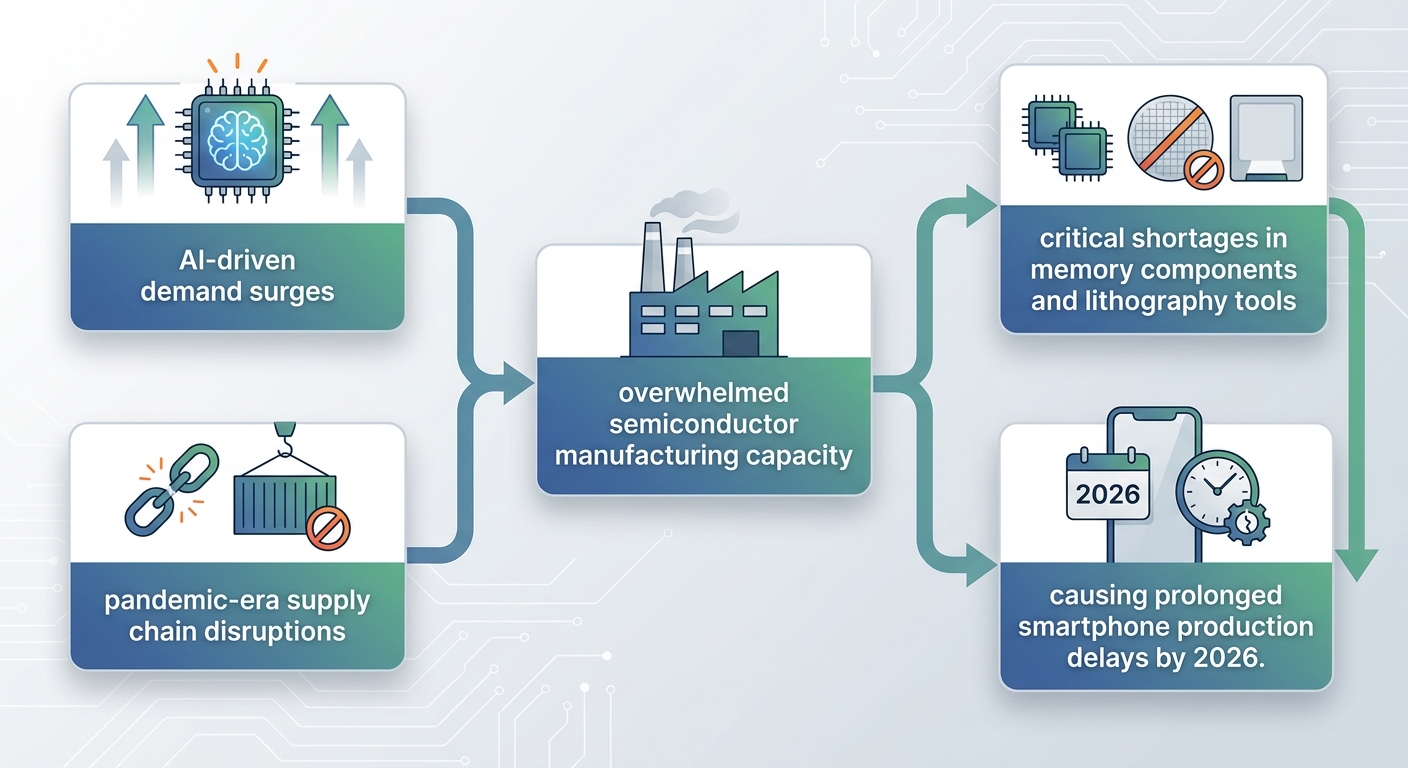

In an era marked by rapid technological advancement and escalating consumer demand, the smartphone industry confronts unprecedented challenges manifested in sharply extended production lead times. These delays disrupt not only manufacturing schedules but also market availability and pricing structures, compelling stakeholders to reassess operational paradigms. At the heart of these lead time elongations lie multifaceted disruptions in the semiconductor supply chain, which forms the foundational backbone of modern smartphone hardware.

The origins of current supply constraints are deeply rooted in the COVID-19 pandemic era, where initial demand collapses were followed by rapid rebounds, unanticipated surges in consumer electronics consumption, and fragile inventory practices. Compounding these dynamics, the meteoric rise of artificial intelligence applications has redirected semiconductor capacity priorities toward data-center demands, severely limiting availability for consumer-grade devices. Simultaneously, labor disputes, geopolitical upheavals, and raw material export restrictions have introduced further volatility into critical component availability and production continuity.

The purpose of this report is to dissect the underlying causes driving extended lead times in smartphone production, quantifying impacts on shipment volumes, component costs, and competitive market positioning. Additionally, the report explores structural vulnerabilities in the semiconductor ecosystem, highlighting regional disparities in manufacturing infrastructure deployment. Finally, it outlines emerging strategies and technological innovations designed to mitigate delays and bolster supply chain agility, offering a roadmap for industry stakeholders navigating a protracted period of supply-demand imbalance.

Infographic Image: Infographic

1. Understanding the Semiconductor Shortage and Its Origins

Pandemic-Era Disruptions as the Catalyst for Semiconductor Supply Shocks

This subsection establishes the initial conditions that triggered the semiconductor shortage impacting smartphone production. By dissecting the specific pandemic-induced supply chain disruptions and operational responses, it sets the foundation for understanding the protracted lead times observed in subsequent manufacturing stages.

Quantifying the Early Pandemic Semiconductor Demand Collapse and Its Implications

At the onset of the COVID-19 pandemic, semiconductor manufacturers faced an unprecedented contraction in orders. Many original equipment manufacturers drastically curtailed their semiconductor procurement in anticipation of declining consumer demand, particularly during the first half of 2020. This initial reduction reached double-digit percentages in some sectors, translating to significant idle capacity in foundries and component plants.

This early decline created a pronounced mismatch between supply and demand when, contrary to expectations, the appetite for consumer electronics—especially smartphones and remote work technologies—surged later in 2020. This caused tremendous strain on manufacturing resources as the semiconductor supply chain was unprepared for the swift rebound.

Factory Closures and Labor Shortages Among Upstream Suppliers Exacerbating Production Delays

Pandemic-related health measures induced temporary closures, quarantines, and labor shortages across critical tiers of the semiconductor supply chain. Many upstream suppliers, including raw material providers and component manufacturers, suspended operations for weeks or even months. This disruption had cascading effects downstream, reducing overall semiconductor production capacity over an extended period.

Given the intricate multi-tier supplier networks in semiconductor manufacturing, even minor delays at key upstream nodes amplified lead times at assembly and packaging facilities. Furthermore, efforts to maintain social distancing and enhanced sanitation protocols diminished operational throughput at remaining facilities, creating persistent bottlenecks.

The Breakdown of Just-In-Time Inventory Practices and Its Role in Extending Lead Times

Just-in-time (JIT) production and inventory management, a widely adopted strategy to minimize working capital, proved fragile in the face of pandemic shocks. With prolonged shipping delays and sudden order fluctuations, the lean inventory buffers that manufacturers depended upon rapidly emptied.

Consequently, firms scrambled to build inventory cushions, leading to over-ordering and a surge in freight demand. These reactions, while intended to stabilize supply, further stressed logistics networks and semiconductor availability, expanding lead times significantly. This systemic fragility highlighted the lack of resilience inherent in JIT models when confronted with multi-dimensional disruptions.

Having established how the pandemic's early impact disrupted semiconductor supply chains and operational practices, the following subsection will explore how escalating demands—particularly driven by emerging technologies—magnified capacity constraints, perpetuating extended lead times in smartphone production.

AI-Driven Demand Surges and the Strain on Foundry Capacities

This subsection explores how the rapid growth of artificial intelligence applications has sharply intensified demand for the most advanced semiconductor technologies, particularly at the 3nm node. It elucidates how leading smartphone and tech companies have secured sizeable manufacturing capacity at top foundries, thereby contributing to sustained bottlenecks and lengthened lead times in smartphone production. The analysis also includes the operational realities faced by Chinese foundries, which are running beyond nominal capacity, further underscoring systemic capacity constraints that extend beyond Taiwan’s dominant suppliers.

TSMC’s 3nm Capacity Pre-Booking by Leading Device Makers

Taiwan Semiconductor Manufacturing Company (TSMC), the world’s leading semiconductor foundry, has experienced unprecedented booking of its 3-nanometer production capacity through 2026 and beyond. Major technology companies including Apple, Qualcomm, NVIDIA, and AMD have reserved nearly all available slots for the 3nm node, reflecting its critical role in powering next-generation smartphones and AI computing devices. This tight reservation status means that opportunistic customers without advance contracts face extremely limited access to cutting-edge 3nm chips, significantly constraining the semiconductor supply available for smartphone manufacturers.

TSMC’s advanced 3nm process is distinguished by higher wafer costs, reported to be approximately 25% above the prior 5nm node, which combined with supply constraints amplifies the pricing power of the foundry. In response to soaring demand, TSMC has been reallocating some 5nm equipment capacity to increase 3nm output and is aggressively investing in new production lines in Taiwan, the United States, and Japan. However, these expansions will not reach operational maturity until 2027 or later, prolonging the capacity shortage in the near term and contributing directly to longer lead times in semiconductor procurement for smartphone makers.

Capacity Utilization and Operational Overload at Chinese Foundries

Chinese foundries such as Hua Hong Semiconductor play a pivotal role in supplying mature and specialty semiconductor nodes that are integral to a broad swath of smartphone components. These foundries have been operating at or beyond 100% capacity utilization rates, a feat that often entails running additional shifts and stretching equipment lifecycles to meet demand. This sustained overload environment reflects significant systemic constraints where incremental scale-up is constrained by capital intensity and long qualification cycles for new capacity.

The 100%+ utilization rate at Hua Hong Semiconductor not only indicates peak operating conditions but also forebodes looming price adjustments, as the supply-demand imbalance tightens further. These conditions signal that domestic Chinese foundries are also intensifying price and delivery pressures on smartphone component supply, compounding difficulties manufacturers face even as they wrestle with global capacity shortages at advanced nodes.

Forecast and Duration of Foundry Capacity Shortfalls

Advanced foundry capacity shortages are projected to persist at least through 2026, with well-documented full-booking status at leading foundries reinforcing this outlook. TSMC’s expansion plans, including new 3nm production lines in Taiwan, the U.S., and Japan, are scheduled to come online predominantly in 2027 and 2028. Until these expansions materialize, the rampant demand for AI-optimized chips, alongside traditional smartphone processors, continues to place sustained strain on fabrication facilities.

Industry analyses caution that the current supply-demand mismatch will prolong elevated lead times across the semiconductor supply chain. The constraint is further exacerbated by the long lead times intrinsic to new fab construction and equipment installation, as well as qualification cycles that prevent rapid absorption of surges in demand. Consequently, smartphone manufacturers reliant on the newest nodes face lead times stretching many months, as chip supply is rationed among flagship device producers and AI-specialized component customers.

Having established the immense pressure advanced-node foundries face due to AI-driven demand surges and widespread capacity saturation—including both TSMC’s booked-out 3nm capacity and Chinese foundries’ operational overload—the subsequent section will analyze how these factors translate into component-specific bottlenecks and elevated production costs that directly impact smartphone manufacturing timelines.

2. Component-Specific Delays and Manufacturing Bottlenecks

Critical Memory Component Shortages and Escalating Cost Pressures in Smartphone Production

This subsection delves into the acute shortages of memory components—primarily DRAM and NAND chips—that have become a pivotal bottleneck in smartphone manufacturing. It quantifies how these constraints extend production lead times, drives up costs, and restructures supply priorities. Understanding these dynamics is essential to apprehend why smartphone shipments in early 2026 continue to fall short of demand forecasts, despite ongoing capacity expansion efforts within the broader semiconductor landscape.

Quantifying DRAM Shortage Effects on Smartphone Shipments into Mid-2026

Smartphone manufacturers face prolonged lead times attributable to persistent DRAM shortages, which have materially contracted device production volumes. Industry projections indicate that the tight supply of memory components will extend delays beyond the first quarter of 2026, suppressing global smartphone shipments further into the second quarter. Estimates point to an expected year-over-year decline in smartphone production volumes ranging from 7% to 15% in 2026, reflecting ongoing supply chain challenges tied directly to memory scarcity.

This impact disproportionately affects mid- to low-tier Android device manufacturers, who lack vertical integration in memory chip production and thus have limited leverage in capacity allocation negotiations. Conversely, integrated manufacturers with both memory fabrication and device assembly capabilities, such as Samsung, demonstrate relative resilience to these shortages, maintaining steadier shipment levels despite overall market contraction.

Recent and Projected Memory Chip Price Volatility and Implications on Component Costs

Memory chip prices have experienced unprecedented volatility through late 2025 and early 2026, with contract prices for DRAM modules surging by approximately 80% to 90% quarter-over-quarter in early 2026. For instance, the average price of a 16GB DDR5 module increased from around $72 in late 2025 to nearly $120 by the first quarter of 2026, with forecasts suggesting potential escalation to $168 by year-end. This rapid price inflation has multiplied the memory content share within the smartphone bill of materials from an industry baseline of about 10-15% up to 30-40% in some segments.

The steep component cost ramp translates directly into higher retail pricing for smartphones. Leading manufacturers have responded with price increases of roughly 14-15% on average across flagship and premium models, as seen in recent launches such as Samsung’s Galaxy S26 series. Price hikes are broad-based but particularly impactful on devices geared toward cost-sensitive consumers, where memory cost increases can comprise up to a third of the total production cost escalation.

AI Sector Memory Demand Prioritization Over Smartphones and Its Supply Chain Signal

The surge in AI applications has fundamentally altered memory demand priorities within the semiconductor ecosystem. High-bandwidth memory (HBM) and other specialized DRAM variants essential for AI inference and training workloads consume large portions of available production capacity, prompting wafer fabs and memory manufacturers to prioritize AI data-center orders over consumer electronics. This reallocation reduces available supply for conventional DRAM and NAND chips used in smartphones, exacerbating shortages.

This technology-driven demand pivot has created a structural shift where data centers now consume over 60% of the memory chip output, with projections suggesting this share could approach 70% by 2026. Consequently, memory suppliers concentrate capacity on the higher-margin AI segment, effectively limiting the volume of memory chips allocated for smartphone production and prolonging manufacturer lead times. Additionally, AI-driven memory demand intensifies price pressure, as premium memory types command elevated pricing and reduce the pool of chips suitable for mobile devices.

Having established the critical role memory shortages and cost pressures play in constraining smartphone production, the report will next examine how delays in manufacturing equipment procurement and challenges in facility expansion further compound production lead times.

Extended Lead Times in Lithography Equipment and Facility Development: Regional Disparities and Qualification Challenges

This subsection investigates the critical delays embedded in the procurement and installation of lithography equipment as well as the construction and ramp-up of semiconductor fabrication facilities. By analyzing regional construction lead times and qualification cycles, it provides a granular understanding of a core bottleneck contributing to longer smartphone production lead times. This analysis frames how technological dependencies and regulatory environments slow capacity expansions essential for meeting escalating chip demand.

Regional Construction Timelines for Polysilicon and Fab Facilities: China’s Advantage Versus Western Delays

The construction lead times for polysilicon manufacturing plants, foundational upstream facilities in semiconductor supply chains, vary significantly across regions, directly impacting downstream chip availability. Plants in China typically take between 12 and 18 months to construct, which is markedly shorter than the 24 to 40 months commonly required in the United States and European Union. These disparities arise from less cumbersome permitting, streamlined land acquisition processes, and more centralized regulatory oversight in China. Additionally, Chinese facilities benefit from accelerated ramp-up phases, reaching full production capacity within months of completion, whereas Western plants often experience protracted ramp-up durations due to stricter environmental and operational compliance requirements.

Downstream segments such as ingot and wafer plants have somewhat more consistent development times internationally, typically spanning 12 to 18 months. However, assembly segments like cell and module factories generally demand shorter lead times, between 3 to 12 months, with regional gaps being less pronounced. The cumulative effect of extended upstream plant lead times in Western countries bottlenecks overall semiconductor throughput, delaying component delivery to smartphone manufacturers reliant on these segments.

Regional construction differences are quantitatively underscored by a comparative lead time average of approximately 15 months in China versus 32 months in both the US and EU for polysilicon plants, highlighting how China's significantly shorter construction cycle enhances its upstream semiconductor capacity readiness relative to Western counterparts [Chart: Regional Construction Timelines for Semiconductor Facilities].

Procurement and Installation Cycles for Lithography Tools: The Multi-Year Challenge

Lithography tooling, especially extreme ultraviolet (EUV) systems essential for cutting-edge semiconductor production, impose among the longest lead times in chip manufacturing value chains. Production cycles for these highly specialized machines span multiple years due to their extreme technical complexity and the geographic concentration of manufacturers, primarily within the Netherlands and Japan. Lead times for advanced lithography tools range typically from 18 to 30 months, including the manufacturing, shipment, installation, and calibration phases.

Following physical installation, equipment undergoes a rigorous qualification and process-matching period to ensure consistent yield and performance. This calibration and qualification stage often takes an additional 12 to 24 months, during which production volumes incrementally increase as process parameters stabilize. The cumulative procurement-to-full-production cycle for leading-edge lithography equipment can, therefore, exceed three years. The geographic distribution of these vendors means that politically sensitive export controls, especially those affecting China, add further uncertainty and delay for some manufacturers attempting to source such tools.

In less advanced lithography segments (e.g., deep ultraviolet or immersion lithography), procurement cycles are somewhat shorter, yet still measured in excess of one year. The dominance of a handful of suppliers creates a natural bottleneck, constraining the pace at which new fabs can be equipped even if physical construction timelines are compressed.

Qualification Processes for New Semiconductor Fabs: A Deliberate and Lengthy Ramp-Up

After facility construction and equipment installation, semiconductor fabs undergo an intensive qualification process to achieve mass-production readiness. This includes sequential design qualification, installation qualification, operational qualification, and performance qualification. Each phase verifies that the facility and tools conform to stringent design specifications and can produce chips meeting quality and yield standards reliably.

The overall fab qualification lifecycle averages between 12 and 24 months, depending on the complexity of the technology node and the type of chips being produced. High-end logic and memory device fabs typically require the upper end of this spectrum due to the precision and repeatability standards demanded.

These qualification delays introduce a nonlinear dynamic in capacity expansion: significant capital expenditure and construction effort must be committed years before any effective output contributes to supply. Any disruptions or shortcomings detected during qualification necessitate iterative corrective measures, further elongating timelines. Additionally, the high qualification burden discourages frequent switching of equipment vendors and creates substantial switching costs, thereby slowing the industry’s ability to rapidly diversify and augment production capacities.

The prolonged timelines associated with lithography tool procurement and fab qualification, alongside regional disparities in facility construction speed, establish critical chokepoints that exacerbate delayed semiconductor availability. These factors, when compounded with increasing demand surges, extend lead times for critical components within smartphone manufacturing. Subsequent sections delve into the systemic supply chain vulnerabilities and external challenges that further amplify these delays.

3. Structural Vulnerabilities in the Semiconductor Supply Chain

Risks of Supplier Concentration: How Dominance Extends Lead Times

This subsection assesses the structural vulnerability arising from heavy supplier concentration in the semiconductor foundry market, predominantly exemplified by one major manufacturer. It explores how this dominance translates into longer lead times and magnifies the impact of disruptions on smartphone production timelines.

Consequences of Near-Monopoly Foundry Market Share on Production Delays

The semiconductor foundry market is heavily concentrated, with a single company commanding close to 70% of global pure-play foundry capacity. This dominant share delivers operational efficiencies and economies of scale under stable demand but inherently creates systemic risks when capacity constraints or geopolitical tensions arise. The sheer volume of orders funneled through this single supplier amplifies queueing effects, thereby extending lead times for advanced-node chip fabrication essential to smartphones.

Production schedules become highly sensitive to fluctuations in this company's capacity utilization rates. When demand surges outpace expansion capabilities, the lead times for wafer supply can increase by several months. This phenomenon is particularly consequential given the complexity of modern chip fabrication, which involves multi-year investment cycles in fabrication plants and equipment. Consequently, smartphone manufacturers reliant on this supplier face cascading delays that shift project timelines well beyond initial forecasts.

Real-World Disruptions Illustrate Timeline Extensions from Supplier Fragility

Historical and recent incidents at key semiconductor production facilities highlight how the concentration of supply induces production bottlenecks for smartphones. For example, unplanned labor strikes at major foundries have paused wafer processing, causing backlogs that ripple through the supply chain and delay subsequent assembly stages significantly.

Geopolitical tensions have further exacerbated this fragility. Heightened trade disputes and regional instability affecting the dominant foundry’s home base have led to precautionary order acceleration by customers, creating artificial capacity tightness. Additionally, disruptions among essential upstream suppliers of niche materials or specialty chemicals can halt entire fabs, as qualifications for alternative sources typically require several months, underscoring the ecosystem's limited redundancy.

Such single points of failure translate directly into extended lead times for smartphone manufacturers, often measured in weeks to months, depending on the duration and severity of the incident. These delays reduce manufacturing agility and complicate product launch planning in an already competitive market.

Having established how supplier concentration magnifies lead time risks through dominant capacity control and ecosystem fragility, the report next examines the compounding effect of slow supplier substitution cycles and the limited flexibility within semiconductor supply chains.

Protracted Supplier Qualification and Capacity Challenges Undermine Supply Chain Agility

This subsection delves into critical causes behind the semiconductor supply chain's inflexibility, focusing on the lengthy supplier qualification durations and the constrained capacity of alternate sources. Understanding these factors clarifies why manufacturers cannot quickly switch suppliers or scale production, thereby aggravating lead time extensions in smartphone manufacturing.

Extended Supplier Qualification Processes Incur Months-Long Delays

The semiconductor industry's supplier qualification timelines represent a fundamental contributor to production lead time elongation. Incoming suppliers must undergo rigorous qualification procedures involving comprehensive testing, audit of manufacturing capabilities, and product validation within client systems. These processes typically range from four to twelve months, with some critical or safety-related components requiring up to a year or more for full qualification. This timeframe encompasses multiple phases, including initial assessments, sample evaluation, pilot runs, and ongoing validation cycles prior to approval for volume manufacturing.

Such protracted qualification cycles introduce a structural inertia within supply networks, as manufacturers face significant barriers to onboarding new vendors rapidly in response to shortages or disruptions. The complexity and technical specificity of semiconductor components, combined with stringent performance and reliability demands, impede streamlined qualification. Additionally, any change in component specification or manufacturing technology may reset qualification, causing further delays. This systemic latency reduces supply flexibility, locking manufacturers into existing supplier relationships and amplifying the impact of capacity bottlenecks when disruptions occur.

Capacity Saturation at Alternative Suppliers Limits Rapid Switching Potential

Even if manufacturers seek to diversify suppliers to mitigate risk, the feasibility of rapid switching is constrained by the high utilization rates across existing semiconductor producers. Many alternative suppliers are operating near or at full production capacity, leaving limited room to absorb sudden increases in order volume. This capacity saturation is particularly acute for advanced memory components and cutting-edge process nodes, where fabrication facilities are heavily booked for AI and data-center related demand.

The lead times for scaling additional capacity are further exacerbated by the multi-year horizon required for facility construction and equipment installation. Therefore, shifting volume away from bottlenecked suppliers cannot be accomplished through volume reallocation alone. Instead, it requires extended planning and capital investment cycles. Moreover, production ramp-up at new sources must coincide with necessary supplier qualification, compounding delays. As a result, semiconductor supply chains display significant rigidity, with insufficient spare capacity or rapid substitution options to accommodate demand fluctuations or supply interruptions effectively.

These capacity and flexibility challenges contribute to expected year-over-year declines in smartphone production volumes, with forecasts predicting drops ranging from 7% to 15% in 2026, largely driven by ongoing supply constraints including memory shortages that amplify lead time issues across the ecosystem [Chart: Predicted Decline in Smartphone Production Volumes in 2026].

Fragmented Supply Chain Silos Impede Integrated and Agile Responses

Beyond capacity and qualification constraints, functional silos within semiconductor supply chains further hamper agility. There is often poor cross-functional integration among procurement, manufacturing, engineering, and quality assurance teams, resulting in slow decision-making and delayed responses to emergent supply risks. Communication gaps and data fragmentation hinder rapid visibility into supplier status and available alternatives.

This disjointed coordination limits proactive risk mitigation, as contingency supplier qualification and volume allocation plans are not fully synchronized. The lack of collaborative development models between chipmakers and component vendors contributes to a reactive rather than prospective posture toward supply disruptions. Addressing these systemic organizational weaknesses is essential to reduce substitution cycle times and enhance flexibility across the semiconductor supply network.

Having established how prolonged qualification periods and capacity saturation at alternate sources restrict semiconductor supply flexibility, the following sections will further investigate how external disruptions and material constraints compound these structural vulnerabilities, creating cascading delays throughout the smartphone production ecosystem.

4. External Disruptions and Material Constraints

Labor Strikes Threatening Production Continuity and Supply Chain Reliability

This subsection examines how labor unrest, particularly the impending strike actions at a leading memory chip manufacturer, directly disrupts smartphone production lead times. It connects production delays to workforce dynamics, quantifies potential volume impacts, and highlights the recurrent nature of labor disputes in semiconductor manufacturing, thereby elucidating a critical external disruption layer affecting lead times.

Impact of the May 2026 Samsung Strike on Semiconductor Output and Global Supply Chains

Samsung Electronics is facing an unprecedented labor strike spanning 18 days from late May to early June 2026, a magnitude and duration never before seen in the company's history. This strike threatens to idle approximately half of Samsung's semiconductor production capacity at its key Pyeongtaek facility, the world's largest memory chip fabrication complex. Given Samsung's cornerstone role in the global supply of DRAM and NAND flash memory, such a prolonged halt could generate immediate and severe shortages, disrupting supply chains beyond South Korea and affecting smartphone manufacturers worldwide.

The timing is particularly critical as Samsung simultaneously ramps up production for the Galaxy S26 Ultra smartphone and other high-demand consumer electronics. Production stoppages during this interval risk delaying component shipments, escalating lead times, and forcing downstream manufacturers to adjust inventory buffers and launch schedules. Analysts forecast that any disruption of even a few days could cascade into multi-week delays in smartphone assembly lines, as alternative memory chip sources have constrained capacity and cannot quickly compensate for Samsung's shortfall.

Moreover, the strike's anticipated ripple effect includes tightening supply and upward pressure on DRAM and NAND prices, potentially increasing manufacturing costs and further complicating production planning for smartphone makers already contending with component shortages and geopolitical supply risks. Contract prices for DRAM modules have surged approximately 80-90% quarter-over-quarter in early 2026, sharply inflating the bill of materials and adding cost pressures to smartphone production during this critical period [Chart: DRAM Price Increase Trends From 2025 to 2026].

Frequency, Duration, and Escalation Patterns of Labor Disputes in 2026

The May strike follows an earlier three-day labor walkout scheduled in July 2026, underscoring a pattern of recurrent workforce disruptions. The union negotiations have deteriorated over disagreements encompassing wage increases, performance bonus caps, and profit-sharing mechanisms, exacerbated by Samsung's record-setting financial performance in early 2026. This environment has emboldened union members, with over 93% voting in favor of the May strike, reflecting deep-rooted dissatisfaction and a collective willingness to engage in extended industrial action.

Short-term stoppages earlier in the year did impact chip output and shifted production schedules, indicating that even limited labor disruptions can meaningfully stretch lead times. As the company anticipates potential further strikes, the risk of iterative interruptions poses ongoing uncertainty for component delivery timelines, necessitating continuous reassessment of supply chain resilience and contingency buffers by smartphone manufacturers.

The repeated scheduling of labor actions during peak production phases weakens the predictability of supply chain flows, compelling downstream partners to adopt risk mitigation strategies such as increased inventory holdings or alternate sourcing, both of which inherently extend lead times and add cost.

Adjustment of Inventory Buffers and Production Scheduling Amid Labor Disruptions

Manufacturers typically react to strike-induced production halts by increasing inventory buffers to cushion against supply variability. However, the scale and timing of the May 2026 strike strain this approach, as chip inventories deplete rapidly amid strong AI-driven demand, limiting the extent to which inventory can absorb shocks without inducing further lead time extensions.

To manage scheduling resilience, production planners must incorporate extended lead times for memory components, recalibrate just-in-time delivery parameters, and prioritize critical model assemblies. This results in elongated development and ramp-up cycles, particularly for mid-tier smartphone models where cost and timing pressures are pronounced.

The uncertainty over strike duration and the potential for escalation also necessitates conservative scheduling policies, delaying final assembly orders and increasing production cycle variability. Such operational adjustments reinforce the systemic nature of labor disruptions in prolonging smartphone production lead times beyond the direct strike period.

While labor strikes cause immediate and direct impacts on semiconductor output and smartphone assembly timelines, these disruptions often intersect with broader material constraints and geopolitical tensions. The following subsection explores how geopolitical conflicts and raw material restrictions compound supply challenges and further extend production lead times.

Geopolitical Conflicts Driving Raw Material Supply Shocks and Production Delays

This subsection examines how escalating geopolitical tensions, particularly involving key raw material suppliers, have led to significant disruptions in the availability and delivery of critical semiconductor inputs. By quantifying the lead time extensions resulting from export restrictions and analyzing the impact of material shortages—such as helium and lithium—on semiconductor production processes, this analysis reveals underlying mechanisms by which global conflicts exacerbate smartphone manufacturing delays.

Lead Time Extensions from Zimbabwe’s Lithium Export Restrictions

Zimbabwe’s recent and indefinite ban on the export of raw lithium and lithium concentrates has introduced pronounced supply chain bottlenecks that directly extend lead times for battery module production integral to smartphones. The ban, implemented ahead of the initially planned 2027 timeline, also suspended shipments already in transit, intensifying immediate supply disruptions. As the world’s fourth-largest lithium producer, Zimbabwe’s export limitations remove a critical feedstock from the global market, with notable dependence from China, which receives nearly one-fifth of its lithium supply from Zimbabwe.

The restriction’s downstream impact propagates through a multi-tiered supply chain and results in delivery delays extending well beyond standard procurement buffers. Inventory adjustments at lithium compound producers occur within days, but renegotiations and contract revisions at cell manufacturers add roughly one to two weeks. Battery module assemblers, operating with rigid production cycles, face additional delays ranging from two to four weeks. Cumulatively, these constraints can extend lead times by approximately eight to twelve weeks, significantly affecting smartphone production schedules that rely on just-in-time component deliveries.

Helium Shortage and Its Impact on Semiconductor Manufacturing Capacities

Helium, a critical and irreplaceable gas in semiconductor fabrication processes such as wafer cooling, inert atmosphere maintenance, and equipment stabilization, is increasingly affected by geopolitical conflicts centered in the Middle East. The ongoing war involving Iran, Israel, and the United States has caused intermittent halts in helium production and disrupted shipping routes through the Strait of Hormuz, one of the primary transit points for LNG-derived helium supplies, especially from Qatar, which produces over one-third of the global supply.

While the helium market operates under long-term contracts and inventories have cushioned short-term shocks, persistent conflict threatens longer-term supply stability. Semiconductor fabs, especially in memory chip manufacturing concentrated in South Korea and Taiwan, face escalating operational risks, including potential slowdowns or partial production shutdowns if helium availability deteriorates further. Current logistics constraints, including transportation delays and container shortages, compound the issue beyond raw availability, transforming helium into a logistics and supply reliability bottleneck. These factors contribute to delays in chip production timelines, thereby indirectly extending lead times in smartphone manufacturing reliant on these chips.

Middle East Conflict's Broader Influence on Semiconductor Material Costs and Supply Chains

The Middle East conflict has not only disrupted raw material supplies but has also precipitated sharp increases in critical semiconductor-related material costs. Prices for helium have surged by over 50%, while petrochemical precursors such as PGMEA and solvents including ethanol and isopropyl alcohol have experienced price pressures driven by escalating oil prices and constrained supply chains. These cost increases inflate manufacturing expenses throughout the semiconductor ecosystem, further complicating production schedules and financial planning.

Additionally, the conflict’s indirect effects—rising energy costs and heightened geopolitical uncertainty—add operational burdens to fabs and chipmakers, tightening margins and potentially limiting investments in capacity expansions. Although immediate production shutdowns have been avoided due to strategic stockpiles and diversified suppliers, persistent instability raises the risk of prolonged delays that ripple into the global smartphone supply chain. The combined effect results in longer component procurement cycles, elevated input costs, and reduced flexibility, which cumulatively contribute to the extended lead times currently experienced in smartphone production.

Understanding the depth and breadth of these geopolitical and material supply disruptions frames the broader challenges faced by smartphone manufacturers. These external shocks compound internal supply chain vulnerabilities and amplify component-specific bottlenecks, necessitating adaptive strategies to mitigate extended lead times explored in subsequent sections.

5. Cascading Effects on Production Costs and Market Dynamics

Escalating Memory Prices and Their Direct Impact on Smartphone Costs in Early 2026

This subsection investigates the magnitude and dynamics of memory component price surges in the first half of 2026 and quantifies their direct repercussions on the bill of materials (BoM) for smartphones. Understanding these cost escalations is critical to contextualizing production challenges and pricing pressures faced by manufacturers, particularly as they vary across device tiers and regions.

Unprecedented DRAM and NAND Price Increases in Q1 and Q2 2026

Memory chip prices, particularly DRAM and NAND flash, experienced extraordinary quarter-over-quarter increases in early 2026, with DRAM prices soaring by approximately 90-95% in Q1 alone. This steep upward trajectory continued into Q2, where an additional increase of 30-60% was projected, positioning 2026 as a period of unprecedented market tightness and sustained cost inflation. The surge is largely driven by prioritization of high-performance memory production for AI applications, constraining supply for consumer-grade components.

Such sharp price escalations have transformed the memory market into a seller’s environment, where supplier leverage is at an all-time high. Market reports highlight the persistent undersupply and the absence of new capacity adequate to meet this demand until late 2027 or 2028, further entrenching the price momentum in the near term.

Substantial Increases in Smartphone Bill of Materials Attributable to Memory Costs

Memory components have become a dominant factor in smartphone production costs, making up over 15% of the total bill of materials for many devices. Price hikes of 40-50% reported in late 2025 accelerated steeply through Q1 2026, pushing memory's share of BoM significantly higher. In entry-level smartphones priced below $200 wholesale, memory now accounts for an estimated 43% of BoM costs, illustrating the disproportionate burden on budget devices.

Mid-range smartphones are projected to see growing memory cost shares, reaching approximately 20% for DRAM and 16% for NAND flash by Q2 2026. Premium flagship devices, characterized by high-capacity memory configurations such as 16GB LPDDR5X RAM combined with 512GB UFS storage, are forecast to face BoM cost increases in the range of $100 to $150 per unit by mid-2026. These figures underscore that even devices at the high end of the market are experiencing material cost inflation significant enough to influence retail pricing.

Regional and Segment-Specific Variations in Cost Pressure and Price Inflation

The inflationary pressures from memory shortages are unevenly distributed across global markets and smartphone segments. Regions with high concentrations of low-end smartphone sales, such as the Middle East, Africa, China, and parts of Asia Pacific, are forecast to experience the steepest declines in shipments driven by escalating prices. For instance, localized price increases of 15% in the Indian market during Q1 2026 reflect both component cost surges and currency fluctuations, severely impacting affordability in sub-$200 segments.

Pricing strategies have diverged by brand and segment: premium manufacturers like Apple and Samsung have absorbable margins and have implemented selective pricing and production prioritization strategies to mitigate cost shocks while preserving market share. In contrast, budget and mid-tier brands face existential challenges, with many compelled to either reduce memory specifications or pass on price increases, squeezing demand and contributing to shipment declines of up to 12-15% in affected markets.

Having delineated how sharply rising memory prices in early 2026 have augmented smartphone production costs and altered pricing dynamics across market segments and regions, the report proceeds to analyze how these cost pressures are reshaping manufacturer priorities and product strategies in the face of constrained supply and evolving market demand.

Strategic Production Focus and Deliberate Launch Delays Reshape Smartphone Lead Times

This subsection examines how leading smartphone manufacturers, particularly Apple and Samsung, strategically adjust their production priorities and product launch schedules in response to component scarcity and rising costs. These decisions directly influence lead times across product tiers, revealing a deliberate trade-off between focusing resources on premium models while delaying or scaling back volume-driven segments. Understanding these dynamics is essential for comprehending the complex factors extending overall production timelines in the current market environment.

Apple’s Prioritization of Premium Models Compresses Lead Times for Flagship Production

Apple’s 2026 production strategy centralizes resources around premium devices, notably the iPhone 18 Pro, Pro Max, and the highly anticipated foldable iPhone. Component scarcity, especially memory chips, has driven Apple to allocate critical inputs preferentially to these high-margin products, compressing lead times for flagship models by consolidating supply chain focus. This selective concentration enables Apple to maintain a stringent schedule for premium device ramp-up despite overall industry constraints.

Conversely, Apple has implemented a deliberate delay for the standard iPhone 18 and its budget counterpart, shifting their launches into early 2027. This postponement strategically frees capacity and mitigates supply pressure for high-end model production. While this approach lengthens lead times for entry-level and mid-range devices, it aligns with Apple’s goal of maximizing profitability and sustaining premium market momentum during constrained supply conditions.

The foldable iPhone’s release remains narrowly on track for fall 2026 but faces compressed testing and validation timelines. Engineering complexities inherent in this novel form factor introduce additional risks of further delays, amplifying lead time extension on this segment. By channeling investment and production priority to the foldable and Pro series, Apple effectively reshapes the production calendar, lengthening cycles for lower-tier models but protecting flagship availability and quality.

Samsung’s Mid-Range Production Cutbacks and Their Impact on Lead Times and Shipments

Samsung’s launch schedule for 2026 demonstrates a contrasting but equally strategic adaptation to component shortages and elevated costs. The Galaxy S26 flagship series experienced launch delays early in the year, which depressed cumulative shipments in initial quarters. Despite this, Samsung leveraged its premium offerings’ strength, with the Galaxy S26 series generating a significant rebound in sales post-launch and outperforming its predecessor in key markets.

However, Samsung’s mid-range refresh cycle faced deliberate scaling back and postponements, reflecting an effort to conserve constrained memory supplies for flagship models where margins are higher. This selective launch strategy extends lead times for lower-tier and Fan Edition devices, with anticipated releases shifted into later months or even beyond Q3 2026. The delay of the Galaxy S26 FE exemplifies this trend, pushing its market availability to fall or later, thus prolonging the full portfolio’s production timeline.

The mid-range cutbacks have tangible market consequences; Samsung’s overall shipments declined year-over-year due to postponed releases and weaker demand in entry and mid-tier segments. While the Galaxy S26’s premium segment performs robustly, the uneven production prioritization inflates lead times and reduces volume in more price-sensitive categories, reinforcing a wider trend of stretched production schedules across the industry.

Financial Trade-Offs and Margin Preservation Through Selective Launches Lengthen Development Cycles

Both Apple and Samsung navigate a complex economic landscape shaped by surging component prices and supply constraints. Their selective production approaches balance the imperative to preserve profit margins with the operational challenges of extended lead times. Concentrating chip allocations to premium devices enables these manufacturers to absorb elevated bill-of-materials while maintaining price stability in core profitable segments.

This strategy translates into longer development and production cycles for budget and mid-range smartphones. Apple’s delaying of the standard iPhone 18 and Samsung’s deferred refresh of mid-tier models result in slower product introduction cadence, effectively stretching the time-to-market for less lucrative segments. While this preserves margins and mitigates supply risks, it also risks weakening competitive positioning in volume-driven tiers.

Overall, the selective launch focus reflects a deliberate trade-off: manufacturers accept lengthening timelines for entry-level and mid-tier products as a cost of safeguarding flagship performance, sustaining brand prestige and financial health amid an industry-wide semiconductor shortage. These extended development cycles contribute significantly to the broader phenomenon of increasing lead times in smartphone production.

Timeline Extensions and Market Implications of Postponed Lower-Tier Smartphone Launches

The delay of lower-tier and standard models is not just a scheduling inconvenience but a structural shift in production timelines. Industry sources indicate that Apple’s entry-level iPhone launch may be deferred by up to six months, creating a bifurcated release cycle that pushes many budget product deliveries into the first half of 2027. Samsung mirrors this pattern with staggered launches for mid-range devices, further elongating the overall product development horizon.

These shifts ripple through global supply chains as prolonged schedules require longer component stocking and assembly lead times. The extension of the development and launch window disrupts traditional annual refresh rhythms, complicates inventory management, and forces manufacturers and retailers to recalibrate marketing and inventory strategies. Consequently, consumers may face lengthened wait times, and price sensitivity in these segments could erode demand elasticity.

This protracted rollout schedule underscores a broader market recalibration wherein suppliers, contract manufacturers, and OEMs align to a new norm of selective prioritization and extended lead times, with lower-tier models becoming the most affected in terms of availability and timing.

Having detailed how Apple’s and Samsung’s deliberate production prioritizations and strategic delays affect lead times and product availability, the report now turns to assessing the resulting financial impact on production costs, pricing, and overall market dynamics. Understanding these economic consequences is essential for framing the broader implications of prolonged smartphone manufacturing timelines.

6. Regional Variations and Global Market Implications

Regional Lead Time Disparities in Semiconductor Manufacturing and Their Impact on Smartphone Production

This subsection elucidates the critical regional differences in semiconductor facility construction timelines with a focus on contrasting China’s accelerated manufacturing capabilities against the protracted processes in the US and Europe. Understanding these disparities provides insight into how upstream delays in semiconductor fabrication cascade down to lengthen smartphone production lead times globally, affecting supply chains and market responsiveness.

Lead Time Differences: China’s Accelerated Polysilicon and Wafer Plant Construction Compared to US and EU

New polysilicon manufacturing plants, a foundational segment of semiconductor production, display wide variance in lead times across regions. In China, construction and ramp-up of such plants typically range from 12 to 18 months, markedly shorter than the 30 to 40 months seen within the European Union and United States. This advantage is driven by streamlined permitting processes, streamlined land acquisition, and concentrated government support.

For wafer, cell, and module plants, regional disparities are less pronounced but still significant. While China achieves deployment within a 3 to 6-month window, the same facilities in US and EU markets frequently require 9 to 12 months due to increased regulatory scrutiny and more complex infrastructure requirements. Consequently, China’s faster build-out cycles facilitate more rapid scaling of semiconductor supply capacity, alleviating component bottlenecks earlier than competitors in Western markets.

Permitting and Land Acquisition Delays Extend US and EU Semiconductor Facility Timelines

Protracted regulatory environments in the US and Europe significantly inflate semiconductor facility development timelines. Permitting procedures in these regions involve comprehensive environmental impact assessments, public consultations, and layered governmental approvals, which can add between 6 to 18 months to initial construction estimates. Land acquisition complexities, including property negotiations and zoning challenges, further exacerbate these delays.

These administrative and legal hurdles restrict manufacturers’ ability to initiate projects swiftly in response to market demands. The cumulative effect is a bottleneck in expanding critical manufacturing infrastructure, creating persistent supply capacity deficits that slow the downstream production of semiconductor-dependent goods like smartphones.

How Regional Construction Lead Time Variability Translates into Extended Smartphone Manufacturing Lead Times

The elongated construction and ramp-up cycles characteristic of US and EU silicon manufacturing facilities directly impact the availability of semiconductor components essential for smartphones. In contrast to China’s earlier capacity expansions, Western manufacturers face prolonged equipment commissioning schedules, which delay chip production increases needed to satisfy growing demand.

These upstream delays propagate through the smartphone supply chain, extending lead times for critical components such as processors and memory chips. As a result, global smartphone manufacturers sourcing from US and EU foundries must accommodate longer planning horizons and buffer inventories, negatively affecting responsiveness to market shifts. Conversely, capacity scaling in China enables more agile supply chain replenishment, providing competitive advantages to manufacturers leveraging Chinese semiconductor outputs.

Moreover, geopolitical disruptions, such as helium shortages and lithium export restrictions, have been projected to add lead time extensions of approximately 3 and 8 weeks respectively to semiconductor manufacturing processes, further compounding these regional disparities and prolonging component availability delays globally [Chart: Estimated Lead Time Extensions Due to Geopolitical Events].

Having established how regional disparities in semiconductor facility lead times contribute to delays in component availability, the analysis now proceeds to examine the broader market implications, including shipment declines and evolving competitive dynamics among smartphone manufacturers.

Declining Smartphone Shipments and Market Consolidation Amid Component Constraints

This subsection elucidates the quantifiable contraction in global smartphone shipments during early 2026, highlighting brand-specific performance divergences and underlying component-driven supply constraints. It reveals how memory shortages and lead-time disruptions have reshaped market dynamics, culminating in shipment declines and altered competitive positioning among key players. This insight is indispensable for understanding how component availability directly influences industry volume trends and strategic shifts within the global smartphone ecosystem.

Quantifying Global and Brand-Specific Smartphone Shipment Declines in Early 2026

The global smartphone industry experienced a notable contraction in market volume during the first quarter of 2026, with total shipments falling approximately 4.1% year-over-year to around 290 million units. This downturn marks the first significant shipment decline since mid-2023 and reflects mounting pressures from constrained component supplies and geopolitical uncertainties. Notably, only two major vendors expanded their shipment volumes during this period, underscoring the uneven impact across the competitive landscape.

Samsung emerged as the largest shipper in Q1 2026, achieving roughly 63 million units, which translates to a 3.6% increase year-over-year. This was driven primarily by strong demand for its premium Galaxy S26 Ultra and the continued popularity of its mid-range A-series devices. Meanwhile, Apple closely followed with shipments of approximately 61 million units, up 3.3% year-over-year, propelled by robust demand for the iPhone 17 and effective supply chain execution that mitigated component bottlenecks.

In contrast, other leading players encountered sharp shipment declines. Xiaomi, for example, suffered nearly a 19% year-over-year decrease, while Oppo and Vivo reported declines in the range of 7-10%. These declines were largely attributable to their more pronounced exposure to memory chip shortages, pricing pressures, and weaker consumer sentiment in key markets.

Detailed Market Share Changes and Competitive Shifts Between Apple and Samsung

Apple achieved a historic milestone in early 2026 by securing the top global smartphone market share for the first time in a first quarter, capturing approximately 21% of worldwide shipments. This surpassed Samsung’s roughly 20% share, a noteworthy shift given Samsung’s longstanding leadership position. Apple's market share growth was underpinned by its ultra-premium positioning, cohesive supply chain integration, and targeted growth in high-potential markets, particularly China, where the iPhone 17 series recorded a 23% sales increase within the opening nine weeks of the year.

Samsung’s market share contraction, despite volume growth, reflected competitive challenges within its entry-level and mid-tier device segments, which were disproportionately affected by memory shortages and delayed product launches. Its Galaxy S26 flagship received favorable traction but was insufficient to offset softness in lower-tier categories. Consequently, Samsung’s year-over-year shipments declined about 6%, illustrating the pressure to balance portfolio breadth with constrained component supply.

These divergent trajectories between Apple and Samsung underscore how supply chain resilience, strategic product prioritization, and market focus can drive competitive advantage amid systemic supply challenges.

Linking Component Shortages and Extended Lead Times to Shipment Declines and Market Consolidation

The contraction in smartphone shipments across most market segments can be directly traced to persistent shortages of critical memory components such as DRAM and NAND flash. These shortages stem from supply prioritization toward AI data center demands, which have escalated lead times and inflated component costs. Manufacturers incapable of securing sufficient memory supply faced production constraints, forcing reductions in device output and shipment volumes.

Extended component lead times in combination with rising raw material and logistics costs have compelled many smartphone OEMs to rationalize their model portfolios and delay lower-tier product launches. This approach disproportionately affected volume-driven brands reliant on aggressive mid-range and entry-level segments, thereby accelerating market consolidation favoring players with premium device portfolios and stronger supply chain control.

The elevated cost structure resulting from memory chip price surges—reportedly rising by approximately 90% quarter-over-quarter in early 2026—also pressured consumer demand by pushing up retail prices. The compounded effects of supply constraints and price elasticity resulted in slower end-market adoption, reinforcing the observed volume declines. Premium brands like Apple, leveraging supply chain agility and ecosystem lock-in, have better mitigated these pressures, while others experienced more significant shipment contractions.

Having established the direct correlation between component shortages, shipment declines, and market share shifts, it is critical to contextualize these phenomena within regional manufacturing lead-time disparities and the broader global supply landscape. The following subsection will delve into how geographic differences in production timelines and regulatory environments further influence smartphone production and market outcomes.

7. Improvement Options and Mitigation Strategies

Harnessing Digital Collaboration to Break Functional Silos and Accelerate Lead Times

This subsection explores how digital collaboration models serve as a strategic lever to overcome entrenched functional silos in smartphone production supply chains. It examines concrete evidence of digital integration enhancing cross-functional coordination and client involvement, thereby reducing lead times. Positioned within the broader improvement strategies section, the analysis highlights the transformative impact of collaborative, digitally enabled product and service development on time to market and supply chain responsiveness.

Evidence of Lead Time Reductions via Digital Collaborative Product Development

Manufacturers facing elongated lead times have increasingly turned to digital and collaborative product development frameworks as a remedy to systemic fragmentation across functions. Empirical studies report that integrating continuous customer engagement within product cycles enables more adaptive design iterations, translating to shorter development times. This approach leverages digital platforms to maintain sustained interaction with end users, allowing rapid feedback incorporation, and prevents costly rework downstream.

Quantitative impact assessments from pilot initiatives in analogous manufacturing contexts show a typical reduction of time-to-market by approximately 20-30%. One longitudinal study of multi-organizational innovation ecosystems demonstrated that ecosystems with well-governed digital collaboration platforms accelerated product deployment by over 30%, while concurrently lowering innovation risk through shared investments. This acceleration was attributed to improvements in process connectivity and data exchange efficiencies enabled by digital tools.

Furthermore, these collaborative models reduce functional silos by fostering transparency and information flow between development, procurement, and manufacturing teams. Enhanced cross-functional coordination ensures early identification and mitigation of bottlenecks, improving schedule adherence and material readiness. The dynamic integration made possible by digital collaboration hence directly addresses the delays introduced by traditional siloed workflows.

Quantifiable Benefits from Digital Collaboration Pilots: Time Savings and Efficiency Gains

Pilot programs employing digital collaboration technologies provide measurable evidence of improvements relevant to lead times. In these pilots, coordinated use of cloud-based platforms, real-time data sharing, and joint decision-making tools led to a 40% increase in knowledge sharing efficiency and a 39% reduction in transaction costs related to partner coordination. These efficiency gains, as reported in multi-sector innovation ecosystems, highlight how digital collaboration enables quicker resolution of ambiguities that otherwise delay production flows.

Digital platforms also facilitate customer co-creation processes by enabling firms to integrate user-generated data seamlessly into design iterations. This capability not only customizes products more precisely to market needs but also reduces the iteration cycle duration. Trials showed that early and ongoing customer participation supported by digital tools shortened feedback loops by over 25%, directly impacting lead times.

Moreover, the incorporation of continuous digital workflows allows organizations to better synchronize supplier capacities with in-house production schedules, minimizing idle times and avoiding late-stage procurement surprises. This synchronization is critical in smartphone manufacturing, where components such as semiconductors and memory modules require precise timing to prevent cascading delays. Hence, digital collaboration tools serve as enablers of both strategic alignment and operational agility.

Building upon the demonstrated efficacy of digital collaboration models in compressing production timelines, the subsequent subsection will explore essential operational practices such as supplier quality management systems, which complement digital strategies by fortifying supply chain robustness and further mitigating lead-time risks.

Implementing Supplier Quality Management to Streamline Lead Times and Enhance Supply Chain Reliability

This subsection explores the critical role of Supplier Quality Management (SQM) systems in mitigating extended lead times within smartphone manufacturing. Positioned within the broader discussion on improvement options and mitigation strategies, it provides a fact-based analysis of how robust supplier oversight and quality frameworks directly contribute to shortening delivery cycles and elevating product quality. By examining precise operational benefits and implementation pathways, this section informs decision-makers of actionable strategies to boost supply chain resilience amid ongoing production challenges.

Quantifying Impact: How SQM Drives Lead Time Reduction and Supplier Responsiveness

Empirical data consistently demonstrates that adopting Supplier Quality Management systems leads to measurable improvements in supplier lead times and responsiveness. By tracking the time suppliers take to fulfill orders—from placement to delivery—and monitoring their responsiveness to queries and issue resolution, SQM creates accountability and transparency in supply chain interactions. These factors enable manufacturers to reduce uncertainties and buffer stock requirements, thus shortening overall production cycles.

Studies within high-complexity industries show that structured supplier evaluation processes, including audits and performance certifications, help identify suppliers most capable of meeting stringent quality and timing standards. This prequalification reduces the risk of delays caused by quality defects or material shortages, directly impacting lead time variability. Moreover, SQM fosters improved communication flows and collaborative problem-solving which further enhance supply reliability.

A recurrent theme in lean procurement initiatives is the positive correlation between SQM implementation and reduced procurement cycle times. By eliminating non-value-adding activities and enforcing process standardization, manufacturers have reported lead time reductions ranging from 19% to 24%, sustained over multi-year periods. These gains are attributed to tighter integration of supplier workflows and mechanisms that empower suppliers to proactively identify and resolve bottlenecks.

Strategic Implementation: Key Steps and Best Practices for Effective SQM Deployment

Successful SQM deployment hinges on clearly defined objectives aligning quality improvement with business goals, such as defect reduction and delivery time enhancement. The process begins with robust supplier evaluation protocols incorporating comprehensive audits, certifications review, and financial stability assessments. Such diligence ensures a reliable supplier base that minimizes disruptions and improves predictability in components arrival.

Ongoing monitoring of key performance indicators—including on-time delivery rates, defect ratios, and lead time variability—is essential to sustaining supply chain improvements post-implementation. Implementing digital tools and e-business strategies facilitates real-time data exchange and enhances connectivity across tiers, further optimizing procurement efficiency and supplier collaboration. This integration supports just-in-time production models critical for reducing inventory carrying costs and lead times.

Manufacturers are encouraged to adopt continuous improvement philosophies within SQM frameworks. Embedding feedback loops allows early detection of quality issues and operational inefficiencies, empowering cross-functional teams to implement corrective measures promptly. This dynamic approach cultivates supplier partnerships grounded in transparency and shared accountability, leading to progressively shorter lead times and enhanced product quality over time.

Performance Outcomes: Statistical Evidence Linking SQM to Improved Supply Chain Metrics

Quantitative outcomes from SQM adoption reveal substantial improvements in supply chain reliability metrics central to smartphone manufacturing efficiency. Lead time variability indicators show marked reduction as manufacturers engage in detailed procurement data analysis and supplier performance tracking. These gains translate into smoother inventory turnover and enhanced ability to meet fluctuating customer demand.

Cost efficiency is another major benefit, with lean procurement principles integrated into SQM frameworks driving waste elimination and process streamlining. This approach has yielded measurable savings through decreased inventory holding and reduced expedited shipping needs resulting from late deliveries or quality failures.

Case studies highlight that supplier responsiveness, a key component of SQM, directly correlates with improved fill rates and fewer production stoppages. Enhanced communication supported by digital platforms amplifies these benefits, enabling just-in-time delivery alignment and lower operational risk. Collectively, these improvements contribute to shortening development and production timelines, offering manufacturers a critical competitive advantage amid pervasive supply chain uncertainty.

Having established the substantial benefits and practical steps for effective Supplier Quality Management implementation, the discussion will next explore complementary mitigation strategies—such as digital collaboration models and diversified sourcing—that collectively enhance supply chain robustness and further curtail lead times.

De-Risking Through Diversified Sourcing: Mitigating Lead Time Volatility in Smartphone Production

This subsection examines the critical strategy of sourcing diversification as a means to alleviate prolonged lead times in smartphone manufacturing. By analyzing the tangible impacts of geographic and supplier base diversification, it highlights how manufacturers can enhance supply chain resilience, reduce production delays, and buffer against geopolitical and capacity-driven disruptions. This evaluation directly informs actionable mitigation pathways discussed later in the strategic recommendations section.

Quantifying Lead Time Improvements via Geographic Supply Diversification

Geographic diversification of semiconductor and memory production is increasingly recognized as an essential approach to reduce dependency on single regions, which are often subject to regulatory, logistical, or geopolitical disturbances. Expanding manufacturing footprint across multiple countries or continents helps mitigate risks of localized disruptions that can cascade into prolonged component shortages and manufacturing bottlenecks.

Recent industry data reveal that firms with diversified supply chains experience measurably shorter lead times during periods of heightened volatility. For instance, the establishment of new high-bandwidth memory and DRAM facilities by leading manufacturers in South Korea and the United States is projected to alleviate supply pressures by mid to late 2027, offsetting deficits concentrated in historically dominant Asian hubs. This gradual shift broadens capacity access and enables buffer lead time reductions of several weeks to months for critical components compared to mono-regional sourcing strategies.

Moreover, geographic diversification can alleviate bottlenecks stemming from export restrictions or trade conflicts by allowing alternate routes for raw materials and finished components. This elasticity in logistics and production flexibility directly translates into more predictable and compressed procurement cycles, supporting faster iteration in smartphone assembly stages.

Impact of Diversified Supplier Base on Smartphone Production Delays

Beyond geographic spread, broadening the supplier base itself plays a crucial role in enhancing responsiveness and minimizing lead time variability. A more diverse array of approved and qualified suppliers enables manufacturers to adapt swiftly to supplier-specific disruptions, fluctuating yields, or surges in component demand without halting or postponing production lines.

However, diversification must overcome inherent industry challenges: the qualification process for new sources typically spans multiple months and demands extensive testing to ensure yield stability and quality standards. In the highly specialized smartphone component ecosystem, alternative suppliers often face capacity constraints themselves, limiting their ability to function as immediate backups.

Despite these obstacles, investments into supplier qualification and cultivating multi-sourcing capabilities yield meaningful improvements. Companies adopting this strategy report reductions in average component procurement lead times by approximately 10-20%, and markedly lower risks of full stoppages triggered by single-supplier failures. Consequently, this enables smartphone manufacturers to better synchronize inventory buffers, improve production schedules, and reduce the incidence of time-consuming emergency sourcing or product launch delays.

It is also important to note the competitive pressure on memory availability due to shifting demand priorities in the industry. Memory suppliers are increasingly allocating about 70% of production capacity to high-margin AI data center applications, limiting the share available for smartphone production to around 20%. This reallocation constrains memory supplies critical to smartphones, adding urgency to diversification strategies and the need for supply chain agility to mitigate resultant lead time risks [Chart: Memory Demand Segmentation by Sector (2026)].

Building on the demonstrated benefits of supply chain diversification, the subsequent subsections will explore complementary strategies, including enhanced digital collaboration and supplier quality management, to further streamline production and mitigate lead time challenges.

Conclusion

The comprehensive examination of extended lead times in smartphone production reveals a confluence of structural, operational, and external factors that collectively challenge industry agility. Foremost among these is the semiconductor supply crunch, where capacity at advanced nodes remains saturated through at least 2026, driven by the dual pressures of AI-related chip demand and constrained memory availability. The concentration of manufacturing capabilities in a handful of suppliers, coupled with protracted facility qualification cycles and geopolitical tensions, creates systemic fragility. Labor disruptions, raw material export bans, and regional infrastructure disparities further compound delays and elevate production costs.

These supply constraints have tangible market ramifications, manifesting in notable declines in global smartphone shipments, shifts in brand market shares favoring premium manufacturers with robust supply chain integration, and escalating bill-of-material costs that undermine affordability in entry- and mid-tier segments. Strategic production prioritization by leading OEMs, such as Apple’s focus on flagship devices and Samsung’s scaling back of mid-range refreshes, exemplify adaptive responses that, while safeguarding profitability, may recalibrate market dynamics and consumer accessibility.

Looking forward, the pathway to mitigating extended lead times involves embracing digital collaborative platforms to dismantle functional silos, instituting rigorous supplier quality management frameworks to enhance predictability, and pursuing diversified geographic sourcing to reduce vulnerability to localized disruptions. Investments in accelerated construction and qualification of manufacturing facilities—particularly in regions with streamlined regulatory environments—are critical to expanding future capacity. Ultimately, an integrated approach combining technological innovation, supply chain transparency, and proactive risk management is requisite to restore resilience and support sustainable smartphone production amid ongoing global supply uncertainties.

References

- Apple leads fastest consumer electronics ramp-up, tops PLI

- The Rise of Memory Chip Prices and Their Impact on Major Tech Companies | Value The Markets

- PDF Special Report on Solar PV Global Supply Chains - .NET Framework

- Trade facilitation, market size, and supply chain efficiency of Taiwan semiconductor companies

- PDF Glocalisation in Manufacturing: Redesigning Supply Chains

- Comparative Advantage, Technology and Labor Demand

- Smartphone Market – Size, Share, Trends, Analysis & Forecast 2026–2035 2025-2034 | Size,Share, Growth

- AI's Chip Appetite Is Squeezing The Global Smartphone Market— Analysts Warn Of 31% Shipment Slump Ahead

- Annual Financial Report

- Supplier Quality Management: A Complete Guide